Quick Navigation

Report Overview

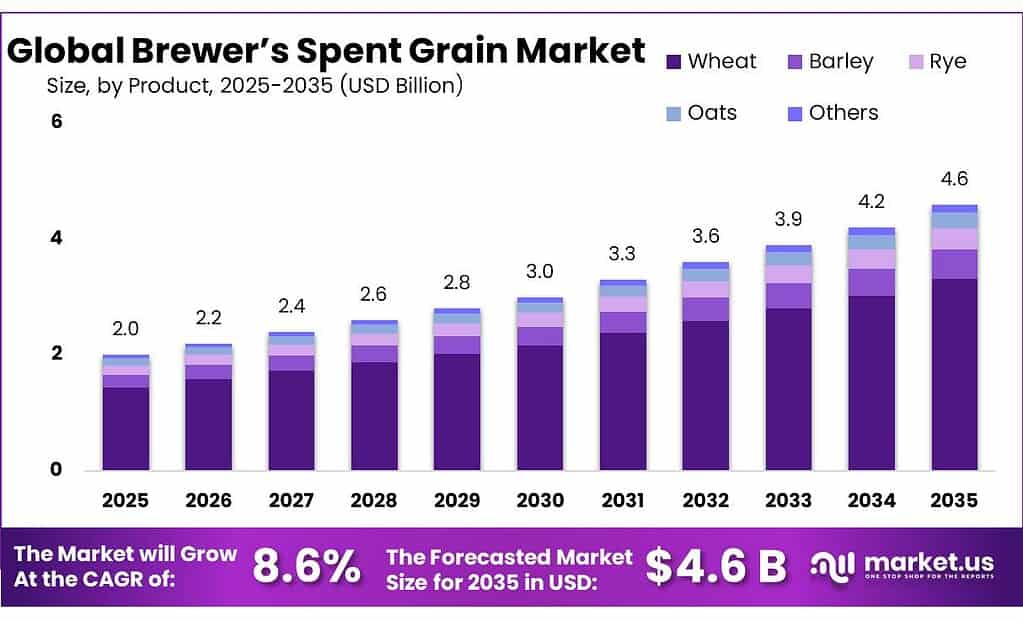

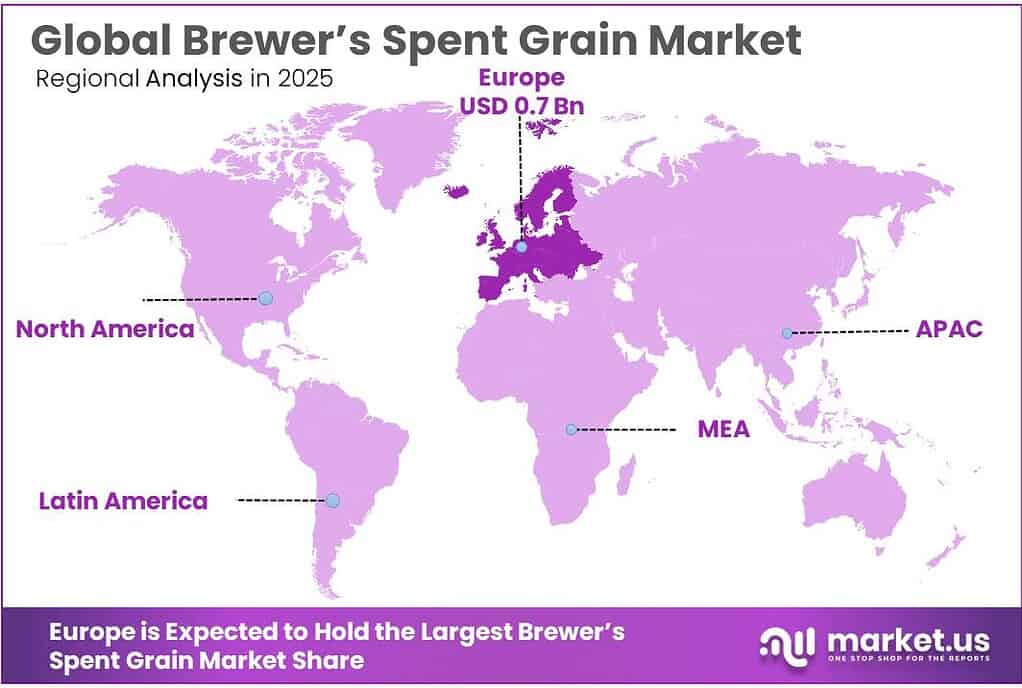

The Global Brewer’s Spent Grain Market size is expected to be worth around USD 4.6 Billion by 2035, from USD 2.0 Billion in 2025, growing at a CAGR of 8.6% during the forecast period from 2026 to 2035. In 2025, Europe held a dominant market position, capturing more than a 37.4% share, holding USD 0.7 Billion revenue.

Brewer’s spent grain (BSG) is the primary solid co-product of beer making and remains one of the most commercially relevant side streams in the circular food economy. Industry and public sources consistently position it as the dominant brewing residue: the European Commission’s LIFE RESTART project states that BSG accounts for about 85% of brewery by-products and that roughly 20 kg of BSG is generated for every 100 litres of beer produced.

The industrial scenario remains closely tied to beer output. The BarthHaas Report 2024/2025 states that the world’s 40 largest brewing groups produced 1,639 million hectolitres in 2024, while The Brewers of Europe reports that European Union beer production declined from about 367 million hectolitres in 2019 to 345 million hectolitres in 2024. In the United States, the Brewers Association reported 23.1 million barrels of craft beer production in 2024, with craft accounting for 13.3% of beer volume and supporting 197,112 jobs. Even in a soft beer-volume environment, these output levels still create a very large and recurring BSG stream for valorization.

Demand-side momentum is being driven by three measurable factors. First, the beer economy remains large enough to sustain a dependable BSG supply chain; in the United States, the Beer Institute stated in 2025 that the beer industry supports more than 2.42 million jobs, contributes $471 billion in economic activity, and pays $58 billion in taxes. Second, breweries and food manufacturers are under stronger pressure to monetize by-products as input costs stay elevated; The Brewers of Europe reported that EU beer consumer spending reached €110 billion in 2022, while brewing contributed over €52 billion in value added.

Government and institutional support is also improving the outlook. The European Commission’s LIFE RESTART initiative highlights BSG-based bioplastics and links the brewing chain to higher-value non-food applications. The EU-backed BiOBreW project is focused on biologically upgrading BSG into higher-value outputs, while the 2025 Circular Bio-based Europe Joint Undertaking opened funding calls worth €172 million across circular-bioeconomy themes. In Australia, the official End Food Waste program notes that the country produces more than 300,000 tonnes of BSG annually, and a 2025 Western Australia government-backed collaboration is converting brewery by-products into food, fibre, nutraceutical and plant-based material opportunities.

Leiber remains more directly connected to by-product valorization. Its spent grains platform positions BSG as a protein-rich feed ingredient, and its brewery partnership model emphasizes collection logistics, storage expansion, intermodal transport, and circular-economy services. A notable 2025 development was Asahi Group Foods’ agreement on 5 March 2025 to acquire 100% of Leiber by the end of April 2025, with stated plans to invest in R&D and production capacity expansion.

Key Takeaways

- Brewer’s Spent Grain Market size is expected to be worth around USD 4.6 Billion by 2035, from USD 2.0 Billion in 2025, growing at a CAGR of 8.6%.

- Wheat held a dominant market position, capturing more than a 72.5% share in the brewer’s spent grain market.

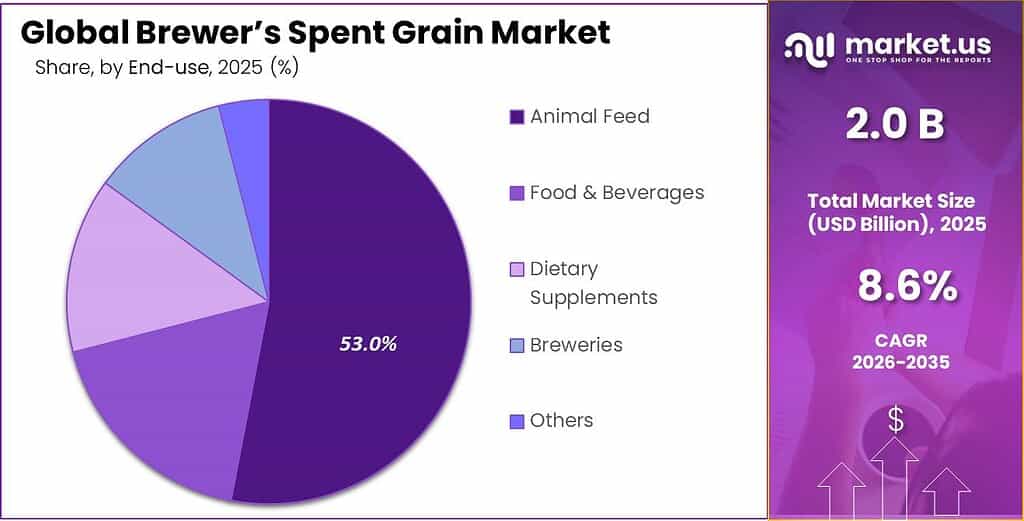

- Animal Feed held a dominant market position, capturing more than a 53.8% share in the brewer’s spent grain market.

- Europe remained the dominant region in the Brewer’s Spent Grain market, accounting for 37.4% share and valued at around USD 0.7 Bn.

By Product Analysis

Wheat dominates with 72.5% share due to its strong availability from wheat beer production and wider use in food and feed applications.

In 2025, Wheat held a dominant market position, capturing more than a 72.5% share in the brewer’s spent grain market by product type. This leading position was mainly supported by the steady production of wheat-based beer across major brewing regions, which consistently generates high volumes of nutrient-rich spent grain. Wheat-based brewer’s spent grain is widely preferred in the industry because it offers a balanced fiber and protein profile, making it suitable for animal feed, bakery enrichment, functional flour blends, and sustainable ingredient development. Its lighter texture and better compatibility with food formulations also make it easier for processors to use in value-added applications compared with some other grain residues.

By Application Analysis

Animal Feed leads with 53.8% share because it remains the most practical and established use for brewer’s spent grain.

In 2025, Animal Feed held a dominant market position, capturing more than a 53.8% share in the brewer’s spent grain market by application. This segment remained the largest because brewer’s spent grain continues to be one of the most widely used by-products in livestock nutrition, especially for cattle, dairy herds, poultry, and swine feed blends. Its strong fiber and protein content makes it a cost-effective ingredient for feed manufacturers and farms looking to improve nutritional value while managing input costs. The steady availability of spent grain from breweries also supports regular supply for feed use, particularly in regions with strong beer production and developed livestock industries.

Key Market Segments

By Product

- Wheat

- Barley

- Rye

- Oats

- Others

By Application

- Animal Feed

- Cattle (Dairy/Beef)

- Horse Feed

- Poultry

- Others

- Food & Beverages

- Dietary Supplements

- Breweries (Return)

- Others

Emerging Trends

Fermentation and food-grade upcycling are the latest major trends shaping Brewer’s Spent Grain

One of the most important latest trends in brewer’s spent grain in 2025 is the move toward fermentation-based and extrusion-enabled food ingredient development. Instead of limiting spent grain to traditional feed use, food processors are now using advanced fermentation and extrusion methods to convert it into high-fiber flours, protein-rich snack bases, breakfast cereals, meat alternatives, and clean-label bakery blends. Recent 2025 food science studies highlight that brewer’s spent grain naturally contains 30–50% dietary fiber and 19–30% protein on a dry basis, which is making it highly attractive for health-focused food innovation.

Another major sign of this trend is how quickly plant-based food and functional snack applications are expanding. In 2025, peer-reviewed research showed successful use of brewer’s spent grain in burgers, meat alternatives, cookies, and extruded cereal-style products, with studies reporting up to 50% and 75% flour replacement levels in cookie formulations while still maintaining product quality targets in selected trials.

Government-backed circular bioeconomy projects are accelerating the trend in 2025

Government and institutional support is also making this one of the most visible trends going into 2026. Across Europe, circular bioeconomy funding programs continue to support food waste valorization, residue fermentation, and biomass-to-ingredient technologies. The broader circular bioeconomy literature continues to state that brewer’s spent grain represents nearly 85% of total brewing by-products, which gives public innovation programs a large and reliable feedstock base for scaling food applications.

What makes this trend especially important is that it combines nutrition, sustainability, and processing innovation in one direction. Food brands are under growing pressure to launch products with stronger fiber claims, plant protein content, and waste-reduction credentials. Brewer’s spent grain fits all three needs in a simple and commercially realistic way.

Drivers

Sustainability-led feed demand is a major growth driver for Brewer’s Spent Grain

In 2025, one of the strongest driving factors for brewer’s spent grain demand is its growing role as a low-cost and sustainable animal feed ingredient. Breweries generate large volumes of spent grain every day, and instead of treating it as waste, the feed industry increasingly uses it as a practical protein- and fiber-rich raw material. Recent trusted academic and industry-backed studies estimate that global brewer’s spent grain generation has reached nearly 37 million tons annually, showing the scale of raw material available for feed conversion.

The demand side is being strengthened by sustainability targets from governments and food organizations. A highly practical example comes from Ireland’s official EPA Food Waste Charter guidance for the brewing sector, which states that up to 75% of soybean feed can be replaced with spent brewer’s grain in livestock feed systems. This is an important numerical benchmark because soybean replacement directly lowers feed costs while reducing deforestation-linked sourcing pressure and greenhouse gas emissions.

Government circular economy and food waste initiatives are accelerating adoption

Another major reason this factor is becoming stronger in 2025 is the rise of government-supported circular economy and waste reduction programs. Food and environmental agencies across Europe and other developed brewing regions are actively promoting industrial by-product valorization, especially in feed and bioresource recovery. This policy support gives breweries a clear route to convert disposal costs into value streams. Because animal feed requires relatively limited processing compared with food-grade applications, it remains the easiest and most commercially reliable outlet.

Restraints

High moisture content and short shelf life remain a major restraint for Brewer’s Spent Grain

One of the biggest restraining factors for brewer’s spent grain in 2025 is its very high moisture content, which makes storage and transportation difficult. Trusted scientific sources note that fresh brewer’s spent grain usually contains around 75–80% moisture, which causes it to spoil quickly if it is not dried, refrigerated, or processed immediately.

The short shelf life limits its wider use in food ingredients, bio-based packaging, and nutraceutical applications, even though demand for circular raw materials is growing. Industry-backed reviews further estimate that the world generates around 36.4–39 million tonnes of brewer’s spent grain every year, but a large share still remains underutilized mainly because handling wet material at scale is operationally challenging.

Limited storage infrastructure and government circular economy push highlight the challenge

Another important reason this restraint continues through 2026 is the lack of regional drying and storage infrastructure. Many breweries, especially independent and craft producers, do not have in-house systems to stabilize spent grain quickly after brewing. As a result, they are often forced to sell it at low value for immediate feed use or discard part of the stream when local demand is weak.

Government circular economy initiatives in the EU and national food waste reduction programs are encouraging better residue utilization, but infrastructure investments are still catching up with the scale of supply. Until low-energy drying, fermentation, or decentralized preservation systems become more widely available, moisture-driven spoilage and transport costs will remain one of the strongest barriers to the full commercial expansion of brewer’s spent grain across food, feed, and industrial material markets.

Opportunity

Food-grade protein and fiber ingredient development is the biggest growth opportunity

One of the strongest growth opportunities for brewer’s spent grain in 2025 is its rapid shift from low-value feed use into food-grade protein and fiber ingredients. The biggest advantage is nutritional density. Trusted food science studies continue to show that brewer’s spent grain is naturally rich in dietary fiber at nearly 30–50% and protein at around 19–30% on a dry basis, making it highly suitable for bakery blends, breakfast cereals, snacks, meat alternatives, and nutrition-focused formulations.

A major part of this opportunity comes from the scale of supply. Scientific and industry-backed sources estimate that brewer’s spent grain accounts for nearly 85% of total brewery by-products, giving processors a stable and year-round raw material stream for ingredient extraction. In simple business terms, this means companies can build consistent supply chains for high-fiber flour, plant protein concentrates, antioxidant extracts, and soluble fiber ingredients without depending on seasonal crop cycles.

Circular bioeconomy funding and government-backed food innovation projects are opening new doors

Government and institutional support is making this opportunity even stronger through 2026. The Circular Bio-based Europe Joint Undertaking continues to fund circular food and biomass valorization projects across Europe, creating direct support for technologies linked to residue conversion, protein extraction, and food ingredient innovation.

In parallel, a 2025 Sweden-based “Brewed and Renewed” research project led by RISE is specifically focused on converting brewer’s spent grain into bread and breakfast cereal ingredients, showing how public-private food innovation programs are now moving the category closer to large-scale commercialization.

Regional Insights

Europe dominates with 37.4% share, reaching nearly USD 0.7 Bn, supported by its large brewing base and strong circular economy infrastructure.

Europe remained the dominant region in the Brewer’s Spent Grain market, accounting for 37.4% share and valued at around USD 0.7 Bn, supported by its well-established beer production industry, advanced feed utilization networks, and growing food upcycling ecosystem. The region benefits from one of the world’s most mature brewing landscapes, where recent trusted industry studies show Europe produces nearly 511 million hectoliters of beer annually, creating a strong and continuous raw material stream for spent grain utilization.

Based on standard brewery conversion ratios of 20 kg of spent grain per hectoliter of beer, the European market generates more than 6.4 million tonnes of brewer’s spent grain every year, which strongly supports industrial-scale use across feed, food ingredients, bio-based packaging, and biomaterial applications.

Europe also benefits from stronger regulatory and sustainability support compared with many other regions. EU-backed circular bioeconomy projects are actively promoting residue valorization, helping convert spent grain into protein concentrates, dietary fiber ingredients, fermentation substrates, and biodegradable composite materials. This policy-driven shift is helping the region move beyond low-value feed applications into premium food and industrial uses.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Malteurop remains one of the strongest players in brewer’s spent grain because of its global malt manufacturing scale and direct integration with brewery supply chains. The company operates in 14 countries with 27 malt production plants and a malting capacity of around 2.2 million tonnes per year, creating a large and stable stream of grain residues that can be redirected into feed and food ingredient channels.

Anheuser-Busch Companies LLC is a major brewer’s spent grain supplier because of its huge brewing footprint and efficient by-product recovery systems. The company operates more than 100 facilities across the U.S. supply network, and its parent group AB InBev reported USD 59.8 billion in revenue for 2025, reflecting exceptional beverage production scale. This allows the company to generate very high volumes of spent grain for animal feed, renewable energy, and circular agriculture uses.

MGP is an important specialized player in the brewer’s spent grain market due to its grain processing and distillation operations. In fiscal 2025, MGP reported net sales of USD 703.6 million, supported by its ingredient solutions and distilling businesses. Its grain-based production process generates valuable fiber- and protein-rich residual streams that are increasingly positioned for feed and specialty ingredient applications.

Top Key Players Outlook

- Malteurop

- Anheuser-Busch Companies LLC

- MGP

- DSM

- Lallemand Inc.

- Leiber

- Briess Malt & Ingredients

- Kerry Group plc.

- Buhler

- ReGrained

Recent Industry Developments

In 2025, Malteurop continued to hold a strong strategic position in the brewer’s spent grain sector because of its large-scale malt production network and direct connection with global breweries. The company operates in 14 countries, runs 23 industrial sites, and has an annual malt production capacity of 2.3 million tons, which creates a very large and stable stream of grain side residues that can be redirected into animal feed, food fiber ingredients, and circular bio-based applications.

In 2025, DSM-Firmenich remained an important technology partner in the brewer’s spent grain sector, even though it is not a brewery itself. From a market research view, the company’s role is linked to enzymes, fermentation solutions, feed nutrition, and food texture systems that help improve how grain side streams are processed and reused in animal feed and food applications. The company reported €12.521 billion in total group sales in 2025, operated 234 sites, and had 28,550 employees, which shows the financial scale and technical reach behind its nutrition and ingredient platform.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.0 Bn |

| Forecast Revenue (2035) | USD 4.6 Bn |

| CAGR (2026-2035) | 8.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Wheat, Barley, Rye, Oats, Others), By Application (Animal Feed, Cattle (Dairy/Beef), Horse Feed, Poultry, Others, Food And Beverages, Dietary Supplements, Breweries (Return), Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Malteurop, Anheuser-Busch Companies LLC, MGP, DSM, Lallemand Inc., Leiber, Briess Malt & Ingredients, Kerry Group plc., Buhler, ReGrained |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |