Quick Navigation

Report Overview

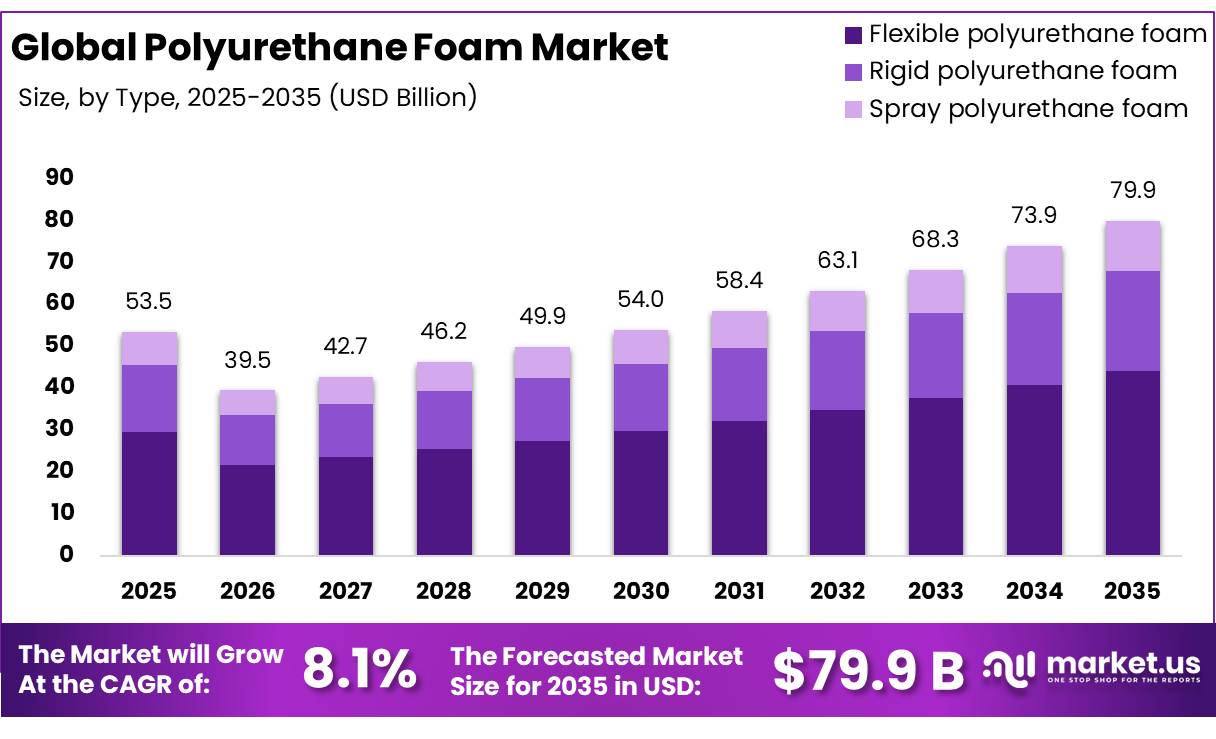

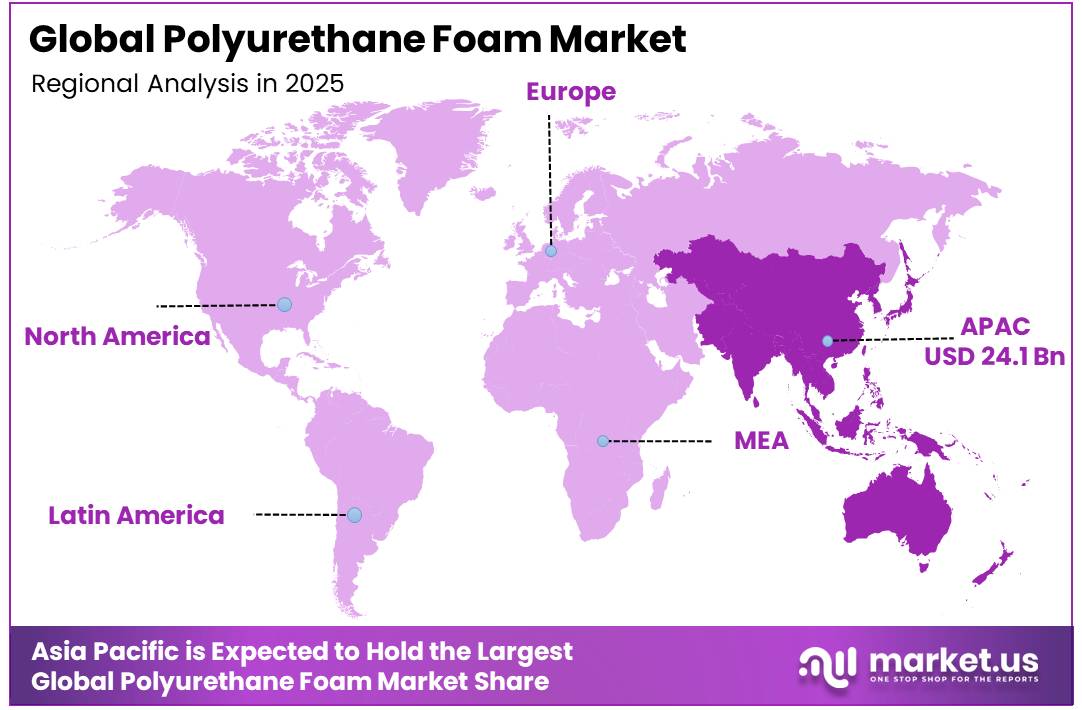

In 2025, the Polyurethane Foam Market was valued at US$53.5 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 8.1%, reaching about US$79.9 billion by 2035. In 2025, Asia Pacific led the market, achieving over 45.1% share with a revenue of US $24.1 billion.

The polyurethane foam market is a versatile global system that produces rigid and flexible materials for insulation, furniture, automobile cushioning, and construction sealing. Demand is growing as major economies’ regulatory frameworks increasingly require thermal performance standards that polyurethane foam is technically and commercially positioned to satisfy. Residential and commercial retrofits are among the most direct demand channels, with building owners upgrading envelope insulation to fulfill code requirements and cut energy costs.

- According to the U.S. Department of Energy’s Buildings Energy Data (2024 update), buildings account for approximately 40% of total U.S. energy consumption, reinforcing insulation mandates and expanding the addressable market for polyurethane foam in retrofit applications.

Key Takeaways

- The global polyurethane foam market was valued at USD 53.5 billion in 2025.

- The market is projected to grow at a CAGR of 8.1% and is estimated to reach USD 79.9 billion by 2035.

- Flexible Polyurethane Foam accounted for a leading 55.1% share of the market in 2025, supported by widespread volumetric consumption across consumer bedding, furniture, and automotive seating applications.

- Medium-Density accounted for a leading 45.1% share of the market in 2025, driven by engineering requirements for structural air barriers and premium thermal insulation boards across commercial and residential construction.

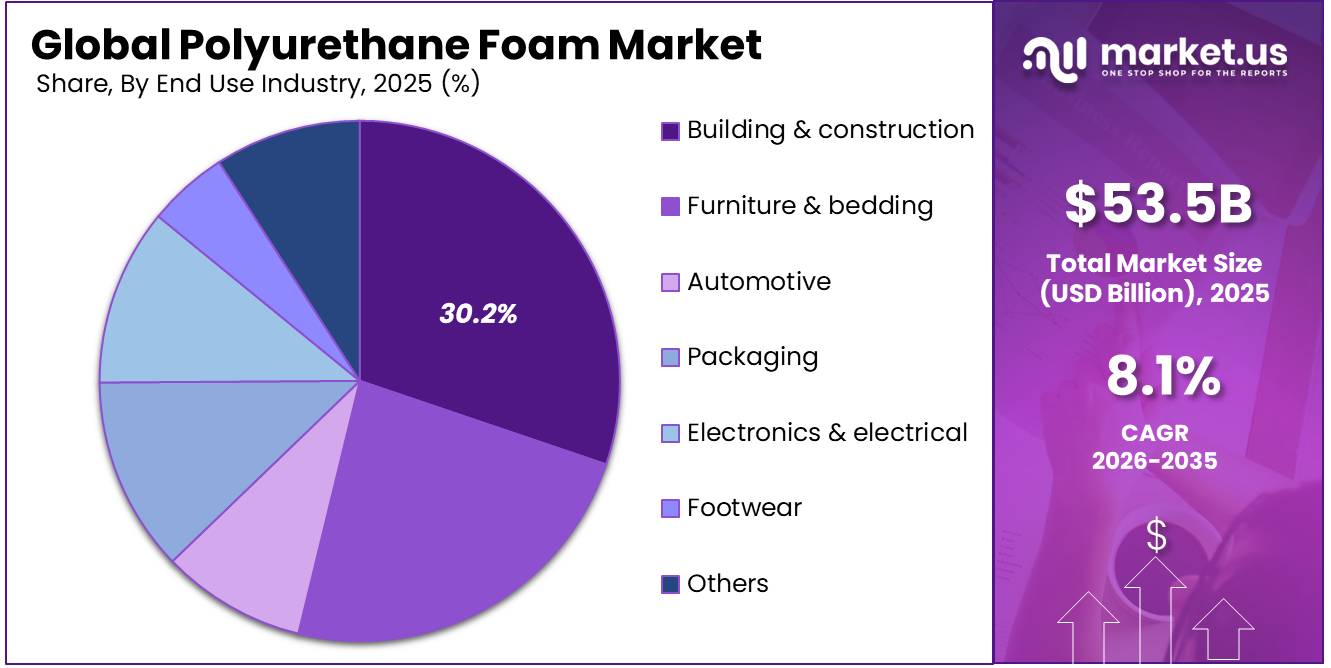

- Building & Construction accounted for a leading 30.2% share of the market in 2025, sustained by legally enforced net-zero building codes and large-scale insulation retrofit programs across developed and emerging economies.

- Asia-Pacific accounted for a leading 45.1% share of the market in 2025, supported by high-density manufacturing activity, rapid urbanization, and the scale of industrial production in China and India.

Manufacturing is carried out using three main process technologies: reactive injection molding, continuous slabstock extrusion, and high-pressure on-site spray dispensing, the latter of which is rapidly gaining popularity in commercial construction and building retrofit projects. Automated AI algorithms are utilized to improve chemical dosing ratios, predict precise exothermic reactions during continuous slabstock processing, and eliminate material waste throughout the manufacturing process.

Polyurethane Foam Market Segmentation

Type Analysis

Flexible polyurethane foam represents dominant segment in the market.

Flexible polyurethane foam represents the dominant segment in the market, accounting for 55.1% share due to the large consumption quantities throughout the household bedding, commercial upholstered furniture, and transportation seating segments, where the material delivers crucial viscoelastic cushioning, open-cell breathability, and structural durability. The material’s structural versatility, remarkable energy absorption qualities, and highly cost-optimized macro-scale continuous manufacturing methods all contribute to its dominant market position.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached approximately 4 million units in 2025. Flexible polyurethane foam is extensively used in seats, headrests, armrests, and interior components.

Rigid Polyurethane Foam is the fastest growing segment in the Polyurethane Foam Market, driven by its excellent thermal insulation properties, lightweight structure, and increasing use in energy-efficient construction and refrigeration applications. In 2025, demand for rigid polyurethane foam remained strong across residential, commercial, and industrial buildings as governments and developers focused on reducing energy consumption and improving insulation performance.

Density Analysis

Medium-Density PU Foam dominates the rigid polyurethane foam market with a 45.1% share due to its balanced strength, insulation performance, and broad industrial use

In 2025, Medium-density PU foam held a dominant market position, capturing more than a 45.1% share of the rigid polyurethane foam market. The segment maintained its leadership because it offers an effective balance between thermal insulation, mechanical strength, and material efficiency, making it suitable for building insulation panels, cold storage facilities, refrigerated transport systems, and industrial equipment. Medium-density rigid polyurethane foam continued to gain preference across the construction sector as demand for energy-efficient buildings increased. In 2026, the segment benefited further from growing investments in cold-chain infrastructure and commercial buildings requiring high-performance thermal insulation.

- The International Energy Agency (IEA) reported that buildings account for nearly 30% of global final energy consumption, encouraging the adoption of advanced insulation materials such as medium-density rigid polyurethane foam to improve energy efficiency and reduce operating costs. Its ability to provide structural stability while maintaining strong insulation performance continues to support its dominant position across multiple end-use industries.

Low-density PU foam systems are a highly technological upcoming growth path, with important milestone modifications scheduled for 2030 and 2035. To improve breathability and temperature dissipation, mattress and upholstery makers are incorporating ultra-soft, low-density open-cell memory foams created with infused gel polymers. Shifting consumer demands for premium ergonomic bedding, as well as strong corporate mandates to reduce total chemical material weight per unit, are influencing this trending category.

End Use Analysis

Polyurethane Foam Are Mostly Utilized in the Building & Construction Sector.

The Building & Construction segment, accounting for 30.2% of the Polyurethane Foam market, remains the dominant end-use category due to the widespread implementation of statutory building energy regulations worldwide, which legally compel architectural frames to incorporate high-performance thermal insulation layers. The construction industry increasingly adopted advanced insulation materials to comply with stricter energy-efficiency standards and reduce building operating costs.

- In 2026, the U.S. Census Bureau reported that private residential construction spending reaching approximately US$909.9 billion, reflecting continued investment in housing and infrastructure projects that require effective insulation materials.

Furniture and Bedding is a rapidly increasing consumption segment that is poised to reach significant worldwide operating milestones between 2026 and 2035. A growing worldwide middle-class demographic, increased disposable consumer income, and expanding public desire for sophisticated ergonomic mattress designs are all contributing factors to this rapid acceleration. To capitalize on this momentum, manufacturers are building automated continuous slabstock extrusion lines to increase production of high-resilience, viscoelastic memory foams that meet changing consumer comfort and structural durability standards.

Key Market Segments

By Type

- Flexible polyurethane foam

- Rigid polyurethane foam

- Spray polyurethane foam

By Density

- Medium‑density PU foam

- High‑density PU foam

- Low‑density PU foam

By End-use Industry

- Building & construction

- Furniture & bedding

- Automotive

- Packaging

- Electronics & electrical

- Footwear

- Others

Driver Analysis

Building envelope retrofits and insulation code tightening

The strongest structural demand driver remains tighter building-efficiency policy, because polyurethane foam retains one of the highest insulation values per unit thickness and therefore captures projects where wall depth, roof loading, or retrofit geometry constrain mineral wool or lower-performance plastics. The European Commission’s Renovation Wave still targets 35 million buildings renovated by 2030 and at least a doubling of the annual renovation rate, which directly enlarges the addressable market for rigid polyurethane boards, spray foam, and insulated panels in roofs, walls, and HVAC envelopes.

On the activity side, official Eurostat releases showed EU construction output still growing year on year in mid-2025, with June 2025 construction production up 1.9% in the EU and 1.7% in the euro area versus June 2024, even though monthly volatility remained high; that pattern supports a demand base where retrofit-linked insulation outperforms weaker new-build segments.

In the United States, total construction spending reached $2.172 trillion annualized in April 2026, with private residential at $909.9 billion and private nonresidential at $729.8 billion, preserving a large installed base for insulation upgrades even in a mixed housing cycle. Strategically, this driver shifts polyurethane suppliers toward specification-led selling, certified thermal-system packages, and contractor distribution partnerships rather than commodity resin sales, because value capture increasingly depends on compliance performance, installed R-value density, and labor-time reduction per square foot.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Building envelope retrofits and insulation code tightening | +1.9% | EU core, North America core, Northeast Asia advanced markets | Medium term (2-4 years) |

| Data center, cold-chain, and industrial build-out lifting rigid foam demand | +1.5% | North America core, EU industrial clusters, APAC corridors | Short term (≤ 2 years) |

| HFC phase-down and low-GWP blowing-agent conversion accelerating replacement cycles | +1.2% | North America core, EU core, Japan/Korea compliance markets | Short term (≤ 2 years) |

| Affordable housing and modular/manufactured construction supporting spray and panel foam use | +1.0% | North America core, India and Southeast Asia urban corridors, Latin America spill-over | Medium term (2-4 years) |

| Automotive lightweighting and EV thermal management expanding flexible and specialty foam content | +0.9% | China core, EU core, North America core | Medium term (2-4 years) |

| Public-energy efficiency funding and renovation programs de-risking insulation purchases | +0.8% | EU core, U.S. federal-state programs, selected APAC policy markets | Long term (≥ 4 years) |

Restraint Analysis

Weak housing starts and patchy construction demand

Demand-side softness in residential construction is capping near-term foam volume expansion because housing is still one of the largest end-use channels for insulation boards, spray foam, underlayments, sealants, and furniture-related foam consumption. Official Census-based housing data for the United States showed 2025 housing starts at roughly 1.3587 million units, down 0.6% from 2024, indicating that the market did not enter a strong cyclical rebound despite lower expectations for an easing rate environment.

Europe has shown similar inconsistency: Eurostat reported that in January 2026, production in construction fell 1.3% in the euro area and 2.1% in the EU month on month, while February 2026 output was still down 1.9% year on year in the euro area and 2.0% in the EU, underscoring that the demand recovery across residential and building envelope segments remained fragile.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Isocyanate trade friction | -1.7% | North America core, China-linked APAC corridors | Short term (≤ 2 years) |

| Feedstock and energy cost volatility | -1.4% | EU core, North America core, Northeast Asia | Short term (≤ 2 years) |

| Weak housing starts and patchy construction demand | -1.3% | North America core, EU core | Medium term (2-4 years) |

| Solvent and workplace chemical restrictions | -0.9% | North America core, EU compliance markets | Short term (≤ 2 years) |

| Compliance-led reformulation burden | -0.8% | EU core, North America core, Japan/Korea | Medium term (2-4 years) |

| Margin squeeze from mixed-volume recovery | -0.7% | Global, strongest in EU and North America | Medium term (2-4 years) |

Opportunity Analysis

Deep-retrofit premium systems

This is an opportunity rather than a current driver because the baseline already reflects ordinary insulation demand, whereas the incremental upside lies in monetizing deep-retrofit projects with bundled high-performance polyurethane systems, certified installation, energy-audit linkage, and financing-compatible product design. The European Commission’s Renovation Wave still targets 35 million buildings by 2030 and aims to at least double the annual renovation rate, while parallel policy discussion around building performance standards is pushing owners toward deeper interventions rather than light repairs.

That creates a white space for polyurethane suppliers to move from selling boards or spray foam by volume to selling system-value packages roof, wall, air-sealing, vapor management, and compliance documentation where gross margins can expand by an estimated 300 to 600 basis points versus commodity insulation sales because the value proposition is measured against whole-building energy savings and space efficiency. In the U.S., DOE guidance continues to highlight spray foam, rigid sheathing, rim-joist sealing, and attic envelope improvements in retrofit pathways, which means suppliers that build contractor networks and digital specification tools can lower customer acquisition costs by roughly 10% to 15% while increasing revenue per project by 1.4x to 2.0x compared with stand-alone material sales.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Deep-retrofit premium systems | +1.8% | EU core, North America core | Medium term (2-4 years) |

| Low-GWP conversion share capture | +1.5% | North America core, EU core, Japan/Korea | Short term (≤ 2 years) |

| Data-center thermal envelope solutions | +1.3% | North America core, EU digital hubs, Gulf/APAC corridors | Short term (≤ 2 years) |

| Weatherization and low-income housing channels | +1.0% | U.S. core, Canada spill-over | Medium term (2-4 years) |

| Modular and factory-built system kits | +0.9% | North America core, India, Southeast Asia | Medium term (2-4 years) |

| Circular foam recovery and M&A roll-up | +0.8% | EU core, North America core | Long term (≥ 4 years) |

Challenges Analysis

Regulatory complexity and compliance overhead

Regulatory complexity is a long-horizon challenge rather than a discrete restraint because it introduces recurring compliance overhead, technical uncertainty, and product-development drag even when products remain legal to sell; this is evident in the evolving patchwork of chemical, climate, and workplace rules affecting polyurethane value chains.

In parallel, the EU’s F-gas regulation commits to deep reductions in fluorinated greenhouse gas supply, with official communications noting that EU F-gas supply in 2023 was about 45% lower than in 2015, driving a multiyear cascade of restrictions and reporting obligations that foam producers must interpret and integrate into product roadmaps. The challenge lies in the ongoing nature of these regimes: compliance teams must track multiple timelines, coordinate plant investments across regions, and run repeated reformulation and re-certification projects that can each consume 6–18 months and millions of dollars in lab, tooling, and customer-qualification costs, which slows innovation cycles and absorbs management bandwidth.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile petro-chemical feedstock costs | -1.4% | North America core, EU industrial hubs, Northeast Asia | Medium term (2-4 years) |

| Construction-cycle volatility and demand signaling | -1.2% | EU core, North America core | Medium term (2-4 years) |

| Regulatory complexity and compliance overhead | -1.0% | EU regulatory hubs, North America core, Japan/Korea | Long term (≥ 4 years) |

| Skilled operations and formulation talent gaps | -0.9% | EU industrial clusters, North America core, APAC emerging | Long term (≥ 4 years) |

| Process variability and quality-yield dispersion | -0.8% | Global manufacturing corridors | Medium term (2-4 years) |

| Circularity and end-of-life systems immaturity | -0.7% | EU core, North America core | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Polyurethane Foam Market.

The continuation of unstable geopolitical conflicts until 2026 has created severe structural friction in the global polyurethane foam industry, affecting raw material security and increasing production costs. Because polyurethane manufacture is primarily based on energy-intensive chemical processing, continuous war-related disruptions to regional natural gas pipelines and marine shipping lanes have resulted in severe cost inflation for critical upstream feedstocks.

Production facilities for methylene diphenyl diisocyanate (MDI) and toluene diisocyanate (TDI), particularly in Western and Central Europe, are running on tight margins due to highly fluctuating industrial energy prices. For example, the implementation of tight trade embargoes and localized infrastructure damage in Eastern European energy corridors has necessitated a permanent reconfiguration of chemical supply chains.

Furthermore, shipping disruptions at crucial maritime chokepoints, combined with war-related risk premiums on international freight, have extended lead times for essential specialized additives and environmentally friendly blowing agents. To cope with these geopolitical headwinds, major chemical conglomerates are rapidly decentralizing their synthesis plants and investing substantially in localized bio-based polyol production to decouple their supply chains from politically insecure fossil fuel regions.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Polyurethane Foam Market.

In 2025, the Asia Pacific dominated the global polyurethane foam market, holding about 45.1% of the total global consumption, due to The region’s leadership is principally backed by its big population, rising urbanization, expanding construction sector, and increasing manufacturing activities. World Population Review 2025 Asia Pacific has over 4.8 billion people, accounting for approximately 60% of the global population, resulting in high demand for residential housing, commercial infrastructure, furnishings, appliances, and automobiles. China is still the largest consumer and producer of polyurethane foam due to its enormous construction industry and robust industrial environment, while India is seeing increased demand from building insulation, furniture production, and cold-chain infrastructure expansion.

North America benefits from strong building energy-efficiency laws, increased retrofit efforts, and the growing use of spray polyurethane foam for residential and commercial insulation applications. Sustainability programs, green building standards, and legislative frameworks that promote low-carbon construction materials continue to drive high demand in Europe. The region is also leading the way in the development of bio-based polyurethane formulations and low-GWP blowing agents.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global polyurethane foam market is fairly consolidated to oligopolistic in structure, with a small number of multinational chemical manufacturers owning a large percentage of global production capacity, raw material supply, and technological innovation. The market has high entry hurdles due to large capital needs, proprietary polyurethane formulas, integrated isocyanate and polyol production capabilities, stringent environmental restrictions, and vast distribution networks.

Leading companies in the polyurethane foam market include BASF SE, Covestro AG, Dow Inc., Huntsman Corporation, Wanhua Chemical Group Co., Ltd., Recticel NV, Saint-Gobain, Woodbridge Group, and Carpenter Co. Competition is centered on product innovation, sustainability, manufacturing capacity, and application-specific solutions across flexible, rigid, and spray polyurethane foam segments.

The Major Players In The Industry

- Covestro AG

- BASF SE

- Dow Inc.

- Huntsman Corporation

- Wanhua Chemical Group Co., Ltd.

- Sekisui Chemical Co., Ltd.

- Recticel NV/SA

- Rogers Corporation

- Saint‑Gobain S.A.

- DuPont

- INOAC Corporation

- Armacell International S.A.

- Sheela Foam Ltd.

- Carpenter Co.

- Trelleborg AB

- Others

Key Development

- In April 2026, BASF SE introduced ELASTOSPRAY BMB isocyanate for the North American spray polyurethane foam market, expanding its low-carbon insulation range. When compared to standard spray polyurethane foam systems, the biomass-balanced approach can reduce the product’s carbon footprint by 21-29% while retaining current processing needs.

- In January 2026, Covestro AG launched the CQ-Configurator, a digital sustainability platform that allows polyurethane value-chain participants to develop and evaluate flexible and rigid foam solutions based on real-time environmental performance data. The tool facilitates sustainability reporting and product development for foam applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$53.5 Bn |

| Forecast Revenue (2035) | US$79.9 Bn |

| CAGR (2026-2035) | 8.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Flexible polyurethane foam, Rigid polyurethane foam, Spray polyurethane foam), By Density (Medium‑density PU foam, High‑density PU foam, Low‑density PU foam), By End-use (Industry, Building & construction, Furniture & bedding, Automotive, Packaging, Electronics & electrical, Footwear, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Covestro AG, BASF SE, Dow Inc., Huntsman Corporation, Wanhua Chemical Group Co. Ltd., Sekisui Chemical Co. Ltd., Recticel NV/SA, Rogers Corporation, Saint‑Gobain S.A., DuPont, INOAC Corporation, Armacell International S.A., Sheela Foam Ltd., Carpenter Co., Trelleborg AB, Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |