Quick Navigation

Report Overview

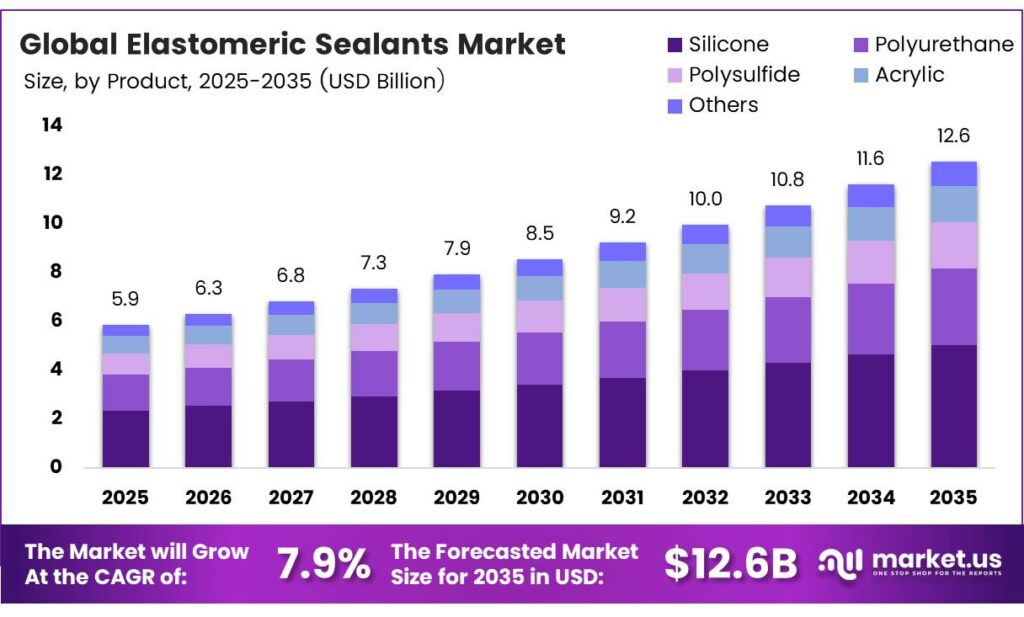

The Global Elastomeric Sealants Market size is expected to be worth around USD 12.6 billion by 2035 from USD 5.9 billion in 2025, growing at a CAGR of 7.9% during the forecast period 2026 to 2035.

Elastomeric sealants are flexible, rubber-like compounds that seal gaps and joints in construction, automotive, and industrial applications. They maintain adhesion under mechanical stress, temperature changes, and weather exposure. Consequently, manufacturers and contractors rely on these materials to ensure long-term structural integrity across diverse environments.

Building elastomeric joint sealants designed and tested per ASTM C920 handle joint movement of ±25% while maintaining adhesion and cohesive integrity under cyclic conditions. This performance capability confirms why these materials dominate high-movement facade and infrastructure sealing applications globally.

Polyurethane-based elastomeric sealants deliver movement capability of ±25% to ±50%, depending on formulation. This wider performance range enables use in more dynamic joints, positioning polyurethane variants as preferred solutions for heavy civil and industrial construction markets worldwide.

Automotive lightweighting trends also fuel adoption, as vehicle manufacturers increasingly replace metal joints with advanced polymer sealant systems. Electronics and marine sectors further diversify demand. Additionally, renewable energy installations such as solar panel mounting systems require specialized sealing solutions that withstand UV exposure and thermal cycling.

Key Takeaways

- The Global Elastomeric Sealants Market is valued at USD 5.9 billion in 2025 and is projected to reach USD 12.6 billion by 2035 at a CAGR of 7.9% during the forecast period 2026 to 2035.

- Silicone dominates the market with a 38.5% share in 2025.

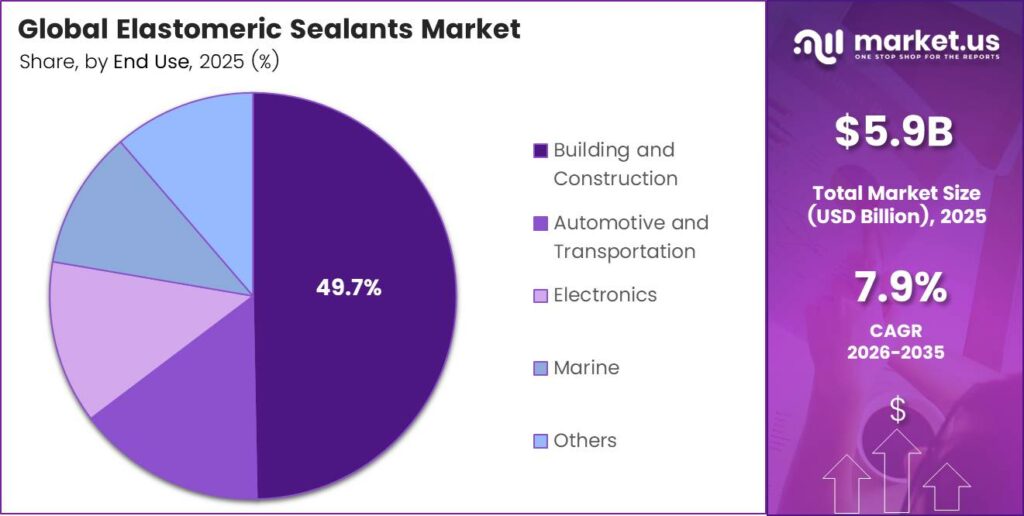

- Building and Construction holds the largest share at 49.7% in 2025.

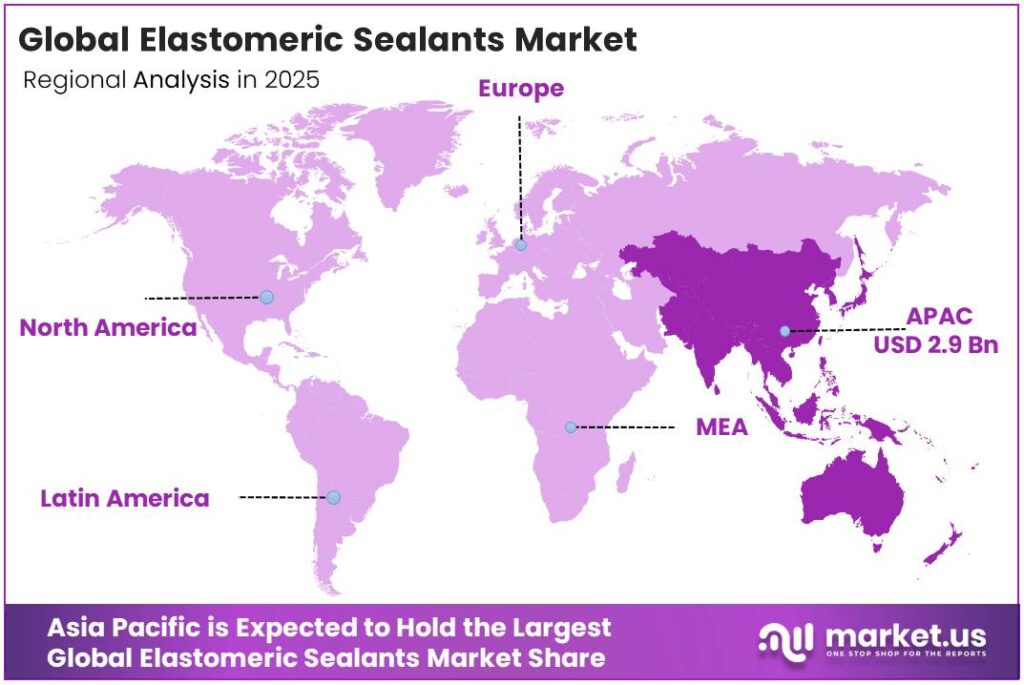

- Asia-Pacific leads the regional market with a 49.6% share, valued at USD 2.9 billion.

By Product Analysis

Silicone dominates with 38.5% due to superior weathering resistance and long-term durability.

In 2025, Silicone held a dominant market position in the by-product segment of the Elastomeric Sealants Market, with a 38.5% share. Silicone sealants offer outstanding UV resistance, thermal stability, and flexibility across extreme temperature ranges. Additionally, their compatibility with glass and metal substrates makes them the preferred choice for curtain wall glazing and facade sealing applications globally.

Polyurethane sealants rank as the second most adopted product category, valued for their high tensile strength and paintability. These materials find extensive use in flooring joints, pavement sealing, and automotive body assembly. Moreover, their adhesion performance on porous substrates such as concrete makes them highly suitable for infrastructure and civil engineering projects worldwide.

Polysulfide sealants deliver exceptional chemical resistance and are widely used in fuel tank sealing, aerospace joints, and marine applications. Their two-component formulation allows precise control over cure speed and hardness. Consequently, polysulfide remains a preferred choice where resistance to aviation fuels and harsh solvents is a critical requirement.

By End Use Analysis

Building and Construction dominates with 49.7% due to high demand for weatherproof and structural sealing solutions.

In 2025, Building and Construction held a dominant market position in the By End Use segment of the Elastomeric Sealants Market, with a 49.7% share. Rapid urbanization and green building mandates across emerging economies continue to drive sealant consumption in facades, window frames, roofing, and expansion joints. Therefore, construction remains the largest and most consistently growing end-use segment globally.

Automotive and transportation represent the second largest application area, driven by the push for vehicle lightweighting and improved noise-vibration-harshness (NVH) performance. Elastomeric sealants replace mechanical fasteners in body panels and door seams. Additionally, electric vehicle production growth creates new demand for battery pack sealing and thermal management bonding solutions in this segment.

Electronics applications require precision-grade sealants that protect components from moisture, dust, and thermal cycling. Consumer electronics, industrial controls, and LED assemblies rely on clear silicone formulations. Moreover, the miniaturization trend in semiconductor packaging demands sealant materials with high dielectric properties and dimensional stability under cyclic thermal stress.

Key Market Segments

By Product

- Silicone

- Polyurethane

- Polysulfide

- Acrylic

- Others

By End Use

- Building and Construction

- Automotive and Transportation

- Electronics

- Marine

- Others

Emerging Trends

Silicone-Modified and Hybrid Sealant Innovations Gain Market Momentum

Manufacturers increasingly invest in silicone-modified and hybrid polymer sealant formulations that combine the flexibility of silicone with the paintability of polyurethane. These advanced blends address limitations of single-chemistry products. VOC tightening is accelerating portfolio transitions toward hybrid, low-emission elastomeric sealant systems across multiple product lines.

Green Building Standards and Ready-to-Apply Systems Drive Adoption

Green building certification programs such as LEED and BREEAM increasingly specify low-VOC and UV-resistant sealants as mandatory materials. Consequently, product developers focus on pre-formulated, ready-to-apply systems that reduce on-site waste and labor time. Additionally, the growing popularity of weatherproof, high-durability sealants reflects contractor preference for longer-service-life solutions in commercial construction projects.

Drivers

Energy-Efficient Buildings and Automotive Lightweighting Accelerate Sealant Demand

Rapid expansion of energy-efficient building envelopes creates strong demand for advanced weatherproof sealant solutions in facades, curtain walls, and roofing systems. Governments worldwide enforce stricter energy codes that require high-performance sealing materials. Silicone elastomeric sealants deliver approximately 8–10 years of service life, making them a cost-effective long-term choice for building envelope applications.

Infrastructure Modernization and Renewable Energy Installations Fuel Market Growth

Surge in infrastructure modernization projects across emerging economies drives demand for durable and flexible sealing compounds in bridges, tunnels, and road joints. Simultaneously, renewable energy installations, including solar farms and wind turbine assemblies, require sealants that withstand outdoor weathering cycles. Moreover, high-performance materials in automotive lightweighting applications further expand market volumes as vehicle manufacturers shift toward polymer-based assembly systems.

Restraints

Petrochemical Price Volatility Disrupts Manufacturer Cost Structures

Volatility in petrochemical feedstock prices directly impacts the production costs of silicone, polyurethane, and acrylic elastomeric sealants. Raw material prices for siloxanes and MDI fluctuate with crude oil markets. Consequently, manufacturers face unpredictable margin pressure that limits their ability to offer stable pricing to distributors and large construction project buyers globally.

Environmental Regulations Restrict Certain Chemical Formulations

Stringent environmental regulations increasingly limit the use of specific chemical ingredients in elastomeric sealant products. Reducing VOC limits from 250 g/L to 180 g/L achieves measurable emission reductions of approximately 0.01 tons per day per district. However, reformulation investments impose significant compliance costs on smaller manufacturers with limited R&D budgets.

Growth Factors

Low-VOC Technologies and Smart City Expansion Create New Opportunities

Rising demand for eco-friendly and low-VOC elastomeric sealant technologies opens new market segments across North America and Europe. VT-200 multipurpose sealants formulated to comply with South Coast AQMD Rule 1168 demonstrate that low-emission products can meet commercial performance requirements. Furthermore, the expansion of smart cities drives the procurement of high-performance construction sealants globally.

Hybrid Polymer Innovations and Aerospace Applications Expand Market Scope

Technological advancements in hybrid polymer sealant formulations significantly expand application potential across aerospace, marine, and industrial sectors. These next-generation products combine multi-chemistry advantages into single-component systems that simplify installation. Additionally, increasing application scope in aerospace structures and offshore platforms creates premium demand segments where performance requirements justify higher price points for advanced elastomeric solutions.

Regional Analysis

Asia-Pacific Dominates the Elastomeric Sealants Market with a Market Share of 49.6%, Valued at USD 2.9 Billion

Asia-Pacific holds the largest regional share of the elastomeric sealants market at 49.6%, valued at USD 2.9 billion in 2025. China, India, Japan, and South Korea drive demand through rapid urbanization, large-scale infrastructure projects, and growing automotive manufacturing output. Moreover, government-backed smart city programs across the region continue to generate sustained consumption of high-performance sealing materials through the forecast period.

North America maintains a strong market position driven by advanced construction activity, automotive production, and robust regulatory frameworks promoting low-VOC product adoption. The United States leads demand through commercial real estate renovation, transportation infrastructure upgrades, and expanding electric vehicle manufacturing. Additionally, demand for energy code-compliant building envelope sealants continues to grow across both new construction and retrofit projects.

Europe demonstrates steady market growth supported by stringent green building regulations, REACH chemical compliance requirements, and high adoption of sustainable construction practices. Germany, France, and the UK represent the largest national markets within the region. Furthermore, the European Green Deal initiative accelerates demand for low-emission, high-durability sealant formulations across residential and commercial building renovation programs.

Latin America presents moderate but improving growth prospects supported by infrastructure investment in Brazil and Mexico. Construction activity, road maintenance programs, and expanding automotive assembly operations fuel local sealant consumption. Consequently, demand for cost-effective polyurethane and acrylic formulations remains strong, while premium silicone sealant adoption grows among larger commercial construction contractors.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Dow holds a leading position in the global elastomeric sealants market through its broad silicone and polyurethane product portfolio. The company serves construction, automotive, electronics, and industrial end-use markets with application-specific formulations. Moreover, Dow’s global manufacturing network and investment in low-VOC silicone technologies reinforce its competitive advantage among large-scale commercial construction and OEM customers worldwide.

Henkel AG operates a diversified sealant and adhesive business that addresses multiple end-use sectors, including automotive, electronics, and building construction. The company’s Loctite and Teroson branded product lines deliver performance-critical bonding and sealing solutions for industrial assembly applications. Additionally, Henkel’s focus on sustainable formulation development and digital application tools strengthens its position among automotive and electronics manufacturing customers globally.

3M brings advanced materials science capabilities to the elastomeric sealants market through its construction and industrial division. The company’s product range covers weatherproofing tapes, silicone sealants, and polyurethane adhesive systems for commercial building applications. Furthermore, 3M’s investment in low-VOC product reformulation in response to tightening regulatory requirements demonstrates proactive portfolio management aligned with environmental compliance trends.

Arkema competes in the elastomeric sealants market through its specialty adhesives and sealants business unit, which offers thiokol-based, polyurethane, and hybrid polymer formulations. The company targets aerospace, marine, and construction segments with high-performance chemical-resistant products. Consequently, Arkema’s focus on innovation in hybrid and bio-based sealant chemistries positions it well for growth in sustainable construction and advanced industrial applications.

Top Key Players in the Market

- Dow

- Henkel AG

- 3M

- Arkema

- Sika AG

- H.B. Fuller

- Wacker Chemie AG

- PPG Industries, Inc.

- RPM International

- Mapei

- Franklin International

Recent Developments

- In 2025, Dow said its Performance Materials & Coatings segment, with volume gains in downstream silicones partly offset by lower acrylic monomer and upstream siloxane volumes. Dow also said sequential demand improved in building & construction, which is relevant for sealants and glazing applications.

- In 2025, Henkel launched Loctite AA 5885, a 1K UV-curable polyacrylate gasketing sealant for automotive electronics. Henkel positioned it for ECU housings, ADAS modules, fuse boxes, actuators, and related electronic units exposed to heat and harsh environments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 5.9 Billion |

| Forecast Revenue (2035) | USD 12.6 Billion |

| CAGR (2026-2035) | 7.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Silicone, Polyurethane, Polysulfide, Acrylic, Others), By End Use (Building and Construction, Automotive and Transportation, Electronics, Marine, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Dow, Henkel AG, 3M, Arkema, Sika AG, H.B. Fuller, Wacker Chemie AG, PPG Industries, Inc., RPM International, Mapei, Franklin International |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |