Quick Navigation

Report Overview

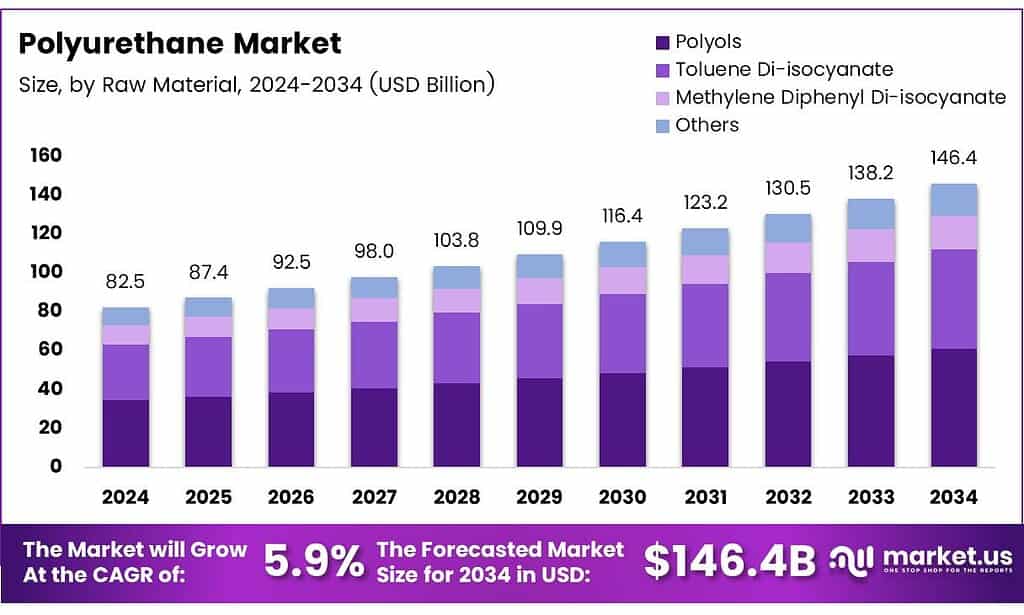

The Global Polyurethane Market size is expected to be worth around USD 146.4 billion by 2034, from USD 82.5 billion in 2024, growing at a CAGR of 5.9% during the forecast period from 2025 to 2034.

The Polyurethane Market represents a broad materials ecosystem covering foams, coatings, adhesives, sealants, and elastomers. It supports industries such as construction, automotive, furniture, insulation materials, and packaging. Polyurethane is valued for being lightweight, durable, customizable, and energy-efficient, making it suitable for modern industrial needs requiring sustainability and performance.

Polyurethane continues expanding due to rising infrastructure and industrial output. Companies and governments invest more in insulation materials and lightweight engineered polymers. The material’s adaptability and cost efficiency drive steady adoption across furniture, mobility, and electronic applications, aligning with circular economy and performance-driven manufacturing priorities.

- In terms of technical relevance, rigid polyurethane stands out for its insulation advantage. Rigid polyurethane typically has a density of 30–40 kg/m³ and thermal conductivity of 0.018–0.024 W/m-K, enabling excellent energy retention in wall and roof systems and improving building efficiency. Flexible polyurethane foam represents around 30% of regional polyurethane demand and is widely used in bedding, furniture, and automotive seating applications.

Toward the regulatory environment, sustainability policies and waste-management rules remain influential. Regions enforce policies on low-emission chemical formulations and recycling, encouraging the development of recyclable or bio-based polyurethane materials. These frameworks enhance long-term value creation while reshaping production models toward cleaner chemical manufacturing sectors.

Key Takeaways

- The Global Polyurethane Market is projected to reach USD 82.5 billion in 2024 and to hit USD 146.4 billion by 2034, expanding at a 5.9% CAGR.

- Polyols dominated the raw material category with a leading share of 43.8% in 2024.

- Rigid Foam held the largest contribution at 34.4% in 2024, driven by insulation applications.

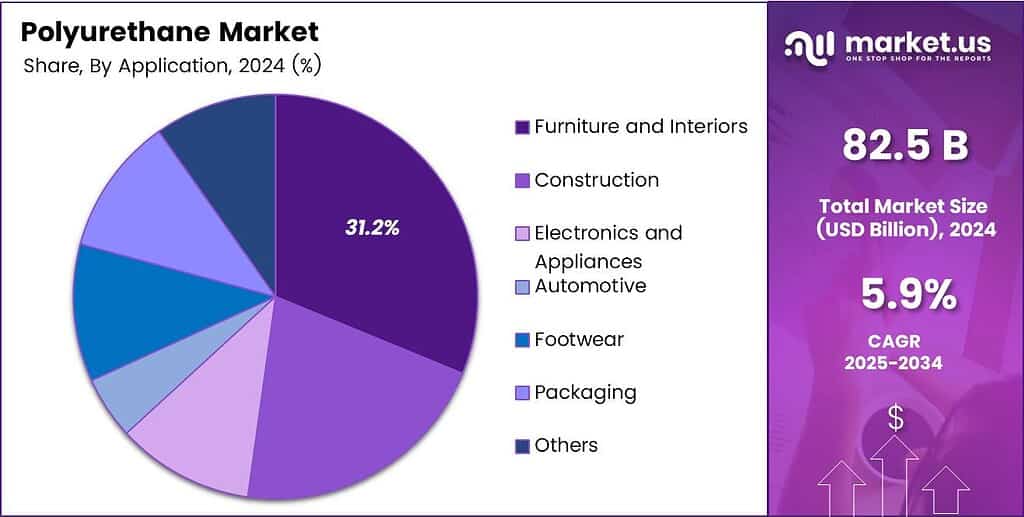

- Furniture and Interiors led the application segment with a strong share of 31.2% in 2024.

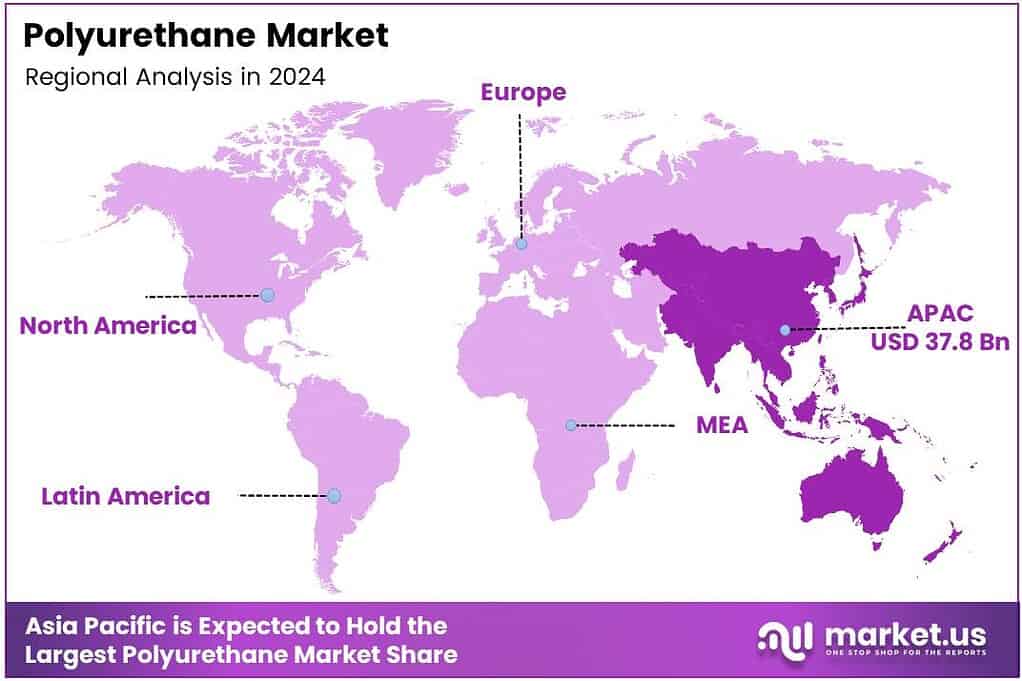

- Asia-Pacific remained the top regional market, accounting for a significant 45.9% share valued at USD 37.8 billion in 2024.

By Raw Material Analysis

Polyols dominate with a 43.8% share due to wide use in foam and coatings production.

In 2024, Polyols held a dominant market position in the By Raw Material Analysis segment of the Polyurethane Market, with a 43.8% share. Polyols are widely used to produce rigid and flexible polyurethane foams. They help enhance durability, comfort, and insulation performance across multiple industrial sectors such as furniture, bedding, and automotive.

Toluene Di-isocyanate continued to grow steadily in 2024 as a key raw material for flexible foams. It is primarily used in mattresses, furniture cushions, and automotive seats. Its strong bonding properties and compatibility with polyols keep demand stable, especially in consumer goods and transportation-related cushioning solutions.

Methylene Diphenyl Di-isocyanate gained traction as industries demand materials with better insulation and fire resistance. It is widely used in rigid foams applied in construction and cold-chain environments. Its strong mechanical properties make it suitable for applications requiring structural stability and energy efficiency improvements.

By Product Analysis

Rigid Foam dominates with a 34.4% share, driven by insulation and energy efficiency needs.

In 2024, Rigid Foam held a dominant market position in the By Product Analysis segment of the Polyurethane Market, with a 34.4% share. It is widely used in construction and refrigeration systems. Its low thermal conductivity and lightweight nature support energy efficiency measures, especially in insulation panels and building envelopes.

Flexible Foam remained widely used in furniture, mattresses, and automotive seating in 2024. It is valued for comfort, resilience, and lightweight properties. Rising consumer demand for ergonomic and soft furnishing products helped this segment maintain consistent steady growth in home interiors and mobility industries.

Coatings continued to gain demand due to their protective and aesthetic properties. Polyurethane coatings offer abrasion resistance, gloss retention, and weather tolerance. They are used across industrial machinery, flooring systems, and automotive finishes. Growing infrastructure and renovation activities supported continued uptake in this category.

By Application Analysis

Furniture and Interiors dominate with a 31.2% share, supported by cushioning and comfort demand.

In 2024, Furniture and Interiors held a dominant market position in the By Application Analysis segment of the Polyurethane Market, with a 31.2% share. Polyurethane foam is widely applied in sofas, chairs, bedding, and décor materials. Its softness, durability, and comfort performance make it suitable for lifestyle and commercial furnishings.

Construction remained a strong user of polyurethane through rigid insulation boards, sealants, and coatings. Its thermal efficiency and moisture resistance support long-term energy savings in buildings. Demand continued rising as green building certifications and energy regulations influenced material selection across infrastructure projects.

Electronics and Appliances benefited from polyurethane components offering insulation, vibration reduction, and protective encapsulation. The growth of consumer electronics and household appliances supported increased usage in modern designs requiring precise performance capabilities and improved safety characteristics in compact systems.

Automotive demand continued to expand as polyurethane is used in dashboards, seating, insulation, and coatings. Lightweight design strategies and comfort-focused interiors helped increase its adoption. Improved energy absorption and sound insulation also support modern vehicle engineering requirements.

Key Market Segments

By Raw Material

- Polyols

- Toluene Di-isocyanate

- Methylene Diphenyl Di-isocyanate

- Others

By Product

- Rigid Foam

- Flexible Foam

- Coatings

- Adhesives and Sealants

- Elastomers

- Others

By Application

- Furniture and Interiors

- Construction

- Electronics and Appliances

- Automotive

- Footwear

- Packaging

- Others

Emerging Trends

Growing Use of Energy-Efficient Materials Drives Market Trend

One major trend shaping the polyurethane market today is the increasing use of energy-efficient materials. Many construction companies prefer polyurethane foam because it provides strong insulation and helps reduce heating and cooling costs. As buildings move toward greener standards, polyurethane becomes more useful due to its thermal efficiency and durability.

- Automakers and aircraft manufacturers now use polyurethane foams, coatings, and adhesives to make vehicles lighter and more fuel-efficient. This shift supports emission reduction goals and improves overall performance. The Waste Framework Directive stipulates that member States must prepare at least 65% of municipal waste for reuse or recycling, creating a downstream incentive for more sustainable polyurethane products and recycling systems.

Sustainability is also becoming a key focus in the polyurethane market. Companies are exploring bio-based and recyclable polyurethane to reduce environmental impact. This trend is driven by customer awareness, stricter rules, and a push for eco-friendly materials across industries. Polyurethane demand is growing in furniture and bedding because it offers comfort, flexibility, and long-lasting performance.

Drivers

Growing Use of Polyurethane in Construction Boosts Market Growth

Polyurethane is widely used in insulation panels, roofing, flooring, and sealants due to its strong durability and energy-saving ability. As cities expand and governments focus on energy-efficient buildings, the demand for polyurethane continues to increase. Developers prefer polyurethane materials because they have good thermal performance and help reduce heating and cooling costs in buildings.

- The shift toward green and sustainable building regulations supports market growth. Many regions are encouraging the use of insulation materials that improve efficiency and reduce carbon emissions. The production of rigid polyurethane foam reached about 2.6 million tonnes. Polyurethane fits well in this trend because it offers high insulation capability in a lightweight form.

Polyurethane can be produced in many forms, such as flexible foam, rigid foam, coatings, adhesives, and elastomers. This makes it valuable across several end-use industries like automotive, electronics, and furniture. As technology evolves, manufacturers are developing new polyurethane grades with improved performance, longer durability, and lower environmental impact.

Restraints

Strict Environmental Rules Limit Market Expansion

Environmental regulations are becoming stricter worldwide, and this is creating challenges for the polyurethane market. Governments are pushing manufacturers to reduce emissions from chemicals such as isocyanates and blowing agents. These materials are essential for making polyurethane, but they contribute to air pollution and the carbon footprint. As a result, producers must invest more in compliance and cleaner technology, which increases production costs and slows down supply.

- Polyurethane products are long-lasting but difficult to recycle because they do not melt easily and require special treatment. Many countries are now imposing landfill restrictions, especially on foams used in furniture, insulation, and packaging. Rigid foam growth is modest, 2-3% in parts of East Asia like China and South Korea, reflecting saturation and competitive substitutes.

Fluctuating raw material prices also impact the market. Polyols and isocyanates are derived from petroleum, so their cost changes with oil market volatility. When oil prices rise, polyurethane becomes more expensive compared to alternative materials such as rubber, polystyrene, or wood-based insulation. This sometimes leads industries like automotive and construction to reconsider their material choices.

Growth Factors

Rising Focus on Sustainable and High-Performance Materials Creates Market Opportunity

The polyurethane market is experiencing strong growth opportunities as industries look for lightweight and durable materials. Many automotive and construction companies are now choosing polyurethane because it reduces weight while maintaining strength. This shift supports better fuel efficiency in vehicles and improves building insulation performance.

- Polyurethane foam and elastomers are being used for thermal management, cushioning, and vibration control in EV batteries and electronic devices. The flexible PU-foam industry in Europe estimates that each year about 40 million mattresses reach end-of-life in the EU, up from 30 million, and of those discarded mattresses, only 17% were recycled, 33% energy-recovered, and 49% landfilled.

Infrastructure growth in developing markets creates significant long-term potential. Polyurethane insulation systems, sealants, and coatings support energy-efficient buildings and modern construction methods. Governments across regions are promoting energy-saving construction, which could further drive adoption.

Regional Analysis

Asia-Pacific Leads the Polyurethane Market with a 45.9% Share, Valued at USD 37.8 Billion

Asia-Pacific remained the largest regional market due to rapid industrialization, growing automotive production, and strong infrastructure spending. In 2024, the region accounted for a dominant 45.9% market share, valued at approximately USD 37.8 billion. Demand was supported by large-scale construction projects in China, India, and Southeast Asia, including smart city infrastructure and industrial insulation upgrades.

North America showed stable demand, driven by energy-efficient building materials, automotive lightweighting strategies, and increasing adoption of polyurethane insulation. The U.S. construction sector, especially in residential roofing, spray foam, and insulation materials, continued to support market expansion. Sustainability initiatives, including bio-based polyurethane development and regulatory pressure on VOC emissions, also shaped product innovation in the region.

Europe’s market growth was supported by stringent environmental regulations, advanced manufacturing technologies, and increasing use of polyurethane in automotive and packaging applications. Insulation demand increased due to stricter building efficiency directives under EU climate targets. The region also saw growing momentum toward circular polyurethane technologies, including mechanical recycling and renewable feedstock-based production.

The United States represented a major market within North America, driven by strong innovation, construction spending, and energy-efficient renovation programs. Growing adoption of polyurethane-based spray foam insulation, flexible foams in furniture and bedding, and lightweight automotive polymers continued to boost demand. Federal initiatives supporting sustainable infrastructure and industrial energy efficiency further strengthened market momentum.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Dow Inc. continues to strengthen its position in the polyurethane market with a broad materials portfolio serving construction, furniture, automotive, and insulation industries. The company is focusing on improving material efficiency and advancing circular polymer strategies, which makes its polyurethane systems more aligned with long-term sustainability and regulatory direction.

BASF SE remains a highly integrated polyurethane producer with capabilities spanning isocyanates, polyols, and specialty formulation systems. The company is strategically investing in low-carbon and bio-balanced polyurethane offerings, reflecting shifting customer expectations and regulatory pressure. Its strong technology ecosystem and global supply capabilities allow BASF to maintain a competitive edge as demand accelerates in construction, mobility, and durable goods.

Covestro AG continues to play a major role in polyurethane materials used across insulation, consumer goods, and automotive lightweighting. The company’s expertise in both rigid and flexible foams helps it respond to diverse market needs, especially in energy-efficient buildings and modern mobility platforms. Covestro’s focus on material innovation and long-term sustainability keeps it well-positioned in a changing regulatory and commercial environment.

Huntsman International LLC remains a notable supplier of polyurethane solutions driven by its strong presence in MDI systems and downstream formulation capabilities. The company continues to support demand from flexible foams, appliances, adhesives, and engineered insulation applications. Huntsman’s focus on high-performance and application-specific polyurethane solutions helps it maintain a resilient market position as industrial and consumer sectors expand.

Top Key Players in the Market

- Dow, Inc.

- BASF SE

- Covestro AG

- Huntsman International LLC

- Eastman Chemical Company

- Mitsui and Co. Plastics Ltd.

- Mitsubishi Chemical Corporation

- Recitel NV/SA

- Woodbridge

- DIC Corporation

Recent Developments

- In May 2025, the EPA finalized NESHAP amendments prohibiting methylene chloride in flexible PU foam fabrication, reducing HAP emissions by over 14,000 tpy (70% from baseline) to protect public health in upholstery and automotive applications.

- In May 2025, Labelling and Packaging (CLP) Regulation continues to evolve, with daily updates to the C&L Inventory, ensuring hazard communication for PU precursors like isocyanates. Alignment with the EU Green Deal emphasizes bio-based alternatives.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 82.5 billion |

| Forecast Revenue (2034) | USD 146.4 billion |

| CAGR (2025-2034) | 5.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Polyols, Toluene Di-isocyanate, Methylene Diphenyl Di-isocyanate, Others), By Product (Rigid Foam, Flexible Foam, Coatings, Adhesives and Sealants, Elastomers, Others), By Application (Furniture and Interiors, Construction, Electronics and Appliances, Automotive, Footwear, Packaging, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Dow, Inc., BASF SE, Covestro AG, Huntsman International LLC, Eastman Chemical Company, Mitsui and Co. Plastics Ltd., Mitsubishi Chemical Corporation, Recitel NV/SA, Woodbridge, DIC Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |