Quick Navigation

Report Overview

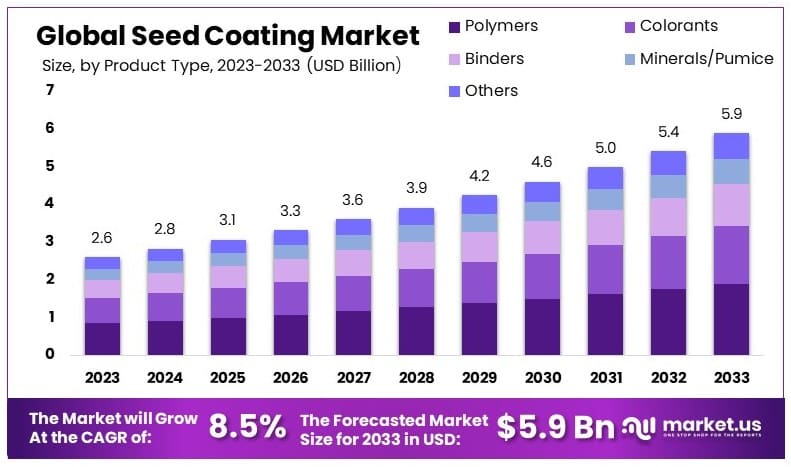

The Global Seed Coating Market size is expected to be worth around USD 5.9 Billion by 2033, from USD 2.6 Billion in 2023, growing at a CAGR of 8.5% during the forecast period from 2024 to 2033.

The Seed Coating Market deals with the enhancement of seed performance by applying chemical or biological agents directly to the seed surface.

This practice improves seed handling and sowing, enhances nutritional support, and protects against pests. The market is experiencing growth due to technological innovations in coating materials and an increasing global demand for high-yield crops.

The seed coating market is poised for significant growth, driven by rising global food demand and advances in agricultural technology. Food demand is set to increase by over 40% by 2040, and potentially by 59% to 98% by 2050. This surge necessitates enhanced agricultural productivity, making seed coatings an essential tool for farmers.

Seed coatings improve seed performance by protecting against pests, diseases, and harsh environmental conditions. They also enhance germination rates and seedling vigor, leading to better crop yields. As the global population grows and dietary habits shift, the pressure on agricultural systems intensifies, highlighting the importance of innovative solutions like seed coatings.

Regions with rapid population growth, particularly in Asia and Africa, are expected to drive demand. These areas face significant agricultural challenges and stand to benefit greatly from the advantages offered by seed coatings. Improved seed performance translates to higher crop productivity, essential for meeting rising food needs.

Key Takeaways

- The Seed Coating Market was valued at 2.6 Billion in 2023 and is expected to reach 5.9 Billion by 2033, with a CAGR of 8.5%.

- Polymers dominated the product type segment with 32.3%, crucial for improving seed performance.

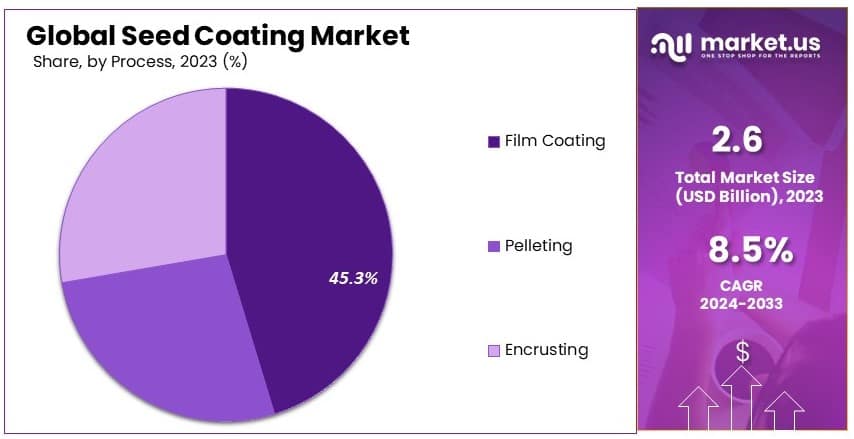

- Film Coating led the process segment with 45.3%, important for its efficiency in seed protection.

- Cereals & Grains application segment held 36.4%, essential for its role in global food supply.

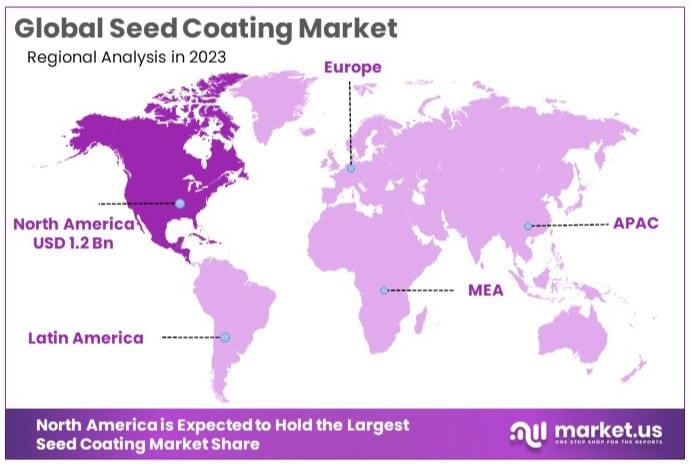

- North America dominated with 44.3% market share, driven by advanced agricultural practices.

Driving Factors

Increasing Global Food Demand Catalyzes Seed Coating Market Growth

The escalating global population, projected to reach 9.7 billion by 2050 according to the United Nations, is driving an urgent need for enhanced agricultural productivity. Seed coating technologies like polymer coatings and nutrient-infused coatings significantly improve seed germination rates, protect seeds from pests and diseases, and boost overall crop yields.

Bayer CropScience’s Poncho/VOTiVO seed treatment, for example, combines an insecticide and a biological nematicide for corn and soybeans, enhancing root health and increasing yields by up to 8%. This direct contribution of seed coating to improving agricultural output in response to rising food demand is a key driver of market growth.

Technological Advancements in Coating Materials Enhance Market Dynamics

Advancements in nanotechnology, biopolymers, and controlled-release formulations are transforming the seed coating market. These technologies enable precise delivery of nutrients and pest control agents right to the seed, minimizing the need for broad application of chemicals in the field.

Incotec’s Disco technology exemplifies this trend with its film coating process that improves seed flowability during planting and significantly reduces dust-off, thus lessening environmental impact. These innovations not only improve the effectiveness of seed coatings but also align with environmental conservation efforts, propelling market growth.

Adoption of Precision Agriculture Boosts Seed Coating Applications

The increasing adoption of precision agriculture techniques among farmers is a major factor driving the seed coating market. Precision farming aims to optimize resource use and maximize crop yields, with seed coatings playing a vital role by ensuring uniform seed placement, minimizing seed waste, and delivering targeted nutrition.

Technologies such as Precision Planting’s vSet seed meters, when used with coated seeds from providers like Corteva Agriscience, achieve over 99% singulation accuracy. This accuracy supports optimal plant spacing and enhanced yield potential, demonstrating the integral role of seed coatings in modern precision agriculture strategies.

Restraining Factors

Regulatory Hurdles and Environmental Concerns Restrain Seed Coating Market Growth

Stringent regulations on chemical usage in agriculture significantly impact the seed coating market. The EU’s Farm to Fork Strategy aims to reduce pesticide use by 50% by 2030, posing challenges for chemical-based seed coatings. Concerns about the impact of certain coatings, like neonicotinoids, on pollinators and biodiversity have led to bans or restrictions in various countries.

For instance, the EU’s ban on outdoor use of three neonicotinoids (imidacloprid, clothianidin, and thiamethoxam) has forced companies like Syngenta to reformulate their seed coatings, slowing market growth. These regulatory pressures and environmental concerns limit the adoption and development of seed coatings.

High Initial Investment and Farmer Education Restrain Seed Coating Market Growth

Adopting advanced seed coating technologies requires significant investment in equipment and training, which can be prohibitive for small-scale farmers, especially in developing countries. Additionally, there is a knowledge gap among farmers about the benefits of coated seeds versus traditional methods.

A study by the International Maize and Wheat Improvement Center (CIMMYT) in India found that despite clear yield benefits, only 25% of smallholder farmers used coated maize seeds, primarily due to cost concerns and lack of awareness. Addressing these issues through education and support can enhance adoption, but until then, high initial costs and limited knowledge continue to restrain the market.

Product Type Analysis

Polymers dominate with 32.3% due to their effectiveness in improving seed performance and protection.

In the Seed Coating Market, the segment by Product Type is prominently led by Polymers, which account for a 32.3% market share. Polymers are favored in seed coating due to their excellent properties in enhancing seed performance by providing better adherence of other coating materials and improving the delivery of active ingredients such as pesticides and nutrients. This enhances seed germination rates and seedling health, leading to improved crop yields.

Other segments within the Product Type category, including Colorants, Binders, Minerals/Pumice, and Others, also play significant roles. Colorants are used to differentiate seed types and enhance their aesthetic appeal, while Binders increase the durability of the coatings. Minerals and Pumice are added to improve the texture and weight of the seed coating, which can help with planting uniformity. These additional components are critical in customizing seed treatment solutions to meet specific agricultural needs and environments.

The dominance of Polymers is driven by the ongoing innovation in agricultural biotechnologies where efficiency and yield optimization are crucial. As farming practices evolve and the demand for high-quality agricultural products increases, the role of advanced seed coating materials like Polymers is expected to expand further. This growth will likely be complemented by advancements in other segments as well, as manufacturers continue to develop specialized products to address diverse agricultural challenges and opportunities.

Process Analysis

Film Coating dominates with 45.3% due to its precision and efficiency in seed treatment applications.

In the Seed Coating Market, segmented by Process, Film Coating holds the largest share at 45.3%. This process involves applying a thin layer of coating material to the seed, which is designed to enhance seed handling and performance without significantly altering its size or shape. The precision and efficiency of Film Coating make it highly desirable for applying various protective chemicals and growth enhancers in a controlled manner.

Other important processes in the market include Pelleting and Encrusting. Pelleting involves coating the seed with several layers to change its size and shape, making it easier to plant and increasing the accuracy of seed placement. Encrusting adds a thicker layer to the seed, providing more substantial protection and nutrient delivery. Each of these methods has specific applications based on crop type and planting technology.

The prominence of Film Coating is indicative of a shift towards more sophisticated agricultural practices where precision agriculture plays a key role. As farmers and agricultural companies continue to seek more efficient and effective planting solutions, the demand for advanced seed coating processes like Film Coating is expected to grow. This trend is likely to drive innovations within Pelleting and Encrusting as well, as the market responds to diverse needs for seed treatment across various agricultural sectors.

Crop Type Analysis

Cereals & Grains dominate with 36.4% due to their fundamental role in global agriculture.

In the Crop Type segment of the Seed Coating Market, Cereals & Grains lead with a market share of 36.4%. This segment’s dominance stems from the pivotal role that crops such as wheat, corn, and rice play in global food security. Seed coating technologies are particularly valuable in enhancing the growth and yield of these staple crops by providing protection against pests and diseases and improving nutrient availability.

Other significant crop types in the seed coating market include Pulses & Oilseeds, Fruits & Vegetables, and Others. Pulses and Oilseeds benefit from seed coatings that improve germination and seedling vigor, which is critical for crops like soybeans and canola. Fruits and Vegetables use seed coatings to ensure uniform germination and reduce the risk of disease, which is crucial for high-value crops.

The continued dominance of Cereals & Grains is likely to drive further advancements in seed coating technologies, as these crops are essential to meeting the growing global demand for food. Innovations in seed coating for Pulses, Oilseeds, and Fruits & Vegetables are also expected to increase, reflecting the expanding need for agricultural efficiency and productivity in a variety of cropping systems. This growth underlines the importance of tailored seed treatment solutions across different agricultural sectors to enhance overall crop performance and sustainability.

Key Market Segments

By Product Type

- Polymers

- Colorants

- Binders

- Minerals/Pumice

- Others

By Process

- Film Coating

- Pelleting

- Encrusting

By Crop Type

- Cereals & Grains

- Pulses & Oilseeds

- Fruits & Vegetables

- Others

Growth Opportunities

Customized Regional Solutions Offer Growth Opportunity

The diversifying impacts of climate change across different regions create a robust demand for tailored seed coating solutions. Companies have the opportunity to innovate by developing seed coatings that address specific regional challenges—such as drought resistance for arid areas in Sub-Saharan Africa, cold tolerance for cooler climates in Northern Europe, or salt tolerance for coastal regions facing salinity issues due to rising sea levels.

Corteva Agriscience’s LumiGEN technology, which offers customized fungicide and insecticide seed treatments based on local conditions, exemplifies this trend. Such targeted solutions not only improve crop resilience and yield in varying climatic conditions but also enhance the market adaptability and reach of seed coating products, driving growth through specialization.

Digital Integration and Traceability Offer Growth Opportunity

The integration of digital tools with seed coatings marks a significant advancement in agricultural technology. By embedding sensors or RFID tags within seed coatings, companies can provide farmers with valuable real-time data about soil conditions, germination rates, and overall plant health. This technology supports precision farming, enabling more informed decision-making and optimizing agricultural outputs.

Additionally, the demand for traceability in the food supply chain is increasing among consumers who want to know more about the origin and handling of their food products. Bayer’s FieldView platform illustrates how digital integration with coated seeds can enhance performance tracking from planting to harvest, meeting consumer demands and pushing the boundaries of what seed coatings can accomplish in modern agriculture. This convergence of technology and traditional farming practices opens new avenues for market growth and development in the seed coating industry.

Trending Factors

Nanotechnology in Seed Coatings Are Trending Factors

Nanotechnology is revolutionizing the seed coating market by enabling advanced features such as controlled release of nutrients and pesticides, enhanced seed surface area for better soil contact, and improved water uptake. A study in ACS Sustainable Chemistry & Engineering showed that nano-silica coated rice seeds improved germination by 20% and seedling vigor by 31%.

Startups like Nanografen are exploring graphene-based coatings that enhance seed vitality and stress resistance. These advancements significantly boost seed performance, leading to higher yields. The integration of nanotechnology in seed coatings is expected to expand the market by offering innovative solutions that enhance agricultural productivity and sustainability.

Multi-functional Coatings Are Trending Factors

The trend towards multi-functional seed coatings is transforming the seed coating market. These ‘all-in-one’ coatings combine pest control, nutrient delivery, moisture regulation, crop protection chemicals and plant growth promotion, reducing the need for multiple field applications.

For instance, Syngenta’s Vibrance Trio for cereals combines three fungicides with different modes of action, a polymer for dust reduction, and a nutrient package, providing comprehensive early-season protection and vigor. This approach simplifies the planting process and enhances seed performance, making it highly attractive to farmers. The demand for multi-functional coatings is expected to grow, driving market expansion by offering efficient, cost-effective, and high-performing agricultural solutions.

Regional Analysis

North America Dominates with 44.3% Market Share in the Seed Coating Market

North America’s leading 44.3% market share in the seed coating market, valued at USD 1.1518 billion, is propelled by advanced agricultural technologies and a strong focus on crop yield enhancements. The region’s sophisticated farming practices and the widespread adoption of biotech crops necessitate high-quality seed treatments, including coatings that improve seed performance and protection. Additionally, the presence of major agricultural biotech corporations, which invest heavily in research and development, drives innovation and application in seed coating technologies.

The agricultural sector in North America benefits from high levels of mechanization and technological integration, which includes precision farming that heavily utilizes coated seeds for uniformity and efficiency. Environmental conditions varying across the continent also necessitate seeds that are tailored to different climates and soil types, increasing the demand for specialized seed coatings. The regulatory environment in North America further supports the development and safe use of agricultural inputs, including seed coatings.

Regional Market Share Analysis:

- Europe: Holds approximately 26.7% of the market. Europe’s market is driven by stringent regulations on crop protection chemicals, which increase the demand for alternative solutions like seed coatings that offer protection with reduced chemical usage.

- Asia Pacific: Accounts for 21.5% of the market share. Rapid agricultural development in countries like China and India, coupled with the need to improve crop yields for a growing population, fuels the demand for seed coatings.

- Middle East & Africa: This region represents about 3.6% of the market, with potential growth driven by agricultural expansion and the need to combat harsh climatic conditions that affect seed viability and productivity.

- Latin America: With a market share of 3.9%, growth in this region is spurred by increasing agricultural output and the adoption of modern farming techniques that integrate seed coating technologies to enhance crop resilience and yield.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

The Seed Coating Market features key players with strong market influence. Bayer and Syngenta lead the market with their advanced technologies and extensive distribution networks. BASF and Clariant International leverage their innovative solutions and global reach to maintain a competitive edge.

Chromatech Incorporated and Incotec Group focus on specialized coatings and strategic partnerships. DOW Agrosciences and Monsanto emphasize research and development to drive product innovation. Arysta Lifescience and Nufarm maintain robust market positions through diverse product portfolios and strategic collaborations.

DuPont and FMC are recognized for their strong customer relationships and market-driven approaches. Sumitomo Chemical invests heavily in sustainable practices and advanced technologies. These companies collectively drive market growth by ensuring high-quality seed coatings, meeting global agricultural demands.

Their strategic positioning, strong supply chains, and commitment to innovation set industry standards and influence market trends. Through continuous improvement and strategic initiatives, these market leaders shape the future of the seed coating market.

Market Key Players

- Bayer

- Syngenta

- BASF

- Clariant International

- Chromatech Incorporated

- Incotec Group

- DOW Agrosciences

- Monsanto

- Arysta Lifescience

- Nufarm

- Dupont

- FMC

- Sumitomo Chemical

Recent Developments

- November 2023: Lucent Bio, an innovative agricultural technology company, has secured over $3.6 million in funding from PacifiCan through the Business Scale-up and Productivity program. This funding will be used to accelerate the development and commercialization of Nutreos, Lucent Bio’s biodegradable and microplastic-free seed coating technology.

- October 2023 saw a recovery with Clariant’s revenue in the seed coating sector rising to CHF 1.2 billion, aided by the successful execution of their order book in the Catalysts business and improved pricing strategies

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 2.6 Billion |

| Forecast Revenue (2033) | USD 5.9 Billion |

| CAGR (2024-2033) | 8.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Polymers, Colorants, Binders, Minerals/Pumice, Others), By Process (Film Coating, Pelleting, Encrusting), By Crop Type (Cereals & Grains, Pulses & Oilseeds, Fruits & Vegetables, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Bayer, Syngenta, BASF, Clariant International, Chromatech Incorporated, Incotec Group, DOW Agrosciences, Monsanto, Arysta Lifescience, Nufarm, Dupont, FMC, Sumitomo Chemical |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The global seed coating market is projected to grow from USD 2.6 billion in 2023 to USD 5.9 billion by 2033, at a CAGR of 8.5% during the forecast period.

Regions with rapid population growth, particularly Asia and Africa, are expected to drive demand due to their significant agricultural challenges and need for improved crop productivity.

Key players include Bayer, Syngenta, BASF, Clariant International, Chromatech Incorporated, Incotec Group, DOW Agrosciences, Monsanto, Arysta Lifescience, Nufarm, Dupont, FMC, and Sumitomo Chemical.

Opportunities include developing customized regional solutions to address specific agricultural challenges and integrating digital tools for real-time data and traceability in farming.