Quick Navigation

Report Overview

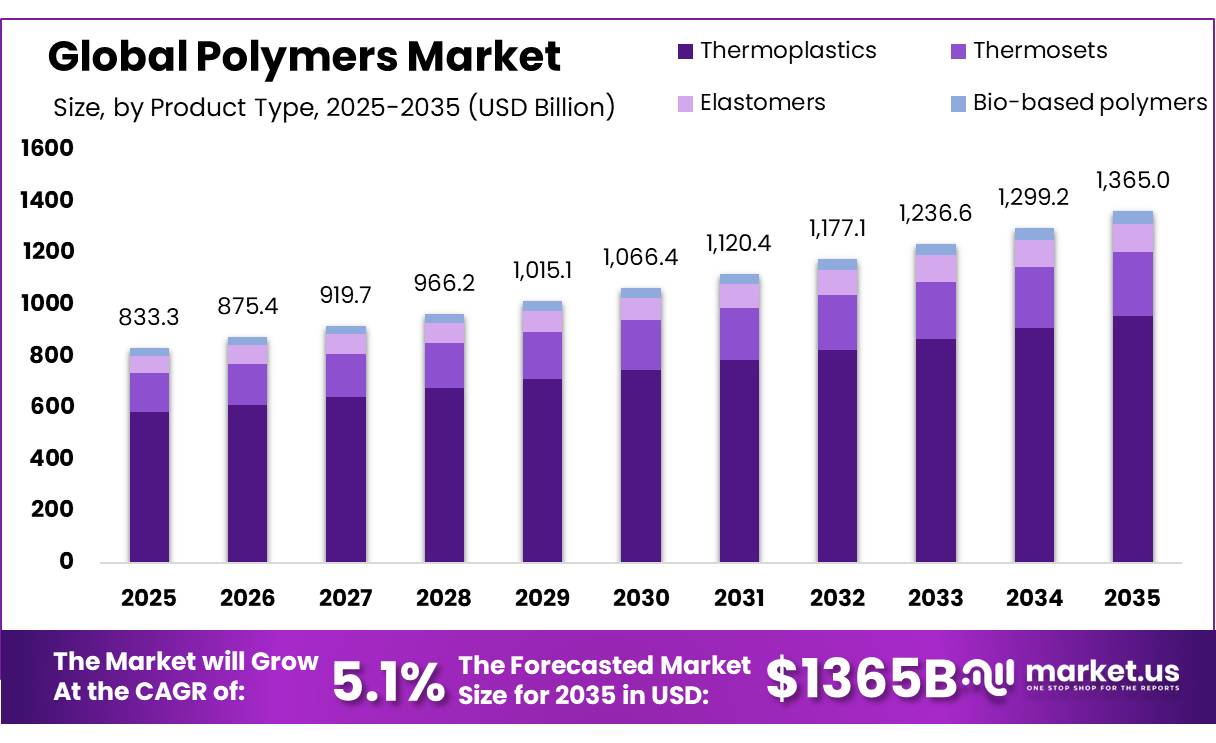

In 2025, the Global Polymers Market was valued at USD 833.3 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 5.1%, reaching about USD 1365 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 41.2% share, holding USD 343.3 billion in revenue.

Polymers form the material base of manufacturing and include thermoplastics, thermosets, elastomers, fibres and resins. Their low weight, chemical resistance, durability and design flexibility support packaging, construction, automotive parts, electrical equipment, healthcare products and consumer goods. Plastics, the largest polymer category, reached production of 430.9 million tonnes in 2024, rising 4.1% year on year. This scale shows that polymer demand is linked with industrial output, urban development and transportation.

- Europe produced 54.6 million tonnes of plastics in 2024 and accounted for 12% of production, compared with 22% in 2006. The industry generated about EUR 398 billion in turnover and supported about 1.5 million employees across 50,650 companies. However, circular polymers represented only 15.4% of European production, showing that fossil-based feedstocks still dominate despite recycling and renewable-feedstock investment.

Key Takeaways

- The global Polymers market was valued at USD 833.3 billion in 2025.

- The global Polymers market is projected to grow at a CAGR of 5.1% and is estimated to reach USD 1365 billion by 2035.

- On the basis of product type, Thermoplastics dominated the global polymer market, accounting for 70.1% of the total market share.

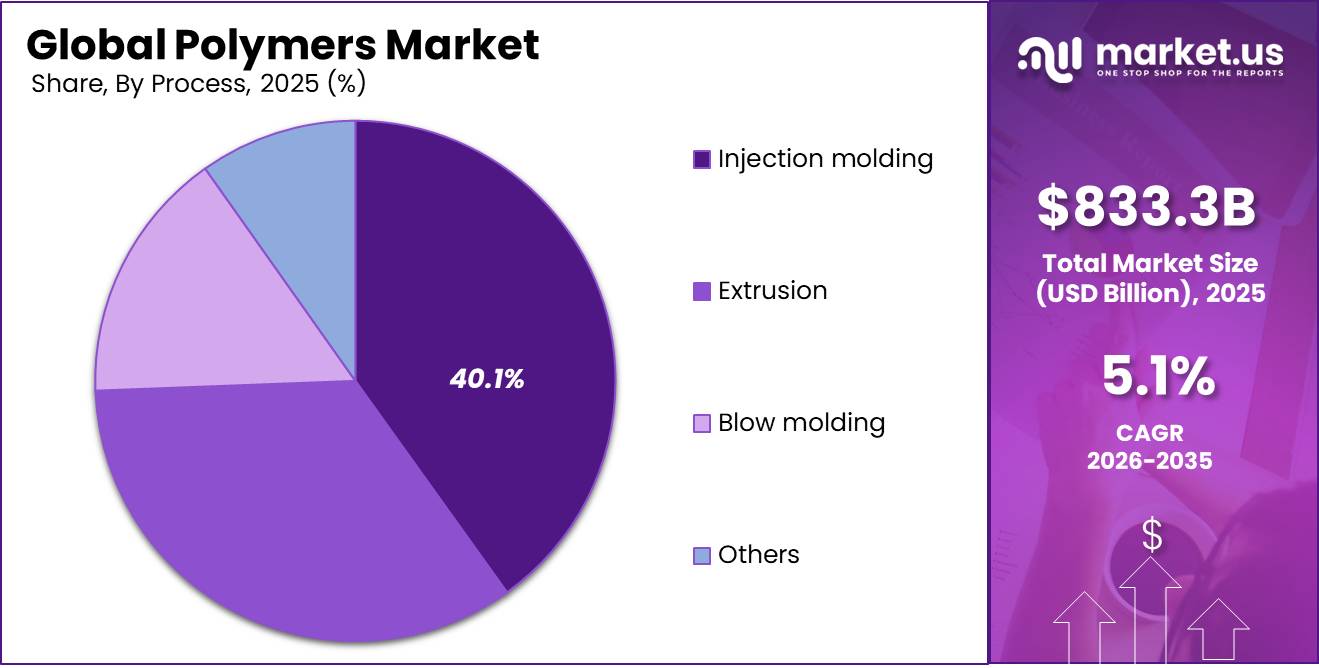

- Based on process, Injection Molding held the dominant position with approximately 40.1% market share.

- By material, Polyethylene (PE) dominated the market with around 35.2% share.

- Based on application, Packaging accounted for nearly 34.9% of the global market share.

- Asia Pacific dominated the global polymer market, holding approximately 41.2% of the total market share.

Packaging remains a major demand centre because polymers provide lightweight barriers, product safety and lower transport costs. The European Commission states that packaging accounts for 40% of plastics used in the European Union, while packaging waste reached 186.5 kilograms per person in 2022. Demand is also supported by infrastructure renovation, electric vehicles, electronics, medical and energy systems, where high-performance polymers replace metal, glass and heavier materials. Growth is increasingly driven by engineered resins offering heat resistance, electrical insulation and impact strength.

Government regulation is becoming an investment driver. The European Union’s Packaging and Packaging Waste Regulation entered into force on 11 February 2025 and will generally apply from 12 August 2026. It aims to make all packaging on the EU market economically recyclable by 2030, increase recycled-plastic use and reduce virgin-material consumption. Such rules should expand demand for recycled polyethylene, recycled PET, compatibilizers, sorting technologies and traceable formulations.

Polymers Market Segmentation

Product Type Analysis

Thermoplastics Lead the Worldwide Polymer Industry.

Thermoplastics represent around 70.1% of the global polymer market share due to their high versatility, recyclability, and lightweight nature. They are extensively used in packaging, automotive, construction, and electronics. Their ease of processing, cost efficiency, and durability drive preference, with rising demand for flexible packaging and lightweight components ensuring continued global growth. The segment is experiencing growth from rising recyclable plastic adoption and investments in sustainable polymers. Thermoplastics are favored for their mechanical properties and manufacturing compatibility. Rapid industrialization and consumer goods expansion in Asia Pacific also boost global thermoplastic demand.

Bio-based Polymers are rapidly growing due to environmental concerns, stricter regulations on single-use plastics, and corporate sustainability efforts. Industries like packaging, automotive, and consumer goods are investing in R&D and supply chain processes for renewable, recyclable, and biodegradable materials. Meanwhile, thermosets and elastomers maintain strong demand in automotive, industrial, electronics, and engineering sectors, valued for their thermal resistance, mechanical strength, and chemical durability, outpacing thermoplastic options.

Process Analysis

Injection Molding Leads the Worldwide Polymer Industry.

Injection Molding leads the global polymer market with around 40.1% share, driven by high production efficiency, cost-effectiveness, and precision in producing complex components. It’s widely used in packaging, automotive, electronics, healthcare, and consumer goods for mass production and compatibility with various thermoplastics. Rising demand for lightweight components and industrial manufacturing supports its global growth.

Extrusion, holding the second-largest share in the global polymer processing market, is integral in producing pipes, films, sheets, and cable insulation within construction, packaging, and electrical industries. Its efficiency and high-throughput capabilities drive the use of multi-layer co-extrusion technology for advanced barrier films and specialty packaging. Blow molding remains steady for plastic products in food, beverage, and household sectors, with increased use of recycled resin-compatible processes aligning with circular economy objectives.

Material Analysis

Polyethylene (PE) Dominates the Global Polymer Market.

Polyethylene (PE) ruled the global polymers market, holding a market share of around 35.2%. The main reason behind the leadership of this segment is that polyethylene is used extensively in applications ranging from packaging and consumer goods to construction, agriculture, and industry. Polyethylene has gained popularity because of its lightweight nature, flexibility, durability, cost-effectiveness, and chemical resistance, among other factors. Rising demand for polyethylene films for packaging purposes, bottles, and industrial packaging has fueled the consumption of the material across different economies.

Polypropylene (PP) is the second-largest material share, favored for its chemical resistance, fatigue strength, and processability in automotive, textiles, medical, and consumer products. Polyvinyl Chloride (PVC) is in demand for construction, particularly in pipes and flooring, due to its durability and cost efficiency. Polyethylene Terephthalate (PET) is crucial for beverage packaging, while Polyurethane (PU) is vital in insulation and coatings. Polystyrene (PS) and Expanded Polystyrene (EPS) are used in food packaging and insulation.

Application Analysis

Packaging Leads the Worldwide Polymer Industry.

Packaging represented about 34.9% of the global polymer market, driven by the demand for lightweight, durable, and cost-effective materials in various sectors like food & beverage and e-commerce. Polymers are widely used in flexible films, containers, and protective packaging due to their barrier properties and processability. Rising packaged food consumption and online retail growth further fuel this demand. The segment sees growth from investments in sustainable packaging, recyclable plastics, and bio-based materials.

Building and Construction is the second-largest application sector for polymers, utilizing them in pipes, insulation panels, and sealants due to their corrosion resistance and thermal efficiency. The push for energy-efficient buildings boosts demand for high-performance polymer materials. The Automotive sector sees steady growth as engineering polymers replace metal components for lightweighting and fuel efficiency among vehicles.

Key Market Segments

By Product Type

- Thermoplastics

- Thermosets

- Elastomers

- Bio‑based polymers

By Process

- Injection molding

- Extrusion

- Blow molding

- Others

By Material

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl chloride (PVC)

- Polyethylene terephthalate (PET)

- Polystyrene (PS) & EPS

- Polyurethane (PU)

- Others

By Application

- Packaging

- Building & construction

- Automotive & transportation

- Electrical & electronics

- Agriculture

- Healthcare / medical

- Others

Driver Analysis

Recycled-content mandates lifting demand for circular polymers.

A second regulation-led growth driver is the rise of mandated and quasi-mandated recycled content, which is creating a parallel premium market for circular polymers. The European Commission notes that plastic packaging must contain recycled content with increasing targets for 2030 and 2040, and all packaging must be recyclable by 2030.

That requirement lifts demand not only for mechanically recycled PCR resins but also for virgin polymers designed for compatibility with collection, sorting, washing, and reprocessing systems; producers that can certify blend stability, food-contact pathways, and color or odor performance gain pricing leverage. In CAGR terms, the direct uplift is moderate but durable because every percentage-point increase in mandated recycled share tightens the market for high-quality recovered feedstock, pulls investment into sorting and compounding, and expands higher-value circular resin portfolios instead of pure commodity tonnage competition

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock cost advantage in gas-based polymer chains | +1.4% | North America core, Middle East export hubs, Asia import-linked converters | Short term (≤ 2 years) |

| Packaging regulation accelerating redesign and resin substitution | +1.1% | EU core, UK aligned markets, multinational packaging supply chains | Short term (≤ 2 years) |

| Recycled-content mandates lifting demand for circular polymers | +0.9% | EU core, North America premium packaging, East Asia recycling corridors | Medium term (2–4 years) |

| Infrastructure and urban systems sustaining durable polymer demand | +1.3% | APAC corridors, Middle East build-out markets, South America spill-over | Medium term (2–4 years) |

| Automotive and electronics lightweighting supporting engineering polymers | +0.8% | China, EU, North America, Northeast Asia manufacturing clusters | Medium term (2–4 years) |

| Waste-policy tightening reshaping product mix toward design-for-recycling grades | +0.7% | EU core, OECD markets, ASEAN transition markets | Long term (≥ 4 years) |

Restraint Analysis

Packaging compliance cost

A major near-term restraint is the direct cost of complying with the EU Packaging and Packaging Waste Regulation, which entered into force on 11 February 2025 and generally applies from 12 August 2026, while also requiring packaging to be recyclable by 2030, adding recycled-content obligations, and exposing non-compliant materials to higher cleanup and producer-responsibility burdens.

This is commercially restrictive because polymer suppliers and converters must fund redesign cycles, migration testing, line validation, labeling changes, and portfolio rationalization within an 18-month-to-5-year compliance window, while the regulation also points toward reuse systems and transport-packaging obligations that can cannibalize some single-use resin volumes over time. The resulting drag is not merely regulatory overhead; it delays customer qualification, raises working capital tied to SKU transitions, increases risk of stranded tooling and obsolete multilayer inventories, and narrows the addressable market for polymers lacking strong recyclability credentials or food-contact compliance pathways.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycling gap | -1.3% | North America core, EU, OECD markets | Medium term (2-4 years) |

| Packaging compliance cost | -1.1% | EU core, UK aligned markets, export suppliers to EU | Short term (≤ 2 years) |

| Trade and tariff friction | -0.9% | North America core, China-linked APAC corridors, global exporters | Short term (≤ 2 years) |

| Feedstock export disruption | -0.8% | U.S. ethane chain, China crackers, Asia polymer trade lanes | Short term (≤ 2 years) |

| Carbon cost pass-through | -0.7% | EU core, carbon-intensive import routes, adjacent OECD markets | Medium term (2-4 years) |

| Upstream demand curbs | -0.6% | EU, OECD markets, ASEAN transition markets | Long term (≥ 4 years) |

Opportunity Analysis

Reuse-system polymers

Reuse is not a present baseline growth engine for polymers because most markets still run on single-use economics, but the PPWR creates a future white space for durable, wash-resistant, trackable polymer formats in transport packaging, pallets, crates, refill packs, and beverage circulation systems. The regulation framework indicates reuse targets by 2030 and 2040, including 10% reuse for selected beverage packaging by 2030 and much higher requirements in transport and industrial packaging, while it also pushes refill availability and deposit-return systems, meaning the opportunity is in redesigning packaging from a unit-sales model into a circulation model.

For polymer companies, that opens new TAM in thicker-wall PP, HDPE, and engineering resins, embedded RFID-ready compounds, and maintenance or replacement loops where value is earned per cycle delivered rather than per kilogram sold once; although absolute virgin tonnage may not rise sharply, supplier revenue per package system can increase through higher-spec resin, molded component integration, and service-led contracts, which makes this a genuine strategic pivot rather than a continuation of current demand

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Food-grade PCR premium | +1.5% | EU core, North America premium packaging, Japan | Short term (≤ 2 years) |

| Reuse-system polymers | +1.2% | EU core, UK aligned markets, urban APAC retail hubs | Medium term (2-4 years) |

| Design-for-recycling compounds | +1.0% | EU, North America core, ASEAN export manufacturers | Short term (≤ 2 years) |

| Chemical recycling feedstock chains | +1.4% | EU, U.S. Gulf Coast, South Korea, Japan | Medium term (2-4 years) |

| Biobased specialty substitution | +0.8% | EU, North America, high-value Asia packaging niches | Long term (≥ 4 years) |

| Non-OECD waste roll-up platforms | +1.1% | India, Southeast Asia, Latin America, Africa corridors | Long term (≥ 4 years) |

Challenges Analysis

Talent and skills transition

Talent and skills transition present a long-term challenge because the polymer industry is being asked to operate simultaneously as a traditional petrochemical sector and as a circular, digitally enabled, low-carbon materials system, and the corresponding skills mix is not yet available at scale; UNEP and UNESCO emphasize the need for green skills to support circular economy transitions, and their workshop on youth skills in 2023 illustrates both the demand for and the current lack of trained professionals in areas such as lifecycle analysis, circular design, advanced recycling, and environmental data management.

This talent gap adds friction by lengthening project start-up times, limiting the throughput of R&D portfolios, and forcing higher per-head compensation to attract scarce profiles, often adding 10–20% to fully loaded costs in strategic roles and stretching innovation lead times from, for example, 18 to 30 months for complex reformulations; because educational pipelines and retraining ecosystems take many years to mature, this challenge has a mitigation horizon well beyond four years and will continue to shave growth potential until green and circular skills become mainstream in the global workforce

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile feedstock logistics | -1.2% | APAC logistics corridors, Middle East–EU lanes, India | Medium term (2-4 years) |

| Circularity execution gap | -1.0% | EU regulatory hubs, OECD markets, export-oriented EMs | Long term (≥ 4 years) |

| Compliance and data complexity | -0.9% | EU regulatory hubs, North America core, global exporters | Medium term (2-4 years) |

| Talent and skills transition | -0.7% | Global, with APAC and EU skills hotspots | Long term (≥ 4 years) |

| Trade regime uncertainty | -0.8% | North America core, China-linked APAC, EU importers | Medium term (2-4 years) |

| Multi-regime policy divergence | -0.6% | EU, OECD, ASEAN, Latin America | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Trade Regulations, fluctuations in crude oil prices, and sustainability policies are impacting the global polymer market.

The worldwide polymer industry is greatly affected by changes in the prices of crude oil, geopolitics, and trade regulations because most traditional types of polymers are made using petrochemicals as their source. Changes in the price of crude oil and natural gas directly affect the cost of polymer manufacturing and materials. Shipping disruptions around the world could also have a negative effect on polymers’ availability and prices.

Furthermore, geopolitical instability in key oil-exporting areas, as well as logistical challenges, continue to cause uncertainties for petrochemical companies and industrial polymer producers worldwide. This is driving more companies to look into local polymer manufacturing, recycling capabilities, and sustainable alternatives to feedstocks.

- According to the International Energy Agency (IEA) Oil 2025 report published in 2025, the global production of polymers and synthetic fibres will require 18.4 million barrels of oil per day by 2030 equivalent to more than one in every six barrels of global oil supply directly reflecting the profound dependence of conventional polymer manufacturing on petrochemical feedstock availability, and the degree to which energy market fluctuations and geopolitical disruptions to oil supply translate into direct input cost and production volatility across the global polymer industry.

Regional Analysis

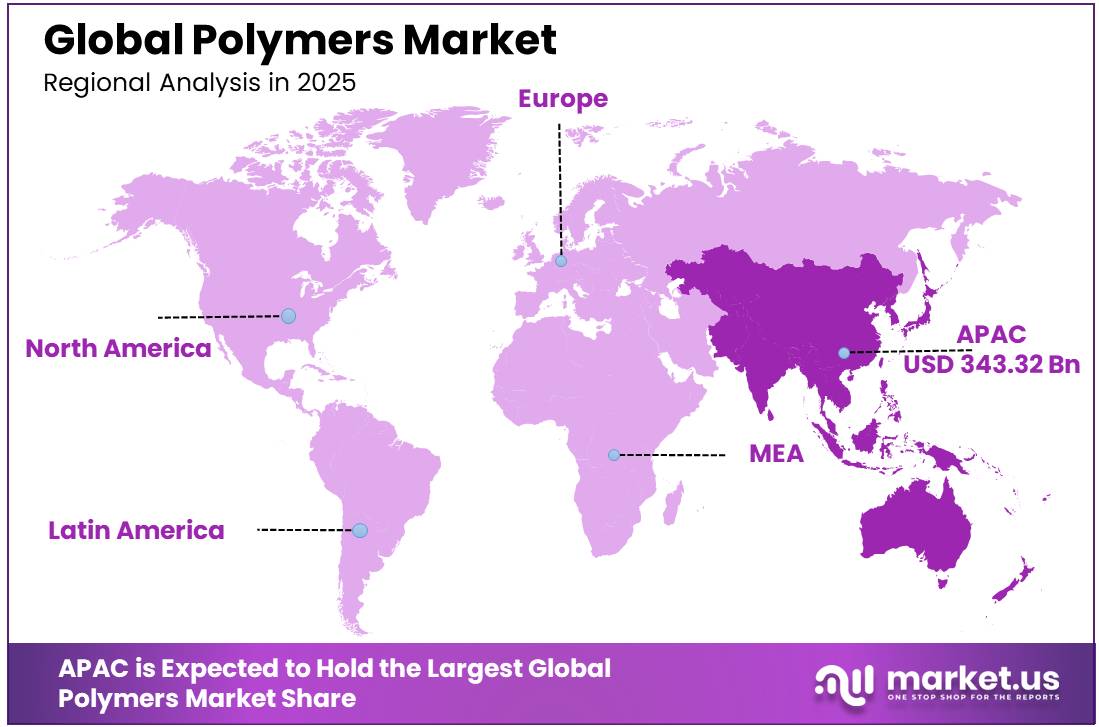

The Global Polymer Market is Led by Asia Pacific.

The Asia Pacific region accounted for the largest market share of about 41.2% in the global polymers market during the forecast period. The key reasons behind the leading position of the region include fast industrialization, extensive manufacturing operations, development of packaging industries, and well-developed infrastructure in China, India, Japan, and other countries of Southeast Asia. Growing demand for polymers in the packaging, automotive, construction, electronic, and consumer goods sectors is fueling significant market growth.

The region benefits from petrochemical facilities, raw material availability, and efficient production. China, a leading global polymer producer and consumer, sees rising demand from its manufacturing base, expanding packaging sector, urbanization, population growth, and e-commerce and food packaging industry growth across Asia Pacific.

Europe had the second-highest market share of the global polymer market as a result of growing demand for sustainable material, recycling technology, and flourishing automotive and construction industries. On the other hand, steady growth can be seen in the North American region because of increasing investments in high-performance polymers and rising packaging and healthcare applications.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The international polymer market features cutthroat competition with large multinational petrochemical firms, specialist polymer producers, and material solutions providers battling each other for supremacy based on factors like innovation, capacity, sustainability, and global logistics network. More and more players are investing in recyclable polymers, renewable resources, lightweight engineering plastics, and innovative technology in order to increase their market reach.

Strategic alliances, capacity enhancement, and investments towards circular economy are being witnessed in the market owing to the rising global demand for advanced polymers. Additionally, there will be increased competition in the global polymer market owing to the rising emphasis on sustainable packaging solutions, electric vehicles, and lightweight materials used in industrial applications.

Market Key Players

- BASF SE

- Dow Inc.

- ExxonMobil Corporation

- SABIC

- LyondellBasell Industries N.V

- INEOS Group Holdings S.A.

- LG Chem Ltd.

- Formosa Plastics Corporation

- Mitsubishi Chemical Group Corporation

- Sumitomo Chemical Co., Ltd.

- Covestro AG

- DuPont de Nemours, Inc.

- Eastman Chemical Company

- Reliance Industries Limited

- Borealis AG

- Others

Key Development

- In February 2025, BASF SE expanded investments in sustainable polymer solutions and advanced recycling technologies to strengthen circular economy initiatives and reduce plastic waste across industrial applications.

- In September 2024, Dow Inc. introduced new recyclable polymer materials designed for sustainable packaging applications to support increasing global demand for eco-friendly packaging solutions.

- In November 2024, SABIC expanded its bio-based and certified renewable polymer portfolio to address rising industrial demand for low-carbon and sustainable material solutions across packaging and consumer goods industries.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 833.3 Bn |

| Forecast Revenue (2035) | USD 1365 Bn |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Thermoplastics, Thermosets, Elastomers, Bio-based Polymers), By Process (Injection Molding, Extrusion, Blow Molding, Others), By Material (Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polyethylene Terephthalate (PET), Polystyrene (PS) & EPS, Polyurethane (PU), Others), By Application (Packaging, Building & Construction, Automotive & Transportation, Electrical & Electronics, Agriculture, Healthcare / Medical, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BASF SE, Dow Inc., ExxonMobil Corporation, SABIC, LyondellBasell Industries N.V, INEOS Group Holdings S.A., LG Chem Ltd., Formosa Plastics Corporation, Mitsubishi Chemical Group Corporation, Sumitomo Chemical Co., Ltd., Covestro AG, DuPont de Nemours, Inc., Eastman Chemical Company, Reliance Industries Limited, Borealis AG, and Other Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |