Quick Navigation

Report Overview

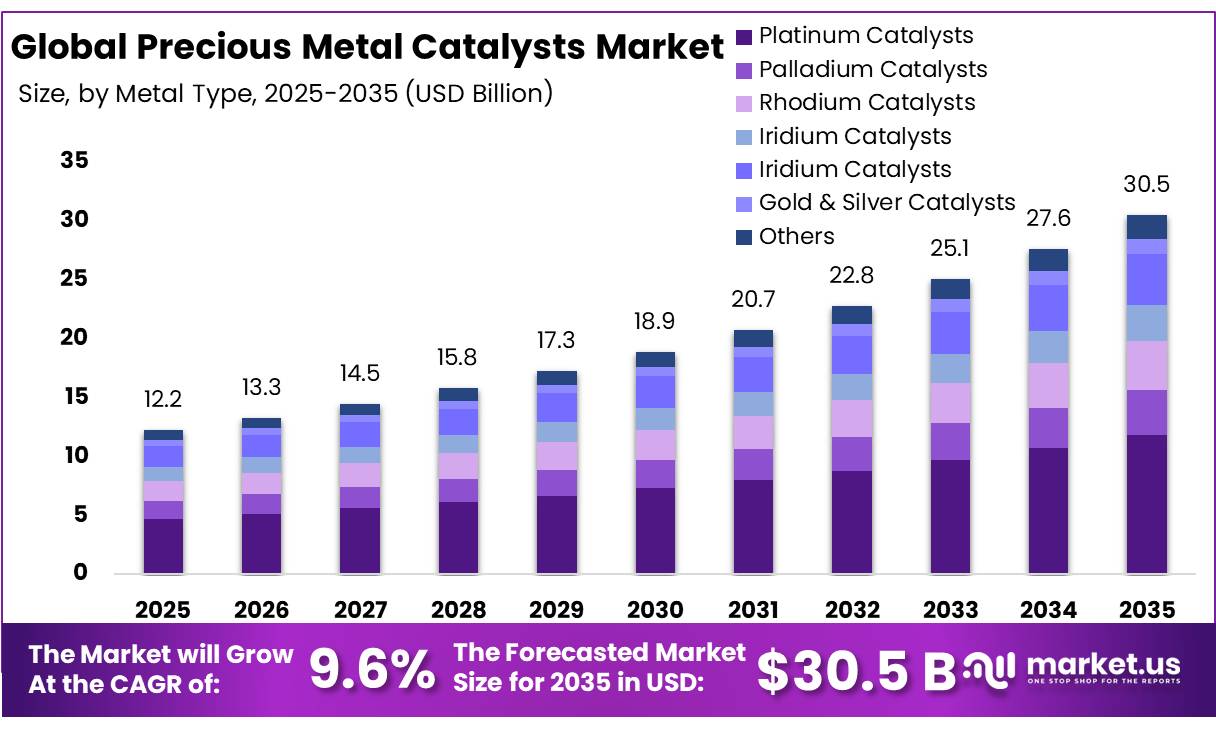

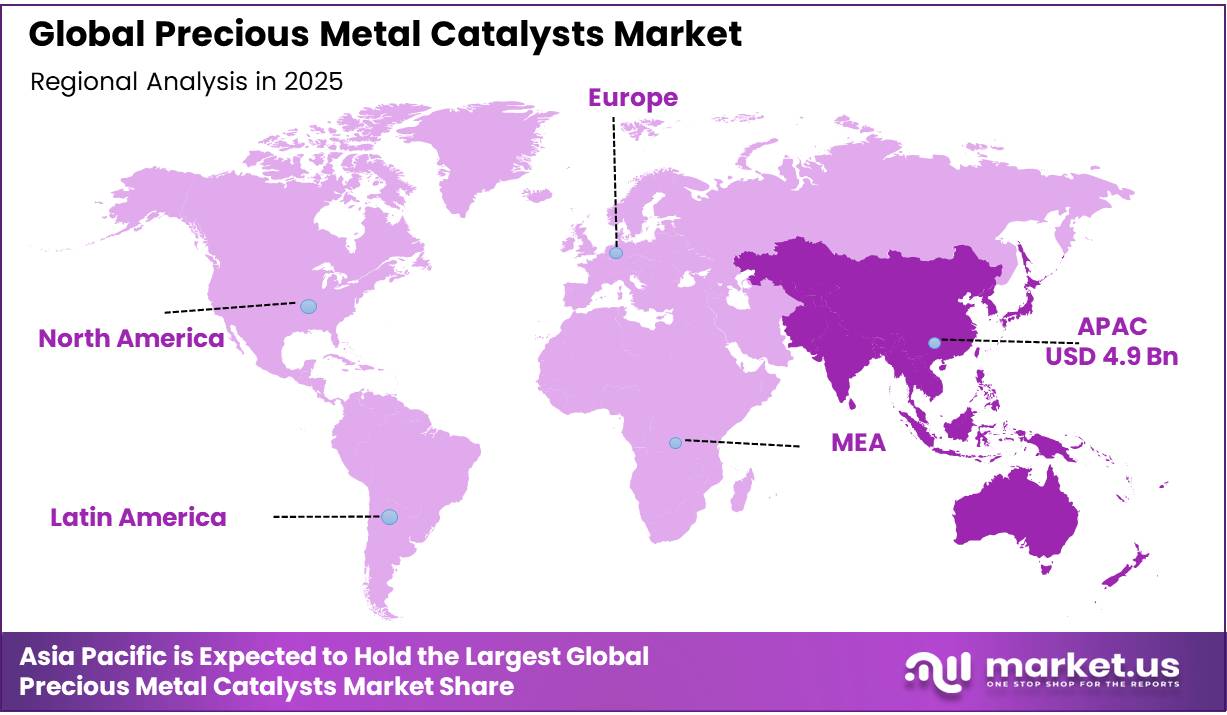

The Global Precious Metal Catalysts Market size is expected to be worth around USD 30.5 Billion by 2035, from USD 12.2 Billion in 2025, growing at a CAGR of 9.6% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 39.8% share, holding USD 4.9 Billion revenue.

Precious metal catalysts are specialized materials primarily based on platinum, palladium, rhodium, ruthenium, iridium, gold, and silver that enable high-efficiency chemical transformations across multiple industrial systems. Their functionality is driven by exceptional surface reactivity, allowing reduced activation energy pathways in oxidation, hydrogenation, reforming, and electrochemical reactions.

These catalysts are integral to automotive emission control systems, where three-way catalysts and diesel after-treatment units support compliance with stringent NOx, CO, and hydrocarbon limits such as Euro 6 and U.S. EPA Tier 3 standards. In refining operations, they facilitate hydrocracking and desulfurization processes essential for producing cleaner fuels, while in chemical and pharmaceutical manufacturing, they enable high-selectivity synthesis routes.

Supply dynamics are shaped by the concentrated availability of platinum-group metals, with major production linked to a limited set of mining regions, contributing to price sensitivity and recycling-driven secondary supply growth. Technological advancements increasingly emphasize atom-efficient designs, including single-atom dispersion and nano-structured supports, reducing metal intensity while maintaining performance.

Furthermore, emerging applications in hydrogen production and fuel cell systems further expand demand pathways, linking catalyst usage directly to clean energy transition infrastructure and low-carbon industrial development.

Key Takeaways

- The global precious metal catalysts market was valued at USD 12.2 billion in 2025.

- The global precious metal catalysts market is projected to grow at a CAGR of 9.6% and is estimated to reach USD 30.5 billion by 2035.

- On the basis of metal type, platinum catalysts dominated the market, constituting 38.7% of the total market share.

- Based on the catalyst form, powdered catalysts led the market, comprising 51.8% of the total market.

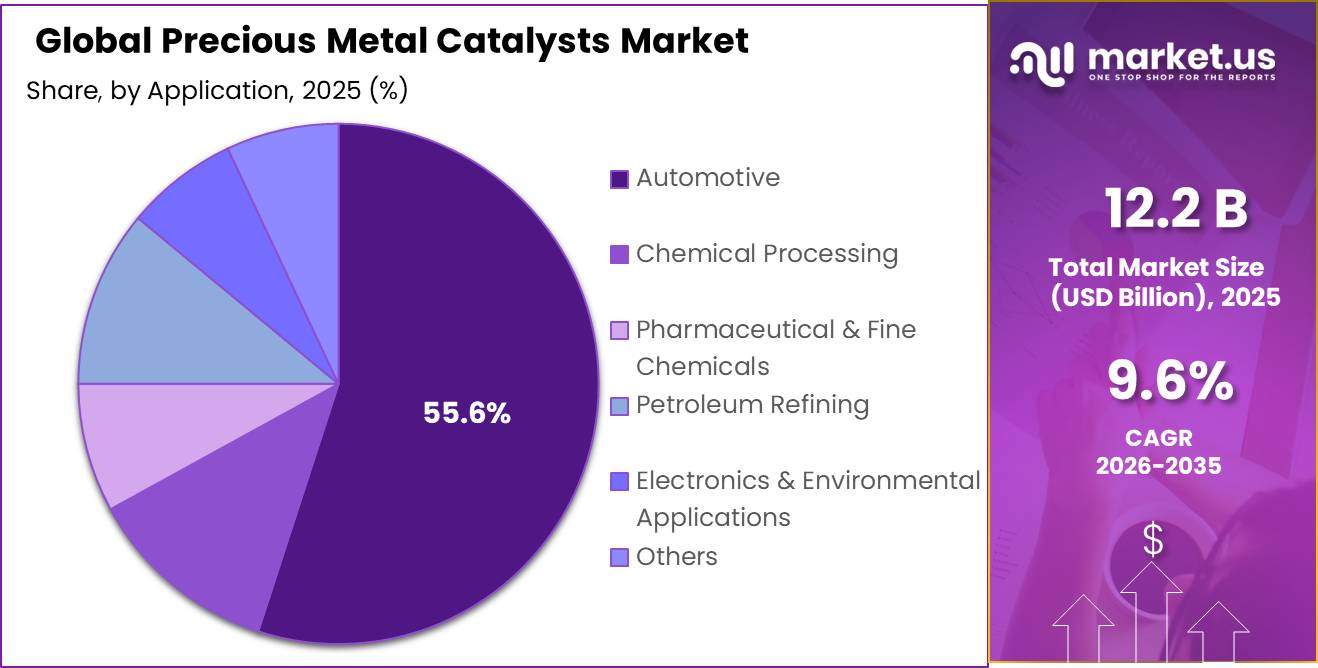

- Among the applications, the automotive sector held a major share in the precious metal catalysts market, 55.6% of the market share.

- Among the manufacturing processes, impregnation is the most considerable within the market, accounting for around 45.6% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the precious metal catalysts market, accounting for 39.8% of the total global consumption.

Metal Type Analysis

Platinum Catalysts are a Prominent Segment in the Market.

Platinum catalysts account for approximately 38.7% share of the global precious metal catalysts market, making them the leading segment by metal type. This dominance is primarily driven by their extensive deployment in automotive emission control systems, where they facilitate efficient oxidation and reduction reactions under stringent regulatory conditions. Their application in petroleum refining processes, particularly in catalytic reforming and hydrocracking, further strengthens consumption, as they enhance fuel quality and process efficiency.

In addition, platinum catalysts are increasingly integrated into hydrogen-related technologies such as fuel cells and electrolysers, reinforcing their relevance in emerging low-carbon energy systems. Their superior thermal stability, resistance to deactivation, and high catalytic efficiency ensure sustained preference despite price volatility linked to constrained supply sources. The combination of mature industrial usage and expanding clean energy applications supports their continued leadership position within the broader precious metal catalyst landscape.

Catalyst Form Analysis

Powdered Catalysts Dominated the Precious Metal Catalysts Market.

Powder catalysts represent the dominant segment within the catalyst form category, accounting for approximately 51.8% share of the global precious metal catalysts market. Their leadership is attributed to their high surface area-to-volume ratio, which enhances reactant contact efficiency and improves reaction kinetics across a wide range of chemical processes. These catalysts are extensively utilized in fine chemical synthesis, pharmaceutical intermediates, and petroleum refining operations, where precise control over reaction pathways and selectivity is essential.

Their fine particulate structure allows flexible dispersion on various supports, enabling customization for specific industrial requirements. Powder catalysts are widely preferred in laboratory-scale and batch processing applications due to ease of handling and regeneration. Despite challenges related to recovery and separation in some continuous systems, their versatility, cost-effectiveness in formulation, and strong catalytic performance sustain their widespread adoption across both established and emerging industrial applications.

Manufacturing Process Analysis

Impregnation Held a Major Share of the Precious Metal Catalysts Market.

The impregnation method represents the dominant manufacturing process in the precious metal catalysts market, accounting for approximately 45.6% share. Its leadership is driven by its simplicity, scalability, and cost efficiency in dispersing active metal components onto porous support materials such as alumina, silica, and activated carbon. This technique enables precise control over metal loading levels, making it highly suitable for large-scale industrial production of catalysts used in automotive emission control, petroleum refining, and chemical synthesis applications.

The process supports strong metal-support interactions, which enhance catalytic stability and performance under high-temperature and chemically aggressive environments. Its compatibility with multiple noble metals, including platinum, palladium, and rhodium, further strengthens its widespread adoption. Despite the emergence of advanced deposition technologies, impregnation continues to remain the preferred method due to its established industrial reliability and ability to deliver consistent catalyst quality across diverse end-use sectors.

Application Analysis

Precious Metal Catalysts Are Mostly Utilized in the Automotive Sector.

The automotive segment holds the leading position in the precious metal catalysts market, accounting for approximately 55.6% share. This dominance is primarily driven by the extensive use of platinum, palladium, and rhodium in catalytic converters designed to reduce vehicular emissions. These catalysts enable the conversion of harmful gases such as carbon monoxide, nitrogen oxides, and unburned hydrocarbons into less toxic compounds, supporting compliance with increasingly stringent emission regulations across major automotive markets. High vehicle production volumes, particularly in emerging economies, further reinforce demand intensity.

The segment further benefits from the growing penetration of hybrid vehicles, which continue to rely on internal combustion engine systems requiring advanced emission control technologies. Additionally, continuous tightening of environmental standards has led to higher catalyst loading and more durable formulations, sustaining strong consumption of precious metal catalysts within automotive exhaust treatment systems globally.

Key Market Segments

By Metal Type

- Platinum Catalysts

- Palladium Catalysts

- Rhodium Catalysts

- Iridium Catalysts

- Ruthenium Catalysts

- Gold & Silver Catalysts

- Others

By Catalyst Form

- Powder Catalysts

- Pellet / Bead Catalysts

- Extrudates & Honeycomb Structures

- Wash-coated Monolith Catalysts

By Manufacturing Process

- Impregnation

- Chemical Vapor Deposition (CVD) / Atomic Layer Deposition

- Sol-Gel / Precipitation Methods

- Electrochemical Deposition

- Others

By Application

- Automotive

- Chemical Processing

- Pharmaceutical & Fine Chemicals

- Petroleum Refining

- Electronics & Environmental Applications

- Others

Market Dynamics

Driver Analysis - Expanding Emission Regulations Drive Precious Metal Catalysts

Strengthening emission compliance frameworks across road transport and industrial operations has intensified reliance on platinum group metal catalysts in exhaust after-treatment systems. In the United States, the EPA Tier 3 standards introduced fleet average NOx limits of 0.03 g/mi for light-duty vehicles, requiring high-performance three-way catalytic converters integrating platinum, palladium, and rhodium systems to simultaneously control CO, NOx, and hydrocarbons under stoichiometric conditions.

Similar tightening under Euro 6/VI regulations enforces NOx caps of 80 mg/km for diesel passenger vehicles, further reinforcing catalyst loading intensity and durability requirements across engine platforms. Diesel oxidation catalysts and selective catalytic reduction systems in heavy-duty applications demonstrate measurable conversion efficiencies, with EPA-verified retrofit systems reporting up to 50% reductions in CO and hydrocarbons and around 20% particulate matter reduction under compliant operating conditions in diesel engines.

Such performance thresholds necessitate higher dispersion of active metals and advanced washcoat engineering to sustain activity over extended duty cycles exceeding 150°C exhaust conditions. The studies have shown three-way platinum-rhodium systems achieving NOx conversion efficiencies in the range of 40-60% under controlled air-fuel feedback conditions, highlighting the sensitivity of catalytic performance to combustion stoichiometry stability.

Beyond mobility, industrial combustion sources and refinery heaters are increasingly required to adopt catalytic abatement units to meet sub-ppm emission ceilings for NOx and volatile organic compounds in regulated zones. These systems rely on similar noble metal chemistries, reinforcing cross-sector demand for platinum and palladium-based formulations.

Restraint Analysis - Volatile Precious Metal Supply Costs Challenge Market

Global supply conditions for platinum, palladium, rhodium, and other platinum-group metals used in catalyst systems remain structurally concentrated, with production heavily dependent on a limited set of mining regions, particularly South Africa and Russia, which together account for the majority of global output. According to USGS data, more than 90% of historical platinum-group metal production has originated from these regions, underscoring a high degree of geographic concentration in primary supply chains. This concentration exposes downstream catalyst manufacturing to disruptions arising from energy constraints, labor disruptions, and policy shifts in a narrow set of jurisdictions.

Mine output characteristics further intensify supply rigidity, as platinum-group metals are typically co-produced as by-products of nickel and copper mining, limiting the responsiveness of supply to price signals. Annual global production volumes remain relatively inelastic in the short term, with USGS reporting total PGM output in the range of only several million ounces per year, reinforcing constrained scalability.

Cost structures are further influenced by deep ore grades, often measured in low parts-per-million concentrations, which increases energy intensity and extraction complexity. Combined with long development timelines for new mining capacity, this results in persistent exposure of catalyst manufacturers to input price volatility and intermittent supply gaps, particularly during periods of geopolitical tension or energy price escalation affecting major producing regions.

Opportunity Analysis - Hydrogen Economy Expansion Creates Precious Metal Opportunities

Low-emission hydrogen systems increasingly rely on electrochemical pathways where platinum, iridium, and ruthenium-based catalysts are embedded in both hydrogen production and utilization stages. Proton exchange membrane (PEM) electrolysers, a key industrial configuration, operate through water-splitting reactions requiring noble metal catalysts at both electrodes, with total platinum group metal loading in conventional designs historically exceeding 3.0 mg/cm² of electrode area.

The U.S. Department of Energy technical targets indicate a reduction pathway toward 0.5 mg/cm² by 2026 and 0.125 mg/cm² in long-term system designs, reflecting ongoing emphasis on material efficiency improvements while maintaining reaction kinetics and durability under acidic operating conditions.

- Global hydrogen production is estimated at around 50 billion kg per year, predominantly from fossil-based processes, positioning electrolysis as a scaling alternative for low-carbon hydrogen generation.

In parallel, installed electrolyser capacity has reached the gigawatt scale and is expected to expand significantly through pipeline projects targeting multi-hundred-gigawatt deployment levels by 2030, indicating rising embedded demand for catalyst systems in energy conversion infrastructure.

Fuel cell applications further extend platinum usage into energy utilization systems, where hydrogen oxidation and oxygen reduction reactions depend on highly active catalyst surfaces to sustain power densities under variable load conditions. Industrial fuel cell stacks integrate catalyst-coated membranes operating under high current densities, requiring stability against acidic environments, thermal cycling, and water management constraints over extended lifetimes.

Emerging Trend Analysis - Rising Shift Toward High-Dispersion and Atom-Efficient Catalyst Designs

A pronounced shift in catalyst engineering has been observed toward maximizing metal atom utilization through highly dispersed and atomically isolated active sites, driven by the intrinsic scarcity and cost intensity of platinum group metals. Single-atom catalyst architectures are explicitly designed to expose nearly all metal atoms for reaction participation, achieving theoretical utilization close to 100%, compared with conventional nanoparticle systems where a significant fraction of atoms remain buried and inactive.

This structural transition is reinforced by the fact that noble metals account for only a small fraction of global crustal abundance, estimated at around a few parts per million scale for platinum-group elements, creating strong material efficiency imperatives. In proton exchange membrane electrolysers, platinum-group metal loadings are already being reduced toward sub-milligram per square centimeter ranges under development targets defined for next-generation systems, reflecting ongoing efforts to preserve catalytic performance while minimizing material intensity.

Advances in synthesis routes, including impregnation refinement, atom trapping, and controlled thermal treatments, have enabled stable dispersion at higher metal loadings while suppressing sintering phenomena. This has allowed catalytic systems to maintain activity in oxidation and reforming reactions while significantly lowering total precious metal inventory per functional unit. The convergence of atomic-scale dispersion control with durability under industrial temperature and chemical stress conditions is increasingly shaping catalyst design toward ultra-efficient material architectures rather than bulk metal utilization.

Geopolitical Impact Analysis

Supply Chain Strain and Strategic Reconfiguration in Platinum-Group Metal Flows Under Geopolitical Fragmentation.

Geopolitical tensions have increasingly reshaped the flow of platinum-group metals, which are essential inputs in automotive catalysts, petrochemical refining, and chemical synthesis systems. Supply concentration remains structurally high, with USGS indicating that South Africa accounts for more than 70% of global platinum output and Russia being a leading source of palladium production, creating exposure to jurisdiction-specific disruptions.

The Russian palladium supply to the United States has been affected by trade restrictions and conflict-related constraints, while South African output has faced operational pressures from deep-level mining costs, labor disputes, and electricity instability. In modeled disruption scenarios by USGS, restrictions on imports from Russia alone were shown to reduce available palladium quantities by approximately 5% and increase equilibrium prices by around 24%, reflecting tight substitution elasticity in the supply chain.

These constraints directly affect catalyst manufacturing, where platinum, palladium, and rhodium loadings are critical for achieving emission compliance under stringent standards. Automotive catalytic converters remain the largest consumption channel, and any supply tightening propagates quickly into downstream production planning due to limited short-term material substitution options.

Similarly, export control measures and import restrictions on precious metal alloys in certain jurisdictions are further tightening cross-border material flows, reinforcing regional segmentation of supply chains. This has increased reliance on recycling from spent catalytic converters and secondary recovery streams, although recovery rates remain insufficient to fully offset primary supply variability during disruption periods.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Precious Metal Catalysts Market.

In 2025, the Asia Pacific dominated the global precious metal catalysts market, holding about 39.8% of the total global consumption, supported by dense industrial activity and large-scale manufacturing ecosystems across China, India, Japan, and South Korea. Asia Pacific accounts for the majority of global demand for platinum-group metal catalysts, reflecting its concentration of automotive production, refining capacity, and chemical synthesis operations.

Automotive applications form the primary consumption base, where catalytic converters using platinum, palladium, and rhodium are embedded across gasoline and diesel vehicles to comply with tightening emission thresholds. In parallel, refinery operations across China and India deploy these catalysts in hydrocracking and reforming units to meet cleaner fuel specifications and rising domestic fuel demand.

Rapid expansion in pharmaceutical and fine chemical manufacturing further reinforces catalyst utilization, particularly in hydrogenation and selective oxidation processes requiring high-purity outputs. Recycling infrastructure development, though improving, still lags primary demand intensity, reinforcing continued reliance on imported PGMs and strengthening the Asia Pacific’s position as the most structurally significant demand center in the global precious metal catalysts value chain.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Companies operating in the precious metal catalysts space focus heavily on improving metal utilization efficiency to reduce dependency on high-cost platinum-group inputs while maintaining catalytic performance. Significant emphasis is placed on recycling and closed-loop recovery systems, particularly from spent automotive catalysts, to secure secondary metal supply and stabilize input costs. Firms further invest in application-specific formulation development, tailoring catalyst structures for stricter emission standards in automotive systems and higher selectivity requirements in chemical and refining processes.

Strategic partnerships with end-use industries support co-development of next-generation emission control and hydrogen technologies. Additionally, geographic diversification of production and supply chains is pursued to mitigate risks linked to concentrated mining regions, while R&D investments target durability improvements under high-temperature and corrosive industrial environments.

The following are some of the major players in the industry

- Johnson Matthey Plc

- BASF SE

- Umicore

- Heraeus Group

- Clariant AG

- Evonik Industries AG

- Honeywell International Inc.

- TANAKA Precious Metal Group

- Thermo Fisher Scientific Inc.

- American Elements

- CHIMET S.p.A.

- Sabin Metal Corporation

- Haldor Topsoe A/S

- R. Grace & Co.

- Alfa Aesar

- Other Key Players

Key Development

- In March 2026, BASF commissioned the world’s first production facility for X3D technology-based catalysts in Ludwigshafen. The company stated that the additive-manufactured catalysts enhance surface area, reduce reactor pressure drop, and improve mechanical strength through optimized open structures.

- In January 2025, Mattiq announced a strategic partnership with Heraeus Precious Metals to develop and commercialize advanced electrocatalyst materials for green hydrogen production.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$12.2 Bn |

| Forecast Revenue (2035) | US$30.5 Bn |

| CAGR (2026-2035) | 9.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Metal Type (Platinum Catalysts, Palladium Catalysts, Rhodium Catalysts, Iridium Catalysts, Ruthenium Catalysts, Gold & Silver Catalysts, and Others), By Catalyst Form (Powder Catalysts, Pellet / Bead Catalysts, Extrudates & Honeycomb Structures, and Wash-coated Monolith Catalysts), By Manufacturing Process (Impregnation, Chemical Vapor Deposition (CVD) / Atomic Layer Deposition, Sol-Gel / Precipitation Methods, Electrochemical Deposition, and Others), By Application (Automotive, Chemical Processing, Pharmaceutical & Fine Chemicals, Petroleum Refining, Electronics & Environmental Applications, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Johnson Matthey Plc, BASF SE, Umicore, Heraeus Group, Clariant AG, Evonik Industries AG, Honeywell International Inc., TANAKA Precious Metal Group, Thermo Fisher Scientific Inc., American Elements, CHIMET S.p.A., Sabin Metal Corporation, Haldor Topsoe A/S, W. R. Grace & Co., Alfa Aesar, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |