Quick Navigation

Report Overview

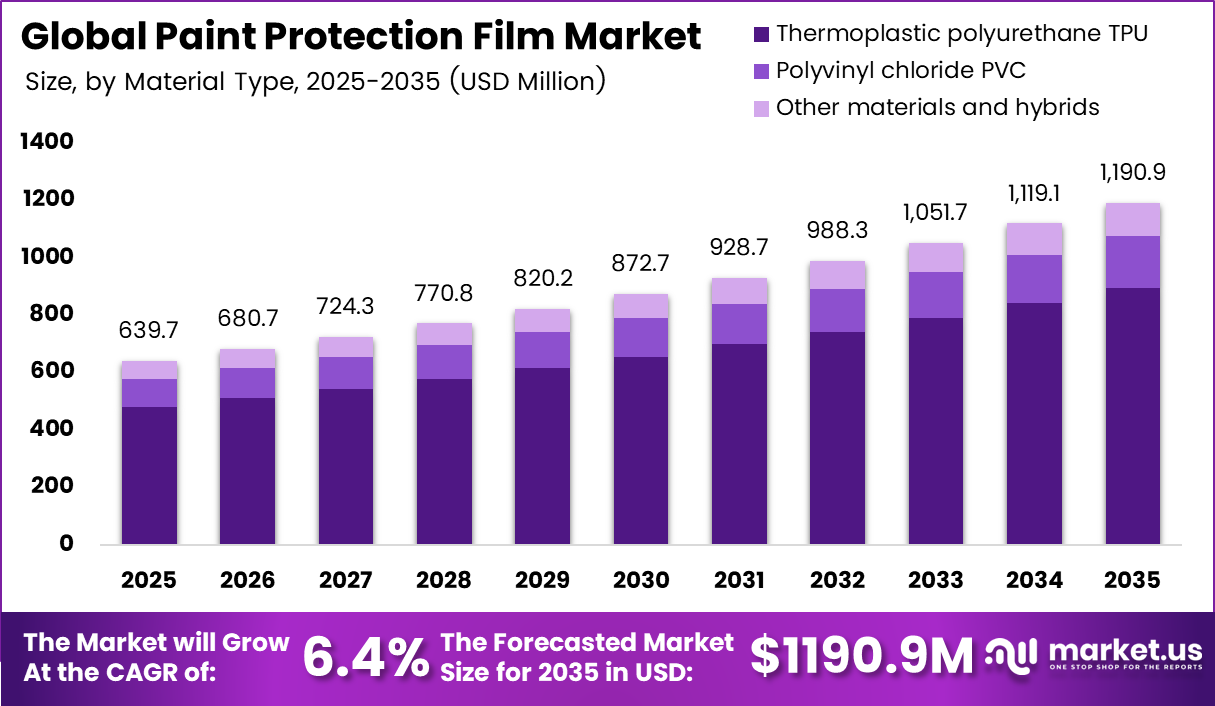

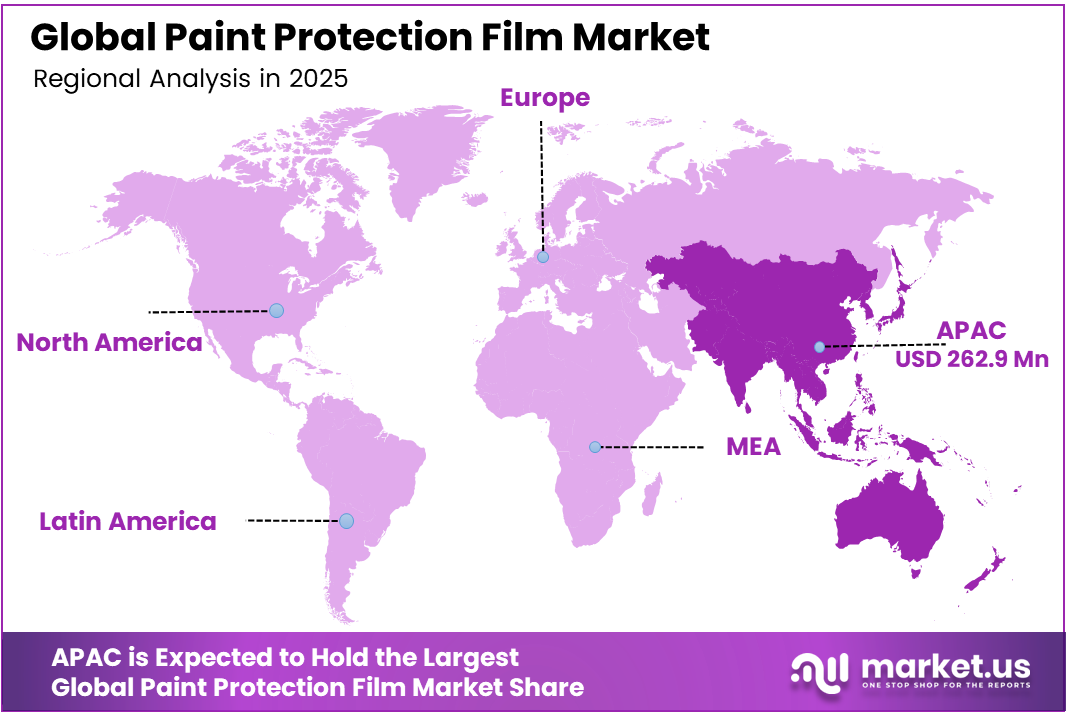

The Global Paint Protection Film Market was valued at USD 639.7 million, and between 2026 and 2035, this market is estimated to register a CAGR of 6.4%, reaching about USD 1,190.9 million by 2035. Asia Pacific held a dominant Market position, capturing more than a 41.4% share, holding USD 262.9 million in revenue.

The global paint protection film market is rapidly growing in the automotive aftermarket, offering transparent coatings that protect surfaces from scratches, UV radiation, and environmental damage while preserving appearance. Market growth is driven by consumer preference for premium vehicle aesthetics, awareness of long-term maintenance, and demand for advanced surface protection solutions.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production exceeded 93 million units in 2023, reflecting strong automotive manufacturing activity and increasing demand for vehicle protection and customization solutions worldwide. The development of self-repairing coating technology, hydrophobic qualities, and good film quality has made the product more acceptable globally.

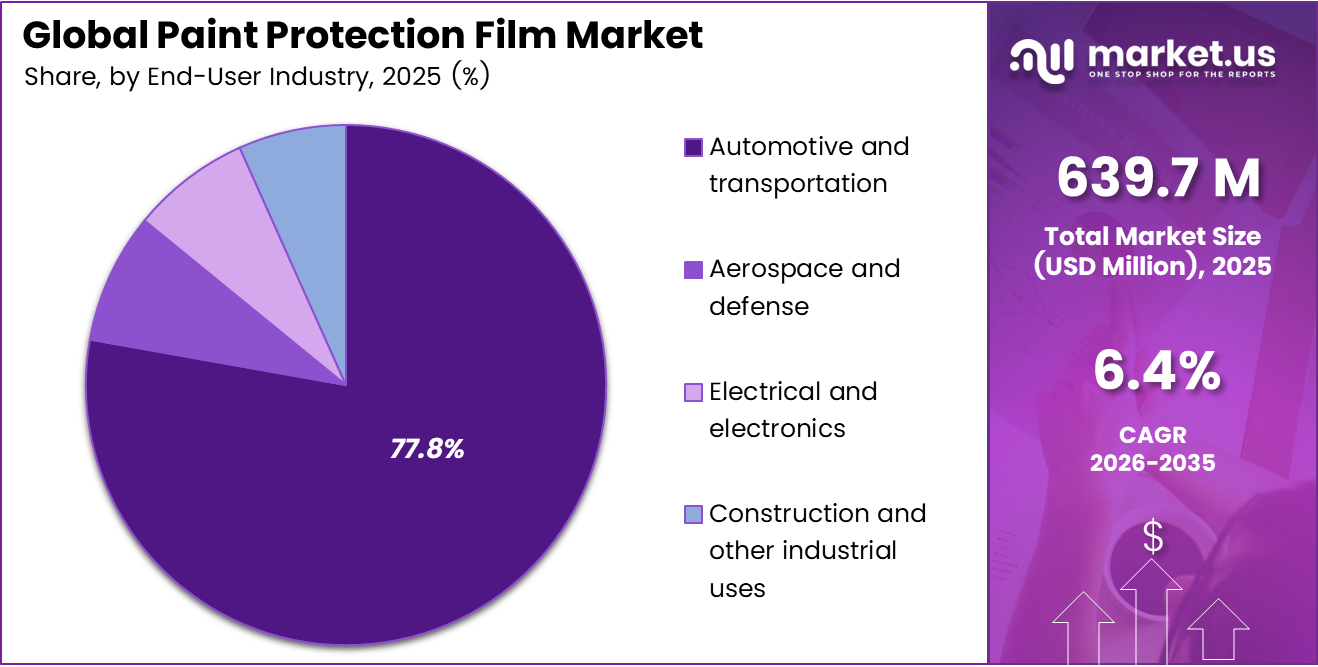

The automotive and transportation sector constitutes 77.8% of the paint protection films market in 2025, driven by increased vehicle production and demand for aesthetic solutions. Asia Pacific leads globally with a 41.1% share, fueled by automotive manufacturing growth and rising vehicle ownership in China, India, Japan, and South Korea.

However, high installation costs, dependence on skilled labor for proper application, and availability of lower-cost alternative coatings may restrain market growth to a certain extent. Despite these challenges, increasing adoption of premium vehicles, expansion of automotive detailing services, and continuous advancements in protective film technologies are expected to create significant long-term growth opportunities within the global paint protection film market.

Key Takeaways

- The global paint protection film market was valued at approximately USD 639.7 million in 2025.

- The global paint protection film market is projected to grow at a CAGR of 6.4% and is estimated to reach nearly USD 1,190.9 million by 2035.

- On the basis of material, Thermoplastic Polyurethane (TPU) dominated the market, constituting 75.1% of the total market share.

- Based on finish, Gloss Finish Films dominated the paint protection film market, accounting for around 60.1% of the total market share.

- Based on application area, Partial Wraps (hood, fender, bumper) led the market, comprising 40.6% of the total market share.

- Among the end-user industries, the Automotive and Transportation segment held a major share in the paint protection film market, accounting for 77.8% of the market share.

- In 2025, Asia Pacific was the most dominant region in the paint protection film market, accounting for 41.1% of the total global market share.

Material Type Analysis

Thermoplastic Polyurethane (TPU) Dominated the Paint Protection Film Market.

The TPU segment held the maximum share of the overall global market at 75.1%, owing to high strength, flexibility, transparency, and self-healing capabilities. The films made from TPU are used widely in various automotive applications because of their better protective performance against scratches, stone chip resistance, UV protection, and environmental protection while retaining the aesthetic appearance of the surfaces.

Growing demand for luxury cars and detailing services, coupled with increased emphasis on surface protection, is propelling the usage of such films across the globe. The Polyvinyl Chloride (PVC) segment accounted for approximately 15.2% of the market share owing to its cost-effectiveness and widespread use in budget-friendly protective film applications.

Meanwhile, the Other Materials and Hybrids segment represented around 9.7% of the total market share due to increasing development of multilayer and customized protective film technologies designed for specialized industrial and non-automotive applications.

Finish Analysis

Gloss Finish Films Led the Paint Protection Film Market.

Gloss finish films were the most prevalent segment in the global market for paint protection films since it accounted for 60.1% of the overall market share owing to the rising trend among consumers of enhancing the aesthetics of their vehicles.

Increased demand for luxury and premium cars, together with auto detailing services, has driven the growth of this segment in the global market. The Matt or Satin Finish Films segment accounted for approximately 30.2% of the market share owing to increasing popularity of customized vehicle appearances and premium matte aesthetic preferences among automotive enthusiasts.

Meanwhile, the Other Textured or Colored Finishes segment represented around 9.7% of the total market share due to growing demand for specialized surface customization solutions and decorative protective film applications across automotive and industrial sectors.

Application Area Analysis

Partial Wraps (Hood, Fender, Bumper) Led the Paint Protection Film Industry.

Partial Wraps held the majority market share of 40.6% in the global paint protection film market because the parts of the automobile like the hood, bumper, fender, and side mirrors were vulnerable to scratching, stone chips, dirt, and other external damages.

Consumers are now turning toward partial wraps because it is a viable option for protecting the surface of their car with additional durability and no need for full body wrapping, while still keeping the appearance of the car intact.

The Full Body Wraps category captured a market share of about 31.4% on account of rising needs for comprehensive exterior surface protection on luxury vehicles, sports vehicles, and electric cars. The Specific Panels and Non-automotive Surface Protection categories together captured a market share of about 28.0% on account of the increased usage of paint protection films on aircraft, electronics, machinery, and other products that require specific protection of their surfaces.

End-User Industry Analysis

The Paint Protection Film Market Was Dominated by Automotive and Transportation.

The Automotive & Transportation vertical captured the highest market share of 77.8%, owing to the rising manufacturing of automobiles, rising demand for luxurious appearances on vehicles, and the increased adoption of protection solutions for automobiles.

These protective films are widely used for various types of automobiles such as passenger cars, luxury cars, sports cars, and even electric cars to prevent damage to their body from any external environmental factors or elements. Consumer expenditure on automotive detail work, paint protection services, and customization services is driving the growth of the Automotive vertical.

Aerospace and Defense, Electrical and Electronics, and Construction and Other Industrial Applications segments together held an approximate 22.2% market share owing to rising usage of protective films on aerospace exteriors, electronic displays, machinery, and industrial structures that require additional surface resistance and protection from the environment.

Key Market Segments

By Material

- Thermoplastic polyurethane TPU

- Polyvinyl chloride PVC

- Other materials and hybrids

By Finish

- Gloss finish films

- Matt or satin finish films

- Other textured or colored finishes

By Application Area

- Full body wraps

- Partial wraps

- Specific panels

- Non-automotive surface protection

By End-user Industry

- Automotive and transportation

- Aerospace and defense

- Electrical and electronics

- Construction and other industrial uses

Market Dynamics

Opportunity

Despite being a well-established aftermarket solution, paint protection film has achieved less than 5% penetration across global OEM factory-fit and authorized-dealership pre-delivery channels. This leaves an estimated untapped annual opportunity of USD 280–320 million in 2026. The main barrier is commercial rather than technical, as vehicle manufacturers and dealers have traditionally prioritized easier-to-install accessories such as floor mats, window tints, and alloy upgrades.

However, rising electric and luxury vehicle prices are changing this approach. For a vehicle valued above USD 45,000, a pre-installed PPF package costing around 3–5% of the purchase price, or USD 1,350–2,250 per unit, can be added during the sales process with limited customer resistance. Post-purchase offers, by comparison, can experience conversion declines of 35–45%.

Preferred-supplier agreements with automakers and dealer groups could also help PPF companies build recurring B2B revenue while lowering customer acquisition costs by 12–18%. India offers strong potential, as new passenger vehicle sales exceeded 4.2 million units in 2025. Dealership integration could improve national installer revenue productivity by 8–11 percentage points within three years. However, large-scale adoption will require certified installers, aligned warranties, and vehicle-specific film templates, making this a future opportunity rather than an established market driver.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| OEM & Dealership Pre-Delivery Integration | +1.8% | North America, Germany, India | Medium term (2–4 years) |

| Non-Automotive Adjacent Vertical Expansion (Marine, Aerospace, E&E) | +2.2% | APAC, North America, EU | Long term (≥ 4 years) |

| Subscription & Warranty-as-a-Service Monetization | +1.5% | North America, GCC, India | Medium term (2–4 years) |

| EV Platform-Specific PPF Engineering | +1.9% | North America, EU, APAC (China, South Korea) | Medium term (2–4 years) |

| M&A Roll-Up of Regional Installer Networks | +1.3% | India, Southeast Asia, GCC, Latin America | Short term (≤ 2 years) |

| Architectural & Industrial Surface Protection Pivot | +1.6% | EU, North America, APAC | Long term (≥ 4 years) |

Drivers

The luxury and premium vehicle category has expanded by approximately 6–8% annually since 2022, compared with overall new vehicle sales growth of only 2–3%. This trend directly supports PPF demand because premium vehicle owners record installation rates of 25–40%, while mass-market vehicle owners show adoption of only 3–7%. Luxury and near-luxury brands account for an estimated 17–19% of new registrations in North America but generate nearly 45–55% of regional PPF installation revenue.

Average revenue per installation reaches USD 2,200–3,500 in the luxury category, compared with USD 600–950 for mainstream vehicles. In China and other Asia-Pacific markets, premium ownership is closely linked with status and appearance, helping PPF demand grow around 2.2–2.8 percentage points faster than the wider automotive sector.

The increasing use of matte, satin, and multi-layer metallic finishes is also strengthening demand. Repainting these specialized surfaces can cost USD 8,000–18,000 per panel, making protective film a practical financial safeguard. As a result, premium installers can charge USD 3,000–5,500 for full-vehicle coverage without causing a major decline in customer demand.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Premium & Luxury Vehicle Penetration | +1.9% | North America, EU, APAC | Short term (≤ 2 years) |

| Self-Healing & Advanced TPU Technology Adoption | +1.5% | Global — North America, EU lead | Medium term (2–4 years) |

| Growing Consumer Awareness & Digital Influence | +1.3% | India, GCC, Southeast Asia, LATAM | Short term (≤ 2 years) |

| Expansion of Automotive Aftermarket Services | +1.1% | APAC, North America, EU | Medium term (2–4 years) |

| India’s Anti-Dumping Duty on Chinese TPU PPF | +0.9% | India (immediate); APAC spill-over | Short term (≤ 2 years) |

| EV & Luxury Fleet Resale Value Consciousness | +1.4% | North America, EU, China | Medium term (2–4 years) |

Restraints

High product and installation costs remain the most important demand-side restraint for the PPF industry. Premium film pricing makes the service unaffordable for an estimated 65–75% of new vehicle buyers in cost-sensitive markets. In India, full-vehicle installation can range from INR 20,000 to INR 250,000 depending on the vehicle, film brand, and coverage area. For mid-range models priced between INR 12 lakh and INR 18 lakh, this represents roughly 1.5–18% of the total on-road cost.

The same affordability challenge exists in developed markets. A professional TPU full wrap costing USD 2,500–5,000 on a USD 50,000 SUV adds a significant expense that competes with warranties, maintenance plans, and other vehicle upgrades. The cost structure also limits discounting, as film materials account for around 35–50% of installer revenue and skilled labor contributes another 25–35%.

This generally leaves gross margins of only 20–30%. Partial packages covering the bumper, hood, and fenders are available for USD 600–1,200, but they produce 40–55% lower customer lifetime value than complete wraps, reducing revenue generated from each buyer.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Installation Cost & Consumer Price Sensitivity | -1.8% | India, Southeast Asia, LATAM, Eastern Europe | Short term (≤ 2 years) |

| Competition from Ceramic Coatings & Alternative Protectants | -1.2% | Global — APAC, India highest risk | Short term (≤ 2 years) |

| TPU Raw Material Price Volatility & Supply Constraints | -1.5% | APAC manufacturing corridor, EU | Medium term (2–4 years) |

| Low Consumer Awareness in Emerging & Tier-2 Markets | -1.0% | India Tier-2/3, SEA, Africa, LATAM | Medium term (2–4 years) |

| Import Tariffs & Trade Protectionism (Anti-Dumping Measures) | -0.8% | India (post-June 2026), GCC, LATAM | Short term (≤ 2 years) |

| Counterfeit & Low-Quality Film Proliferation | -0.7% | APAC, GCC, LATAM | Medium term (2–4 years) |

Challenges

A shortage of skilled technicians is creating a serious supply-side limit on PPF market expansion. Initial practical training generally requires 7–15 days, followed by 6–18 months of supervised work before an installer can consistently deliver bubble-free applications, hidden seams, and accurate film alignment. Current training systems are estimated to produce only 8,000–12,000 qualified installers worldwide each year.

Projected market volumes could require approximately 25,000–35,000 new technicians annually by 2028, indicating a substantial workforce gap. In India, training facilities remain concentrated in major cities such as Mumbai, Delhi, Bengaluru, and Hyderabad, leaving smaller urban markets underserved. In the United States and Canada, experienced installers typically earn USD 18–28 per hour.

Even so, physically demanding working conditions, limited career progression, and strict quality expectations contribute to annual employee turnover that can approach 30% at mid-sized workshops. Replacing a trained worker can cost USD 3,500–6,000 in recruitment and onboarding expenses. Technician shortages also reduce workshop productivity, with many facilities using only 60–75% of their theoretical capacity during peak periods. This creates a revenue-per-bay performance gap of up to 40% and prevents businesses from converting available demand into completed installations.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Skilled Installer Talent Deficit | -1.4% | Global — APAC, India, GCC most acute | Medium term (2–4 years) |

| Inconsistent Installation Quality Standards | -0.9% | India, Southeast Asia, LATAM, GCC | Medium term (2–4 years) |

| Geopolitical & Supply Chain Concentration Risk | -1.1% | APAC manufacturing base, EU importers | Long term (≥ 4 years) |

| Consumer Lifecycle Education & Retention Friction | -0.8% | Global — emerging markets dominant | Short term (≤ 2 years) |

| Environmental Regulatory Pressure on TPU/PVC Chemistry | -0.7% | EU primary, North America secondary | Long term (≥ 4 years) |

| Technology Commoditization & Margin Compression | -1.0% | Global — APAC pricing pressure epicenter | Medium term (2–4 years) |

Geopolitical Impact Analysis

Global Supply Chain Disruptions and Trade Tensions Impacting the Paint Protection Film Market.

Ongoing Geopolitical tensions, trade uncertainties, and supply chain disruptions are impacting the global paint protection film market, reliant on specialty polymers and petrochemicals. Conflicts like the Russia-Ukraine war have raised transportation costs, delayed raw material supply, and hindered manufacturing operations in the specialty films sector.

The paint protection film market is affected by global automotive production trends, especially in Asia Pacific, North America, and Europe. Trade tensions and supply chain disruptions impact vehicle production and aftermarket demand, while rising crude oil prices influence manufacturing costs for paint protection films.

According to the World Bank and the International Energy Agency (IEA, 2024), geopolitical instability and global energy market disruptions have significantly increased logistics, transportation, and petrochemical raw material costs across manufacturing industries in 2023–2024.

Governments are emphasizing domestic manufacturing and localized supply chains to decrease import reliance, boosting investments in regional automotive aftermarket and specialty film industries. However, environmental regulations, trade barriers, and sustainability requirements pose ongoing challenges for global manufacturers in the paint protection film market.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Paint Protection Film Market.

In 2025, Asia Pacific held 41.1% of the global paint protection film market share, driven by rapid automotive production, rising vehicle ownership, and demand for premium customization in countries like China, India, Japan, and South Korea. Increased disposable income, luxury and electric vehicle adoption, and high demand for detailing services contribute to growth, alongside strong manufacturing and specialty film production in the region.

The European and North American markets dominated the global market for paint protection films. This was due to factors such as high penetration of premium cars, strong aftermarkets, and increased awareness among consumers regarding maintenance. Increased use of electric vehicles, luxurious appearance, and investments in detail technologies have enhanced growth.

Latin America and the Middle East & Africa are emerging markets for paint protection films, driven by urbanization, rising vehicle sales, expanded aftermarket services, and increased awareness of vehicle surface protection.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Competitive analysis shows that the worldwide paint protection film industry is characterized by a somewhat fragmented competitive environment since it involves multiple local and foreign competitors who are competing on the basis of their product quality, technology, durability, distribution channels, and price.

Major players in the paint protection film industry have been concentrating more on self-healing abilities, hydrophobic coatings, stain resistance, and clarity of their films. There is a rise in the level of competition in the market because of growing needs for luxury automobile coating, electric vehicle modifications, and detailing services across the globe.

Firms are increasingly working toward building their certified installer network and distribution network alliances and adopting technological innovations in films that offer superior protection against scratches, self-healing ability, and UV protection. Moreover, the emphasis on sustainability and use of recyclable coatings and environmentally friendly methods is anticipated to influence the competitive landscape of the paint protection film market.

Key Development

- In February 2025, XPEL Inc. expanded its global paint protection film distribution and installer network to strengthen its presence across emerging automotive aftermarket markets and increase electric vehicle protection applications.

- In September 2024, Eastman Chemical Company enhanced its advanced paint protection film portfolio under the LLumar and SunTek brands with improved self-healing and hydrophobic coating technologies for premium automotive applications.

- In June 2024, Garware Hi Tech Films Limited expanded production capacity for specialty and paint protection films to meet rising global demand for automotive surface protection and aftermarket customization solutions.

The Following are some of the Major Players in the Industry

- 3M Company

- XPEL Inc

- Eastman Chemical Company

- Avery Dennison Corporation

- Saint-Gobain SA

- Schweitzer Mauduit International Inc

- HEXIS SA

- GRAFITYP Selfadhesive Products NV

- PremiumShield Limited

- STEK Automotive

- BOP PPF China

- Garware Hi Tech Films Limited

- UPPF Ultimate Paint Protection Film

- Kavaca PPF NanoShine Ltd brand

- GSWF Global window and film brand

- Other companies

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 639.7 Mn |

| Forecast Revenue (2035) | USD 1190.9 Mn |

| CAGR (2026-2035) | 6.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Thermoplastic Polyurethane (TPU), Polyvinyl Chloride (PVC), and Other Materials & Hybrids), By Finish (Gloss Finish Films, Matt or Satin Finish Films, and Other Textured or Colored Finishes), By Application Area (Full Body Wraps, Partial Wraps Hood Fender Bumper, Specific Panels, and Non-automotive Surface Protection), By End-user Industry (Automotive and Transportation, Aerospace and Defense, Electrical and Electronics, and Construction & Other Industrial Uses) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | 3M Company, XPEL Inc, Eastman Chemical Company, Avery Dennison Corporation, Saint-Gobain SA, Schweitzer Mauduit International Inc, HEXIS SA, GRAFITYP Selfadhesive Products NV, PremiumShield Limited, STEK Automotive, BOP PPF China, Garware Hi Tech Films Limited, UPPF Ultimate Paint Protection Film, Kavaca PPF NanoShine Ltd brand, GSWF Global window and film brand, Other companies |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |