Quick Navigation

Report Overview

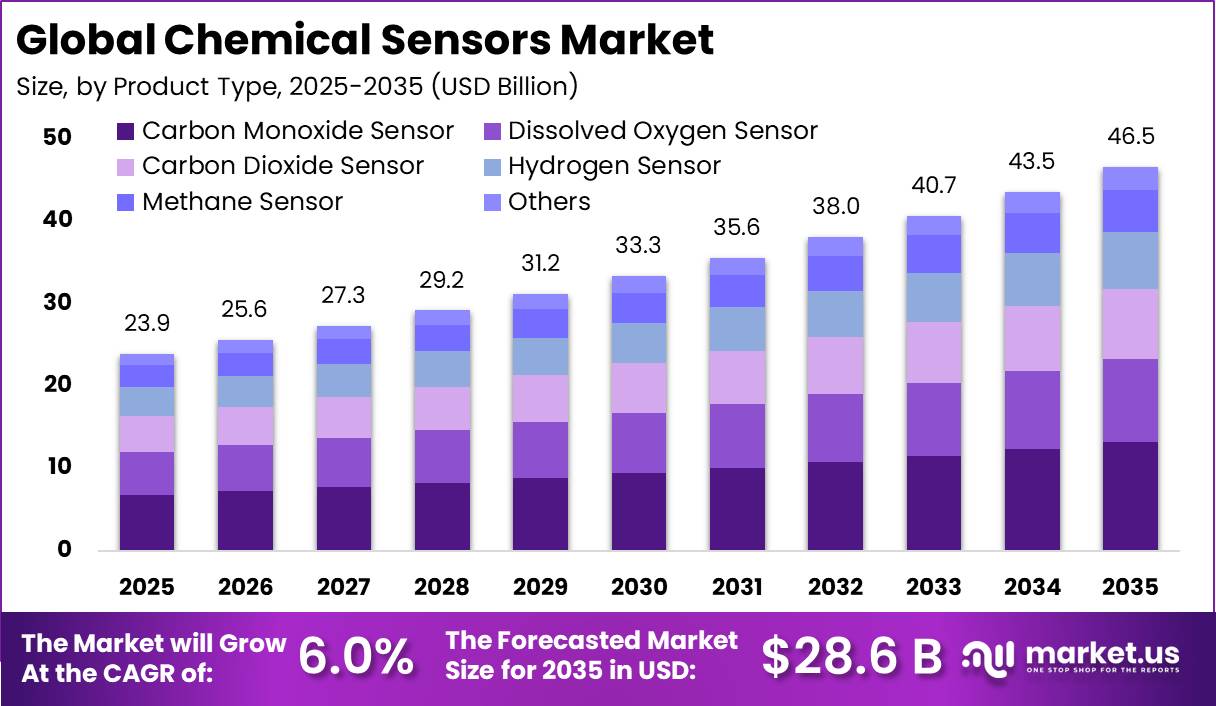

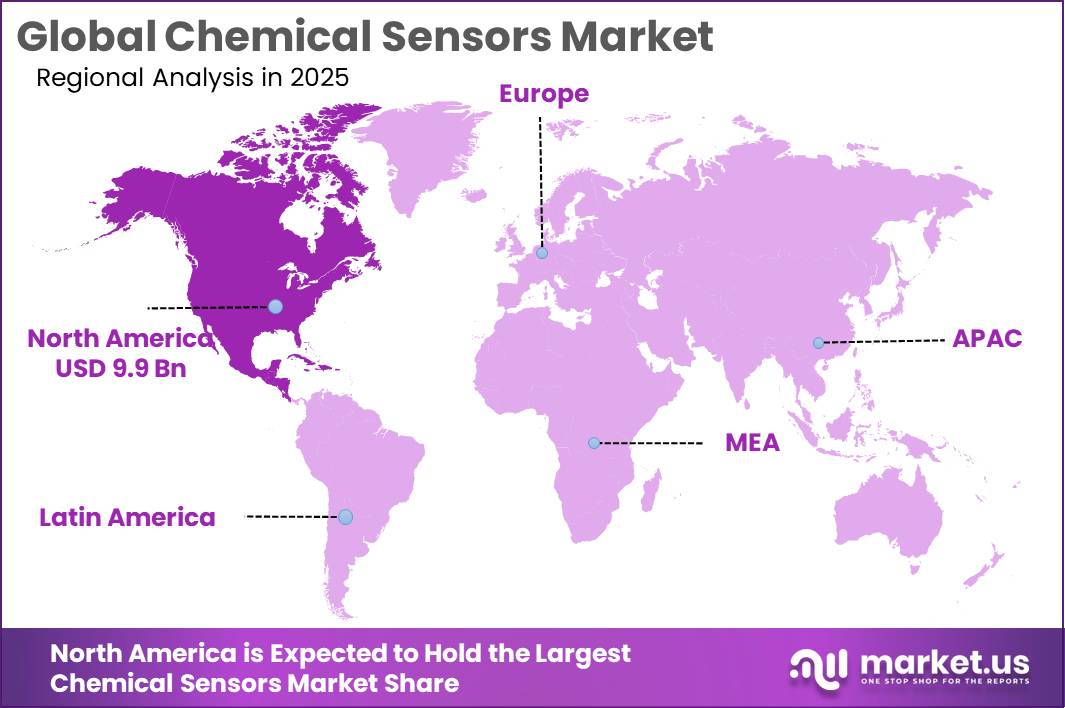

The Global Chemical Sensors Market size is expected to be worth around USD 28.6 Billion by 2035, from USD 23.9 Billion in 2025, growing at a CAGR of 6.0% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 41.70% share, holding USD 9.9 Billion revenue.

Chemical sensors are emerging as critical tools for industrial, environmental, healthcare, food-safety, and precision-agriculture applications, as they detect gases, ions, nutrients, toxins, pH, humidity, volatile organic compounds, and contaminants in real time. Their industrial relevance is strengthened by food-security pressure: FAO reported that about 673 million people faced hunger in 2024, while nearly 2.3 billion people experienced moderate or severe food insecurity, creating stronger demand for technologies that improve crop productivity, water quality, storage safety, and input efficiency.

The industrial scenario is increasingly shaped by agriculture’s need to produce more with fewer resources. FAO stated that the global population is approaching 9.7 billion by 2050, requiring 50% more food, feed, and fibre than in 2012, along with 25% more freshwater. Chemical sensors support this transition by enabling soil-nutrient monitoring, fertilizer optimization, pesticide-residue detection, greenhouse-gas tracking, and early identification of crop stress.

Demand is also supported by productivity and sustainability targets. OECD-FAO projects global agricultural and fish production to rise 14% during 2025–2034, while direct agricultural greenhouse-gas emissions are expected to increase 6%, making sensor-enabled monitoring important for reducing waste, improving compliance, and supporting climate-smart farming.

Government and institutional initiatives are reinforcing adoption. The USDA’s precision agriculture programs highlight site-specific crop management using technologies that manage soil, nutrient, moisture, weed, and crop-growth variability within fields. In Europe, the 2025 EU Soil Monitoring Directive enables monitoring of soil contaminants, including microplastics and nanoplastics, supporting broader use of field-level chemical detection systems.

Thermo Fisher Scientific Inc. was also active in 2025. It agreed to acquire Solventum’s purification and filtration business for about USD 4.1 billion, completed the transaction for about USD 4.0 billion, and announced a definitive agreement to acquire Clario for USD 8.875 billion in cash plus potential future payments. These moves strengthen its life-science, filtration, and data capabilities relevant to analytical and chemical-monitoring ecosystems.

Key Takeaways

- Chemical Sensors Market size is expected to be worth around USD 28.6 Billion by 2035, from USD 23.9 Billion in 2025, growing at a CAGR of 6.0%.

- Carbon Monoxide Sensor held a dominant market position, capturing more than a 28.40% share of the global chemical sensors market.

- Electrochemical held a dominant market position, capturing more than a 46.10% share of the global chemical sensors market.

- Gas held a dominant market position, capturing more than a 68.20% share of the global chemical sensors market.

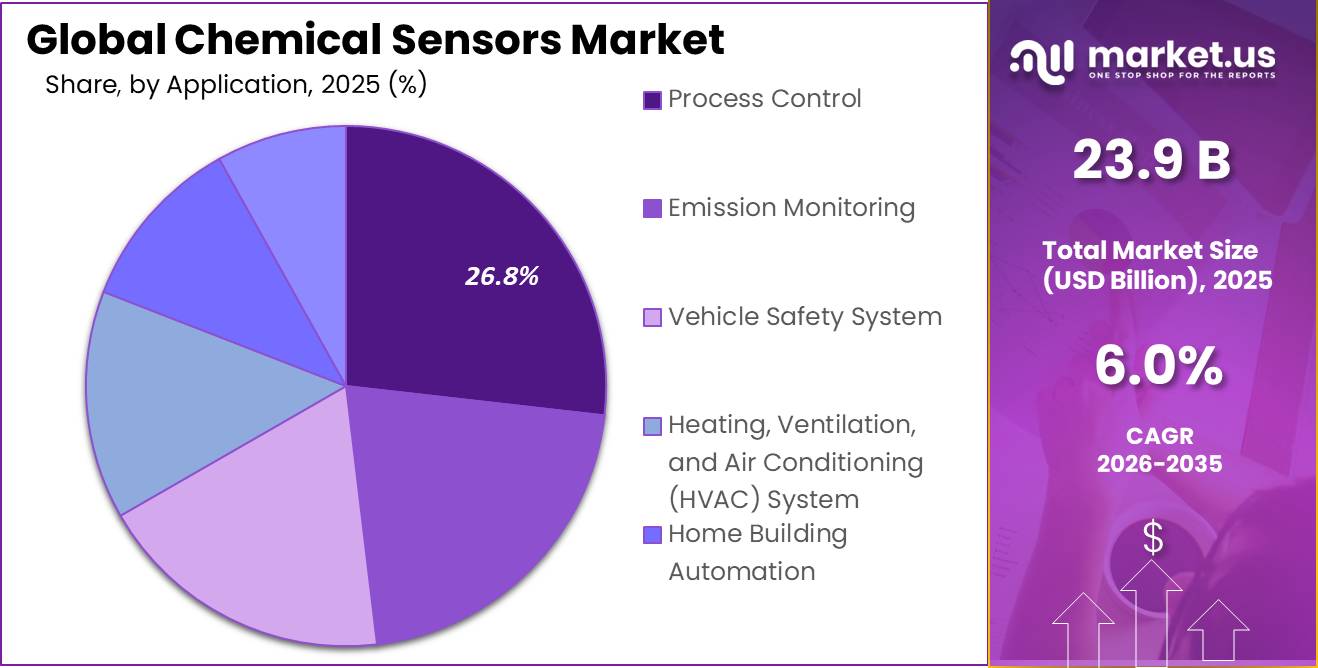

- Process Control held a dominant market position, capturing more than a 26.80% share of the global chemical sensors market.

- Oil and Gas held a dominant market position, capturing more than a 31.60% share of the global chemical sensors market.

- North America held a dominant position in the global Chemical Sensors Market, capturing 41.70% of the total market and reaching a value of USD 9.9 Billion.

By Product Type Analysis

Carbon Monoxide Sensor dominates with 28.40% share due to growing demand for air safety and continuous gas monitoring across industries.

In 2025, Carbon Monoxide Sensor held a dominant market position, capturing more than a 28.40% share of the global chemical sensors market by product type. This leadership was supported by the rising need for reliable detection of harmful gases across industrial facilities, commercial buildings, and residential environments. Carbon monoxide remains one of the most critical gases to monitor because it is colorless, odorless, and difficult to detect without dedicated sensing technology. As safety regulations continued to strengthen across manufacturing plants, energy facilities, and enclosed public spaces, adoption of carbon monoxide sensors increased steadily.

By Technology Analysis

Electrochemical dominates with 46.10% share due to its high sensitivity, reliable performance, and broad industrial adoption.

In 2025, Electrochemical held a dominant market position, capturing more than a 46.10% share of the global chemical sensors market by technology. The segment’s strong position was supported by its ability to provide accurate and fast detection of chemical substances across a wide range of applications. Electrochemical sensing technology continued to gain preference because of its strong sensitivity, low power requirements, and dependable performance in detecting gases and chemical compounds even at low concentrations.

By Particle Type Analysis

Gas dominates with 68.20% share driven by strong demand for continuous monitoring and industrial safety applications.

In 2025, Gas held a dominant market position, capturing more than a 68.20% share of the global chemical sensors market by particle type. The segment maintained its leading position due to the increasing need for accurate gas detection across industrial, commercial, and environmental applications. Industries continued to prioritize gas sensing technologies to monitor air quality, control emissions, and improve operational safety in environments where hazardous or invisible gases can create serious risks.

By Application Analysis

Process Control dominates with 26.80% share supported by rising industrial automation and the need for real-time monitoring.

In 2025, Process Control held a dominant market position, capturing more than a 26.80% share of the global chemical sensors market by application. The segment’s strong performance was driven by increasing demand for accurate monitoring and control systems across industrial operations. Chemical sensors became an important part of process control environments by helping manufacturers maintain product consistency, improve operational efficiency, and reduce process interruptions through continuous measurement and analysis.

By End-use Analysis

Oil and Gas dominates with 31.60% share driven by increasing focus on safety, emissions control, and continuous monitoring.

In 2025, Oil and Gas held a dominant market position, capturing more than a 31.60% share of the global chemical sensors market by end-use industry. The segment maintained its leading position due to the industry’s continuous requirement for accurate detection and monitoring of gases, chemicals, and environmental conditions across exploration, production, refining, and transportation activities. Chemical sensors remained essential for improving operational safety, preventing leaks, and maintaining process efficiency in complex and high-risk environments.

Key Market Segments

By Product Type

- Dissolved Oxygen Sensor

- Carbon Dioxide Sensor

- Carbon Monoxide Sensor

- Hydrogen Sensor

- Methane Sensor

- Others

By Technology

- Optical

- Electrochemical

- Catalytic Bead

- Thermal

- Others

By Particle Type

- Solid

- Liquid

- Gas

By Application

- Process Control

- Emission Monitoring

- Vehicle Safety System

- Heating, Ventilation, and Air Conditioning (HVAC) System

- Home Building Automation

- Others

By End-use Industry

- Oil and Gas

- Chemical

- Pharmaceutical

- Food and Beverage

- Water and Wastewater

- Healthcare

- Others

Emerging Trends

Real-Time Smart Food Monitoring is Emerging as a Major Trend in the Chemical Sensors Market

One of the latest trends shaping the chemical sensors market is the growing use of real-time smart monitoring systems across the food industry. Food manufacturers are increasingly shifting from periodic testing to continuous sensing technologies that can detect chemical changes instantly during processing, storage, packaging, and transportation. Chemical sensors are being integrated into connected monitoring systems to track gas levels, freshness indicators, contamination risks, and environmental conditions with faster response times.

- According to the Food and Agriculture Organization (FAO), around 13.2% of food produced globally is lost between post-harvest and retail stages each year.

This level of food loss has encouraged producers to invest in technologies that improve product monitoring and reduce spoilage. Chemical sensors support these goals by providing early warning signals that allow corrective actions before product quality declines.

Government-Led Digital Food Safety Programs are Encouraging Sensor Integration

Governments and food authorities are increasingly promoting digital monitoring and preventive food safety systems, creating momentum for chemical sensor deployment. Rather than depending only on final-stage inspections, food programs are encouraging continuous monitoring practices that improve transparency and strengthen consumer confidence. Chemical sensors fit well into this approach because they provide immediate measurement and support faster decision-making.

According to the World Health Organization (WHO), unsafe food affects approximately 600 million people annually and causes about 420,000 deaths worldwide every year. These numbers continue to influence policy actions aimed at improving food control systems and strengthening surveillance capabilities. Programs supported by international food organizations are encouraging smarter inspection models and technology-enabled monitoring across production facilities.

Drivers

Rising Focus on Food Safety and Contamination Monitoring is Driving Chemical Sensor Adoption

Food safety has become one of the strongest growth drivers for the chemical sensors market as food manufacturers and regulatory bodies continue to increase monitoring across production, storage, and distribution processes. Chemical sensors are increasingly used to detect gases, chemical residues, spoilage indicators, and contamination in food environments before products reach consumers. Their ability to deliver fast and continuous monitoring supports safer food handling and better quality control.

- According to the World Health Organization (WHO), more than 866 million cases of foodborne illnesses and around 1.52 million deaths were reported globally in 2021 due to food-related hazards, including biological and chemical contamination. In addition, the World Bank estimated that foodborne diseases create an annual productivity loss of nearly US$95.2 billion in low- and middle-income economies.

Government Food Safety Programs and Regulatory Monitoring Supporting Sensor Deployment

Government initiatives and stricter food monitoring frameworks are creating long-term opportunities for chemical sensor deployment across the food industry. Regulatory agencies are placing greater emphasis on preventive monitoring, traceability, and real-time detection systems to reduce contamination events and improve public health outcomes. Chemical sensors support these objectives by enabling continuous measurement and immediate alerts when unsafe conditions appear.

Organizations including WHO and FAO continue promoting stronger food control systems through science-based safety standards and modern risk assessment approaches. Their food safety strategies encourage countries to strengthen surveillance across the complete food chain—from production to final consumption. In the United States, food safety remains a major public health priority, with government estimates showing around 48 million foodborne illness cases, 128,000 hospitalizations, and approximately 3,000 deaths annually.

Restraints

High Implementation and Maintenance Costs Continue to Limit Chemical Sensor Adoption

One of the major restraining factors for the chemical sensors market is the high cost associated with installation, calibration, maintenance, and continuous monitoring systems. While chemical sensors improve safety and quality control, many small and mid-sized food processing facilities still face challenges in adopting advanced sensing technologies due to budget limitations and operational complexity. The cost burden becomes more visible when facilities require multiple sensors, real-time analytics platforms, periodic calibration, and trained personnel to maintain accuracy.

This challenge is particularly relevant in the food industry, where margins are often under pressure despite rising compliance requirements. According to the Food and Agriculture Organization (FAO), approximately 14% of food produced globally is lost between harvest and retail stages each year. Food businesses are increasingly expected to reduce these losses while simultaneously investing in stronger safety and monitoring infrastructure. For many operators, balancing production efficiency with sensor-related spending remains difficult.

Compliance Burden and Operational Complexity Create Adoption Gaps Across Food Facilities

Government-led food safety initiatives continue encouraging stronger monitoring practices, but implementation remains uneven because advanced sensing systems require ongoing operational commitment. Chemical sensors must be regularly validated, tested, and integrated into existing production environments, creating additional cost and time requirements for manufacturers. These challenges become more noticeable in regions where food processing businesses operate with limited technical resources.

Opportunity

Expanding Use of Chemical Sensors in Smart Food Monitoring Creates Strong Growth Opportunity

One of the major growth opportunities for the chemical sensors market is the increasing use of smart monitoring technologies across the food industry. Food manufacturers are moving toward real-time quality control systems to improve product safety, reduce waste, and strengthen supply chain transparency. Chemical sensors are becoming an important part of this transition because they can detect gas composition changes, spoilage indicators, contamination levels, and storage conditions throughout production and distribution.

This opportunity is becoming more significant as global food demand continues to rise. According to the Food and Agriculture Organization (FAO), the world will need to produce around 60% more food by 2050 to feed a growing population. Meeting this demand while maintaining food quality is pushing food companies to adopt advanced monitoring solutions. Chemical sensors support this shift by helping facilities monitor freshness and processing conditions continuously rather than relying only on periodic testing.

Government Food Safety Programs and Waste Reduction Targets Supporting Market Expansion

Government initiatives focused on food security and waste reduction are creating favorable conditions for chemical sensor adoption. Many countries are encouraging digital food monitoring practices to improve food safety outcomes and reduce losses across the value chain. Chemical sensors align with these objectives by providing faster detection and helping operators take corrective action before products become unusable.

According to the United Nations Environment Programme (UNEP), global food waste reached approximately 1.05 billion tonnes in 2022, representing nearly 19% of food available to consumers. Reducing this level of waste has become a priority across public and private sectors. In parallel, food safety agencies continue encouraging preventive monitoring approaches to strengthen consumer protection. Chemical sensing solutions offer measurable support by improving environmental monitoring, shelf-life management, and contamination control.

Regional Insights

North America dominated the Chemical Sensors Market with a 41.70% share, accounting for USD 9.9 Billion due to strong industrial adoption and advanced monitoring infrastructure.

In 2025, North America held a dominant position in the global Chemical Sensors Market, capturing 41.70% of the total market and reaching a value of USD 9.9 Billion. The region’s leadership was supported by the widespread deployment of chemical sensing technologies across industrial manufacturing, oil and gas operations, healthcare facilities, environmental monitoring systems, and food processing industries.

The United States remained the largest contributor within the region due to extensive investments in industrial automation, smart manufacturing systems, and environmental compliance technologies. Chemical sensors continued to see strong demand across process industries where real-time monitoring and preventive maintenance became increasingly important for operational efficiency.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Siemens AG continues to maintain a strong presence in the chemical sensors market through its broad industrial automation and digital sensing portfolio. The company generated approximately €77.8 billion in revenue in fiscal 2025 and continued expanding its industrial monitoring capabilities across manufacturing, energy, and process industries. Siemens supports chemical sensing applications through integrated automation platforms, environmental monitoring systems, and smart factory technologies.

Thermo Fisher Scientific Inc. remains an important participant in the chemical sensors market through analytical instruments, laboratory technologies, and chemical detection solutions. In 2025, the company reported annual revenue exceeding US$43 billion and maintained strong global operations serving industrial, healthcare, environmental, and food sectors. Its sensing and analytical technologies support chemical identification, quality assurance, and environmental monitoring applications.

ABB holds a significant position in the chemical sensors market through industrial automation, process measurement, and smart sensing technologies. In 2025, ABB generated annual revenue of approximately US$32 billion while continuing expansion across energy, manufacturing, utilities, and industrial automation sectors. The company provides sensor-enabled solutions for process efficiency, gas analysis, and operational monitoring. ABB operates in over 100 countries and continues focusing on digital industrial platforms, intelligent process control, and automation-driven industrial productivity improvements.

Top Key Players Outlook

- Siemens AG

- Thermo Fisher Scientific Inc.

- ABB

- Figaro Engineering

- MSA Safety Incorporated

- Teledyne Technologies Incorporated

- Emerson Electric Co.

- Honeywell International

- General Electric

- Smiths Detection Group Ltd

- Bosch Sensortec GmbH

Recent Industry Developments

In 2025, Bosch Sensortec also entered a strategic collaboration with Espressif to launch the ESP SensairShuttle platform, using Bosch sensors such as BME690 for environmental and IoT sensing applications. On the investment side, Bosch Group reported €91.0 billion sales revenue in 2025, with €7.9 billion spent on research and development. Bosch also stated that more than 50% of new smartphones use Bosch MEMS sensors, showing its strong sensor scale.

In 2025, Smiths Detection Group Ltd revenue of £963 million and headline operating profit of £122 million, while more than 50% of its sales came from aftermarket services. In new product development, Smiths Detection advanced chemical, explosives, narcotics, and toxic threat detection systems, including IONSCAN 600, which received G1 approval in 2025. For investment and expansion, the company announced a new assembly and manufacturing facility in Saudi Arabia with METCO in 2025, supporting local production under Vision 2030. In merger and acquisition activity, Smiths Group agreed in 2025 to sell Smiths Detection to CVC Capital Partners for £2.0 billion, with closing expected in the second half of 2026.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 23.9 Bn |

| Forecast Revenue (2035) | USD 28.6 Bn |

| CAGR (2026-2035) | 6.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Dissolved Oxygen Sensor, Carbon Dioxide Sensor, Carbon Monoxide Sensor, Hydrogen Sensor, Methane Sensor, Others), By Technology (Optical, Electrochemical, Catalytic Bead, Thermal, Others), By Particle Type (Solid, Liquid, Gas), By Application (Process Control, Emission Monitoring, Vehicle Safety System, Heating, Ventilation, and Air Conditioning (HVAC) System, Home Building Automation, Others), By End-use Industry ( Oil and Gas, Chemical, Pharmaceutical, Food and Beverage, Water and Wastewater, Healthcare, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Siemens AG, Thermo Fisher Scientific Inc., ABB, Figaro Engineering, MSA Safety Incorporated, Teledyne Technologies Incorporated, Emerson Electric Co., Honeywell International, General Electric, Smiths Detection Group Ltd, Bosch Sensortec GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |