Quick Navigation

Report Overview

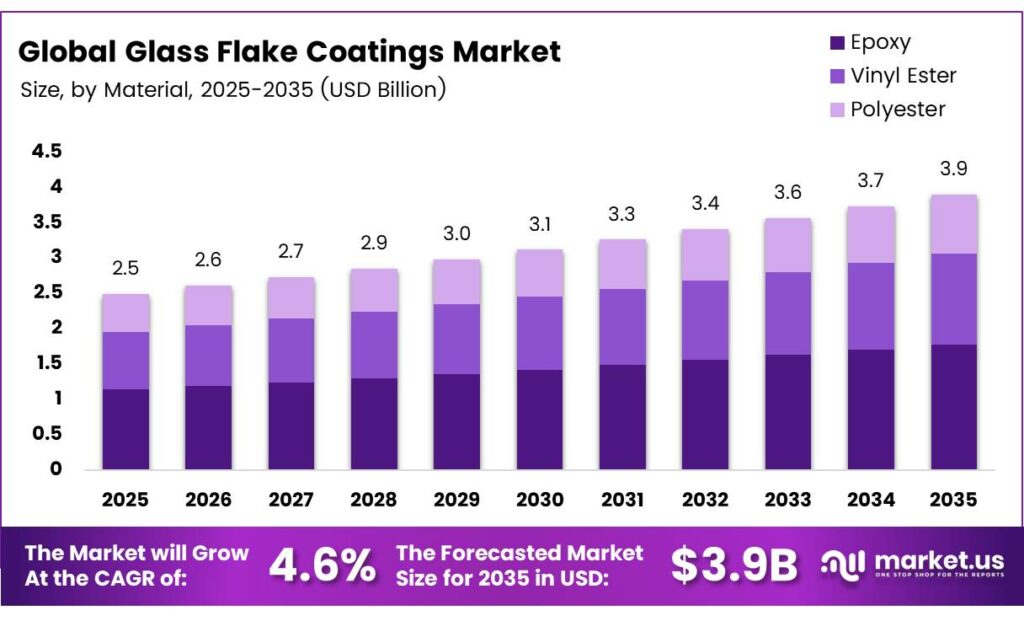

The Global Glass Flake Coatings Market size is expected to be worth around USD 3.9 billion by 2035 from USD 2.5 billion in 2025, growing at a CAGR of 4.6% during the forecast period 2026 to 2035.

Glass flake coatings are high-performance protective systems that use thin glass platelets as reinforcing pigments to create a layered barrier against moisture, chemicals, and corrosion. These coatings serve critical infrastructure in oil and gas, marine, chemical processing, and industrial sectors. Their unique platelet structure forces corrosive agents to travel a longer diffusion path, extending asset life significantly.

A 60 µm thick epoxy coating containing 0.75 wt% graphene nanoplatelets achieved anti-corrosion performance comparable to a 300 µm thick conventional glass-flake epoxy coating. This finding signals that next-generation formulations could redefine thickness specifications industry-wide, compressing material consumption while maintaining barrier performance — a development with direct cost implications for large-scale infrastructure projects.

Epoxy-based formulations dominate the material landscape, while vinyl ester and polyester alternatives compete in niche chemical-resistance applications. The material mix matters because each resin system carries a different margin profile — epoxy commands premium pricing due to proven performance, while polyester competes primarily on cost in lower-specification end markets.

Hempadur Multi-Strength 35840(100% volume solids) can cut CO₂ emissions by up to 26% versus standard 79% systems, while Hempaprime Strength 530 (90% volume solids) achieves up to 41% reduction, enabling lower-carbon offshore coating and maintenance.

Interzone 1000 has protected more than 4,000 offshore assets globally. This scale of deployment confirms that glass flake coatings are not a niche solution — they underpin critical offshore infrastructure at a volume that makes supply chain reliability and application consistency primary competitive differentiators.

Key Takeaways

- The Global Glass Flake Coatings Market is valued at USD 2.5 billion in 2025 and is projected to reach USD 3.9 billion by 2035, growing at a CAGR of 4.6% from 2026 to 2035.

- Epoxy leads with a 51.4% market share in 2025.

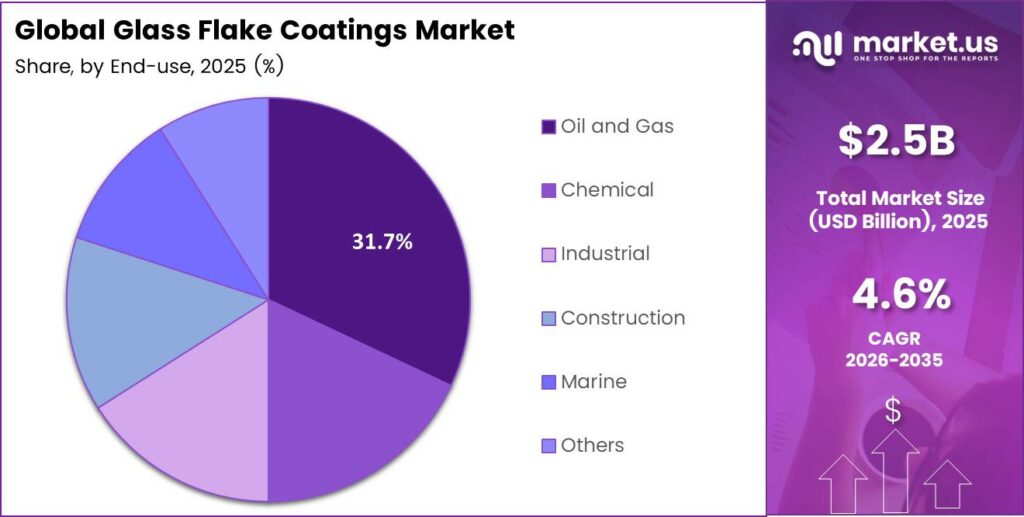

- Oil and Gas holds the largest share at 31.7% in 2025.

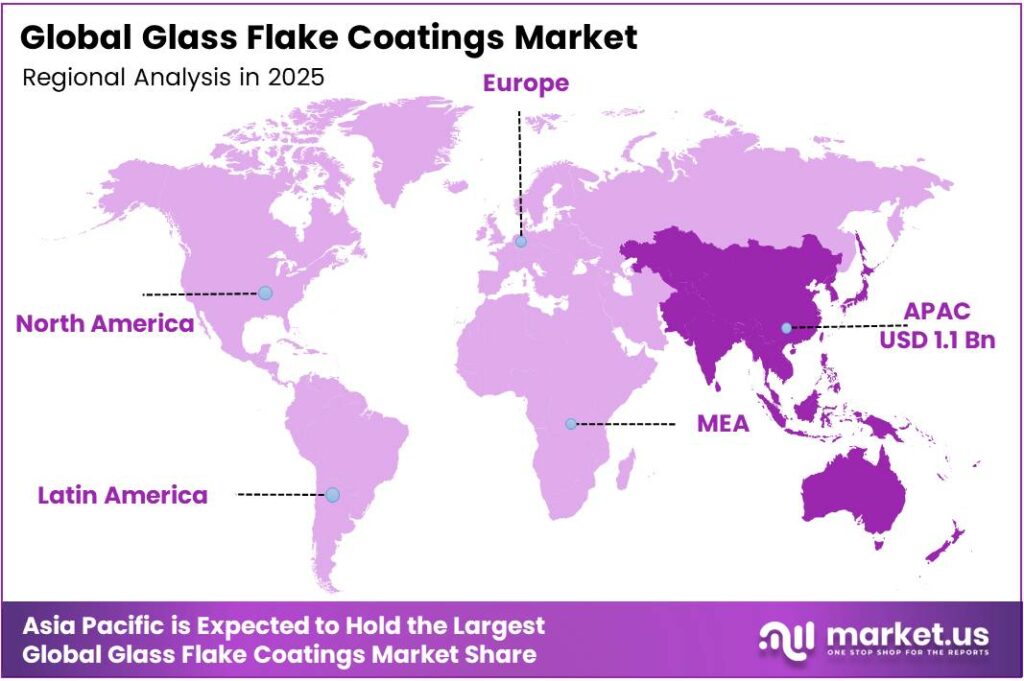

- Asia-Pacific dominates regionally with a 44.9% share, valued at approximately USD 1.1 billion.

Product Analysis

Epoxy dominates with 51.4% due to superior adhesion and proven offshore durability.

In 2025, Epoxy held a dominant market position in the By Material segment of the Glass Flake Coatings Market, with a 51.4% share. This lead reflects epoxy’s exceptional bonding strength, chemical resistance, and documented performance in offshore and industrial environments. Asset owners specify epoxy systems because they offer the most validated long-term performance data under aggressive corrosion conditions.

Vinyl Ester serves as the preferred choice in chemical processing plants where exposure to acids, solvents, and concentrated reagents exceeds epoxy’s tolerance range. Its higher resistance to chemical permeation makes it the logical specification in tank linings and scrubber systems. However, its higher cost and more complex application requirements limit adoption to environments where epoxy falls short.

Polyester competes primarily on cost in lower-specification applications, including general industrial maintenance and construction, where chemical exposure is moderate. Polyester glass flake systems offer acceptable corrosion resistance at a lower price point, making them accessible to budget-constrained operators. However, their performance ceiling is lower than epoxy, which restricts penetration into high-specification offshore and chemical sectors.

End-Use Analysis

Oil and Gas dominate with 31.7% due to extreme offshore corrosion protection requirements.

In 2025, Oil and Gas held a dominant market position in the By End-Use segment of the Glass Flake Coatings Market, with a 31.7% share. Offshore platforms, subsea pipelines, and storage tanks operate under continuous salt spray, hydrocarbon exposure, and pressure cycling — conditions that demand the highest-grade barrier coatings available.

Chemical processing facilities represent the second-most demanding end-use environment, where storage tanks, reactors, and pipe networks face exposure to concentrated acids, alkalis, and solvents. Glass flake coatings reduce permeation rates compared to conventional coatings, making them the protective solution of choice for facilities where coating failure triggers regulatory shutdowns and remediation costs far exceeding coating budgets.

Industrial applications cover a broad range of manufacturing and heavy processing environments, including power generation, mining, and metal processing. These buyers typically balance performance requirements against cost constraints, often specifying glass flake systems on high-value assets while using standard coatings elsewhere. This selectivity means industrial buyers represent a volume opportunity but lower per-unit specification intensity.

Key Market Segments

By Material

- Epoxy

- Vinyl Ester

- Polyester

By End-Use

- Oil and Gas

- Chemical

- Industrial

- Construction

- Marine

- Others

Emerging Trends

Hybrid Coating Systems and Nanotechnology Are Redefining Barrier Performance Standards

Formulators are combining glass flakes with advanced polymers to create hybrid coating systems that outperform either component alone. This shift reflects end-user pressure for coatings that deliver both mechanical toughness and chemical resistance in a single application. A 60 µm graphene-enhanced epoxy achieved barrier performance equivalent to a 300 µm conventional glass-flake coating — signaling that thinner, smarter formulations will increasingly challenge traditional thickness-based specifications.

Nanotechnology integration allows manufacturers to enhance barrier properties at the molecular level without increasing dry film thickness proportionally. This matters because thinner effective coatings reduce material weight, lower application time, and cut waste — advantages that resonate strongly in offshore wind and marine sectors where access logistics amplify every hour of application time.

Automated and spray-based application techniques are also gaining adoption, reducing dependence on skilled manual applicators in markets where labor availability constrains project schedules. This operational shift favors suppliers whose formulations are optimized for spray application, as compatibility with automated systems becomes a specification requirement alongside traditional performance metrics.

Drivers

Offshore Corrosion Demands and Oil and Gas Expansion Anchor Long-Term Glass Flake Coating Adoption

Offshore platforms, subsea pipelines, and marine infrastructure face a combination of salt spray, chemical immersion, and mechanical stress that conventional coatings cannot withstand across multi-decade asset lifespans. Offshore wind OPEX accounts for approximately 30% of the levelized cost of energy — meaning that coating systems directly influence project economics, not just maintenance budgets. This financial link elevates glass flake coatings from a material specification to a cost-management tool.

Chemical processing industries add a parallel demand driver: tanks, reactors, and pipework exposed to acids and solvents require coatings with superior permeation resistance. Furthermore, micronised glass-flake epoxy systems allow dry film thickness of up to 400 µm in a single brush coat, reducing the number of application passes and compressing labor costs on large-scale projects.

Expansion of oil and gas exploration activity — particularly in deepwater and harsh-environment regions — sustains demand for high-performance protective coatings on new assets. Each new offshore installation represents a long-duration coating contract spanning initial application through scheduled inspection and maintenance cycles. This recurring revenue structure makes oil and gas the most commercially attractive end-use segment for glass flake coating suppliers.

Restraints

High Application Costs and Environmental Regulations Constrain Market Penetration Beyond Core Industrial Sectors

Glass flake coatings require skilled applicators trained in surface preparation, mixing ratios, and film thickness measurement — competencies that command premium labor rates. The C-90 series technical specification, for example, mandates that glass flake content constitute 20–30% of the finished product and requires mixing with the mating part within 30 minutes — a pot-life constraint that increases application complexity and reduces tolerance for error on-site.

Hempel’s cost-cutting coating decision in an Irish Sea offshore wind project generated a 15% annual increase in touch-up costs — illustrating that underspecification is financially punishing. However, the same data point reveals the core commercial barrier: asset owners initially resist the higher upfront cost of premium glass flake systems, even when lifecycle economics favor them.

Stringent environmental regulations on volatile organic compounds and hazardous coating ingredients add formulation complexity and compliance cost for manufacturers. Regulatory constraints vary by jurisdiction, requiring suppliers to maintain multiple product variants for different markets. This compliance burden raises operating costs and creates uneven market access — particularly for smaller regional suppliers unable to fund multi-jurisdiction certification programs.

Growth Factors

Renewable Energy Infrastructure and Low-VOC Innovation Open New Revenue Channels for Glass Flake Coatings

Offshore wind foundations, tower structures, and transition pieces face the same aggressive corrosion environment as oil and gas platforms — creating a natural extension market for glass flake coating suppliers. Wind Systems Magazine confirms that Horns Rev 1’s coating showed no cracking, flaking, or rust after 20 years, validating glass flake systems for energy infrastructure. Each new offshore wind installation represents decades of protective coating revenue across initial application and maintenance cycles.

Rapid industrialization in developing economies — particularly across Asia-Pacific — is generating sustained demand for protective coatings on new factories, pipelines, storage terminals, and water treatment infrastructure. Hempadur Multi-Strength 35840 reduces VOC emissions by up to 93% versus a standard 79% volume-solids solution — an innovation that directly addresses the environmental compliance requirements now embedded in infrastructure procurement criteria across regulated markets.

Water and wastewater treatment facilities represent an underutilized but structurally attractive growth segment. Municipal and industrial water treatment assets operate in continuous chemical and moisture exposure — conditions where glass flake coatings deliver measurable extension of asset service life. As aging water infrastructure requires rehabilitation globally, glass flake systems offer operators a verifiable alternative to frequent recoating or structural replacement.

Regional Analysis

Asia-Pacific Dominates the Glass Flake Coatings Market with a Market Share of 44.9%, Valued at USD 1.1 Billion

Asia-Pacific commands 44.9% of the global market, valued at approximately USD 1.1 billion in 2025. Rapid industrialization, large-scale petrochemical infrastructure expansion, and aggressive offshore energy development across China, South Korea, Japan, and India sustain this lead. The region’s combination of new-build volume and expanding regulatory standards for asset protection creates persistent demand for high-performance coating systems.

North America holds a structurally anchored position in the global market, underpinned by mature oil and gas infrastructure, strict environmental compliance mandates, and long-established coating specification frameworks. The US Gulf Coast offshore sector and chemical processing corridor drive consistent, high-value glass flake coating procurement. Additionally, replacement cycles on aging industrial assets generate sustained demand independent of new construction activity.

Europe combines legacy North Sea oil and gas infrastructure with a rapidly expanding offshore wind sector — two asset classes where glass flake coatings deliver measurable lifecycle performance advantages. The region’s rigorous environmental regulations also push suppliers toward low-VOC and high-solids formulations. Consequently, European procurement decisions increasingly reward technical differentiation over price, supporting premium product positioning.

Latin America presents a developing but structurally relevant market anchored by Brazil’s deepwater oil production platforms and Mexico’s onshore and offshore energy assets. Infrastructure investment in industrial processing, water treatment, and port facilities adds additional demand layers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Hempel A/S positions itself as a lifecycle-cost specialist rather than a product supplier — a distinction that resonates in offshore wind and oil and gas, where buyers now evaluate total cost of ownership across 25–30 year asset lifespans. Hempel’s offshore coating portfolio, backed by documented field data from Horns Rev 1 and North Sea deployments, gives the company a verifiable performance narrative that competitors without long-term inspection records cannot easily replicate.

PPG Industries, Inc. leverages its global manufacturing footprint and diversified coatings portfolio to compete across both high-specification offshore markets and volume-driven industrial segments. This dual-market positioning insulates PPG from sector-specific downturns, but it also means the company must balance R&D investment across multiple application contexts — a resource allocation challenge that specialist competitors do not face.

KCC Corporation draws a competitive advantage from its deep integration into South Korean shipbuilding and offshore fabrication supply chains — the world’s largest ship construction ecosystem. This structural access to major marine clients at the point of vessel commissioning gives KCC a specification advantage that geography-dependent competitors cannot replicate without equivalent industrial proximity.

Kansai Paint Co., Ltd. competes through strong technical relationships across the Asia-Pacific industrial and marine sectors, where its regional manufacturing and distribution capabilities reduce lead times compared to Western suppliers. Its presence across Japan, India, and Southeast Asia positions the company to capture demand from regional infrastructure expansion programs, particularly in petrochemical and water treatment facility construction.

Key Players

- Hempel A/S

- PPG Industries, Inc.

- KCC Corporation

- Kansai Paint Co., Ltd.

- Berger Paints India Limited

- The Sherwin-Williams Company

- Jotun A/S

- Deccan Mechanical and Chemical Industries Pvt. Ltd

Recent Developments

- In 2025, Hempel A/S Energy & Infrastructure sales were at EUR 775M, with infrastructure demand supported by passive fire protection, Neogard waterproofing, and Avantguard corrosion protection. Hempel also cites heavy-duty products for splash zones, bridge/jetty pilings, and corrosive environments.

- In 2025, PPG will have direct glass-flake products: SIGMASHIELD 460 and SIGMASHIELD 950 are glass-flake epoxy coatings for abrasion, corrosion, splash/tidal, and heavy-duty service. PPG reported protective & marine coatings as a growth driver; it also launched broader protective-coatings solutions for data centers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.5 Billion |

| Forecast Revenue (2035) | USD 3.9 Billion |

| CAGR (2026-2035) | 4.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Epoxy, Vinyl Ester, Polyester), By End-Use (Oil and Gas, Chemical, Industrial, Construction, Marine, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Hempel A/S, PPG Industries, Inc., KCC Corporation, Kansai Paint Co., Ltd., Berger Paints India Limited, The Sherwin-Williams Company, Jotun A/S, Deccan Mechanical and Chemical Industries Pvt. Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |