Quick Navigation

Report Overview

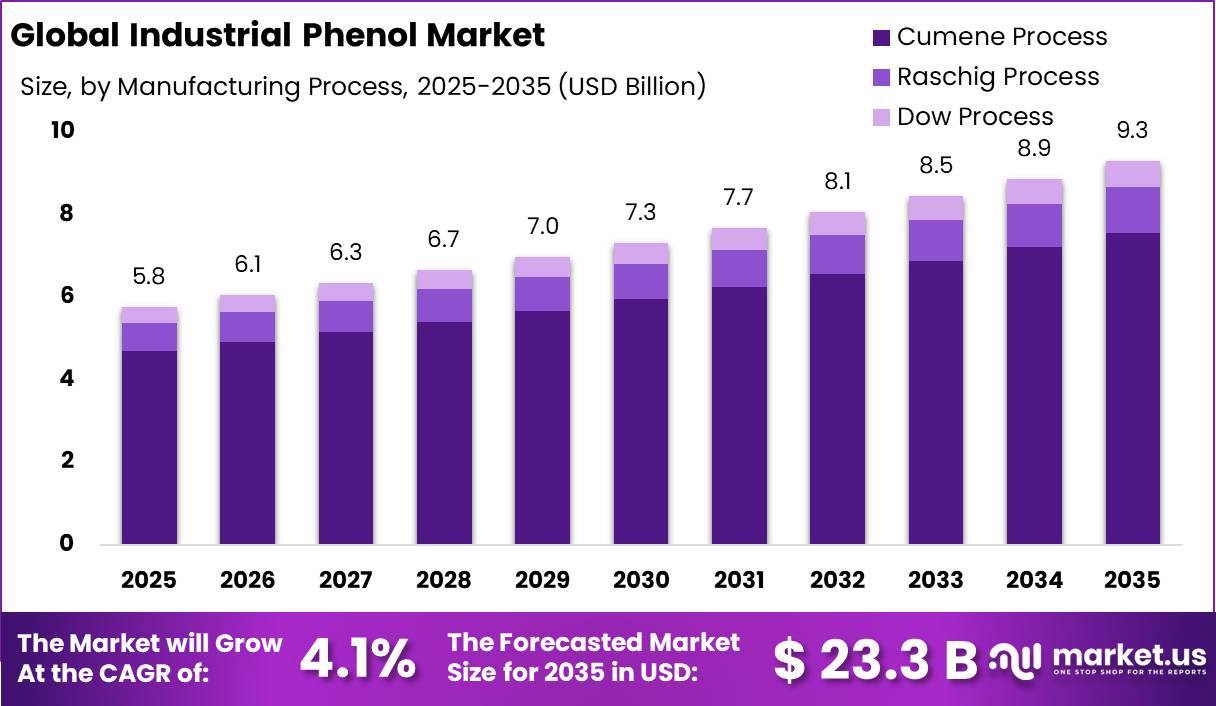

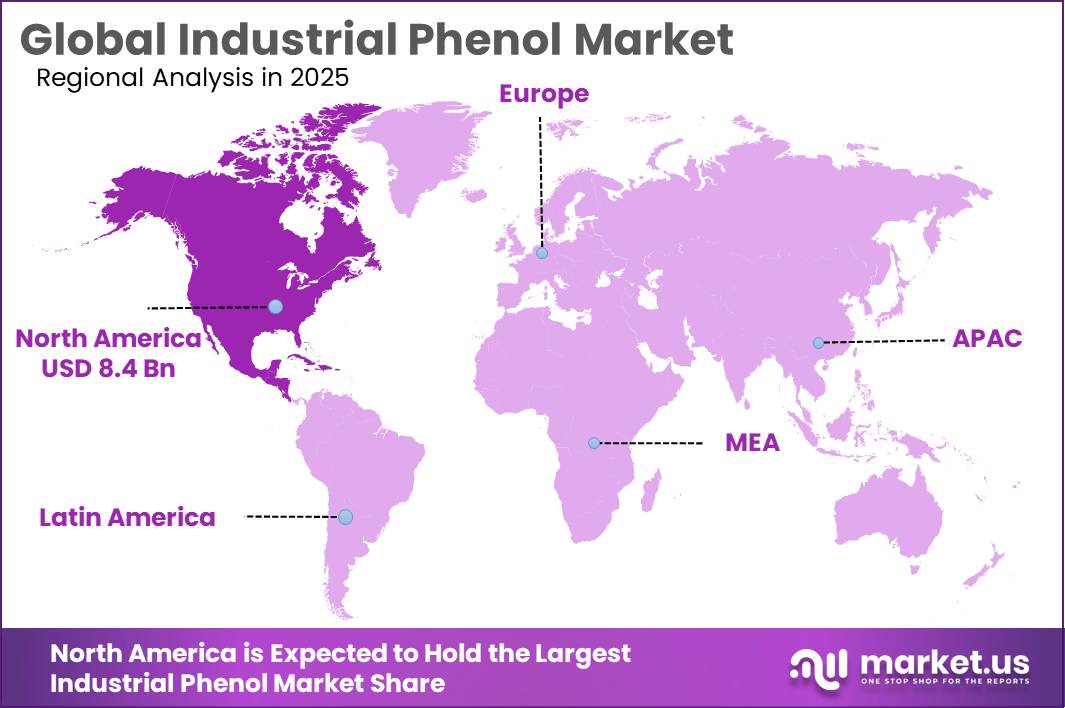

The Global Industrial Phenol Market size is expected to be worth around USD 23.3 Billion by 2035, from USD 15.6 Billion in 2025, growing at a CAGR of 4.1% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 54.20% share, holding USD 8.4 Billion revenue.

Industrial phenol is positioned as a strategic intermediate for bisphenol A, polycarbonate plastics, epoxy resins, phenolic resins, coatings, laminates and engineering materials. Its industrial relevance is supported by BPA consumption, as NIEHS states that BPA is produced in large quantities mainly for polycarbonate plastics and epoxy resins, while CDC NHANES detected BPA in 93% of 2,517 U.S. urine samples, showing the scale of downstream material exposure and use. In the U.S., reported aggregated phenol production volume was 2.5 billion to under 4.0 billion lb in 2023, confirming its large-scale industrial base.

The industrial scenario remains linked to construction, electronics, mobility, coatings, packaging, wind-energy composites and high-performance plastics. Covestro, formerly Bayer MaterialScience, reported €14.2 billion group sales and €1.1 billion EBITDA in 2024, while its Performance Materials segment generated €7.0 billion sales, indicating the continuing industrial base for polycarbonate and related phenol-chain materials. Under EU REACH, substances manufactured or imported at 1 tonne/year or more must be registered, and the U.S. EPA’s Chemical Data Reporting system generally applies from 25,000 lb/site thresholds, reinforcing compliance-driven operations.

Driving factors include demand for lightweight durable plastics, epoxy coatings, thermal insulation, electronics housings, automotive parts and renewable-energy composite systems. Policy support is also emerging: the European Commission’s chemical transition pathway covers more than 150 actions across 26 topics, notes that chemicals are present in about 95% of manufactured goods, and reported that around 80% of 187 transition actions had been launched. Covestro, formerly Bayer MaterialScience, remains relevant through BPA/polycarbonate chains; its Solutions & Specialties segment recorded €6,621 million sales in fiscal 2025, showing the scale of high-performance polymer demand even under pricing pressure.

Government initiatives are increasingly shaping future growth. In July 2025, the European Commission introduced a Chemicals Industry Action Plan targeting high energy costs, unfair global competition, weak demand, innovation and sustainability. These measures may support more resilient phenol chains through energy-cost relief, circularity, cleaner production and protection of strategic chemical manufacturing.

Aditya Birla Chemicals is positioned through advanced materials and epoxy systems; its official site describes the business as one of the world’s major epoxy resin manufacturers serving global markets. In June 2025, Aditya Birla Advanced Materials acquired Cargill’s specialty manufacturing facility in the United States, adding a 17-acre site and planning to expand capacity from 16,000 tonnes per year to over 40,000 tonnes within two years.

Key Takeaways

- Industrial Phenol Market size is expected to be worth around USD 23.3 Billion by 2035, from USD 15.6 Billion in 2025, growing at a CAGR of 4.1%.

- Cumene Process held a dominant market position, capturing more than a 81.30% share.

- Bisphenol A (BPA) held a dominant market position, capturing more than a 45.80% share.

- Polycarbonates held a dominant market position, capturing more than a 36.20% share.

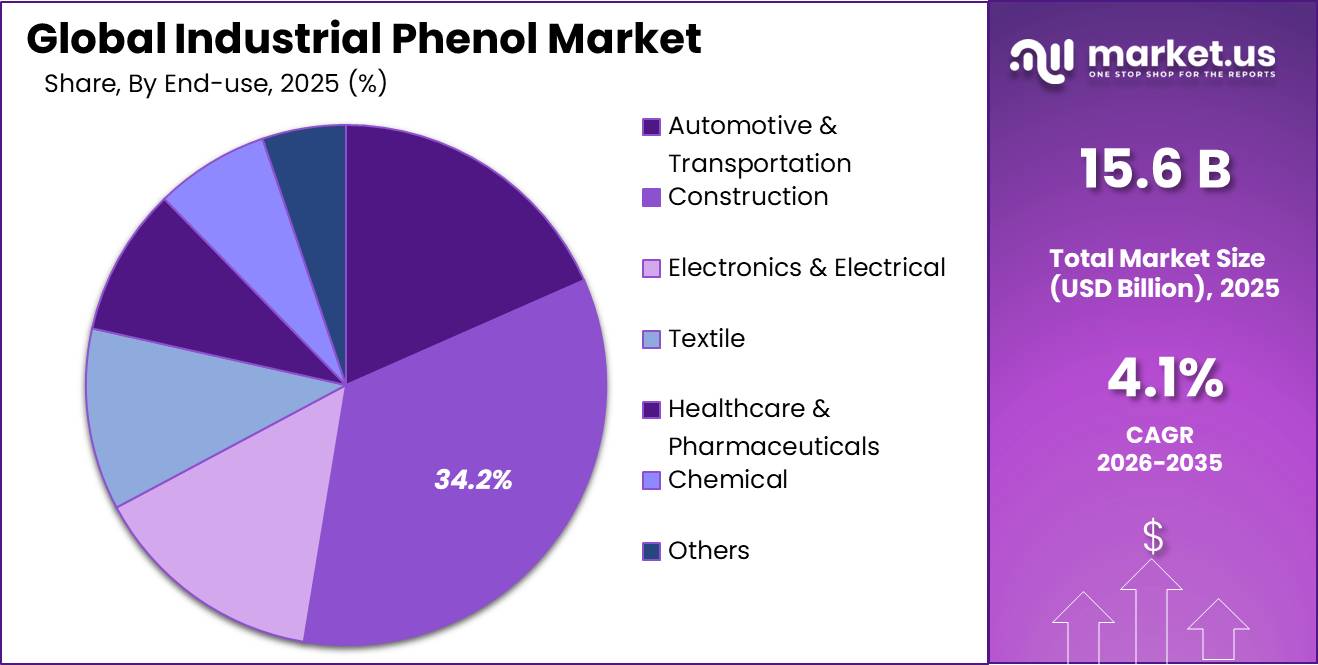

- Construction held a dominant market position, capturing more than a 34.20% share in the industrial phenol market.

- North America held a dominant position in the global industrial phenol market, accounting for 54.20% of the total market share and reaching a market value of USD 8.4 Billion.

By Manufacturing Process Analysis

Cumene Process dominates with 81.30% share driven by large-scale production efficiency and consistent phenol output

In 2025, Cumene Process held a dominant market position, capturing more than a 81.30% share in the industrial phenol market by manufacturing process. This strong position was mainly supported by its long-established industrial use, reliable production economics, and its ability to manufacture phenol together with acetone in a commercially efficient way. The process continues to be preferred by manufacturers because it supports high-volume production while maintaining stable operational performance across large manufacturing facilities.

By Product Type Analysis

Bisphenol A (BPA) dominates with 45.80% share supported by strong demand across industrial and manufacturing applications

In 2025, Bisphenol A (BPA) held a dominant market position, capturing more than a 45.80% share in the industrial phenol market by product type. Its leading position was supported by consistent demand from industries that depend on BPA as a key intermediate material for large-scale manufacturing processes. The product maintained strong market presence because of its broad industrial usability, established supply chains, and its role in supporting high-volume production requirements across multiple end-use sectors.

By Application Analysis

Polycarbonates dominates with 36.20% share driven by steady demand for durable and high-performance materials

In 2025, Polycarbonates held a dominant market position, capturing more than a 36.20% share in the industrial phenol market by application. This leading position was supported by the wide use of polycarbonates in applications that require strength, durability, and long-term performance. Demand remained stable as manufacturers continued to prefer materials that offer lightweight properties along with reliable mechanical performance across industrial production environments.

By End Use Analysis

Construction dominates with 34.20% share supported by continuous demand for durable and performance-based building materials

In 2025, Construction held a dominant market position, capturing more than a 34.20% share in the industrial phenol market by end use. This leading position was supported by steady demand for construction materials that require durability, structural reliability, and long-term performance. Industrial phenol continued to play an important role in supporting the production of materials used across residential, commercial, and infrastructure development activities, helping the construction sector maintain strong consumption levels.

Key Market Segments

By Manufacturing Process

- Cumene Process

- Raschig Process

- Dow Process

By Product Type

- Bisphenol A (BPA)

- Alkyl Phenols

- Chlorophenols

- Caprolactam

- Salicylic Acid

By Application

- Epoxy Resins

- Polycarbonates

- Nylon

- Bakelite

- Phenolic Resins

- Pharmaceutical Drugs

- Others

By End Use

- Automotive & Transportation

- Construction

- Electronics & Electrical

- Textile

- Healthcare & Pharmaceuticals

- Chemical

- Others

Emerging Trends

Circular Production and Recycling Integration Is Becoming a Key Trend in Industrial Phenol

One of the most noticeable trends in the industrial phenol market is the growing shift toward circular manufacturing and better material recovery systems. Producers are increasingly looking beyond traditional production models and focusing on methods that improve resource efficiency, reduce waste, and support long-term sustainability goals. This change is influencing how phenol-based products are designed, processed, and reused across industrial value chains.

According to the OECD Global Plastics Outlook, global plastics production increased from 234 million tonnes in 2000 to 460 million tonnes in 2019, while only 9% of plastic waste was ultimately recycled. These figures have increased industry attention on improving material circularity and reducing dependence on virgin raw materials. Since industrial phenol is closely connected to engineered plastics and resin production, manufacturers are exploring production systems that support recycling and more efficient resource use.

Government Policies Supporting Sustainable Materials Are Reshaping Industrial Development

Another important trend influencing the industrial phenol market is the growing role of government policies that encourage sustainable production and responsible material management. Many countries are introducing frameworks that promote product durability, recycling systems, safer chemical use, and lower environmental impact across manufacturing industries. These policies are gradually changing investment priorities and encouraging industrial producers to improve production efficiency.

The OECD reports that plastics production and conversion account for around 90% of measurable greenhouse gas emissions across the plastics lifecycle, and under current conditions plastics-related emissions could reach 2.8 gigatonnes of CO₂ equivalent annually by 2040, compared with 1.8 gigatonnes in 2020. These environmental targets are encouraging industries to redesign production models and adopt lower-impact manufacturing approaches.

Drivers

Rising Polycarbonate Demand Continues to Push Industrial Phenol Consumption

One of the strongest factors supporting the growth of the industrial phenol market is the rising demand for polycarbonate materials across manufacturing industries. Phenol is a key raw material used to produce Bisphenol A (BPA), which is further converted into polycarbonates and other industrial materials. As industries continue shifting toward durable, lightweight, and long-life materials, demand for phenol remains closely connected to this production chain.

The automotive, electronics, and construction sectors are creating steady consumption of polycarbonate-based products because these materials combine strength with lower weight and good heat resistance.

- According to the United Nations Environment Programme (UNEP), polycarbonate plastic consumption in the Asia-Pacific region increased by around 15% between 2020 and 2022, while the automotive and electronics sectors together represented nearly 60% of this growth. This pattern reflects how industrial manufacturing activity directly supports phenol demand.

Government Support for Industrial Manufacturing and Material Development Strengthens Demand

Government-backed industrial expansion and infrastructure development are also acting as an important driver for industrial phenol consumption. Across major manufacturing economies, policies continue to encourage investment in advanced materials, domestic production capacity, and industrial modernization. These developments increase demand for chemical intermediates that support plastics, coatings, engineered materials, and construction-related applications.

According to the OECD, governments are increasingly promoting policies that improve material efficiency, strengthen manufacturing systems, and support more circular production practices across the plastics value chain. These measures encourage industries to redesign products, improve production efficiency, and maintain stable industrial output. At the same time, industrial sectors continue to adopt high-performance materials for transportation, electronics, and infrastructure projects.

Restraints

Increasing Regulatory Restrictions on Bisphenol A (BPA) Creates Pressure on Industrial Phenol Demand

One of the major factors limiting growth in the industrial phenol market is the increasing regulatory attention around Bisphenol A (BPA), one of the largest downstream applications of phenol. BPA is widely used to manufacture polycarbonate plastics and epoxy resins, including materials used in packaging and industrial products. However, rising concerns around human exposure and environmental impact have resulted in stricter regulations across several regions.

- According to the European Food Safety Authority (EFSA), in 2023 the tolerable daily intake (TDI) for BPA was reduced from 4 micrograms per kilogram of body weight per day to 0.2 nanograms per kilogram per day, representing a 20,000-times lower safety threshold than the previous limit.

This reassessment was based on updated scientific evaluation related to long-term exposure and health concerns. Regulatory changes of this scale create uncertainty across supply chains and encourage industries to evaluate alternative materials and formulations.

Government Actions and Material Substitution Trends Are Slowing Traditional Consumption Patterns

Government initiatives focused on food safety, chemical control, and sustainable materials are creating another restraint for industrial phenol consumption. Several regulatory authorities are introducing stricter policies on chemical migration limits and encouraging industries to reduce dependence on substances under environmental review. These changes are affecting purchasing strategies and material selection decisions across manufacturing sectors.

The European Commission adopted new measures in December 2024 to restrict the use of BPA in food contact materials following EFSA’s updated scientific opinion. In earlier regulations, the EU had already introduced a specific migration limit of 0.05 mg of BPA per kilogram of food and implemented targeted restrictions in sensitive applications. These policy shifts are encouraging producers to invest in alternative chemistries and lower-risk materials.

Opportunity

Expanding Demand for High-Performance Materials Creates New Growth Opportunities for Industrial Phenol

One of the strongest growth opportunities for the industrial phenol market is the increasing demand for high-performance and lightweight materials used across transportation, construction, electronics, and industrial manufacturing. Industrial phenol remains an important raw material for producing engineered materials such as polycarbonates and specialty resins that support product durability and performance. As industries continue upgrading products for efficiency and longer service life, demand for these material systems is creating new opportunities across the value chain.

According to the International Energy Agency (IEA), global electric car sales exceeded 17 million units in 2024, representing more than 20% of total car sales globally. This expansion is increasing demand for lightweight and durable materials that help improve energy efficiency and component performance. Polycarbonate and resin-based materials supported by industrial phenol continue to gain importance in interior systems, electrical components, and advanced manufacturing applications.

Government-Led Infrastructure and Manufacturing Investments Support Long-Term Market Expansion

Public investment in infrastructure and industrial development is creating additional growth opportunities for industrial phenol consumption. Governments across major economies continue introducing policies that encourage domestic manufacturing, advanced materials production, and industrial capacity expansion. These developments support industries that rely on phenol-based materials for coatings, adhesives, insulation, engineered plastics, and industrial components.

- According to the World Bank, global infrastructure investment requirements are estimated at approximately US$94 trillion by 2040 to meet economic growth and development goals.

Large infrastructure programs continue to increase demand for durable construction materials and industrial chemicals used in modern building systems. Government-led industrial policies are also encouraging local manufacturing expansion and supply chain strengthening.

Regional Insights

North America dominates the Industrial Phenol Market with a 54.20% share, valued at USD 8.4 Billion

In 2025, North America held a dominant position in the global industrial phenol market, accounting for 54.20% of the total market share and reaching a market value of USD 8.4 Billion. The region’s leadership was supported by its strong industrial base, established petrochemical infrastructure, and continued demand from downstream industries including construction, automotive, electronics, and advanced manufacturing. Industrial phenol remains an important feedstock for producing polycarbonates, resins, and other industrial materials widely consumed across these sectors.

The region continues to benefit from a mature manufacturing ecosystem and well-developed supply networks that support stable production and distribution of phenol-based products. The presence of large-scale industrial facilities, combined with continuous investment in process efficiency and production modernization, has helped North America maintain a leading market position. Demand has also remained supported by infrastructure activity and ongoing industrial output across major economic centers.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Aditya Birla Chemicals participates in the industrial phenol value chain primarily through advanced materials and epoxy systems that consume phenol derivatives for downstream applications. The company positions itself among the world’s major epoxy resin manufacturers and recently expanded epoxy resin and formulation capacity by 123,000 tonnes per annum, increasing total advanced materials capacity to 246,000 tonnes per annum. Its portfolio serves construction, coatings, composites and electrical industries, strengthening integration across phenol-based specialty materials and value-added chemical applications.

Bayer MaterialScience transitioned into Covestro as an independent company on 1 September 2015, continuing strong participation in phenol-linked markets through polycarbonates and performance materials. Covestro reported approximately €12.9 billion in group sales in FY2025, supported by 46 production sites worldwide and around 17,500 employees. Phenol remains strategically important because bisphenol A is a critical precursor for polycarbonate production, serving automotive, electronics, construction and industrial applications globally.

Top Key Players Outlook

- Aditya Birla Chemicals

- Bayer Material Science

- Royal Dutch Shell plc

- PTT Phenol

- Domo Investment Group

- Solvay SA

- Shandong Sheng Quan Chemicals Co. Ltd.

- Ineos AG

- Domo Investment Group

- Deepak Nitrite Limited

- CEPSA Química, S.A.

- Mitsui Chemicals, Inc

- AdvanSix Inc.

Recent Industry Developments

In 2025, Solvay reported €4.3 billion underlying net sales and €881 million underlying EBITDA, with a 20.7% EBITDA margin, showing stable chemical-sector strength despite weak Coatis and soda ash markets. For partnership, in 2025, Solvay and Sapio launched a 10-year renewable hydrogen agreement in Italy, using a 5 MW electrolyzer and 10 MW solar array, expected to produce up to 756 tons of renewable hydrogen per year by mid-2026.

In 2025, BASF completed the purchase of DOMO Chemicals’ 49% share in the Alsachimie joint venture, making BASF the 100% owner of the PA 6.6 precursor site in France; this helped DOMO sharpen its focus on tailored polyamide solutions. In 2026, Lone Star Funds completed the acquisition of DOMO Engineered Materials and planned to combine it with RadiciGroup’s high-performance polymers and specialty chemicals businesses. DOMO EM brings nearly 70 years of experience, while Lone Star has organized 26 private equity funds with about US$96 billion in capital commitments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 15.6 Bn |

| Forecast Revenue (2035) | USD 23.3 Bn |

| CAGR (2026-2035) | 4.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Manufacturing Process (Cumene Process, Raschig Process, Dow Process), By Product Type (Bisphenol A (BPA), Alkyl Phenols, Chlorophenols, Caprolactam, Salicylic Acid), By Application (Epoxy Resins, Polycarbonates, Nylon, Bakelite, Phenolic Resins, Pharmaceutical Drugs, Others), By End Use (Automotive And Transportation, Construction, Electronics And Electrical, Textile, Healthcare And Pharmaceuticals, Chemical, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Aditya Birla Chemicals, Bayer Material Science, Royal Dutch Shell plc, PTT Phenol, Domo Investment Group, Solvay SA, Shandong Sheng Quan Chemicals Co. Ltd., Ineos AG, Domo Investment Group, Deepak Nitrite Limited, CEPSA Química, S.A., Mitsui Chemicals, Inc, AdvanSix Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |