Quick Navigation

Report Overview

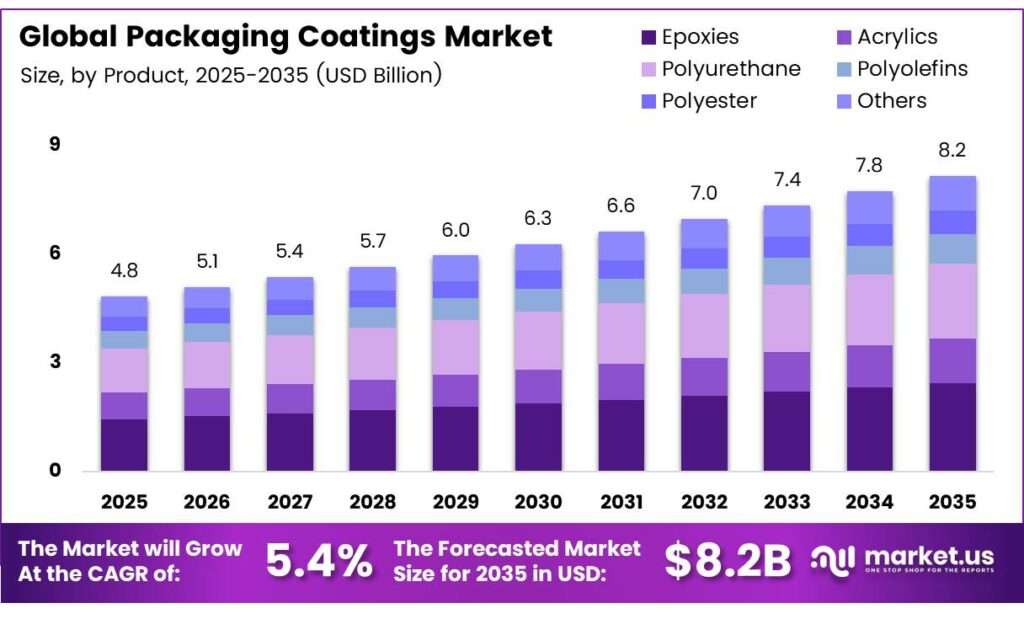

The Global Packaging Coatings Market size is expected to be worth around USD 8.2 billion by 2035 from USD 4.8 billion in 2025, growing at a CAGR of 5.4% during the forecast period 2026 to 2035.

The packaging coatings market covers functional and decorative coatings applied to rigid and flexible packaging across food, beverage, pharmaceutical, and consumer goods sectors. These coatings deliver barrier protection, moisture resistance, chemical inertness, and shelf-life extension. Demand traces directly to the global expansion of packaged goods consumption and the structural shift toward protective, performance-driven packaging formats.

The pharmaceutical and food sectors are particularly strong sources of coating consumption. Both industries operate under strict contamination-prevention standards, requiring coatings to deliver consistent oxygen, moisture, and grease barriers. Extended shelf-life requirements in food packaging and sterility demands in pharmaceutical packaging translate into non-negotiable performance thresholds that budget-focused alternatives cannot easily meet.

Bio-based coating science has advanced measurably in recent laboratory findings. Carnauba wax nano-emulsion coatings improved the water vapor permeability of uncoated paper by approximately 72%. This level of barrier performance from a renewable, compostable source signals that bio-based alternatives are no longer experimental — they are approaching commercial viability, which will compress the market window for synthetic incumbents.

Additional evidence confirms the commercial readiness of wax-based sustainable coatings. Beeswax-coated paper achieved approximately a 77% improvement in water-vapor barrier performance compared to uncoated paper. For brand owners under pressure to eliminate plastic laminates, these numbers represent a credible, performance-proven exit path — accelerating procurement decisions toward bio-based packaging coating suppliers.

Key Takeaways

- The Global Packaging Coatings Market was valued at USD 4.8 billion in 2025 and is forecast to reach USD 8.2 billion by 2035 at a CAGR of 5.4% during the forecast period 2026 to 2035.

- Epoxies held the dominant share at 29.5% in 2025.

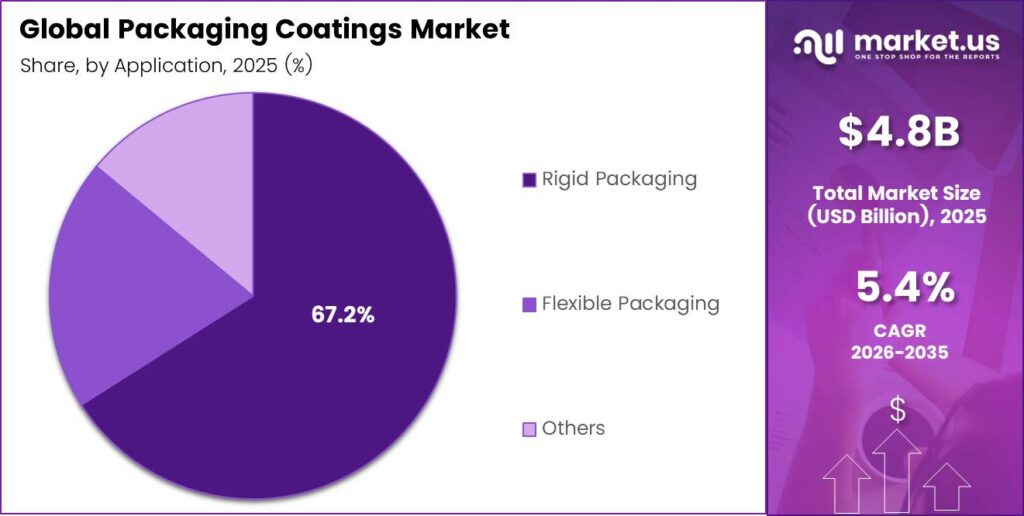

- Rigid Packaging led the market with a 67.2% share in 2025.

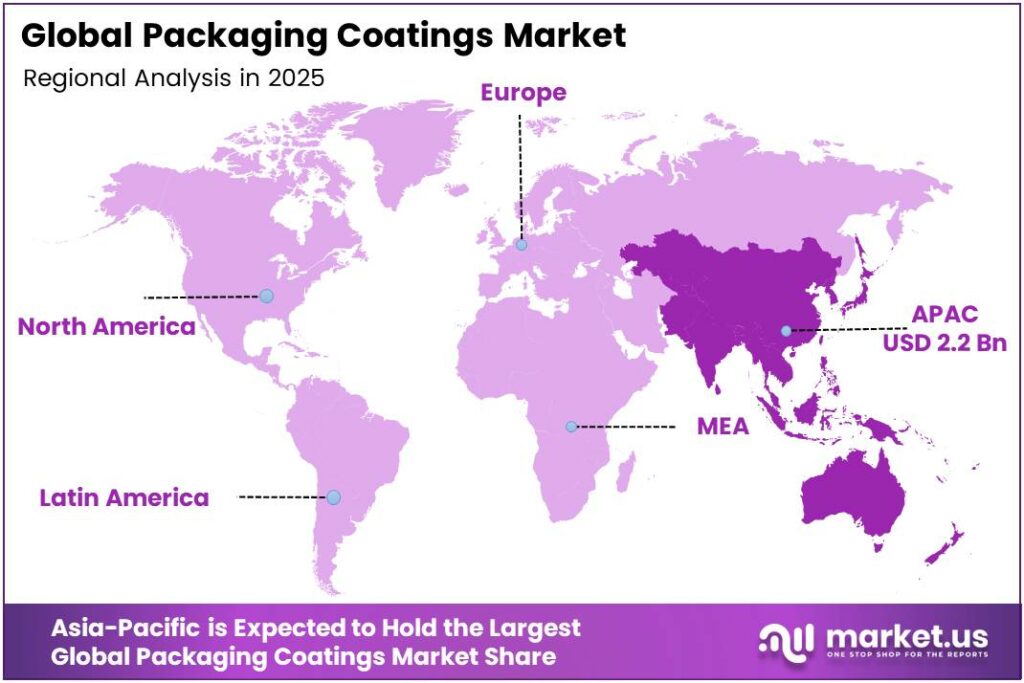

- Asia-Pacific dominated regionally with a 45.7% share, valued at USD 2.2 billion in 2025.

Product Analysis

Epoxies dominate with 29.5% due to superior adhesion and chemical resistance in rigid packaging.

In 2025, Epoxies held a dominant market position in the By Product segment of the Packaging Coatings Market, with a 29.5% share. Epoxy coatings deliver unmatched adhesion to metal substrates and provide consistent chemical inertness, making them the preferred interior coating for beverage cans and food containers. Their dominance reflects rigid packaging’s structural lead and the strict food-contact safety requirements that fewer alternatives can reliably satisfy.

Acrylics serve as the cost-competitive backbone for flexible and paper-based packaging applications. Acrylic coatings offer formulation versatility — water-based variants align with low-VOC regulatory requirements, while solvent-based grades deliver faster cure speeds in high-throughput production lines. This dual-format utility positions acrylics as the most accessible transition technology as converters shift away from legacy solvent systems.

Application Analysis

Rigid Packaging dominates with 67.2% due to high coating intensity per unit and food-contact compliance demands.

In 2025, Rigid Packaging held a dominant market position in the By Application segment of the Packaging Coatings Market, with a 67.2% share. Metal cans, glass containers, and rigid plastic formats require interior and exterior coatings for corrosion prevention, barrier performance, and label adhesion. The food and beverage industry’s high production volumes in rigid formats concentrate coating consumption in this segment, making it structurally the most stable revenue base in the market.

Flexible Packaging represents the fastest-shifting application zone in the coatings market. Converters are increasing coating intensity on films, pouches, and wraps as they replace plastic laminate structures with coated mono-material formats to meet recyclability targets. This structural shift means flexible packaging is not merely a volume segment — it is the primary arena for coating technology competition over the next decade.

Others in the application segment include specialty substrates such as paper-based cartons, tubes, and corrugated formats used in e-commerce and foodservice. These formats are absorbing a disproportionate share of bio-based coating investment as brand owners target fiber-based packaging transitions. Coating performance in these substrates is directly tied to the commercial feasibility of eliminating plastic liners from paper packaging systems.

Key Market Segments

By Product

- Epoxies

- Acrylics

- Polyurethane

- Polyolefins

- Polyester

- Others

By Application

- Rigid Packaging

- Flexible Packaging

- Others

Emerging Trends

Water-Based, UV-Curable, and Circular Economy Coatings Redefine Packaging Performance Standards

Water-based and UV-curable coatings are displacing solvent-based systems across rigid and flexible packaging lines. Brand owners and converters adopt these technologies primarily to meet VOC emission limits, but the performance gap has narrowed substantially. Water-based barrier coatings over CNF precoating reduced oxygen transmission to less than 5 cm³/m²/day — a barrier level competitive with plastic laminate alternatives.

Digital printing-compatible coatings are becoming a commercial necessity as brand owners shift toward shorter print runs and SKU proliferation. Specialty coating formulations now accommodate inkjet and digital offset processes without adhesion failure or surface defect. This compatibility requirement is reshaping coating procurement — converters increasingly specify coatings by their digital printing performance profile, not solely by substrate adhesion or barrier characteristics.

Recyclability and circular economy compliance are moving from voluntary brand commitments to contractual packaging requirements. Retailers and consumer goods companies now mandate certified compostable or mono-material-compatible coatings in supplier agreements. Minimalist packaging aesthetics, driven by the same sustainability narrative, are also creating demand for specialty matte and tactile coatings — extending coating value beyond functional barrier performance into brand differentiation territory.

Drivers

E-Commerce Expansion and Food Safety Standards Concentrate Protective Coating Demand Across Multiple Packaging Substrates

E-commerce fulfillment chains subject packaging to mechanical stresses that traditional retail logistics never required. Protective coatings must now deliver abrasion, moisture, and crush resistance across extended transit cycles. This structural shift in distribution directly expands the coating specification requirement per packaging unit — increasing average coating intensity and creating volume upside for suppliers positioned in the protective coatings segment.

Food and beverage manufacturers are extending product shelf-life through advanced barrier coating adoption, reducing spoilage losses and enabling longer distribution windows. Paper coated with acrylated linseed oil showed a 64% reduction in water vapor transmission rate relative to uncoated paper.

Pharmaceutical packaging demands are adding a separate, high-specification coating demand layer. Sterile and controlled-environment packaging requires coatings to prevent moisture ingress, maintain chemical inertness, and support tamper-evidence features. These requirements do not compress on cost — pharmaceutical brands absorb premium coating pricing as a compliance cost, making this segment one of the most margin-resilient in the packaging coatings market.

Restraints

Regulatory Bans on Solvent-Based Formulations and Raw Material Price Swings Compress Coating Supplier Margins

Regulators across North America and the European Union are phasing out solvent-based and high-VOC coating formulations through increasingly restrictive chemical compliance frameworks. Converters operating existing production lines built around solvent-based systems face capital expenditure requirements to retrofit or replace equipment.

Raw material price volatility directly threatens coating supplier profitability. Petrochemical feedstocks, epoxy resins, and specialty monomers have experienced repeated price disruptions driven by energy market fluctuations and supply chain constraints. Advanced bilayer coating systems delivered approximately a 630-fold decrease in air permeability — but the complexity of these high-performance systems also means higher formulation costs.

The combination of regulatory compliance costs and input price instability creates a structural squeeze on coating manufacturers. Smaller suppliers without vertical integration into raw material production have limited hedging options. Consequently, pricing power in this market concentrates with large vertically integrated players, reducing competitive diversity and increasing consolidation pressure among second-tier coating suppliers.

Growth Factors

Bio-Based Innovations, Smart Coating Properties, and Nanotechnology Open New Revenue Tiers in Packaging Coatings

Bio-based and compostable coating formulations are transitioning from research pipelines into commercial product launches. Packaging converters face mounting retailer pressure to certify compostability across their product portfolio. Fish-based biopolymer coatings achieved a 70% reduction in oxygen transmission rate — a performance outcome that directly competes with petroleum-derived barrier coatings.

Antimicrobial and smart coatings represent a higher-margin product tier within packaging coatings. Additionally, a study confirmed that low coating levels of 4 g/m² CNF combined with 11 g/m² barrier coating achieved a WVTR of 20 g/m²/day, demonstrating that performance gains do not require high coating weights — improving cost efficiency for converters.

Nanotechnology integration is enabling thinner coating applications that outperform conventional heavy-coat systems. Nano-enhanced barrier coatings reduce material usage per unit while delivering superior oxygen and moisture resistance. For emerging-economy packaging manufacturers, where cost-per-unit constraints are tightest, nano-enabled coatings offer a path to achieving premium barrier performance at competitive price points — unlocking volume growth in markets that previously could not afford high-specification coating solutions.

Regional Analysis

Asia-Pacific Dominates the Packaging Coatings Market with a Market Share of 45.7%, Valued at USD 2.2 Billion

Asia-Pacific leads the global Packaging Coatings Market with a 45.7% share, valued at USD 2.2 billion in 2025. The region’s dominance reflects the concentration of global packaging manufacturing capacity in China, India, Japan, and South Korea. High food processing output, pharmaceutical export volumes, and the world’s largest e-commerce fulfillment infrastructure collectively sustain coating consumption at a scale no other region currently matches.

North America holds a structurally mature but high-specification coating market. Regulatory agencies, including the EPA and FDA, impose stringent food-contact and VOC compliance standards, driving converters toward premium water-based and UV-curable formulations. This compliance-led premiumization supports higher average selling prices per coating unit, making North America a margin-accretive market despite slower volume growth relative to Asia-Pacific.

Europe’s packaging coatings demand is anchored by the EU’s Circular Economy Action Plan and Single-Use Plastics Directive. These mandates are accelerating the substitution of plastic laminates with recyclable, bio-based coated paper and fiber structures. European brand owners lead global adoption of certified compostable coating technologies — making the region the primary commercial proving ground for next-generation sustainable coating formulations.

The Middle East and Africa region is building packaging manufacturing capacity to serve growing domestic consumer goods consumption. GCC countries are investing in food processing and pharmaceutical manufacturing infrastructure, creating upstream demand for functional and barrier coatings. The region imports most of its advanced coating formulations, presenting a long-term localization opportunity for coating suppliers with regional distribution networks.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Akzo Nobel NV positions itself as the dominant sustainable coatings architect in the packaging segment. The company’s active transition toward water-based and low-VOC coating portfolios aligns precisely with the regulatory trajectory in its core European and North American markets. This early alignment with compliance-driven demand reduces its retrofit risk and gives its packaging customers a procurement pathway that reduces their own regulatory exposure.

Axalta Coatings leverages its liquid and powder coating technology expertise to serve high-performance rigid packaging applications. Its strategic strength lies in translating industrial coating precision into food-grade and pharmaceutical-grade packaging specifications. This cross-sector capability gives Axalta access to two of the most margin-resilient packaging coatings end markets, where buyers prioritize performance over cost compression.

BASF SE approaches the packaging coatings market through its integrated chemical manufacturing advantage. Its ability to produce specialty resins, crosslinkers, and additives in-house reduces its raw material cost exposure — a structural advantage during periods of petrochemical price volatility. BASF’s scale also enables it to fund bio-based coating R&D at a level that smaller specialty coating suppliers cannot sustain, positioning it to lead the next formulation cycle.

Arkema Group differentiates through its acrylic polymer and specialty monomer capabilities, targeting flexible and functional packaging coatings. Its investment in bio-sourced acrylic acids and UV-curable chemistries places it at the intersection of two converging market forces — bio-based formulation demand and digital printing compatibility. Arkema’s technology assets position it to capture coating specification wins as converters upgrade packaging lines to meet both sustainability and digital production requirements.

Key Players

- Akzo Nobel NV

- Axalta Coatings

- BASF SE

- Arkema Group

- Berger Paints India Limited

- Chemetall

- Chugoku Marine Paints Ltd

- DowDuPont

- Evonik Industries AG

- HEMPEL A/S

- Henkel AG & Co. KGaA

- Jotun

- Kansai Paint Co. Ltd

Recent Developments

- In 2025, Axalta Coatings announced an all-stock merger of equals with AkzoNobel, creating a larger global coatings platform. Axalta’s 2025 10-K confirms the deal, dual HQ plan, shareholder/regulatory approvals, and expected close.

- In 2025, BASF SE Partnered with Metpack on home-compostable coated paper/board for food packaging, using BASF’s ecovio 70 PS14H6 coating; BASF says it is food-contact approved and offers liquid, fat, grease, and mineral-oil barrier properties.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.8 Billion |

| Forecast Revenue (2035) | USD 8.2 Billion |

| CAGR (2026-2035) | 5.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Epoxies, Acrylics, Polyurethane, Polyolefins, Polyester, Others), By Application (Rigid Packaging, Flexible Packaging, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Akzo Nobel NV, Axalta Coatings, BASF SE, Arkema Group, Berger Paints India Limited, Chemetall, Chugoku Marine Paints Ltd, DowDuPont, Evonik Industries AG, HEMPEL A/S, Henkel AG & Co. KGaA, Jotun, Kansai Paint Co. Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |