Quick Navigation

Report Overview

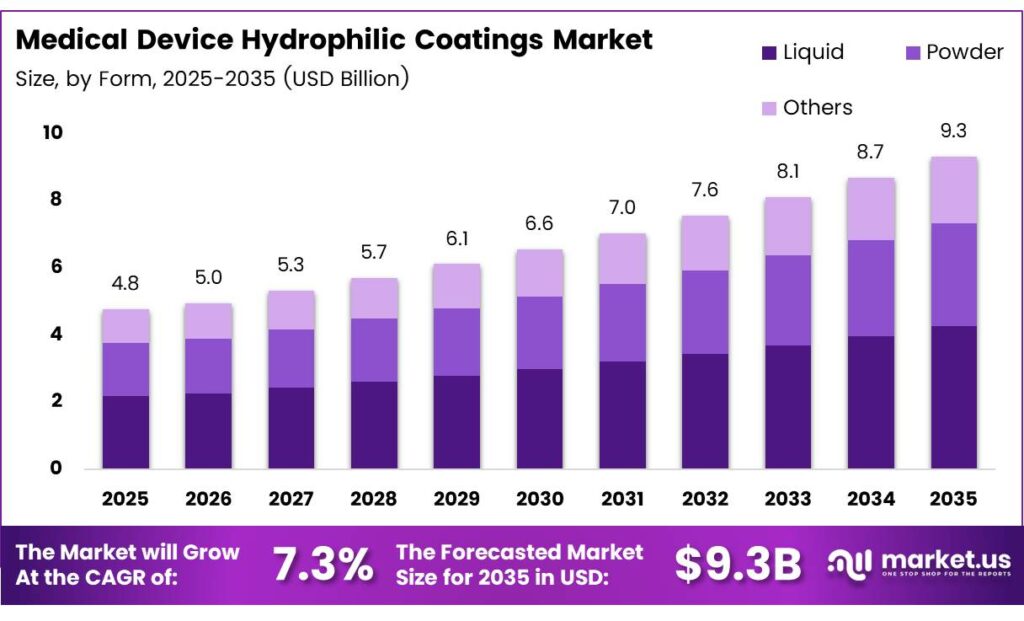

The Global Medical Device Hydrophilic Coatings Market size is expected to be worth around USD 9.3 billion by 2035 from USD 4.8 billion in 2025, growing at a CAGR of 7.3% during the forecast period 2026 to 2035.

Medical device hydrophilic coatings are specialized surface treatments applied to medical instruments to reduce friction. These coatings absorb water and create a slippery surface layer. Consequently, devices such as catheters, guidewires, and sheaths navigate through the body more smoothly with less tissue trauma.

Lubricant-impregnated hydrophilic catheter coatings reduced sliding friction during urethral insertion by more than 50% compared with an uncoated PVC catheter. Furthermore, a randomized clinical evaluation reported that 93% of participants preferred the hydrophilic-coated catheter over a gel-lubricated alternative, citing reduced urethral microtrauma and improved comfort.

OEM manufacturers integrate hydrophilic coatings as a key device differentiation strategy. Additionally, hospital procurement teams evaluate surface performance alongside clinical outcomes when selecting devices. This dual demand from device makers and healthcare systems expands the market opportunity for coating technology suppliers worldwide.

Key Takeaways

- The Global Medical Device Hydrophilic Coatings Market is valued at USD 4.8 billion in 2025 and is projected to reach USD 9.3 billion by 2035, growing at a CAGR of 7.3%.

- Ethoxylated Fatty Acid Amines dominate with a 39.5% market share in 2025.

- The Liquid segment leads with a 54.8% share of the market.

- Polypropylene (PP) holds the largest share at 31.9%.

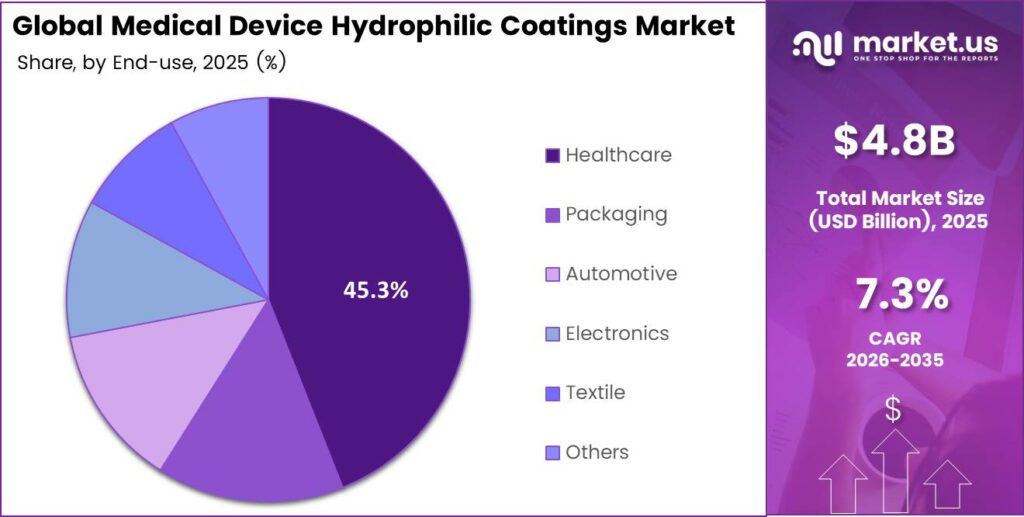

- The Healthcare segment accounts for 45.3% of the total market share.

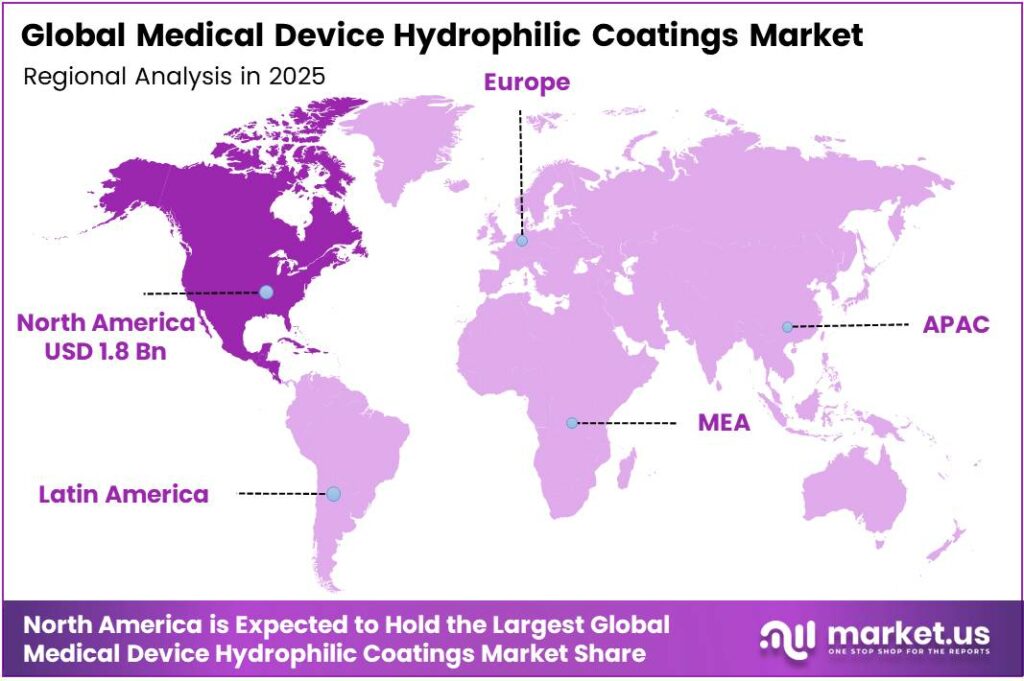

- North America dominates the regional landscape with a 38.1% share, valued at USD 1.8 billion.

By Product Analysis

Ethoxylated Fatty Acid Amines dominate with 39.5% due to superior lubricity performance and wide compatibility across medical-grade polymers.

In 2025, Ethoxylated Fatty Acid Amines held a dominant market position in the By Product segment of the Medical Device Hydrophilic Coatings Market, with a 39.5% share. These compounds deliver reliable wetting and lubrication performance across complex device geometries. Moreover, their strong compatibility with sterilization processes makes them a preferred choice among medical OEM formulators.

Glycerol Monostearate serves as a widely adopted hydrophilic additive in medical coating formulations. Its biodegradable profile and low toxicity appeal to manufacturers prioritizing biocompatible surface solutions. Additionally, glycerol monostearate supports smooth processing in both liquid and powder coating systems across diverse device applications.

Diethanolamides contribute functional lubricity and surface wetting performance in medical coating compositions. Formulators value these compounds for their cost efficiency and stable performance in aqueous coating environments. Consequently, diethanolamides maintain a steady presence across catheter and sheath coating product lines globally.

By Form Analysis

Liquid dominates with 54.8% due to ease of application and uniform surface coverage on complex catheter and guidewire geometries.

In 2025, Liquid held a dominant market position in the By Form segment of the Medical Device Hydrophilic Coatings Market, with a 54.8% share. Liquid formulations allow precise dip-coating and spray-coating processes on intricate device structures. Moreover, liquid coatings support consistent film thickness control, which is critical for meeting lubricity and biocompatibility standards.

Powder form coatings offer processing advantages in high-volume manufacturing environments. These formulations reduce solvent usage and support cleaner production workflows aligned with sustainability goals. Additionally, powder coatings demonstrate strong adhesion characteristics on select polymer substrates used in medical device manufacturing.

The Others form sub-segment captures specialty coating delivery formats, including gel-based and dispersion systems. These formats address unique application requirements for wearable and insertable device categories. Consequently, this sub-segment reflects demand for versatile coating formats beyond conventional liquid and powder technologies.

By Polymer Analysis

Polypropylene (PP) dominates with 31.9% due to its broad use in single-use medical devices and strong compatibility with hydrophilic coating chemistries.

In 2025, Polypropylene (PP) held a dominant market position in the By Polymer segment of the Medical Device Hydrophilic Coatings Market, with a 31.9% share. PP substrates are widely used in disposable catheters, syringes, and drainage systems. Moreover, their chemical resistance and processability make them highly compatible with a broad range of hydrophilic coating technologies.

Polyethylene (PE) serves as a key substrate in hydrophilic coating applications for flexible tubing and drainage device components. Its low surface energy requires surface activation before coating, which manufacturers address through plasma or chemical pretreatment. Additionally, PE substrates are favored in cost-sensitive single-use device segments.

Polyvinyl Chloride (PVC) remains a foundational substrate for catheter manufacturing globally. Hydrophilic coatings applied to PVC devices significantly reduce friction compared to uncoated surfaces, a fact confirmed in multiple clinical bench studies. Consequently, PVC continues to attract coating technology investment from major medical device suppliers.

By End Use Analysis

Healthcare dominates with 45.3% due to high-volume procedural demand for lubricious, biocompatible surface treatments across catheter and guidewire platforms.

In 2025, Healthcare held a dominant market position in the By End Use segment of the Medical Device Hydrophilic Coatings Market, with a 45.3% share. Hospitals and ambulatory surgery centers drive consistent demand for hydrophilic-coated catheters, guidewires, and endoscopic tools. Moreover, clinical emphasis on infection prevention and patient comfort reinforces healthcare as the primary end-use market.

The Packaging end-use segment leverages hydrophilic coating technologies to enhance the surface properties of medical packaging materials. These coatings improve moisture management and reduce static in sensitive device packaging environments. Additionally, packaging applications benefit from the same biocompatible additive chemistries used in device manufacturing.

The Automotive and Electronics end-use segments adopt hydrophilic surface technologies for moisture resistance and anti-fouling applications. These markets use coating chemistries developed in parallel with medical applications. Consequently, technology transfer between healthcare and industrial markets broadens the addressable market for hydrophilic coating suppliers.

Key Market Segments

By Product

- Ethoxylated Fatty Acid Amines

- Glycerol Monostearate

- Diethanolamides

- Others

By Form

- Liquid

- Powder

- Others

By Polymer

- Polypropylene (PP)

- Polyethylene (PE)

- Polyvinyl Chloride (PVC)

- Acrylonitrile Butadiene Styrene (ABS)

- Others

By End Use

- Healthcare

- Packaging

- Automotive

- Electronics

- Textile

- Others

Emerging Trends

PFAS-Free and Sustainability-Aligned Coating Formulations Gain Market Traction

Medical OEM supply chains increasingly shift toward PFAS-free, solvent-reduced hydrophilic coating platforms. Regulatory pressure and hospital sustainability mandates drive formulators to develop greener surface chemistry alternatives. Advanced hydrophilic coatings now achieve approximately a 30% reduction in catheter-associated complications, making sustainable formulations clinically viable replacements.

AI-Enabled Inspection and Nano-Engineered Coatings Reshape Manufacturing Standards

Manufacturers integrate AI-enabled inline coating inspection systems to ensure surface uniformity at scale. Additionally, researchers apply nano-engineered crosslinking systems that improve slip consistency and extend in-use lubricity retention. In bioinspired ultra-low-fouling coating studies, antibacterial slippery coatings achieved greater than 5 log reduction in bacterial adhesion over seven days, demonstrating the performance ceiling of next-generation surface engineering.

Drivers

Rising Minimally Invasive Procedure Volumes Accelerate Hydrophilic Coating Demand

Cardiovascular, neurovascular, and urology procedure volumes continue rising globally, creating strong demand for ultra-low-friction device navigation. Physicians require guidewires, catheters, and sheaths that reduce insertion force and lower tissue trauma. Clinical studies report a 64% relative risk reduction in urinary tract infections when using hydrophilic-coated intermittent catheters, reinforcing their value in reducing procedural complications.

OEM Differentiation and Infection Prevention Drive Advanced Surface Technology Adoption

Device OEMs invest in durable, particulate-resistant hydrophilic coatings to differentiate products in competitive surgical markets. Furthermore, a PVP/PEG hydrophilic composite coating on TPU catheter material reduced the coefficient of friction from approximately 0.40 on uncoated surfaces to around 0.03 after coating. This performance level supports hospital infection-prevention and complication-reduction goals.

Restraints

Stringent Biocompatibility Validation Requirements Extend Product Qualification Timelines

Regulatory agencies require exhaustive biocompatibility, extractables, leachables, and coating adhesion testing before device approval. Manufacturers face lengthy qualification timelines that delay product launches and increase development costs. Moreover, extractables and leachables testing demands specialized laboratory resources, creating barriers for smaller coating technology innovators entering the medical device supply chain.

Coating Durability Challenges Limit Performance in Complex Device Geometries

Hydrophilic coatings on complex device geometries face degradation risks from repeated flexing, hydration cycling, and shelf-life instability. Consequently, manufacturers must invest in advanced crosslinking and adhesion technologies to maintain coating integrity throughout device use. These technical and cost barriers slow adoption timelines, particularly for next-generation robotic and structural heart device platforms.

Growth Factors

Expansion into Structural Heart and Robotic Endovascular Platforms Opens New Growth Pathways

Hydrophilic coatings rapidly penetrate structural heart, electrophysiology, and robotic endovascular device categories. These high-growth platforms require advanced lubricious surface technologies for safe navigation in complex vascular anatomy. The same PVP/PEG-coated TPU catheter coating remained mechanically intact after 30 minutes of reciprocating sliding, demonstrating durability standards necessary for complex procedural environments.

Multi-Functional Coatings and Ambulatory Surgery Center Growth Expand Market Reach

Emerging demand for coatings that combine lubricity with antimicrobial, antithrombotic, or drug-eluting capabilities creates new product development opportunities. Additionally, in a patient-focused technical article, patients using hydrophilic-coated catheters report approximately a 60% reduction in pain and urethral discomfort. This patient satisfaction data drives disposable device adoption in ambulatory surgery centers and home-care healthcare markets.

Regional Analysis

North America Dominates the Medical Device Hydrophilic Coatings Market with a Market Share of 38.1%, Valued at USD 1.8 Billion

North America leads the global medical device hydrophilic coatings market, commanding a 38.1% share valued at USD 1.8 billion in 2025. The United States hosts the world’s largest concentration of medical device OEMs and coating technology suppliers. Moreover, FDA regulatory emphasis on biocompatible and infection-resistant device surfaces sustains strong demand for advanced hydrophilic coating solutions across the region.

Europe represents a mature and innovation-driven market for medical device surface technologies. Germany, France, and the UK lead procedural volume growth in minimally invasive cardiovascular and urology applications. Additionally, EU MDR compliance requirements push device manufacturers toward biocompatible hydrophilic coating platforms that meet evolving safety and performance standards.

Asia Pacific delivers the fastest growth trajectory in the global hydrophilic coatings market. China, Japan, India, and South Korea drive expanding hospital infrastructure investments and rising minimally invasive procedure volumes. Consequently, regional medical device manufacturing growth creates strong demand for locally supplied hydrophilic coating technologies and additive chemistry solutions.

Latin America presents an emerging growth opportunity for medical device hydrophilic coating suppliers. Brazil and Mexico lead regional demand growth driven by expanding public healthcare systems and rising procedural volumes. Additionally, increasing awareness of infection-prevention best practices in Latin American hospitals accelerates the adoption of hydrophilic-coated catheter and guidewire products.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

3M applies its advanced materials science expertise to develop high-performance hydrophilic coating technologies for the medical device sector. The company offers coating solutions targeting lubricity, durability, and sterilization stability across catheter, guidewire, and sheath applications. Moreover, 3M’s global supply chain and regulatory support capabilities make it a preferred coating partner for leading device OEMs worldwide.

BASF SE delivers a broad portfolio of specialty chemical and polymer additive solutions for medical device surface applications. The company focuses on biocompatible hydrophilic additive chemistries compatible with healthcare-grade polymers, including PVC, PP, and polyurethane substrates. Additionally, BASF invests in sustainable coating formulation platforms aligned with growing OEM demand for PFAS-free and solvent-reduced surface technologies.

Evonik Industries AG brings advanced polymer and specialty chemistry capabilities to the medical device hydrophilic coatings space. The company develops high-purity hydrophilic additive systems designed for rigorous biocompatibility and extractables-leachables compliance requirements. Consequently, Evonik’s technical service teams support OEMs through complex device qualification processes, strengthening long-term customer relationships across major global markets.

Clariant offers specialty additives and coating solutions targeting friction reduction and surface performance enhancement in medical device manufacturing. The company focuses on cost-effective hydrophilic coating chemistries that deliver consistent in-use lubricity across diverse device geometries and polymer substrates. Furthermore, Clariant supports customers with formulation expertise and regional technical teams serving North American, European, and Asia-Pacific device manufacturers.

Top Key Players in the Market

- 3M

- BASF SE

- Evonik Industries AG

- Clariant

- CRODA INTERNATIONAL PLC

- ADEKA CORPORATION

- LyondellBasell Industries Holdings BV

- Ampacet Corporation

- Arkema

- Kao Corporation

- Mitsubishi Chemical Group Corporation

- Nouryon

Recent Developments

- In 2025, BASF’s most relevant recent development was the launch/expansion of a biomass-balanced Ultrason PPSU grade. BASF explicitly positions Ultrason resins for medical technology alongside other high-performance uses, which matters because PPSU is widely used in durable, sterilizable medical components.

- In 2025, Evonik opened its largest medical device applications center in Shanghai, focused on R&D and processing of semi-finished components for bioresorbable medical devices. That is a concrete investment in capacity and application development for the medical-device market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.8 Billion |

| Forecast Revenue (2035) | USD 9.3 Billion |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Ethoxylated Fatty Acid Amines, Glycerol Monostearate, Diethanolamides, Others), By Form (Liquid, Powder, Others), By Polymer (Polypropylene (PP), Polyethylene (PE), Polyvinyl Chloride (PVC), Acrylonitrile Butadiene Styrene (ABS), Others), By End Use (Healthcare, Packaging, Automotive, Electronics, Textile, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | 3M, BASF SE, Evonik Industries AG, Clariant, CRODA INTERNATIONAL PLC, ADEKA CORPORATION, LyondellBasell Industries Holdings BV, Ampacet Corporation, Arkema, Kao Corporation, Mitsubishi Chemical Group Corporation, Nouryon |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |