Quick Navigation

Report Overview

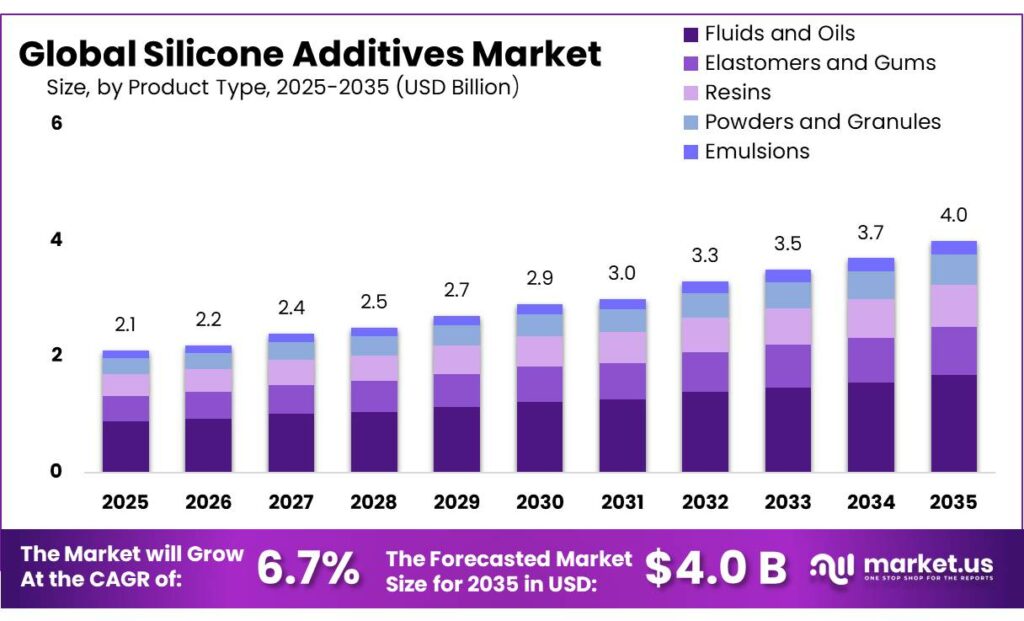

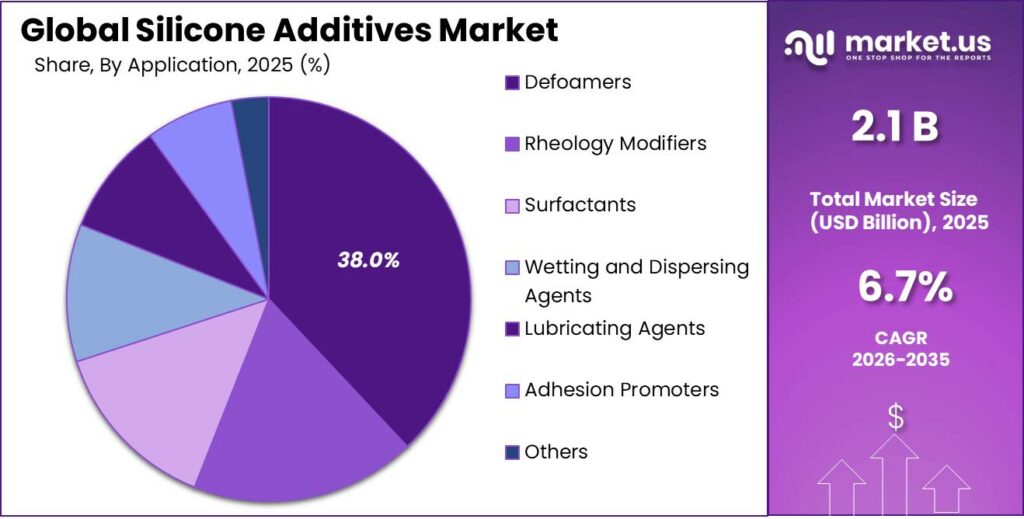

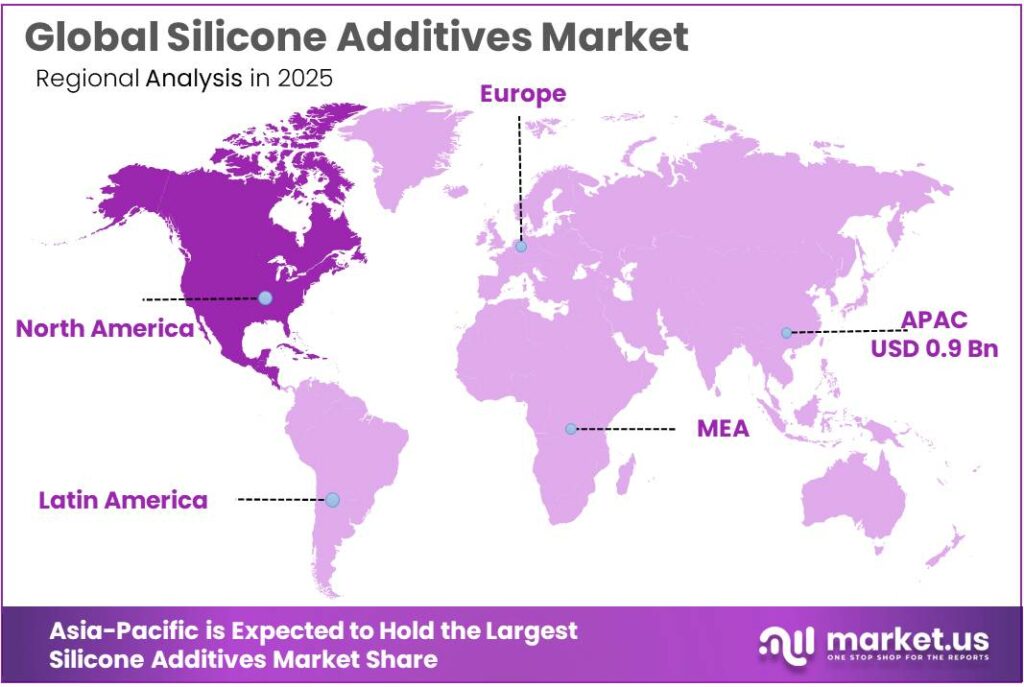

The Global Silicone Additives Market size is expected to be worth around USD 4.0 Billion by 2035, from USD 2.1 Billion in 2025, growing at a CAGR of 6.7% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 44.4% share, holding USD 0.9 Billion revenue.

Silicone additives are specialty performance chemicals used in coatings, plastics, personal care, food processing, electronics, construction and industrial fluids to improve slip, wetting, defoaming, surface leveling, release, water repellency and thermal stability. Industrial demand is supported by regulated food-processing use: the U.S. FDA lists dimethylpolysiloxane under 21 CFR 173.340 for defoaming agents, while FAO/WHO Codex permits polydimethylsiloxane in categories such as milk powder at 10 mg/kg, pre-cooked pasta/noodles at 50 mg/kg, vegetable oils/fats at 10 mg/kg, and flavoured water-based drinks at 20 mg/kg.

The industrial scenario is increasingly shaped by downstream plastics, coatings and sustainable materials. Plastics Europe reported global plastics production rose 4.1% in 2024, while Europe’s share fell from 22% in 2006 to 12% in 2024; European circular plastics reached about 8 million tonnes, or 15% of EU plastics production, creating demand for additives that improve recyclability, durability and processing efficiency.

Key driving factors include stricter performance requirements, lower-VOC coatings, lightweight polymer parts, electronics encapsulation, food-contact compliance and safer process chemistry. In food-contact uses, the U.S. FDA’s 21 CFR 177.2600 permits repeated-use rubber articles for producing, processing, packaging and holding food when specified polymer and additive conditions are met. The EU similarly requires all food-contact materials to comply with Regulation (EC) No 1935/2004, supporting demand for traceable, compliant silicone systems.

Government and policy support is also relevant. In 2025, the European Commission introduced an action plan for the chemicals industry and stated that it would launch EU Innovation and Substitution Hubs and mobilize Horizon Europe funding for 2025–2027, encouraging safer and more sustainable chemical innovation. This favors silicone additives where they help reduce energy use, improve coating efficiency, extend product life and replace less sustainable formulation components.

ALTANA’s BYK division is positioned in additives and instruments, and ALTANA reported 2025 half-year sales of €1,624 million, with R&D expenses up 3%. In December 2025, ALTANA also secured an EIB credit line of up to €300 million for sustainable R&D across the EU and Switzerland.

Key Takeaways

- Silicone Additives Market size is expected to be worth around USD 4.0 Billion by 2035, from USD 2.1 Billion in 2025, growing at a CAGR of 6.7%.

- Fluids and Oils held a dominant market position, capturing more than a 42.8% share.

- Defoamers held a dominant market position, capturing more than a 38.5% share.

- Paints and Coatings held a dominant market position, capturing more than a 27.2% share.

- Asia-Pacific emerged as the leading region in the silicone additives market, accounting for a dominant 44.4% share, valued at around USD 0.9 billion.

By Product Form Analysis

Fluids and Oils dominate with 42.8% driven by their versatility across industries

In 2025, Fluids and Oils held a dominant market position, capturing more than a 42.8% share. This strong position is mainly because these forms are easy to use and mix well with different materials like plastics, coatings, and personal care products. Manufacturers prefer fluids and oils since they spread evenly, improve surface quality, and help in reducing defects during production. Their ability to perform under different temperature conditions also adds to their wide usage.

By Application Analysis

Defoamers lead with 38.5% as industries rely on smoother and bubble-free processing

In 2025, Defoamers held a dominant market position, capturing more than a 38.5% share. This leading position comes from their important role in controlling foam during manufacturing processes. Foam can slow down production, affect product quality, and create handling issues, especially in industries like paints, coatings, food processing, and wastewater treatment. Defoamers help solve these problems by quickly breaking down foam and preventing it from forming again, making operations more efficient.

By End-User Analysis

Paints and Coatings lead with 27.2% as demand for better finish and durability grows

In 2025, Paints and Coatings held a dominant market position, capturing more than a 27.2% share. This is largely because silicone additives play a key role in improving surface quality, smoothness, and resistance in coatings. They help in reducing defects like craters and uneven textures, while also enhancing properties such as water repellency and gloss. These benefits make them highly valuable in both decorative and industrial coating applications.

Key Market Segments

By Product Form

- Fluids and Oils

- Elastomers and Gums

- Resins

- Powders and Granules

- Emulsions

By Application

- Defoamers

- Rheology Modifiers

- Surfactants

- Wetting and Dispersing Agents

- Lubricating Agents

- Adhesion Promoters

- Others

By End-User

- Food and Beverage

- Plastics and Composites

- Paints and Coatings

- Personal Care

- Adhesives and Sealants

- Paper and Pulp

- Oil and Gas

- Others

Emerging Trends

Safer Silicone Additives for Food-Contact Packaging

A major latest trend is the shift toward food-safe, low-migration silicone additives in packaging films, coatings, release liners, and anti-foam uses. Food companies want packaging that runs smoothly on machines, prevents sticking, and protects food without adding safety risk. This trend is growing because regulators are stricter now. The FDA lists silicone substances under food-contact rules and says use depends on identity, purpose, and allowed conditions.

For dimethylpolysiloxane used as a defoaming agent, the U.S. limit is generally 10 ppm in food, with special exceptions such as zero in milk. This matters because packaging and processing are linked to waste reduction. FAO says 13.2% of food is lost after harvest and before retail, while another 19% is wasted at retail, food service, and household level. Better silicone-aided packaging can support smoother handling and longer food protection.

Recyclable and PFAS-Free Packaging Is Pulling Silicone Innovation

Another strong trend is silicone additives being redesigned for recyclable, cleaner food packaging, especially as governments push circular packaging. The European Commission says the new Packaging and Packaging Waste Regulation entered into force on 11 February 2025 and will generally apply from 12 August 2026.

This is pushing manufacturers to use additives that help film slip, release, sealing, and processing without harming recyclability or food safety. The EU also notes that 40% of plastics used in the EU are in packaging, half of marine litter comes from packaging, and EU citizens generated 186.5 kg of packaging waste per person in 2022.

Drivers

Growing demand from food processing industries is pushing silicone additive use

One of the strongest driving factors for silicone additives is their growing use in food processing, especially as defoamers. In large-scale food production, foam can slow down operations, cause overflow, and reduce efficiency. Silicone-based defoamers help solve this by quickly breaking foam and keeping production lines stable.

This demand is directly linked to how modern food factories operate. Processes like frying, fermentation, dairy production, and beverage bottling all create foam, which needs to be controlled for smooth output. Silicone additives are preferred because they work in very small quantities and remain stable even at high temperatures.

Strong regulatory approval and safety standards support adoption

Another key driver is the strong regulatory support and safety approvals for silicone additives in food-related applications. Government bodies like the U.S. Food and Drug Administration allow the use of certain silicone-based defoamers in food processing under strict guidelines. For example, regulations under 21 CFR 173.340 confirm that defoaming agents can be safely used during food production when they meet defined conditions.

These approvals give manufacturers confidence to use silicone additives without worrying about safety or compliance issues. In fact, some silicone defoamers are permitted at very low levels, such as up to 10 ppm in specific food applications, ensuring they do not affect the final product.

Restraints

Strict regulatory limits and usage restrictions slow wider adoption

One of the key restraining factors for silicone additives is the strict regulatory limits placed on their usage, especially in food processing. While silicone-based defoamers are approved, their use is tightly controlled. For example, under U.S. regulations, the use of dimethylpolysiloxane in food is limited to not more than 10 parts per million (ppm) in the final product.

This creates a challenge for manufacturers. Even though silicone additives are effective, companies must carefully control dosage and ensure compliance with safety rules. In many cases, additional testing, monitoring, and documentation are required before using these additives in food production. This adds time and cost to the process.

Concerns around migration and environmental persistence create hesitation

Another important restraint is the concern about migration of silicone compounds into food and their environmental behavior. Studies have shown that certain silicone-related substances can migrate from materials into food, especially under specific conditions like high fat content or repeated use.

Even though many silicone additives are considered safe, this possibility of migration makes both regulators and manufacturers cautious. Food companies must ensure that any transfer remains within safe limits, which again increases testing and compliance efforts. Additionally, some forms of silicone, such as polydimethylsiloxane, are known to be non-biodegradable, meaning they do not break down easily in the environment.

Opportunity

Rising processed food demand is creating strong room for silicone additive expansion

One major growth opportunity for silicone additives is the steady rise in processed and packaged food production worldwide. As food systems become more industrialized, the need for smooth, efficient processing becomes very important. Silicone additives, especially defoamers, play a key role in keeping production lines stable by controlling foam during cooking, fermentation, and bottling.

Government-backed food safety programs and production efficiency goals are also supporting this shift. Many countries are investing in modern food processing infrastructure, which requires reliable additives to maintain hygiene and quality standards. As food production continues to scale globally, silicone additives have a clear opportunity to grow alongside it.

Expansion of food safety testing and quality control opens new demand areas

This shift is not just about compliance—it is also about consumer trust. People today are more aware of what goes into their food, and companies are under pressure to deliver safe and high-quality products. Silicone additives support this by helping maintain uniform textures, reducing defects, and improving overall processing reliability.

This creates space for advanced additives that can meet both performance and safety expectations. As companies invest more in testing and quality systems, the role of silicone additives becomes more important, opening new growth opportunities across the global market.

Regional Insights

Asia-Pacific dominates with 44.4% share (~USD 0.9 Bn) driven by strong industrial and manufacturing base

Asia-Pacific emerged as the leading region in the silicone additives market, accounting for a dominant 44.4% share, valued at around USD 0.9 billion. The region’s leadership is mainly supported by its strong manufacturing ecosystem, rapid urbanization, and expanding end-use industries such as construction, automotive, electronics, and personal care.

Government initiatives such as infrastructure development programs in India and industrial expansion policies in China are also contributing to market growth. These efforts are encouraging the use of advanced materials, including silicone additives, to meet higher quality and performance standards. Additionally, increasing demand for electronics and consumer goods in the region is creating new opportunities for specialized silicone formulations.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

AB Specialty Silicones operates as a niche but focused player in the silicone additives space, especially in personal care, coatings, and industrial applications. The company generates an estimated annual revenue of around USD 7.5 million, supported by a workforce of nearly 89 employees. Its strength lies in customized silicone formulations and specialty products like ANDISIL®, which serve multiple industries.

Bluestar Silicones, part of a larger global silicone network, plays a key role in supplying silicone additives across industrial and consumer applications. The company has shown revenue figures of around USD 75 million in 2024, with a domestic market share of approximately 11.5% in key segments. It continues to expand production capacity, including additions of nearly 20,000 tons per year, strengthening its supply chain.

BRB International is a well-established specialty chemical company with a strong presence in silicone additives and lubricant solutions. The company generates an estimated annual revenue of about USD 184.1 million, with a workforce ranging between 201–500 employees. It also shows a valuation of nearly USD 589 million, reflecting solid market positioning.

Top Key Players Outlook

- AB Specialty Silicones

- Altana AG

- Bluestar Silicones

- BRB International

- Clariant AG

- Dow

- Elkem ASA

- Evonik Industries AG

- Jiangsu Maysta Chemical

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co., Ltd.

Recent Industry Developments

BRB International is a well-recognized player in the silicone additives market, mainly focused on supplying specialty silicones and lube oil additives for industries such as coatings, personal care, and industrial fluids. As of 2025, the company operates with an estimated annual revenue of around USD 184.1 million, supported by a workforce of approximately 201–500 employees, reflecting its position as a mid-sized but globally active manufacturer.

Altana AG plays a strong and well-established role in the silicone additives market through its BYK division, which focuses on additives for coatings, plastics, and industrial applications. In 2025, Altana reported total sales of about €3.081 billion, supported by a global workforce of nearly 8,176 employees, showing its scale as a major specialty chemicals company.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.1 Bn |

| Forecast Revenue (2035) | USD 4.0 Bn |

| CAGR (2026-2035) | 6.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Form (Fluids and Oils, Elastomers and Gums, Resins, Powders and Granules, Emulsions), By Application (Defoamers, Rheology Modifiers, Surfactants, Wetting and Dispersing Agents, Lubricating Agents, Adhesion Promoters, Others), By End-User (Food and Beverage, Plastics and Composites, Paints and Coatings, Personal Care, Adhesives and Sealants, Paper and Pulp, Oil and Gas, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | AB Specialty Silicones, Altana AG, Bluestar Silicones, BRB International, Clariant AG, Dow, Elkem ASA, Evonik Industries AG, Jiangsu Maysta Chemical, KCC SILICONE CORPORATION, Momentive, Shin-Etsu Chemical Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |