Quick Navigation

Report Overview

The Global Leavening Agents Market size is expected to be worth around USD 9.9 billion by 2035 from USD 6.5 billion in 2025, growing at a CAGR of 4.0% during the forecast period 2026 to 2035.

Leavening agents are substances that cause dough and batter to rise by producing gas during mixing, baking, or fermentation. They play a critical role in delivering texture, volume, and consistency across baked goods, snacks, and specialty food products. Moreover, leavening systems span chemical, biological, and physical forms depending on the application.

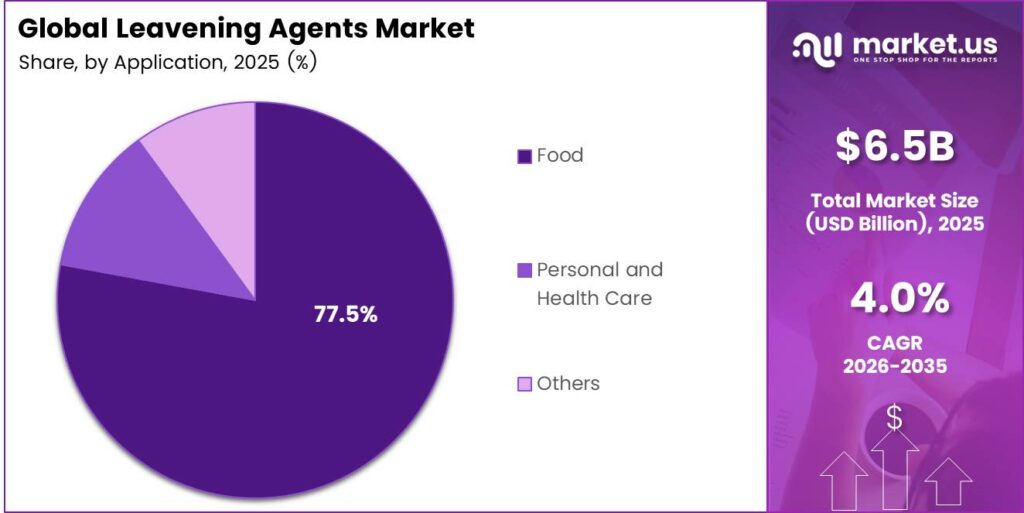

The food processing industry accounts for the largest share of leavening agent demand, at 77.5% of total market application. Rapid urbanization, busier consumer lifestyles, and the surge in packaged bakery consumption continue to push manufacturers to scale up standardized leavening solutions. Additionally, foodservice and quick-service restaurant chains amplify volume-based procurement.

India’s sodium bicarbonate imports rose 10% YoY to 44 KMT in FY2024–25, reflecting demand growth beyond current domestic output and creating opportunities for global suppliers. As of 31 March 2025, India’s installed capacity stood at 490 K MTPA, with 360 K MTPA production and 73% utilization, indicating strong supply infrastructure with further room for efficiency-driven growth.

Chemical leaveners such as baking powder, baking soda, and ammonium bicarbonate dominate commercial baking due to their reliable, fast-acting gas release. Biological agents, particularly yeast and sourdough cultures, serve premium and artisanal segments. Consequently, manufacturers offer both conventional and clean-label formulations to serve a wide range of food producers globally.

Key Takeaways

- The Global Leavening Agents Market is valued at USD 6.5 billion in 2025 and is projected to reach USD 9.9 billion by 2035 at a CAGR of 4.0% during the forecast period 2026 to 2035.

- The Chemical segment holds the dominant share at 57.3% in 2025.

- The Food segment leads with an 77.5% market share in 2025.

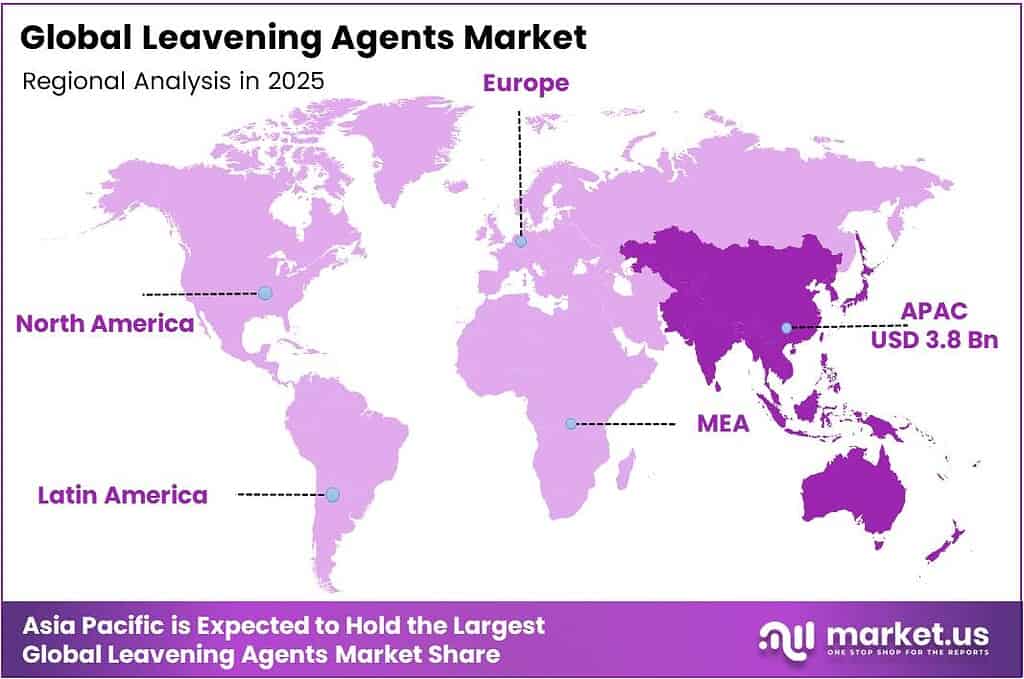

- Asia Pacific dominates the regional landscape with a 38.5% market share, valued at USD 3.8 billion.

By Form Segment Analysis

Chemical leavening agents dominate with 57.3% due to their consistent gas release performance and wide industrial compatibility.

In 2025, Chemical leavening agents held a dominant market position in the By Form segment of the Leavening Agents Market, with a 57.3% share. Chemical agents such as baking powder, baking soda, and ammonium bicarbonate deliver precise, reliable leavening in high-speed industrial bakeries. Moreover, their shelf stability and ease of integration make them the preferred choice across large-scale food manufacturers globally.

Biological leavening agents, including yeast and sourdough starters, serve the premium and artisanal baking segment. These agents produce complex flavors and natural fermentation benefits that appeal to health-conscious consumers. Additionally, growing demand for clean-label and organic baked goods drives increased interest in biological formulations across specialty retail and foodservice channels.

Others in this segment include physical leavening methods such as air and steam, used primarily in specific pastry and confectionery applications. These methods suit delicate products where chemical or biological agents could alter flavor or texture. However, their application scope remains narrow compared to chemical and biological agents in mainstream commercial production.

By Application Segment Analysis

Food applications dominate with 77.5% due to leavening agents being a core functional ingredient across all baked and processed food categories.

In 2025, Food held a dominant market position in the By Application segment of the Leavening Agents Market, with an 77.5% share. Bakery products, snacks, ready meals, and convenience foods collectively drive this dominance. Furthermore, rising global demand for packaged bread, biscuits, cakes, and pastries continues to increase the consumption of both chemical and biological leavening ingredients.

Personal and Health Care applications represent a smaller but growing share of leavening agent use. Sodium bicarbonate, in particular, finds application in antacids, toothpaste, and skin care formulations. Consequently, the personal care segment benefits from the multipurpose nature of chemical leavening compounds, especially as natural and mild ingredient trends gain momentum in consumer health products.

Others include industrial and non-food applications such as cleaning products, fire suppressants, and agricultural uses. These applications draw primarily on sodium bicarbonate’s chemical properties. However, their contribution to overall leavening agent market revenue remains limited, as food processing continues to drive the vast majority of global demand and production capacity.

Key Market Segments

By Form

- Chemical

- Biological

- Others

By Application

- Food

- Personal and Health Care

- Others

Emerging Trends

Double-Acting Baking Powders Gain Ground in Industrial High-Speed Production

Double-acting baking powders are becoming the standard choice for industrial bakeries running high-speed production lines. These systems release gas in two controlled stages, giving manufacturers precise timing and consistent product rise. Moreover, their reliability reduces waste and improves throughput in automated baking environments, making them a go-to solution for large-scale commercial food processors.

Microbial Strain Engineering Advances Flavor and Shelf-Life Performance

Advances in microbial strain engineering allow leavening manufacturers to develop yeast strains with enhanced flavor profiles and improved shelf stability. These innovations support the growing demand for premium, artisanal-style bakery products at a mass-market scale. Additionally, industry stakeholders push toward decarbonized and localized production systems to meet Scope 3 emission targets and satisfy sustainability commitments across global supply chains.

Drivers

Surging Bakery Demand and Urbanization Accelerate Leavening Agent Consumption

Rising urban populations and busier consumer lifestyles fuel strong global demand for packaged bakery products and convenience foods. Supermarkets, quick-service restaurants, and foodservice operators require consistent, high-volume leavening solutions to meet production targets. Soda ash serves as a core upstream raw material for sodium bicarbonate production, with monthly official U.S. supply statistics tracked through 2025, confirming a stable feedstock base supporting the leavening ingredient supply chain.

Clean-Label Mandates and Dietary Trends Drive Specialized Formulation Needs

Regulatory bodies and health-focused retailers increasingly mandate clean-label, natural, and allergen-free ingredient declarations on packaged foods. This shift drives leavening manufacturers to develop specialized biological and gluten-free formulations that deliver equivalent texture and volume. Furthermore, rising adoption of low-carb and gluten-free diets creates demand for engineered leavening systems that perform effectively without traditional wheat-based ingredients.

Restraints

Raw Material Supply Concentration Creates Pricing and Geopolitical Risk

Leavening agent manufacturers depend heavily on concentrated chemical raw material sources, particularly sodium bicarbonate and soda ash. Soda ash represents 2% of the total USD 39 billion U.S. nonfuel mineral industry, reflecting its significant economic scale as a feedstock. Geopolitical disruptions, trade policy changes, and commodity price swings, therefore, expose manufacturers to supply shortfalls and unpredictable input cost increases.

Formulation Sensitivity Causes Inconsistent Quality in Variable Processing Conditions

Leavening agents react sensitively to temperature, humidity, and processing variations during mixing, proofing, and baking. These sensitivities cause inconsistent gas release, affecting product rise, texture, and final quality. Consequently, food manufacturers must invest in tightly controlled production environments and technical support from ingredient suppliers to maintain output consistency, which increases operational complexity and cost, particularly for mid-sized bakers.

Growth Factors

Asia-Pacific Manufacturing Hubs and Frozen Dough Innovation Unlock New Market Potential

Regional manufacturing hubs across Asia-Pacific reduce transit spoilage risks and allow leavening ingredient suppliers to serve local bakery networks more efficiently. According to India’s Ministry of Chemicals and Fertilizers, 100% FDI is permitted under the automatic route in the chemicals sector, which actively encourages foreign investment into leavening and food additive production facilities in the region. This policy creates a favorable environment for capacity expansion.

Sourdough Scaling and Strategic Acquisitions Expand Biological Leavening Portfolios

Commercial scaling of sourdough and organic fermentation solutions enables producers to bring artisanal-style leavening into mass-market channels. Additionally, the development of cold-tolerant and high-osmotic-pressure yeast strains for frozen dough applications opens premium product segments. Strategic acquisitions of specialized biological formulators allow major ingredient companies to quickly expand their portfolios across high-growth emerging markets, accelerating both innovation and geographic reach.

Regional Analysis

Asia Pacific Dominates the Leavening Agents Market with a Market Share of 38.5%, Valued at USD 3.8 Billion

Asia Pacific leads the global leavening agents market, holding a 38.5% share valued at USD 3.8 billion in 2025. The region’s dominance stems from its large-scale bakery manufacturing base, rising urban middle-class consumption, and strong government support for food processing investment. Moreover, countries such as China, India, and Japan drive consistent volume demand across both chemical and biological leavening categories.

North America represents a mature, innovation-driven market for leavening agents, supported by high per-capita bakery consumption and a well-established food processing infrastructure. The United States leads regional demand, particularly for baking powder and specialty yeast products. Additionally, clean-label and organic leavening solutions gain strong traction among health-focused consumers and premium bakery brands across the region.

Latin America shows moderate growth in leavening agent demand, supported by expanding bakery retail networks and rising packaged food consumption in Brazil and Mexico. Urbanization and rising disposable incomes drive increased adoption of commercial baking ingredients. However, currency volatility and import dependency on specialty leavening ingredients can constrain market growth for smaller regional food manufacturers operating on tight margins.

The Middle East and Africa present emerging growth potential for leavening agents, driven by a young population, rising bread consumption, and expanding commercial bakery sectors in GCC countries and South Africa. Moreover, increasing foreign investment in food processing infrastructure supports the local availability of both chemical and biological leavening ingredients. However, import reliance and supply chain gaps remain key challenges across parts of the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Archer Daniels Midland Co. operates as one of the world’s largest agricultural processors and food ingredient suppliers. The company serves the leavening agents market through its extensive yeast and fermentation ingredient portfolio, supplying both biological and specialty leavening solutions to commercial bakeries globally. Its broad distribution network and integrated supply chain give it a strong competitive position across North America and international markets.

Associated British Foods PLC holds a leading position in the global yeast and baking ingredient market through its ingredients division. The company supplies a comprehensive range of yeast products, baking powders, and functional leavening systems to industrial and artisanal food producers. Moreover, its strong research and development capabilities allow it to continuously improve fermentation performance, flavor profiles, and clean-label compliance for evolving customer requirements.

Cargill, Inc. delivers a wide range of food ingredient solutions, including leavening systems tailored for large-scale baking operations. The company leverages its global sourcing infrastructure to provide consistent, high-quality chemical and biological leavening ingredients across multiple geographies. Additionally, Cargill focuses on sustainable ingredient sourcing and custom formulation services, enabling food manufacturers to meet both performance standards and environmental responsibility goals.

Corbion N.V. specializes in biobased ingredients and fermentation-derived solutions, making it a key player in the biological leavening agents segment. The company develops advanced sourdough systems, yeast-based solutions, and clean-label leavening blends that meet growing consumer demand for natural food ingredients. Furthermore, Corbion’s investment in biotechnology and sustainable production methods strengthens its position as an innovation leader in the global leavening ingredient market.

Top Key Players in the Market

- Archer Daniels Midland Co.

- Associated British Foods PLC

- Cargill, Inc.

- Corbion N.V.

- Kerry Group PLC

- Puratos Group NV

- Koninklijke DSM N.V.

- Stern-Wywiol Gruppe GmbH & Co. KG

Recent Developments

- In 2025, ADM offers bakery mixes, bases, concentrates, flours, emulsifiers, and ingredients supporting leavened products. These often work alongside leavening agents for texture and volume in baked goods. ADM launched an online storefront to improve access to ingredients for U.S. food producers, enhancing supply chain efficiency for bakers.

- In 2025, ABF’s ingredients division (via AB Mauri and ABF Ingredients/ABFI) is a major player in bakery ingredients, including yeast, bread improvers, dough conditioners, bakery mixes, and enzymes that support leavening and dough performance. ABF announced the acquisition of Hovis Group Limited (a UK bread/bakery business) from Endless LLP.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 6.5 Billion |

| Forecast Revenue (2035) | USD 9.9 Billion |

| CAGR (2026-2035) | 4.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Chemical, Biological, Others), By Application (Food, Personal and Health Care, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Archer Daniels Midland Co., Associated British Foods PLC, Cargill Inc., Corbion N.V., Kerry Group PLC, Puratos Group NV, Koninklijke DSM N.V., Stern-Wywiol Gruppe GmbH & Co. KG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |