Quick Navigation

Report Overview

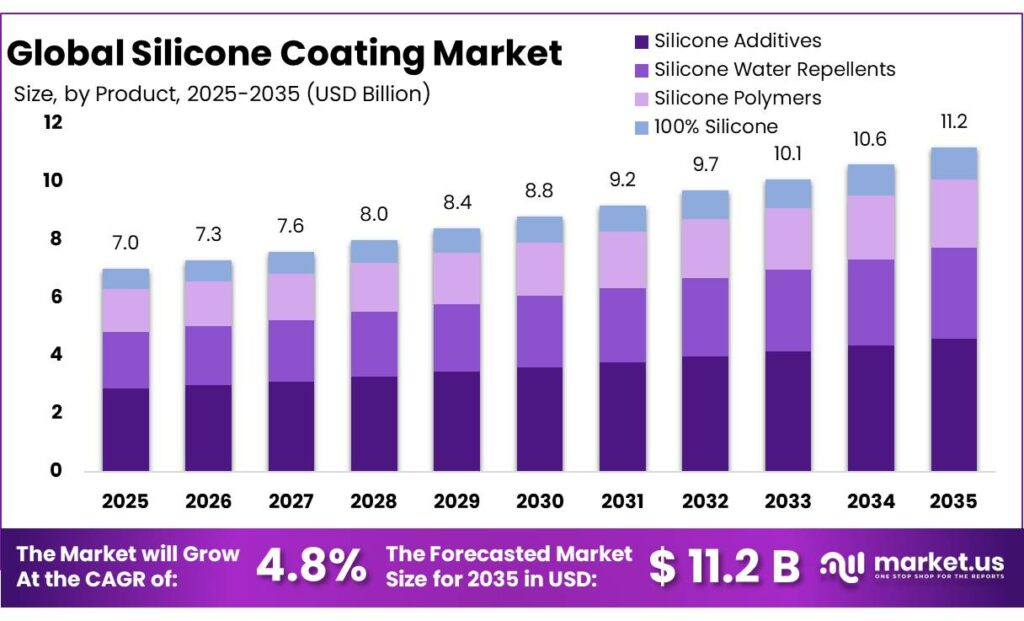

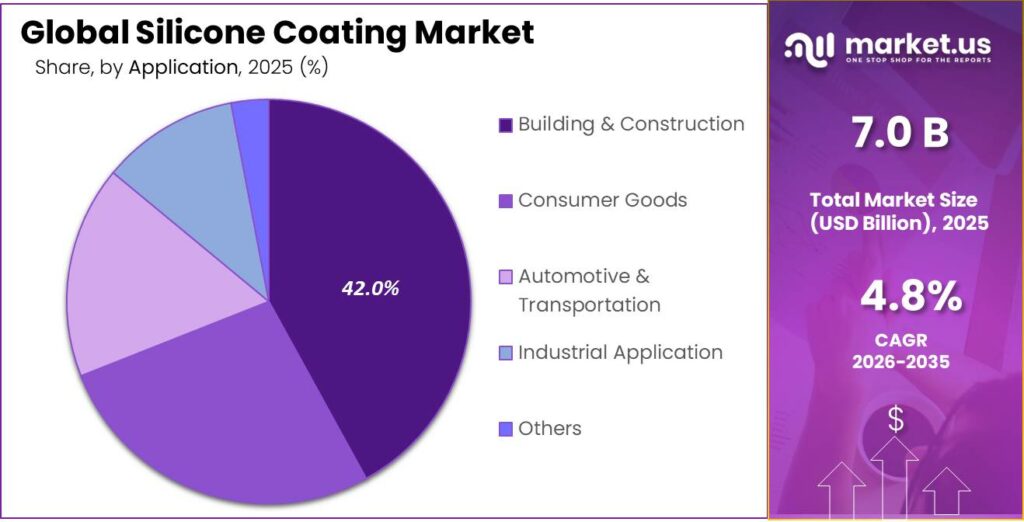

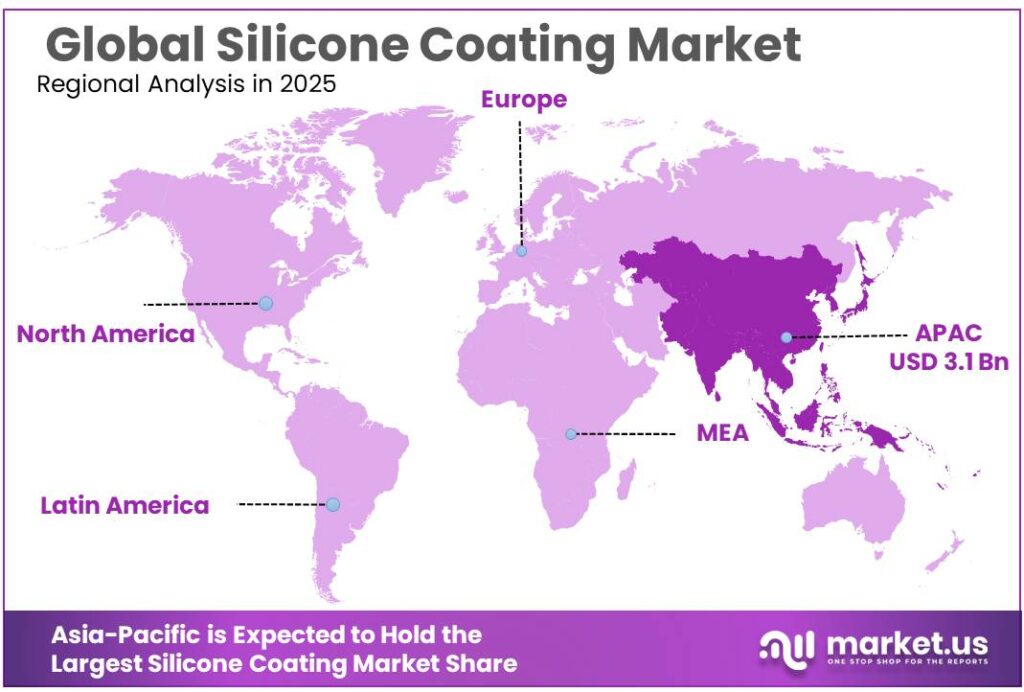

The Global Silicone Coating Market size is expected to be worth around USD 11.2 Billion by 2035, from USD 7.0 Billion in 2025, growing at a CAGR of 4.8% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 44.7% share, holding USD 3.1 Billion revenue.

Silicone coating is positioned as a high-performance protective materials segment used where durability, hydrophobicity, UV stability, temperature resistance, and release properties are critical. In industrial terms, it sits between conventional organic coatings and more specialized engineered surfaces, serving roofing, façade protection, metal protection, electronics, release liners, cookware, food-contact packaging, and processing equipment.

Its commercial relevance is reinforced by the size of the downstream base: FoodDrinkEurope reports that the EU food and drink industry employs 4.7 million people, generates €1.2 trillion in turnover, and contributes €250 billion in value added, while extra-EU food and drink exports reach €182 billion with a trade surplus of €80 billion. That scale supports stable demand for compliant, low-migration, easy-clean, and release-oriented silicone technologies in food handling and packaging applications.

The European Commission states that buildings account for 40% of EU energy consumption and 36% of greenhouse-gas emissions, which keeps reflective, weather-resistant, and long-life coating systems commercially relevant in building envelopes.

The same policy backdrop also matters because the EU Renovation Wave targets 35 million building renovations by 2030 and aims to at least double the annual renovation rate. In parallel, ACEA reported global car manufacturing of 75.5 million units in 2024, with North America producing 11.4 million units, while the EU car market still recorded 10.6 million sales in 2024.

Demand is also being lifted by electronics and advanced industrial processing. The Semiconductor Industry Association reported global semiconductor sales of $627.6 billion in 2024, up 19.1% from $526.8 billion in 2023, with fourth-quarter sales reaching $170.9 billion. For silicone coating suppliers, this matters because miniaturized and heat-sensitive electronic assemblies require dielectric protection, moisture barriers, and thermally stable surface treatments.

The policy signal is equally favorable: the EU Chips Act is expected to mobilize more than €43 billion in public investment and more than €100 billion in total policy-driven investment through 2030, while aiming for a 20% global semiconductor market share for Europe. Together, those figures point to a broader manufacturing environment that rewards specialty coating systems with reliability and regulatory performance.

The U.S. Department of Energy notes that conventional roofs can reach 150°F or more, while reflective roofs can remain more than 50°F (28°C) cooler under the same conditions. The EPA also notes that cool roofs can lower maximum indoor temperatures in non-air-conditioned residential buildings by 1.2–3.3°C (2.2–5.9°F). These operating benefits align well with silicone roof-coating chemistry.

Evonik launched Smart Effects effective 1 January 2025, combining its Silica and Silanes business lines into a business with 3,500 employees worldwide; that move is relevant because silica-silane integration can strengthen formulation know-how in high-performance surfaces, adhesion promotion, and functional coating systems.

Key Takeaways

- Silicone Coating Market size is expected to be worth around USD 11.2 Billion by 2035, from USD 7.0 Billion in 2025, growing at a CAGR of 4.8%.

- Silicone Additives held a dominant market position, capturing more than a 41.5% share.

- Building & Construction held a dominant market position, capturing more than a 42.9% share.

- Asia-Pacific stands out as the dominant region in the silicone coating market, accounting for 44.7% share with an estimated value of USD 3.1 billion.

By Product Analysis

Silicone Additives leads with 41.5% driven by performance-enhancing properties across industries

In 2025, Silicone Additives held a dominant market position, capturing more than a 41.5% share. This strong position was mainly supported by their wide usage in improving surface properties such as smoothness, water resistance, and durability across coatings, paints, and personal care products. Manufacturers continued to prefer silicone additives because they help reduce defects like craters and improve flow, which makes the final product more consistent and high quality.

By Application Analysis

Building & Construction dominates with 42.9% as demand for durable and weather-resistant coatings rises

In 2025, Building & Construction held a dominant market position, capturing more than a 42.9% share. This was largely due to the growing need for long-lasting and weather-resistant coating solutions in residential and commercial projects. Silicone coatings are widely used on roofs, walls, and exterior surfaces because they offer strong protection against moisture, UV exposure, and temperature changes. As construction activities continued to expand, especially in urban areas, the demand for reliable protective coatings increased steadily.

Key Market Segments

By Product

- Silicone Additives

- Silicone Water Repellents

- Silicone Polymers

- 100% Silicone

By Application

- Building & Construction

- Consumer Goods

- Automotive & Transportation

- Industrial Application

- Others

Emerging Trends

Heat-reflective silicone coatings are becoming the most visible trend in the market

One clear latest trend in silicone coatings is the growing demand for reflective and heat-reducing roof coatings. This shift is becoming stronger because buildings are under pressure to perform better in hotter weather while also cutting energy use. The global buildings and construction sector still accounts for 32% of global energy demand and 34% of CO₂ emissions, which is why energy-saving materials are getting more attention from builders, architects, and public agencies.

Silicone roof coatings fit this need well because they handle sunlight, rain, and temperature swings better than many traditional options. The appeal is practical, not just technical. The U.S. Department of Energy notes that a conventional roof can reach 150°F or more on a sunny day, while cool-roof systems are designed to stay far cooler by reflecting more sunlight. The EPA also reports that cool roofs can reduce maximum indoor temperatures in non-air-conditioned homes by 1.2°C to 3.3°C. That kind of improvement matters in real buildings, especially where heat stress and electricity costs are rising.

Government-backed cooling programs are pushing this trend into real projects

What makes this trend more important in 2025 and 2026 is that it is no longer limited to product innovation alone. It is now being supported by public policy, climate planning, and city-level heat action efforts. In India, the Government informed Parliament in March 2026 that Heat Action Plans have been developed for 23 states, and cool roofs are being considered by some states as part of heatwave management to reduce indoor temperatures and cooling demand.

The same reply also noted that ₹2.53 crore was provided to Tamil Nadu in 2025–2026 for environment education programs in schools, alongside support for heat-resilient design measures such as cool roofs and green buildings.

Drivers

Strong push from environmental rules and green building standards

One of the biggest drivers for silicone coatings is the growing pressure to meet environmental standards. Governments and regulatory bodies are tightening rules on emissions, especially volatile organic compounds (VOCs). For example, in Europe, strict industrial emission regulations require coatings to meet low-VOC limits, pushing industries toward cleaner alternatives like silicone-based coatings.

By 2026, around 72% of industry stakeholders were already prioritizing eco-certified materials, which shows how serious this shift has become. Silicone coatings fit well here because they can be formulated as water-based or solvent-free, making them safer for both workers and the environment. At the same time, green building programs and energy-efficiency rules are encouraging builders to use materials that reduce heat absorption and improve insulation.

Rising infrastructure and housing projects increasing real demand

Another key factor driving the silicone coating market is the continuous growth in construction and infrastructure projects backed by government funding. Many countries are investing heavily in housing and public infrastructure, which directly increases the need for durable and waterproof materials. For instance, housing programs like the Build Canada Homes initiative include funding of about $13 billion to accelerate residential construction, creating strong demand for long-life coatings.

Silicone coatings are widely used in roofs, walls, and foundations because they provide strong protection against water leakage, UV rays, and temperature changes. As modern buildings focus more on low maintenance and longer life, these coatings become a natural choice. At the same time, rapid urbanization is pushing construction activity even higher, especially in developing regions.

Restraints

Strict VOC regulations making compliance difficult for manufacturers

One major factor holding back the silicone coating market is the increasing pressure from environmental regulations, especially around volatile organic compounds (VOCs). Governments like the U.S. Environmental Protection Agency have set clear limits on VOC emissions in coatings to control air pollution and protect health. For example, industrial maintenance coatings are often limited to around 450 grams per liter of VOC content, which forces manufacturers to constantly reformulate products.

This sounds simple on paper, but in reality, it adds cost and complexity. Many silicone-based coatings need special formulations to meet these limits without losing performance. In some cases, companies must invest in new production technologies or testing systems just to stay compliant. Smaller manufacturers especially feel the pressure because compliance requires both technical expertise and financial investment.

High cost of raw materials and formulation challenges

Another key restraint comes from the cost side, especially when trying to meet both performance and regulatory standards at the same time. Silicone coatings are known for durability and resistance, but achieving these qualities often requires high-purity raw materials and advanced processing. When companies also try to reduce VOC content or meet strict emission norms, the formulation becomes even more complex and expensive.

Studies show that industries are shifting toward low-VOC or water-based coatings to meet environmental goals, but this transition is not easy. It requires redesigning formulations and sometimes sacrificing certain properties like drying speed or adhesion. At the same time, regulations may demand up to 90% VOC control efficiency in some cases, which adds further cost in terms of equipment and compliance systems.

Opportunity

Growing shift toward green buildings creating strong demand for silicone coatings

One of the biggest growth opportunities for silicone coatings is the rapid shift toward green and energy-efficient buildings. Governments across the world are pushing for sustainable construction, and this is directly increasing the demand for advanced coating solutions. For example, the global green building materials market reached about USD 532.54 billion in 2025 and is expected to grow further in 2026, showing how fast the industry is expanding.

Silicone coatings fit perfectly into this trend because they help improve energy efficiency by reflecting heat and protecting surfaces from weather damage. At the same time, governments are introducing building codes and incentives that encourage the use of eco-friendly materials. In India, policies like the Energy Conservation Building Code (ECBC) are pushing builders to adopt energy-saving materials in large projects.

Rapid urban construction and emission concerns boosting adoption

Another strong opportunity comes from the sheer scale of construction happening globally, especially in developing countries. In India alone, more than 35 billion square feet of new built space is expected by 2050, which is almost double the current stock. This massive expansion means a huge demand for materials that can handle heat, moisture, and pollution over long periods.

At the same time, buildings already contribute around 25% of total emissions in India, which is pushing both governments and builders to find better solutions. Silicone coatings are gaining attention here because they help reduce energy use by improving insulation and surface durability. They also extend the life of structures, which reduces the need for frequent repairs and material waste.

Regional Insights

Asia-Pacific dominates with 44.7% share valued at USD 3.1 Billion driven by strong construction and industrial growth

Asia-Pacific stands out as the dominant region in the silicone coating market, accounting for 44.7% share with an estimated value of USD 3.1 billion. The region’s leadership is largely supported by rapid urbanization, industrial expansion, and strong growth in end-use sectors such as construction, automotive, and electronics. In 2025, the global silicone coating market reached around USD 9.1 billion, with Asia-Pacific contributing a significant portion due to its large manufacturing base and rising consumption levels.

Countries like China, India, Japan, and South Korea continue to drive regional demand, especially with ongoing infrastructure projects and increasing investments in smart cities and industrial corridors. The construction sector remains a key contributor, as silicone coatings are widely used for waterproofing, roofing, and façade protection due to their durability and resistance to extreme weather conditions.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Evonik Industries AG is a major global player in specialty chemicals, reporting around €14.1 billion in revenue in 2025 with an adjusted EBITDA of €1.87 billion. The company operates with over 31,000 employees and focuses heavily on high-value additives and performance materials used in coatings. Its silicone-related solutions are part of its advanced materials portfolio, supporting industries like construction and automotive.

Wacker Chemie AG is a key silicone manufacturer, with expected 2025 sales between €6.1 billion and €6.4 billion and a projected ~10% growth in its silicones division. The company operates across more than 25 production sites globally and is known for its strong integration in silicone and polysilicon technologies.

Carboline Company operates as a subsidiary of RPM International, which reported over $7 billion in annual revenue across its coatings and materials businesses. The company focuses on high-performance protective coatings, including silicone-based solutions for industrial and infrastructure use. Its strong presence in corrosion protection and fireproofing coatings supports its role in demanding environments like oil & gas and power generation.

Top Key Players Outlook

- Evonik Industries AG

- Wacker Chemie AG

- Carboline Company

- OMG Borchers GmbH

- Shin-Etsu Chemical Co., Ltd.

- Momentive Performance Materials Inc.

- DOW Corning Corporation

- ACC Silicones Ltd.

- MAPEI SpA

- Sika AG

Recent Industry Developments

Evonik Industries AG continues to play a strong role in the silicone coating sector through its specialty additives business, especially under its coatings and advanced materials portfolio. In 2025, the company reported total sales of around €14.1 billion, with net income reaching €265 million and a workforce of over 31,000 employees, showing its solid global presence.

Shin-Etsu Chemical continues to hold a strong position in the silicone coating sector, mainly through its large-scale silicone production and advanced material technologies. In fiscal year 2025, the company reported consolidated net sales of around ¥2.56 trillion, with operating income reaching approximately ¥742 billion, reflecting steady growth of about 6.1% year-on-year.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 7.0 Bn |

| Forecast Revenue (2035) | USD 11.2 Bn |

| CAGR (2026-2035) | 4.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Silicone Additives, Silicone Water Repellents, Silicone Polymers, 100% Silicone), By Application (Building And Construction, Consumer Goods, Automotive And Transportation, Industrial Application, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Evonik Industries AG, Wacker Chemie AG, Carboline Company, OMG Borchers GmbH, Shin-Etsu Chemical Co., Ltd., Momentive Performance Materials Inc., DOW Corning Corporation, ACC Silicones Ltd., MAPEI SpA, Sika AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |