Quick Navigation

Report Overview

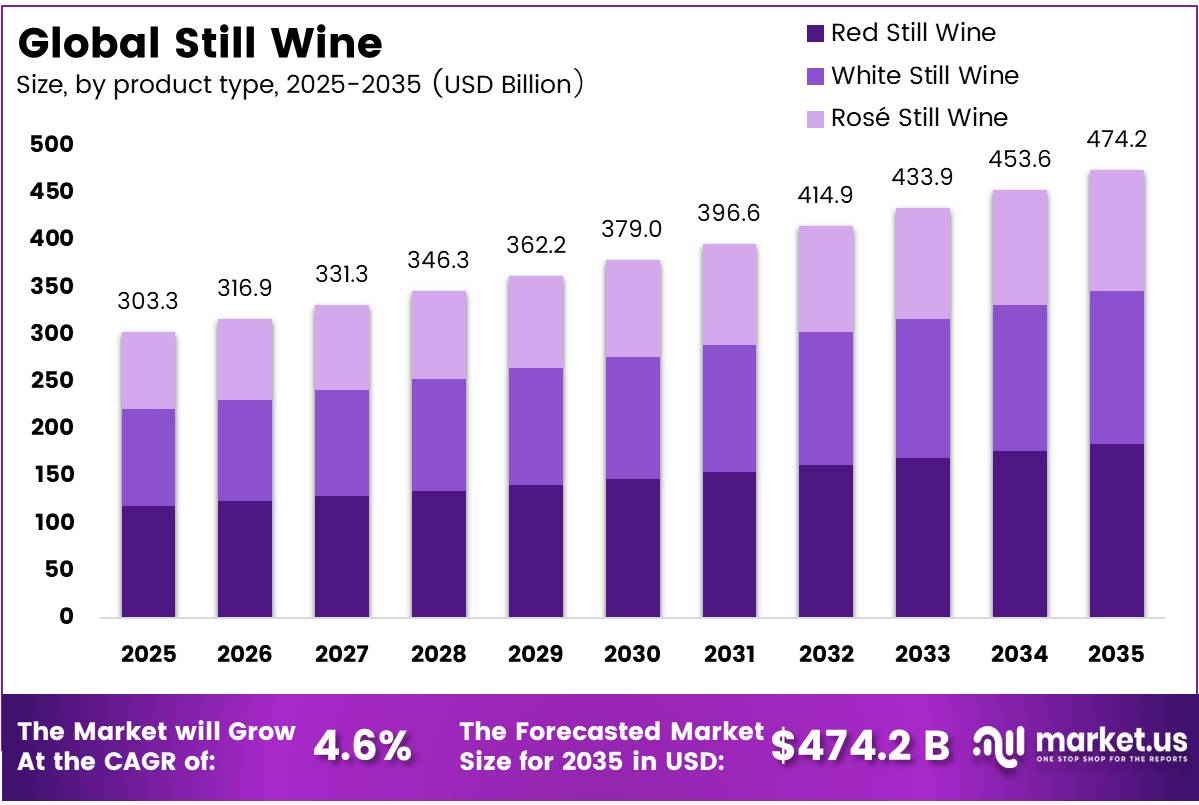

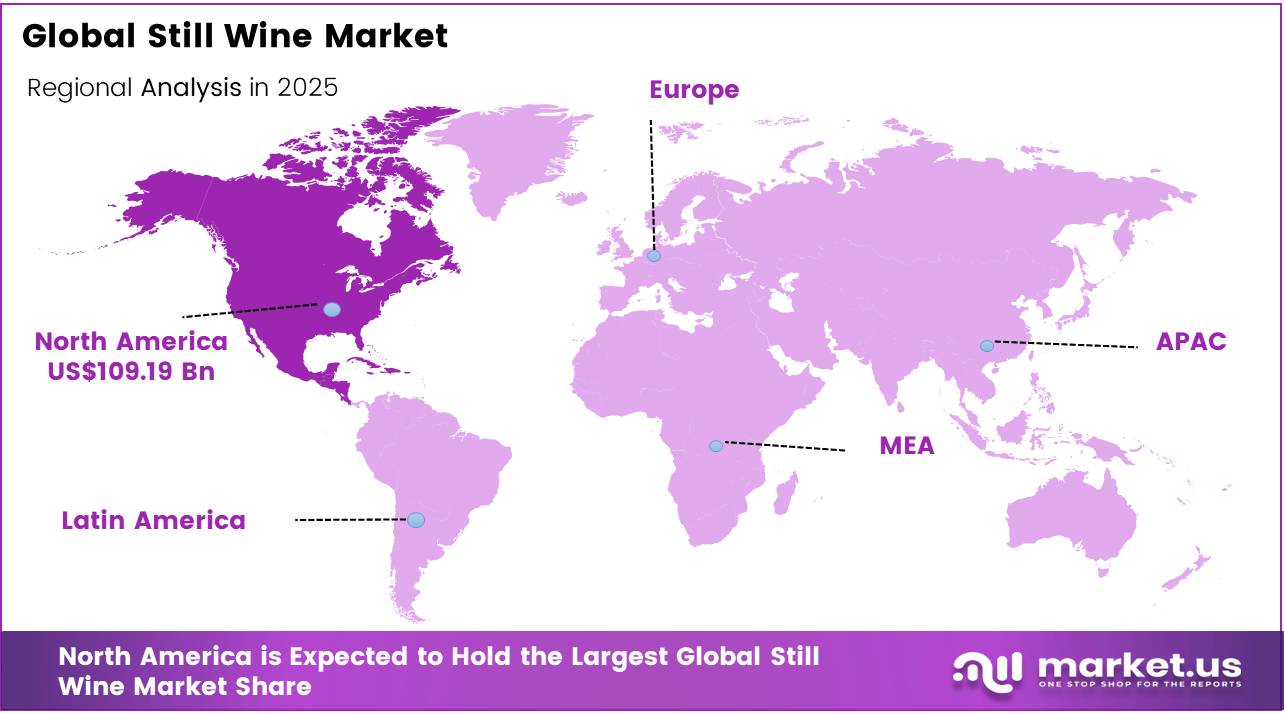

In 2025, the Global Still Wine Market was valued at USD 303.3 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 4.6%, reaching about USD 474.2 billion by 2035. In 2025, North America held a dominant market position, capturing more than a 36% share, holding USD 109.19 Billion revenue.

The Still Wines market is the largest among all wine markets around the globe, forming the base of wine trade and consumption and the cultivation of grapes. The demand is greatly influenced by changing tastes, economic capacity, and drinking behavior across generations due to changes in lifestyle and health consciousness. Even now, wines continue to form the bulk of international wine trading, and product quality, provenance, and pricing determine success in the market place.

- According to the International Organization of Vine and Wine (OIV), the total global wine consumption was reduced to the level of 214 million hectolitres in 2024, which is 3.3% less than in 2023, marking the lowest point for the past 60 years. The output decreased to the level of 225.8 million hectolitres, while exports stayed constant at 99.8 million hectolitres, with their value being increased to the amount of 36 billion EUR at the record-high price of 3.60 EUR per litre.

Key Takeaways

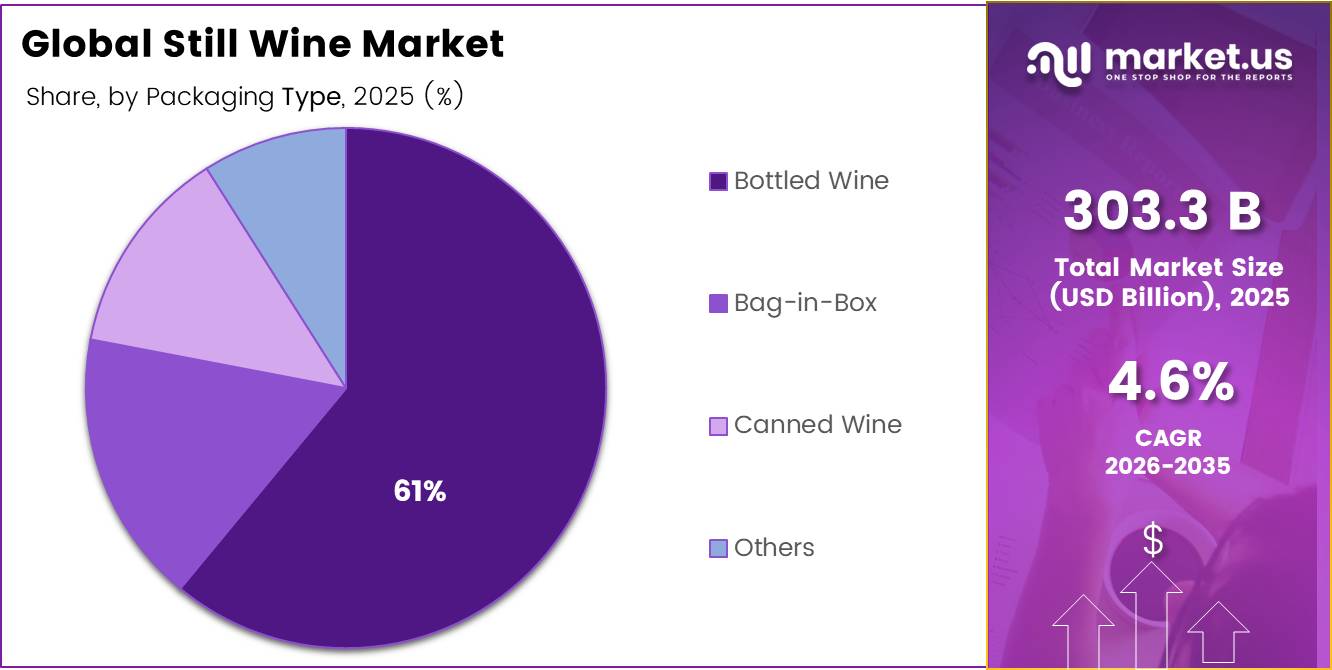

- The global still wine market was valued at USD 303.3 billion in 2025.

- The global still wine market is projected to grow at a CAGR of 4.6% and is estimated to reach USD 474.2 billion by 2035.

- On the basis of product type, Red still wine dominated the market, constituting 39% of the total market share.

- Based on the Packaging type, the Bottled Wine dominated the still wine market, with a substantial market share of around 61%.

- Based on the Distribution Channel, Liquor Store led the market, comprising 32% of the total market.

- Among the Price Category, the economy wine held a major share in the still wine market, 41% of the market share.

- Among the End user, the Household Consumption is the most considerable within the market, accounting for around 64% of the revenue.

- In 2025, the North America was the most dominant region in the still wine market, accounting for 36% of the total global consumption.

During 2025, global wine production stayed on the record-low level of 227 million hectolitres, while wine consumption decreased still further to the level of 208 million hectolitres, decreasing by 2.7% as compared with 2024. Nine out of ten leading markets showed decreased volumes. In addition, global vineyards’ surface area decreased for the sixth consecutive year to 7.0 million hectares.

World wine exports reached a volume of 94.8 million hectolitres, down 4.7%, in 2025, while exports were worth 33.8 billion EUR, down 6.7%, due to decreased trade volume coupled with price adjustments as a result of increased trade uncertainties linked to US tariffs and reduced demand from importing countries. However, despite these challenges, the degree of internationalization of the wine industry was still very high in 2025, with close to half of all bottles consumed being consumed away from their place of production.

Still Wine Market Segmentation

Product Type Analysis

Red Still wine represents dominant Segment in the Market.

In 2025, red wine held a dominant market position, capturing more than a 39% share of the global still wine market. According to the OIV’s State of the World Wine Sector released in May 2026, Italy remained the leading wine producer in 2025, recording a 1% variation over 2024, while Australia posted a 9% increase and South Africa grew 16% all three being significant red wine producing nations underpinning global red wine supply.

Rosé wine is it the fastest-growing colour segment. The OIV confirms that France represents more than 1/3 of total global rosé consumption, with the United Kingdom, Germany, and the United States driving the majority of international demand growth for the segment.

Packaging Type Analysis

Bottled Wine a significant packaging type.

Bottled wine dominates the still wine packaging market with 61% in terms of volume. The dominance is justified by the product’s crucial position within both local demand and exports of the category. According to OIV, wine exports’ total value amounted to 35.9 billion EUR in 2024 with an historically high average export price of 3.60 EUR per litre, reflecting the ongoing premiumisation trend associated with the bottle packaging, which makes up the bulk of global wine exports.

In 2025, the volume of world wine exports decreased to 94.8 million hectolitres and exports’ total value fell to 33.8 billion EUR; however, internationalisation rate remained at the historical level with one out of two bottles being drunk abroad. Thus, bottled wine remains structurally significant within all world markets. Together, Italy, France and Spain constitute the cornerstone of the global production of bottled wine volumes and values.

Distribution Analysis

Liquor Store Are the Most Widely Used Distribution analysis.

Liquor stores account for the highest distribution channel for still wine, comprising 32% of the channel based on the specialty positioning, products assortment, and regulation regimes within the main markets. According to the Monthly Retail Trade Survey of the U.S. Census Bureau, retail sales through beer, wine, and liquor stores amounted to USD 5.9 billion on a seasonally adjusted basis in December 2025 and have remained the major retailing format for wine consumption off premises in the United States.

According to the Census Bureau reveal that retail sales through beer, wine, and liquor stores almost doubled from 2008 to 2024, amounting to USD 104.7 billion. This channel owes its success to the sustained growth pattern and the specialization of the retailing format for alcohol beverages.

- According to data published by the U.S. Census Bureau, e-commerce retail sales in the United States in 2024 reached USD 1,192.6 billion, recording an 8.1% increase compared to 2023, when e-commerce comprised 16.1% of total retail sales.

Price Category Analysis

Economy Wine Held a Major Share of the still wine Market.

Economy wines lead with a 41% share, owing to widespread availability, heavy volume consumption, and increased price sensitivity in the face of inflation in major countries. The OIV estimates that international export prices continue to be about 30% higher than before the pandemic and stand at a record high of 3.60 EUR per litre in 2024, a factor that has led to a deliberate reduction in demand for economy wines due to their affordability. In spite of the lower demand, total export revenue was at an all-time high of 36 billion EUR in 2024, owing to the focus on value rather than volumes.

Luxury wines constitute the fastest-growing pricing segment, supported by ongoing premiumisation trends. The OIV explains that there is an ongoing shift towards consuming less but paying more, resulting in higher prices per litre despite falling consumption volumes.

End Use Analysis

Still wines Are Mostly Utilized in Household.

Household consumption is the major segment in end user accounting for 64% due to the prevalence of strong household wine consumption behavior in key markets. Wine consumption in the world reached 214 million hectolitres according to the data provided by OIV in 2024, down 3.3% from 2023 with the US, being the leader in the world market for wine, experiencing an even bigger fall in consumption, falling 5.8% to 33.3 million hectolitres, since economic and health concerns limited purchases among households.

Europe, which consumes close to half of all consumed wine worldwide, had a fall in consumption of 2.8% in 2024. In 2025, global consumption dropped even further to 208 million hectolitres as nine out of ten leaders of world wine consumption had decreased consumption.

Commercial and hospitality is the fastest growing user segment. According to Statistics Canada sales in food services and drinking places in Canada in 2024 increased by 4.0% compared to 2023, amounting to CAD 96.5 billion in the year under discussion.

Key Market Segments

By Product Type

- Red Still Wine

- White Still Wine

- Rosé Still Wine

By Distribution Channel

- Bottled Wine

- Bag-in-Box

- Canned Wine

- Others

By Price category

- Economy Wine

- Mid-Range/Premium Wine

- Luxury Wine

By End user

- Household Consumption

- Commercial/Hospitality

Drivers

Premiumization in bottled still wine mix

Even with global wine demand contracting, value retention in still wine is being supported by a favorable mix shift toward higher-priced bottled products, which matters because bottled wine accounted for 51.1% of world wine trade volume but 66.4% of export value in 2025, with an average export price of 4.53 EUR/l despite weaker volumes.

Global export prices across all wine averaged 3.56 EUR/l in 2025, still about 24% above the pre-Covid period, showing that value capture remains structurally stronger than volume growth. In the U.S., the world’s largest wine market at 31.9 mhl in 2025, demand softened by 4.3%, yet trade commentary for 2026 points to flat volume but value growth of roughly 2% to 4% as consumers trade up and lower-price tiers weaken.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization in bottled still wine mix | 1.80% | North America core, Western Europe premium tiers, Japan, urban APAC | Short term (≤ 2 years) |

| Climate-led supply tightening and price uplift | 1.40% | EU producers, U.S. West Coast, Chile, South Africa, Australia | Medium term (2-4 years) |

| Route-to-market shift from volume retail to value-led on-trade and DTC | 1.10% | U.S., UK, EU metros, Australia | Short term (≤ 2 years) |

| No/low-alcohol still wine adjacency expanding category access | 0.90% | EU, UK, North America, developed APAC | Medium term (2-4 years) |

| Trade reconfiguration and tariff-driven sourcing diversification | 0.80% | U.S. import market, EU exporters, Portugal, Southern Cone spill-over | Short term (≤ 2 years) |

| EU labeling and digital compliance favoring scaled operators | 0.60% | EU core, imported wines into EU, export-focused wineries globally | Medium term (2-4 years) |

Restraints

Demand erosion

Persistent end-market demand erosion remains the key restraint for the wine sector as global wine consumption declined from 214 million hectolitres in 2024 to 208 million hectolitres in 2025, representing a 2.7% year-on-year decrease and the lowest level seen in decades. This reduced annual demand by approximately 6 million hectolitres, while nine of the ten largest wine-consuming countries recorded volume declines. The result is lower asset utilization across wineries and distribution channels, reducing achievable market CAGR by about 2.3 percentage points.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand erosion | -2.30% | North America core, Western Europe, developed APAC | Medium term (2-4 years) |

| Tariff friction | -1.70% | U.S. import market, EU exporters, UK spill-over | Short term (≤ 2 years) |

| Climate volatility | -1.50% | EU vineyards, U.S. West Coast, Chile, Australia, South Africa | Medium term (2-4 years) |

| Packaging inflation | -1.10% | EU, U.S., Latin America export corridors | Short term (≤ 2 years) |

| Label compliance | -0.80% | EU core, imported wines into EU, export-led wineries | Medium term (2-4 years) |

| Channel squeeze | -0.90% | U.S., UK, EU metros, urban APAC | Short term (≤ 2 years) |

Opportunity

Lightweight and alternative formats

Alternative packaging remains a future growth opportunity rather than a current market driver, as OIV data show bottled wine still dominates global trade while Bag-in-Box represents only 3.6% of volume and 2.0% of value. The largest opportunity exists in sustainability-focused and price-sensitive markets where formats such as lightweight glass, PET, paper bottles, canned still wine, and premium Bag-in-Box can reduce delivered logistics costs by approximately 15%–35% per litre, while lowering breakage and storage costs. Although consumer adoption is still developing, producers using occasion-based packaging strategies could unlock around 1.2 percentage points of additional CAGR, especially across the UK, Nordics, Canada, Australia, and urban Europe.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| No/low still wine scale-up | 2.10% | EU, UK, North America, Japan, Australia | Medium term (2-4 years) |

| India urban premium entry | 1.80% | India metros, travel retail Asia, GCC spill-over | Medium term (2-4 years) |

| DTC wine tourism monetization | 1.50% | U.S., Southern Europe, Australia, South Africa | Short term (≤ 2 years) |

| Lightweight and alternative formats | 1.20% | EU, UK, Nordics, Canada, Australia | Short term (≤ 2 years) |

| Portfolio roll-up of regional wineries | 1.40% | France, Spain, Italy, U.S., Chile | Medium term (2-4 years) |

| Brazil and Japan premium white-space | 1.00% | Brazil, Japan, selective APAC import hubs | Medium term (2-4 years) |

Challenge

Climate adaptation complexity

Climate adaptation remains a long-term challenge for the still wine sector as changing weather patterns continue to reduce yield stability and increase production costs. OIV reported global wine production at 227 million hectolitres in 2025, marking the third consecutive year below historical averages, while global vineyard area declined to 7.0 million hectares, down 0.8% year-on-year and recording the sixth straight annual decline. Producers across major wine regions are facing more frequent frost, drought, and heavy rainfall events, causing vineyard output swings of 20–40%. Rising investment in irrigation, crop protection, and vineyard renewal is increasing operating costs and reducing market growth potential by approximately 1.5 percentage points.

Challenges Impact Analysis

| Challenge | (~) % Potential CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Climate adaptation complexity | -1.50% | EU vineyards, U.S. West Coast, Chile, Australia, South Africa | Long term (≥ 4 years) |

| Volatile trade and logistics costs | -1.20% | U.S. import routes, EU export hubs, APAC corridors | Medium term (2-4 years) |

| Vineyard and cellar labour gaps | -1.00% | Southern Europe, U.S., Chile, South Africa, Australia | Long term (≥ 4 years) |

| Channel and SKU rationalization pressure | -0.90% | North America core, Western Europe, urban APAC | Medium term (2-4 years) |

| Compliance and data-management load | -0.80% | EU regulatory hubs, global exporters into EU | Medium term (2-4 years) |

| Capital discipline under uncertainty | -0.70% | Global mid-sized wineries and distributors | Medium term (2-4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Still wine Manufacturing.

The current trend among geopolitical and trade issues is causing an impact on global still wine production and export, especially in Europe, North America, and Asia Pacific. The International Organisation of Vine and Wine estimates total volume of international wine trade to be around 99.8 million hectolitres in 2024. However, the wine distribution networks faced considerable instability due to trade barriers, tariffs, and new trade relations. EU, which is responsible for more than 60% of total wine exports globally, is continuing to suffer from the impact caused by trade policy changes and new trade alliances.

The European Commission argues that agricultural export chains are becoming fragmented with an increased number of compliance issues related to sustainability standards, labeling, and geographic indications. Moreover, various national trade authorities report the diversification of wine trade routes towards emerging countries located in Asia and Latin America. The latter development is caused by geopolitical realignment of export flows. Geopolitical and structural shifts are increasing complexities within the still wine export and production logistics network, thus affecting the export plan for the period of 2026-2035.

Regional Analysis

North America Held the Largest Share of the Global Still wine Market.

North America is the largest regional market for still wine around the world, comprising 36.0% share based on high consumer spending power, developed distribution channels, and presence of premium and imported still wines. As per OIV statistics, United States alone is responsible for the consumption of approximately 33.3 million hectolitres of still wines in 2024, making it the largest consumer of wine in the world. Also, OIV trade statistics indicate the import of more than 12 million hectolitres of wine in the United States, indicating dependency on wines from Europe and Latin America.

Though the current high disposable income, presence of highly developed retail distribution networks, and presence of premium as well as imported still wine will help North America retain its position, there are indications of moderation in consumption in mature economies due to shifting preferences towards lower alcohol beverages.

Asia Pacific representing the fastest-growing regional segment. The USDA Foreign Agricultural Service reported that China imported approximately USD 1.6 billion of wine and related products in 2024, with Australia and France serving as the leading suppliers, while U.S. wine exports to China totalled USD 95.77 million, and Japan received USD 79.87 million in U.S. wine exports during the same period.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The worldwide still wine market is very fragmented due to a high number of established players mostly located in Europe and the rise of competitive new wine producers from the New World. The European Union makes up more than 60% of world-wide still wine exports in 2024, and France, Italy, and Spain still dominate in terms of volume and value of exports. In 2024, France had exported about 14.2 million hectoliters, thanks to efficient GI wine systems and high-end wine appellations. Meanwhile, Italy and Spain continue to have large capacities of wine production, accounting for over 70 million hectoliters produced in total in 2024.

Outside of Europe, there is competition from the USA, Australia, Chile, and Argentina, with vineyard export structures and trade deals in place. Based on the OIV data on world-wide trade, total wine exports stood at around 99.8 million hectoliters, meaning that fierce competition is present in the global still wine market. Export promotion policies by governments of EU and non-EU countries create additional competition among players trying to develop sustainable products with international reach and brand value.

The major players in the industry

- E & J. Gallo Winery

- Constellation Brands

- Treasury Wine Estates

- Pernod Ricard

- Diageo

- The Wine Group

- Concha y Toro

- Accolade Wines

- Castel Group

- Trinchero Family Estates

- Casella Family Brands

- Changyu Group

- Jackson Family Wines

- Sula Vineyards

- Familia Torres

Key Development

- In June 2026, Concha y Toro positioned itself as the world’s third-largest wine company by value as of end-2025, driven by a premiumisation strategy under which 57% of wine sales revenue now originates from premium and above segments, with cumulative premium revenue growing 47% between 2017 and 2025.

- In June 2024, Treasury Wine Estates increased production of premium still wines for exports, which correlated with increased wine exports reported by the Australian Government Export trade figures for the Asia-Pacific region in 2024.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 303.3 Bn |

| Forecast Revenue (2035) | USD 474.2 Bn |

| CAGR (2026-2035) | 4.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Red Still Wine, White Still Wine, Rosé Still Wine), By Packaging Type (Bottled Wine, Bag-in-Box, Canned Wine, Others), By Distribution Channel (Liquor Stores, Supermarkets/Hypermarkets, Bars, Pubs & Restaurants, Online Retail, Others), By Price Category (Economy Wine, Mid-Range/Premium Wine, Luxury Wine), By Technology (Dry Still wine and Wet Still wine), By End User (Household Consumption, Commercial/Hospitality) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | E. & J. Gallo Winery, Constellation Brands, Treasury Wine Estates, Pernod Ricard, Diageo, The Wine Group, Concha y Toro, Accolade Wines, Castel Group, Trinchero Family Estates, Casella Family Brands, Changyu Group, Jackson Family Wines, Sula Vineyards, Familia Torres. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |