Quick Navigation

Report Overview

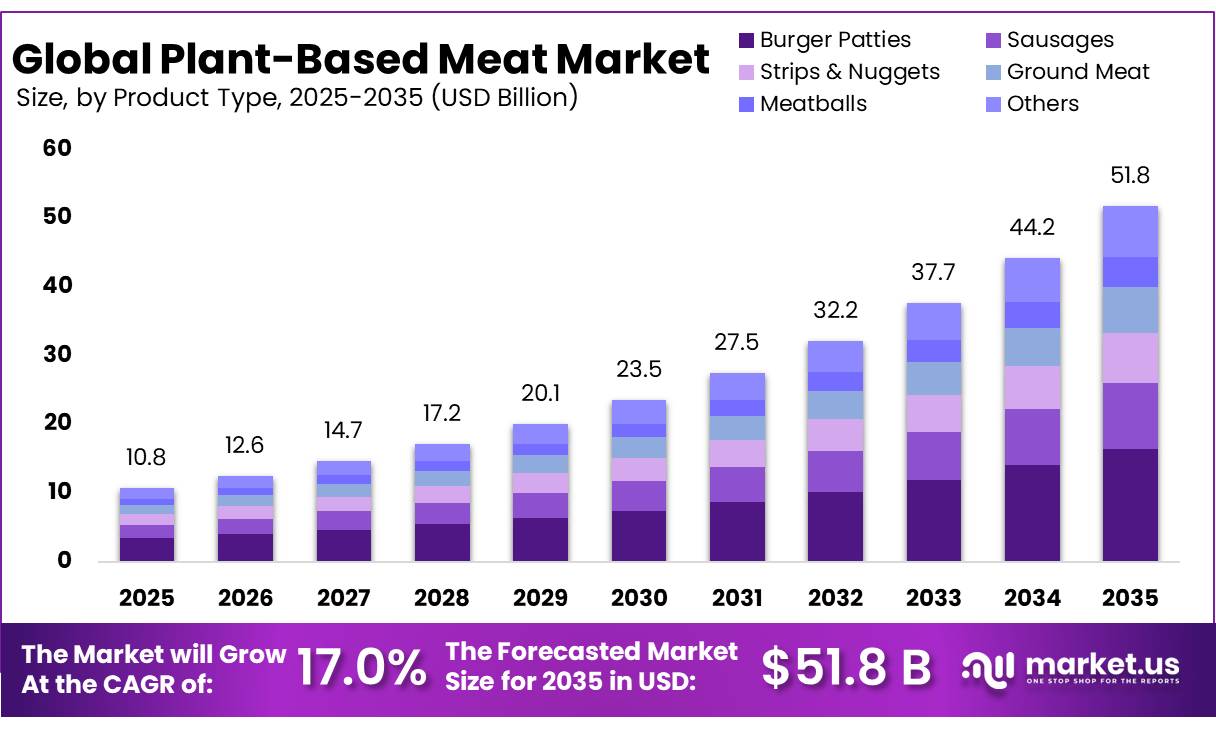

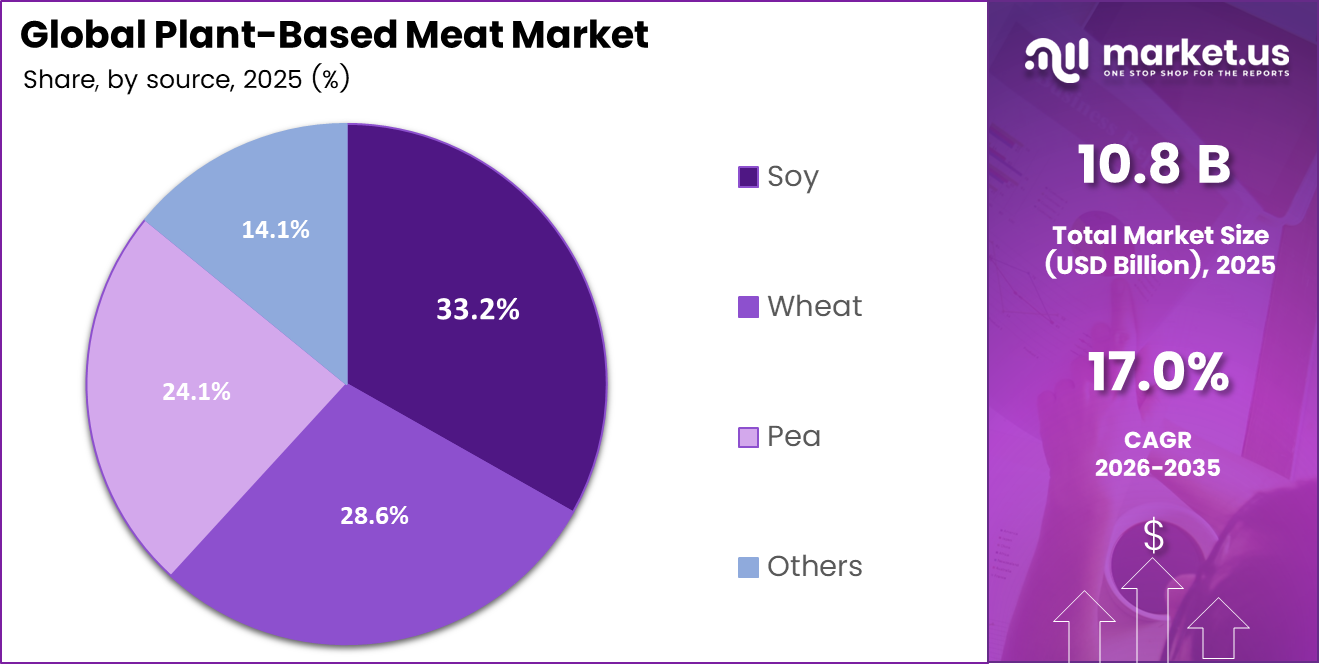

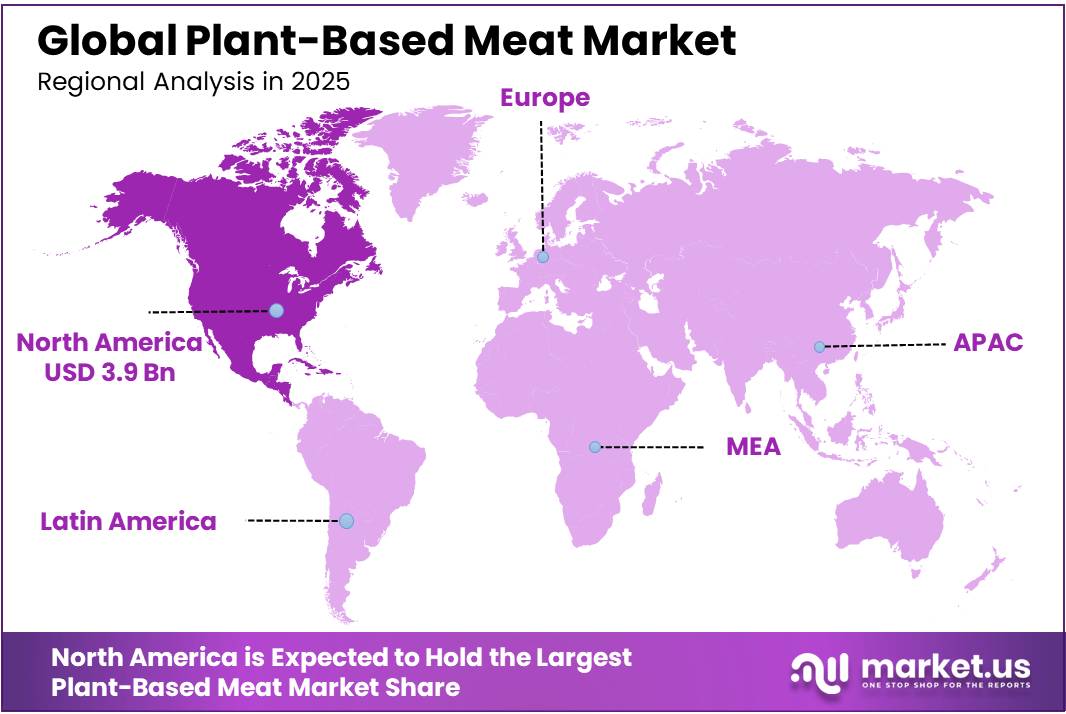

The Global Plant-Based Meat Market was valued at USD 10.08 billion in 2025, and between 2026 and 2035, this market is estimated to register a CAGR of 17.0%, reaching about USD 51.8 billion by 2035. North America held a dominant market position, capturing more than a 36.2% share, holding USD 3.9 billion in revenue.

The plant-based meat market is growing rapidly as consumers prioritise sustainability, health, and improved nutrition. Governments in Canada, Germany, and India are supporting research through grants and financial aid, while consumers increasingly choose products made from wheat, pulses, and soy. These alternatives provide protein, fibre, vitamins, and antioxidants with less saturated fat. In the UK, Food Standards Agency polling found that 27% of adults eat plant-based meat, and 73% of these consumers eat it at least 2–3 times per month.

Demand is also being driven by institutional food policies and industrial decarbonisation targets. Companies and public institutions are replacing animal protein to reduce carbon emissions and the land and water required for livestock production.

- A 2024 Smart Protein survey found that 48% of UK meat consumers had reduced their annual meat intake, while 25% identified as flexitarian, 7% as vegetarian, 4% as pescatarian, and 2% as vegan. The main reasons were health at 48%, environmental concerns at 29%, and animal welfare at 25%.

Future growth will depend on improvements in taste, texture, and affordability. High-moisture extrusion will support realistic whole-cut products such as chicken breasts and steaks, while precision fermentation will combine plant proteins with animal-identical fats and heme. As production expands, these technologies are expected to support price parity with conventional meat, attract mass-market consumers, and accelerate growth in areas such as plant-based seafood.

Key Takeaways

- The plant-based meat market was valued at USD 10.8 billion in 2025.

- The global plant-based meat market is projected to grow at a CAGR of 17.0% and is estimated to reach USD 51.8 billion by 2035.

- Burger patties are the most popular product in the global alternative protein industry, making up 31.8% of the market.

- Soy is the main raw material used in creating textured plant-based products, taking up 33.2% of the market because it holds water very well.

- Beef Alternatives: Products replicating beef lead the market, accounting for 35.8% of total volume.

- Retail Channels: Supermarkets and hypermarkets remain the primary sales venues with a 36.9% market share.

- Driven by mature retail landscapes and extensive food-tech innovation pipelines, North America stands as the largest geographical territory with a 36.2% share.

- The industry behavior is shifting rapidly from a highly fragmented startup ecosystem into a consolidated tier-one corporate oligopoly market by legacy meat titans.

Product Type Analysis

Burger Patties represent the dominant Segment in the Market.

The burger patty category has become the top choice, holding a leading 31.8% of the global market. This strong position is because plant-based meat substitutes don’t need as complicated a structure as whole muscle cuts. Food companies use a system that focuses on cost and ease, where standard twin-screw extrusion machines can mix plant-based ingredients effectively without needing complex texturing.

The strips and nuggets category is growing the fastest, expected to increase at a strong CAGR of 14.5%. This growth is driven by changes in the food service industry and corporate cafeterias aligning with public sector efforts to reduce carbon emissions. These facilities need pre-measured, highly stable alternative proteins that work well in fast-paced, automated kitchens.

Source Analysis

Soy protein dominates global values.

Soy-based meat products continued to be the top choice in the raw ingredient category, taking up an absolute 33.2% of the total market. Soy protein isolates and concentrates are still the main ingredients used in industry because of their well-developed global supply chain and lower costs for buying raw materials. Soy has a great balance of amino acids and can hold a lot of water, which makes it easy for factories to process large amounts.

This ease of processing gives manufacturers a quick return on investment because the product behaves predictably in high-torque texturizing machines. The pea protein group is growing the fastest, expected to grow at a compound annual growth rate (CAGR) of 24.1%, and is becoming a major player in the raw material market.

Meat Type Analysis

Beef Substitutes Command Volume Dominance

Plant-based beef dominates the market, accounting for 35.8% of total volume. This prominent position is partly driven by worldwide consumer movements to reduce the heavy environmental imprint associated with traditional animal husbandry, such as greenhouse gas emissions and extensive land use.

To successfully appeal to the mainstream flexitarian demographic, food technology businesses use precise ingredient formulations, such as plant-derived oils and natural binders, to mimic the marbled look, savory umami flavor profile, and distinct juiciness of animal fat.

Distribution Channel Analysis

Supermarkets and Hypermarkets Held a Major Share of the Battery Separator Market.

Supermarkets and hypermarkets dominate the distribution channel, accounting for 36.9% of global alternative protein sales. This market leadership is partly due to their advanced cold storage facilities and large shelf footprints in densely populated urban areas, which enable them to maintain continuous frozen and chilled supply chains.

The dominance of this supermarket industry is bolstered by aggressive retail marketing methods such as loyalty club promotions, in-store tasting events, and seasonal discounts. These large-scale shops use vast customer purchase data to improve their inventory, ensuring that high-demand items such as burger patties and sausages are consistently available.

Key Market Segments

By Product Type

- Burger Patties

- Sausages

- Strips & Nuggets

- Ground Meat

- Meatballs

- Others

By Source

- Soy

- Wheat

- Pea

- Others

By Meat Type

- Beef

- Chicken

- Pork

- Others

By Distribution Channel

- Supermarkets & Hypermarkets

- Food Service

- Online Retail

- Others

Opportunity

The institutional procurement channel, including EU government cafeterias, hospitals, school meal programs, and military food supply chains, remains a largely underdeveloped opportunity for plant-based meat producers. A 2026 modeling study conducted by Bryant Research for ProVeg International estimated that increasing the plant-based share of EU public food procurement to 85% could deliver €11.61 billion in annual societal benefits.

These gains comprise €3.16 billion in direct food-budget savings, €4.37 billion in avoided environmental costs, and €4.08 billion in reduced healthcare expenditure. The modeled transition would also prevent 8.89 million tonnes of CO₂e emissions each year and approximately 396,187 long-term obesity cases. Although no EU-wide procurement mandate currently exists, the opportunity is becoming increasingly viable as Farm-to-Fork objectives, carbon-neutrality commitments, and public-sector budget pressures converge.

Public institutions across the EU28 are estimated to serve more than 4 billion meals annually. Supplying plant-based products to even 15–20% of these meals, at an incremental supplier value of €0.80–1.20 per portion, could create €500–800 million in annual revenue for early entrants. Success will depend on tender-compliant manufacturing, procurement traceability, dietary labeling, bulk-service formats, centralized-kitchen compatibility, and shelf-stable or frozen product portfolios.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Public Sector & Institutional Procurement Monetization | +2.8% | EU, North America, APAC public systems | Medium term (2–4 years) |

| APAC Emerging Market TAM Penetration | +3.2% | India, Southeast Asia, China Tier-2/3 cities | Medium term (2–4 years) |

| Hybrid Protein Architecture (Plant + Precision Fermentation) | +2.5% | North America, EU, Singapore/ANZ | Long term (≥ 4 years) |

| Functional Health & Nutraceutical Positioning | +2.1% | North America, UK, Germany, Australia | Short–Medium term (1–3 years) |

| B2B/Foodservice White-Label Roll-Up Strategy | +1.8% | North America core, EU, Gulf Cooperation Council | Short term (≤ 2 years) |

| Clean-Label Whole-Muscle & Mycoprotein Formats | +1.5% | North America, UK, Nordic markets | Medium term (2–4 years) |

Drivers

The growing incidence of chronic disease is creating a structural demand driver for plant-based meat through both individual dietary change and healthcare-led nutrition policy. Roughly two in five U.S. adults live with obesity, while cardiovascular disease remains the leading cause of death worldwide. Clinical evidence indicates that replacing conventional meat with plant-based alternatives can lower LDL cholesterol, reduce body weight, and support greater gut-microbiome diversity.

A 2024 systematic review and meta-analysis found statistically significant reductions in total and LDL cholesterol when animal meat was replaced with plant-based or fermentation-derived products. Two studies published in 2026 further reported that this substitution increased dietary fiber intake by 4–6%, reduced saturated-fat consumption by 6–7%, and lowered salt intake by 3–4%. These findings are beginning to influence professional nutrition guidance.

This shift supports the repositioning of plant-based meat from a lifestyle-oriented product to a potential preventive-health tool, expanding its target audience beyond vegans and environmentally motivated consumers. Good Food Institute research indicates that 71% of U.S. consumers aged 18–59 fall within the addressable plant-based market, with health and nutrition acting as major purchase motivations in four of six identified consumer groups.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Consciousness & Chronic Disease Burden | +3.5% | North America, EU, Urban APAC | Short term (≤ 2 years) |

| Environmental Sustainability Mandates & ESG Integration | +2.8% | EU, North America, ANZ | Medium term (2–4 years) |

| Expanding Flexitarian Consumer Base | +2.4% | North America, EU, Urban India, China | Short–Medium term (1–3 years) |

| Product Innovation & Sensory Science Advances | +2.1% | North America, EU, Singapore | Medium term (2–4 years) |

| Retail & Foodservice Channel Expansion | +1.9% | APAC corridors, Gulf, Latin America spill-over | Medium term (2–4 years) |

| Rising Protein Demand in Emerging Economies | +1.7% | India, Southeast Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

Restraints

The continuing price premium over conventional animal protein remains one of the most significant commercial barriers facing the plant-based meat industry. The Good Food Institute has reported that plant-based products can cost two to four times more than comparable conventional items. At retail, a plant-based burger may cost approximately USD 3.50–5.00 per serving, compared with USD 1.20–2.00 for a beef equivalent.

The gap reflects limited production scale, high ingredient costs, and elevated cold-chain and distribution expenses. Many manufacturing facilities are estimated to operate at only 30–50% of capacity, preventing fixed costs from being efficiently spread across production volumes. Pea protein isolate may cost around USD 2,800–3,500 per tonne, compared with USD 900–1,200 for standard-grade soy protein, further increasing formulation expenses.

Progress will depend on higher capacity utilization, lower-cost ingredient systems, improved supply-chain efficiency, and process innovations such as high-moisture extrusion. Industry development targets indicate that these improvements could reduce cost of goods sold by 15–20% by 2027. However, broad adoption is likely to remain constrained until plant-based products reach a premium of no more than approximately 25–30% over conventional meat.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Significant Price Premium vs. Conventional Meat | -3.2% | North America, EU, APAC mass-market | Short term (≤ 2 years) |

| EU/National Labeling Bans on Meat Terminology | -2.1% | EU (all 27 member states), Italy, France | Short–Medium term (1–3 years) |

| Ultra-Processed Food (UPF) Perception Backlash | -2.4% | North America, UK, Australia, Germany | Short term (≤ 2 years) |

| Taste & Texture Parity Gap with Conventional Meat | -1.9% | North America, EU core, Urban APAC | Short–Medium term (1–3 years) |

| Collapsing VC Funding & Capital Scarcity | -1.6% | North America, EU start-up ecosystem | Short term (≤ 2 years) |

| Regulatory Fragmentation & Novel Food Approval Delays | -1.3% | EU, APAC, South America | Medium term (2–4 years) |

Challenges

The alternative-protein industry is also facing a persistent shortage of specialists in food science, fermentation engineering, sensory analysis, and advanced formulation. This talent constraint is slowing research, product development, and improvements in taste and texture. India produces approximately 250,000 biotechnology and engineering graduates each year, yet many lack the application-specific skills required for smart-protein manufacturing, texturization, and precision fermentation.

In North America and Europe, where companies compete for professionals who combine expertise in food science, biotechnology, sensory development, and artificial-intelligence-assisted formulation. These interdisciplinary roles may command salaries 35–50% above conventional food-industry positions, placing plant-based meat companies in competition with pharmaceutical, biotechnology, and precision-fermentation employers.

Senior food-scientist vacancies in the sector may take 12–18 months to fill, compared with four to six months in traditional food manufacturing. These delays extend formulation and testing cycles, slow improvements in sensory quality, and postpone commercial launches. Each additional quarter of development delay may contribute to a 3–5% annual penalty in repeat-purchase performance when unresolved taste or texture issues remain.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Food Science Talent Deficit & R&D Skill Gap | -1.8% | North America, EU, India APAC | Long term (≥ 4 years) |

| Cold Chain Infrastructure Inadequacy in Emerging Markets | -1.5% | India, Southeast Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Ingredient Supply Concentration & Commodity Price Volatility | -1.4% | Global (soy/pea protein belts) | Medium term (2–4 years) |

| Consumer Trust & Health Communication Complexity | -1.2% | North America, UK, Germany, Australia | Medium term (2–4 years) |

| Manufacturing Scale & Capacity Utilization Drag | -1.1% | North America, EU production hubs | Medium term (2–4 years) |

| Allergen & Dietary Restriction Formulation Complexity | -0.9% | EU, North America, Middle East | Short–Medium term (1–3 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Battery Separator Manufacturing.

The current conflicts, along with the rise in geopolitical instabilities in the Middle East and Eastern Europe, have greatly impacted the global supply chain of the plant-based meat market in the year 2026. Security issues at sea have created great disruptions in global supply chains, with ship transits through the strategic Strait of Hormuz and the Red Sea down by more than 95%.

These disruptions have formed a connection between energy and food systems, which, in turn, increased the international shipping freight charges, marine insurance premiums, and bulk cargo rates. Since the Middle East forms the core region of fertilizer manufacturing and shipping, the conflict situation has greatly limited its outbound shipments. As a result, there is already a global shortage of fertilizers, which increases the production costs in terms of pesticides, fuel, and crop management.

The resulting pressure in warfare has led to a modification of the microeconomic fundamentals underlying the alternative protein industry. Raw materials required for the production of plant-based products require large-scale cross-border importation of specific raw materials such as soy, wheat gluten, and pea protein isolates. In view of the local warfare that escalates the prices of grain production, companies that manufacture foods face price inflation in the procurement of these bulk materials. Ingredient inflation conflicts with consumer psychology.

Regional Analysis

North America Held the Largest Share of the Plant-Based Meat Market.

North America dominated the Global Plant-Based Meat Market in 2025, accounting for 36.2% of the total and producing USD 3.9 billion in revenue. This geographic dominance is bolstered by an unusually advanced, very complex cold-chain logistics infrastructure covering the United States and Canada. This customized transportation method ensures that temperature-sensitive, high-moisture alternative proteins are transported from large-scale manufacturing facilities to thousands of retail outlets without texture deterioration, microbiological contamination, or decreased shelf life.

North America’s market supremacy is also driven by high consumer baseline spending and a rapid retail adoption rate among mainstream grocery giants and restaurant chains. Major regional supermarket chains have permanently changed their floor patterns to include specialized alternative protein cases immediately within the fresh meat aisles, increasing consumer exposure and catering to flexitarian buying preferences.

The Asia-Pacific region is experiencing the quickest growth, driven by the expanding middle class in countries like China and India. Companies such as Imagine Meats are leading the way by creating products that fit local food traditions, like plant-based mutton seekh kebabs. In Latin America, established meat companies like JBS are strengthening their position by using their factory systems to produce more affordable 50/50 mix proteins.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The worldwide plant-based beef business is undergoing major structural change, moving from a highly fragmented, startup-driven sector to a consolidated tier-one oligopoly. Previously, a significant flood of venture funding resulted in hundreds of independent firms fighting for retail shelf space, causing severe market fragmentation. However, with a tightening capital flow, rising production costs, and a clear trend toward operational efficiency, the sector is seeing a quick shakeout of undercapitalized businesses.

The market has now concentrated, with a small group of multinational consumer packaged goods (CPG) businesses, legacy meat processors, and well-funded industry pioneers controlling the vast majority of worldwide volumes. This consolidation is generally carried out through strategic mergers, acquisitions, and the closure of smaller businesses that fail to achieve manufacturing scale. Large-scale CPG firms and established animal-protein giants use their enormous, pre-existing distribution networks, extensive regulatory experience, and automated production lines to reduce unit costs.

By acquiring pioneer brands or developing proprietary, well-funded alternatives, established food companies use cross-merchandising methods to acquire permanent store placements that smaller entrepreneurs cannot afford. Furthermore, this centralized structure enables the surviving market leaders to form long-term supply agreements for raw ingredients such as soy and pea protein isolates, ensuring price stability and pricing power that effectively excludes new entrants.

This move to an oligopolistic structure is fundamentally altering how research and development is funded and scaled throughout the industry. With tier-one corporations dominating the market, individual brands no longer need to develop costly, independent manufacturing facilities from the ground up; instead, they rely on co-manufacturing agreements and shared global production centers. This enables the remaining leading businesses to pool resources for costly advances like large-scale extrusion machinery and precision fermentation facilities.

The Major Players in the Industry

- Beyond Meat, Inc.

- Impossible Foods Inc.

- Maple Leaf Foods Inc.

- Conagra Brands, Inc.

- Kellanova

- Unilever PLC

- The Kraft Heinz Company

- Nestlé S.A.

- Tofurky

- VBites Foods Ltd

- Eat Just, Inc.

- LiveKindly Collective

- Sunfed

- Moving Mountains Foods

- GoodDot

- Others

Recent Development

- In April 2026, Beyond Meat strengthened its product positioning after Beyond Burger IV and Beyond Steak became the first plant-based meat products to qualify as climate solutions.

- In January 2026, Impossible Foods entered a strategic partnership with Equii to combine plant-based meat with high-protein pasta and bread formats. This development showed the company’s push into protein-rich meal solutions as consumers looked for taste, convenience, and higher protein content.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 10.8 Billion |

| Forecast Revenue (2035) | USD 51.8 Billion |

| CAGR (2026-2035) | 17.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Burger Patties, Sausages, Strips & Nuggets, Ground Meat, Meatballs, Others), By Source (Soy, Wheat, Pea, Others), By Meat Type (Beef, Chicken, Pork, Others), By Distribution Channel (Supermarkets & Hypermarkets, Food Service, Online Retail, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Beyond Meat, Inc., Impossible Foods Inc., Maple Leaf Foods Inc., Conagra Brands, Inc., Kellanova, Unilever PLC, The Kraft Heinz Company, Nestlé S.A., Tofurky, VBites Foods Ltd, Eat Just, Inc., LiveKindly Collective, Sunfed, Moving Mountains Foods, GoodDot, Others. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, we can provide further customization to meet your requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |