Quick Navigation

Report Overview

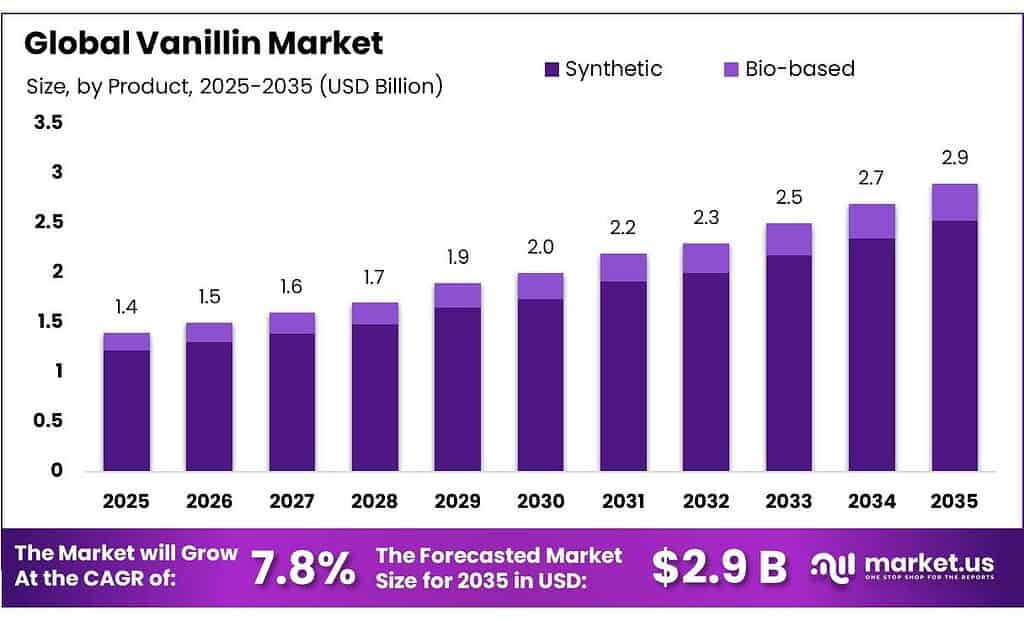

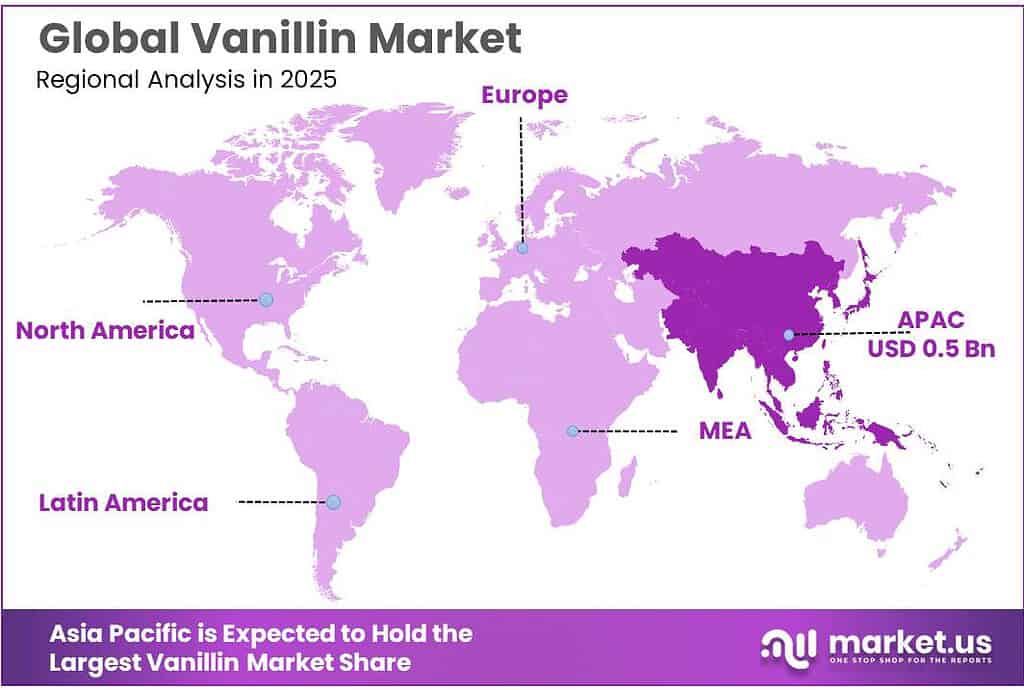

The Global Vanillin Market size is expected to be worth around USD 2.9 Billion by 2035, from USD 1.4 Billion in 2025, growing at a CAGR of 7.8% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 42.6% share, holding USD 0.5 Billion revenue.

Vanillin remains one of the most commercially important aroma molecules in the global flavor system because it delivers a recognizable sweet, creamy, and warm profile at a cost and consistency that natural vanilla beans alone cannot match. Industrially, it serves food and beverage formulators, confectioners, bakers, dairy processors, nutraceutical manufacturers, and fragrance houses.

The structural need for vanillin is reinforced by the limited scale and volatility of natural vanilla supply: in 2024, Madagascar exported vanilla worth about US$231.6 million with a volume of 4.54 million kg, underlining how constrained natural vanilla availability remains relative to broad industrial demand.

The industrial scenario for vanillin is fundamentally supported by the scale of downstream food manufacturing. In Europe, the food and drink industry employs 4.7 million people and generates roughly €1.2 trillion in turnover with €250 billion in value added, making it the EU’s largest manufacturing industry. In the United States, confectionery sales exceeded US$54 billion in 2024, while 98% of shoppers bought confectionery products during the year, and the four major candy seasons accounted for 62% of annual category sales.

Demand growth is being driven by three structural factors. First, packaged bakery and sweet goods remain resilient in emerging and developed markets; the USDA noted that the Philippine baking industry spent about $1.5 billion on ingredients in 2022, with 77% imported, and that baked goods retail sales are projected to reach $2.5 billion by 2027. Second, cleaner-label formulation is intensifying.

In July 2025, HHS said the U.S. dairy industry committed to remove 7 certified artificial dyes from ice cream and frozen dairy desserts by 2028, a policy signal that favors broader natural-ingredient reformulation, including flavor systems. The European Commission imposed a definitive anti-dumping duty of 131.1% on vanillin imports from China, highlighting how trade policy can rapidly alter sourcing economics for buyers in Europe.

Advanced Biotech continued to market VANILLIN NATURAL 1144 and, through its March 2025 market report and February 2025 content on food transparency and label certifications, signaled continued alignment with clean-label and regulatory-conscious flavor development.

Key Takeaways

- Vanillin Market size is expected to be worth around USD 2.9 Billion by 2035, from USD 1.4 Billion in 2025, growing at a CAGR of 7.8%.

- Synthetic held a dominant market position, capturing more than a 87.3% share.

- Powder/Crystal held a dominant market position, capturing more than a 58.4% share.

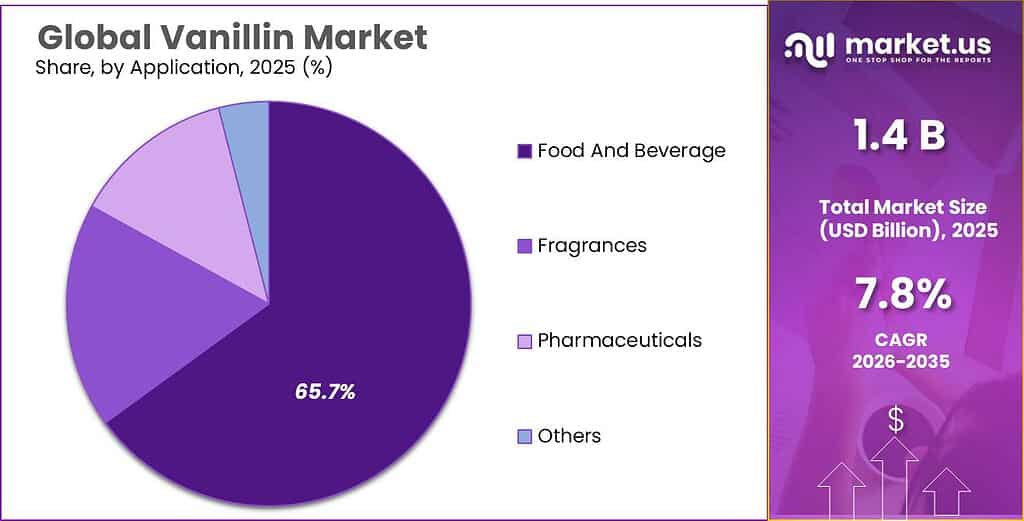

- Food & Beverage held a dominant market position, capturing more than a 65.7% share.

- Asia Pacific held the dominant position in the global vanillin market, accounting for 42.6% of total share and reaching a market value of nearly USD 0.5 billion.

By Product Analysis

Synthetic dominates with 87.3% share due to its reliable supply and cost-efficient large-scale production.

In 2025, Synthetic held a dominant market position, capturing more than a 87.3% share. This strong position was mainly supported by its consistent quality, easy availability, and lower production cost compared to other product types. Synthetic vanillin continues to be the preferred choice across food, beverage, bakery, confectionery, and fragrance applications because manufacturers need stable flavor performance in large volumes.

By Form Analysis

Powder/Crystal leads with 58.4% share thanks to easy storage, longer shelf life, and wide industrial usability.

In 2025, Powder/Crystal held a dominant market position, capturing more than a 58.4% share. This form remained the preferred choice across the vanillin market because it offers better stability during storage and transportation, making it highly suitable for large-scale commercial use. Manufacturers in food processing, bakery, confectionery, dairy, and flavor blending widely prefer powder and crystal formats as they are easy to measure, mix, and maintain in dry formulations. The form also supports precise dosage control, which is important for maintaining consistent aroma and taste in finished products.

By Application Analysis

Food & Beverage dominates with 65.7% share driven by strong demand from bakery, confectionery, dairy, and flavored drinks.

In 2025, Food & Beverage held a dominant market position, capturing more than a 65.7% share. This segment led the vanillin market because vanillin remains one of the most widely used flavor ingredients in everyday food and drink products. Its strong presence in bakery items, chocolates, candies, ice cream, dairy desserts, ready-to-drink beverages, and packaged sweet goods continued to support high demand throughout the year. Food manufacturers prefer vanillin for its ability to deliver a familiar sweet aroma and consistent vanilla taste while remaining cost-effective for large-scale production.

Key Market Segments

By Product

- Synthetic

- Bio-based

By Form

- Powder/Crystal

- Liquid/Solution

- Granules/Other

By Application

- Food & Beverage

- Fragrances

- Pharmaceuticals

- Others

Emerging Trends

Precision Fermentation is the Latest Trend Transforming the Vanillin Industry

One of the most important latest trends in vanillin is the shift toward precision fermentation and bio-based production. Food brands are moving away from only petrochemical or bean-derived sources and increasingly using microbial fermentation to make vanillin from rice bran, ferulic acid, lignin, and other renewable food-side materials. This trend is growing because brands want better traceability, stable pricing, and cleaner labels in bakery, dairy, chocolates, flavored drinks, and nutrition products.

A highly trusted scientific source notes that global vanillin demand had already reached 18,600 tons, showing why food manufacturers are actively adopting scalable fermentation systems. What makes this trend “latest” is that even FAO in 2026 highlighted precision fermentation as an innovative pathway for food sustainability and food security, with strong emphasis on safety-by-design and regulatory transparency.

Upcycling Food By-Products into Bio-Vanillin is a Fast-Rising Trend

Another strong latest trend is the use of food and agro-industrial by-products to create vanillin, especially from lignin, rice bran, corn fiber, and ferulic acid-rich crop streams. Instead of wasting these materials, the food ingredient industry is converting them into high-value flavor molecules. This circular approach is becoming popular because it lowers waste and supports sustainability goals.

Trusted scientific sources show that lignin-based and biotransformation routes are now among the main modern production methods for vanillin, especially for food-grade applications. This trend matches broader government-backed sustainability programs from FAO and national food innovation agencies that encourage waste reduction and resource efficiency across food systems.

Drivers

Rising processed food consumption is the strongest demand driver for vanillin

One of the biggest factors driving the vanillin market is the steady rise in processed and packaged food consumption worldwide. Vanillin is widely used in bakery products, chocolates, biscuits, dairy desserts, flavored milk, ice cream, and ready-to-drink beverages because it gives a familiar sweet vanilla note at a cost-effective level.

Another trusted consumption-side indicator comes from long-established vanillin usage data. Global annual demand for vanillin has historically remained far above natural vanilla bean supply, with around 12,000 tons of annual demand versus only 1,800 tons from natural production, forcing the food industry to depend heavily on synthetic and bio-based vanillin sources. This gap clearly shows why vanillin remains essential for industrial-scale food production.

Growth in bakery, confectionery, and dairy launches continues to lift vanillin use

Another major growth factor is the rapid expansion of vanilla-flavored product launches across bakery, confectionery, and dairy categories. Vanilla remains one of the most preferred flavor profiles globally because it blends easily with chocolate, cream, caramel, fruit, and coffee-based products. A highly trusted usage benchmark shows that ice cream and chocolate alone account for nearly 75% of vanillin flavor use, which directly links market growth to rising dessert and confectionery production worldwide.

This is especially visible in premium cookies, protein shakes, flavored yogurt, milk beverages, and seasonal confectionery items where vanilla is often the base flavor note. Government-backed food processing expansion programs in emerging economies, especially India’s food processing incentives and export-linked manufacturing support, are also helping ingredient demand grow further.

Restraints

Supply Shortage of Natural Vanilla Beans is a Major Restraining Factor

One major restraining factor for the vanillin market is the limited supply of natural vanilla beans, which directly affects natural vanillin production. Vanilla farming is highly concentrated in a few tropical countries, and this makes the supply chain fragile. Global food and flavor demand has stayed much higher than natural vanilla output for years. A trusted food science source notes that annual vanillin demand was around 12,000 tons, while natural vanilla sources could supply only about 1,800 tons, which means natural production covered barely 15% of total demand.

This gap creates strong pressure on food manufacturers that use vanillin in bakery, dairy, confectionery, and beverages. When cyclones, crop disease, or poor flowering affect vanilla-growing regions, prices rise sharply and food companies face cost instability. One industry technical source reports that vanilla prices have shown fluctuations of up to 200 times across different periods because of storms and supply bottlenecks.

Long Curing Time and Climate Risk Slow Market Growth

Another big challenge is the very slow curing and processing cycle of vanilla pods, which makes natural vanillin expensive and difficult to scale. Fresh vanilla beans do not naturally have the strong aroma people expect. They need a long curing process that can take several months, including sweating, drying, and aging before usable vanillin develops.

This long cycle reduces speed for food ingredient manufacturers who need stable volumes for ice cream, chocolate, biscuits, and ready-to-drink products. In simple terms, even if demand rises quickly, farmers cannot increase supply immediately. On top of this, climate change is making flowering cycles less predictable, which lowers yields further.

Opportunity

Clean-Label Food Demand is a Strong Growth Opportunity for Vanillin

One of the biggest growth opportunities for vanillin is the rising demand for clean-label and naturally flavored food products. Consumers today are reading ingredient labels more carefully and prefer simple names they can trust. This is creating strong space for natural and bio-based vanillin in bakery, dairy, chocolates, flavored milk, protein drinks, and premium desserts. A widely cited food science estimate shows global vanillin demand is already around 12,000 tons annually, while natural vanilla sources contribute only about 1,800 tons, leaving a large unmet gap for food-grade natural vanillin solutions. This shortage itself opens a strong growth window for fermentation-based and plant-derived vanillin used by food brands.

Government and regulatory support is also helping this shift. The U.S. FDA permits vanillin as a direct food flavoring substance under 21 CFR 172.515, which supports safe use in mainstream packaged foods. At the same time, global food bodies like FAO are supporting sustainable vanilla farming, better post-harvest handling, and reduced food loss, helping improve long-term raw material supply. FAO’s food system programs focus on better agricultural productivity and value-chain resilience, which directly supports vanilla and vanillin ingredients.

Domestic Vanilla Cultivation and Bio-Based Production Create New Industry Scope

Another major growth opportunity is the development of domestic vanilla cultivation and bio-based vanillin production, especially in countries trying to reduce dependence on imported vanilla beans. A very trusted government-backed example comes from the USDA National Agricultural Library, where a dedicated breeding initiative is working to build a domestic vanilla industry. The program’s goal is to identify superior vanilla plant lines and create a self-sustaining domestic vanilla industry, which can improve both productivity and profitability for food ingredient manufacturers.

This matters because food companies need stable supply for ice cream, biscuits, confectionery fillings, breakfast cereals, and beverages. Bio-based vanillin made from lignin, rice bran ferulic acid, or other renewable food-side streams can meet this demand at scale. It also fits well with sustainability goals from governments and food regulators who are pushing for lower waste and circular ingredient systems. FAO’s wider support for sustainable agrifood systems and reduced crop losses adds further confidence for long-term expansion.

Regional Insights

Asia Pacific dominates the vanillin market with 42.6% share, reaching nearly USD 0.5 Bn.

In 2025, Asia Pacific held the dominant position in the global vanillin market, accounting for 42.6% of total share and reaching a market value of nearly USD 0.5 billion. The region’s leadership is strongly supported by its large and rapidly expanding food and beverage manufacturing base, particularly across China, India, Japan, South Korea, and Southeast Asia.

Rising consumption of bakery products, confectionery, flavored dairy, instant beverages, and packaged snacks has significantly increased the use of vanillin as a core flavoring ingredient. The growth of organized retail and e-commerce food distribution has further accelerated demand for shelf-stable and flavor-consistent processed foods, where vanillin remains widely preferred.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Ennloys holds a specialized position in the vanillin market through its focus on aroma chemicals, flavor intermediates, and customized ingredient solutions. The company’s strength is more visible in small-to-mid volume industrial supply contracts, where consistent purity levels above 99% for food-grade vanillin applications are highly valued. Its market relevance is supported by growing demand from regional bakery, confectionery, and fragrance manufacturers seeking flexible sourcing quantities ranging from 25 kg to 500 kg batch supply formats. This numerical flexibility helps Ennloys stay competitive in custom blending and private-label flavor manufacturing, especially in Asia-focused industrial demand channels.

Advanced Biotech is recognized for its focus on natural flavor compounds, aroma molecules, and high-purity vanillin solutions, widely used in premium food, nutraceutical, and personal care formulations. Its competitive value comes from supplying vanillin in purity ranges above 98%–99%, which is important for manufacturers requiring precise flavor performance. The company serves regulated applications where dosage control can range between 0.05% and 0.5% formulation inclusion levels, depending on end use. This numerical precision makes it highly suitable for premium bakery, dairy flavors, supplements, and fragrance blends where consistency and compliance remain key buying parameters.

Top Key Players Outlook

- Apple Flavor & Fragrance Group Co Ltd.

- Camlin Fine Sciences Ltd.

- De Monchy Aromatics

- International Flavors & Fragrances

- Ennloys

- Evolva Holding

- Advanced Biotech

- Omega Ingredients Ltd.

- Comax Flavors

Recent Industry Developments

In 2025, International Flavors & Fragrances (IFF) remained a key company in the vanillin sector through its wider taste business, supported by USD 10.89 billion in full-year net sales, while its Taste segment generated USD 2.48 billion and posted an adjusted EBITDA margin of 19.3%.

In 2025, Advanced Biotech continued to strengthen its position in the vanillin sector through its natural vanillin ingredient portfolio, especially its flagship “Vanillin Natural 1144” used in food, beverage, nutraceutical, and fragrance formulations. The company’s strength in this space comes from its focus on high-purity natural flavor ingredients with purity levels typically above 98%, which is highly important for premium vanilla taste systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.4 Bn |

| Forecast Revenue (2035) | USD 2.9 Bn |

| CAGR (2026-2035) | 7.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Synthetic, Bio-based), By Form (Powder/Crystal, Liquid/Solution, Granules/Other), By Application (Food And Beverage, Fragrances, Pharmaceuticals, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Apple Flavor & Fragrance Group Co Ltd., Camlin Fine Sciences Ltd., De Monchy Aromatics, International Flavors & Fragrances, Ennloys, Evolva Holding, Advanced Biotech, Omega Ingredients Ltd., Comax Flavors |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |