Quick Navigation

Report Overview

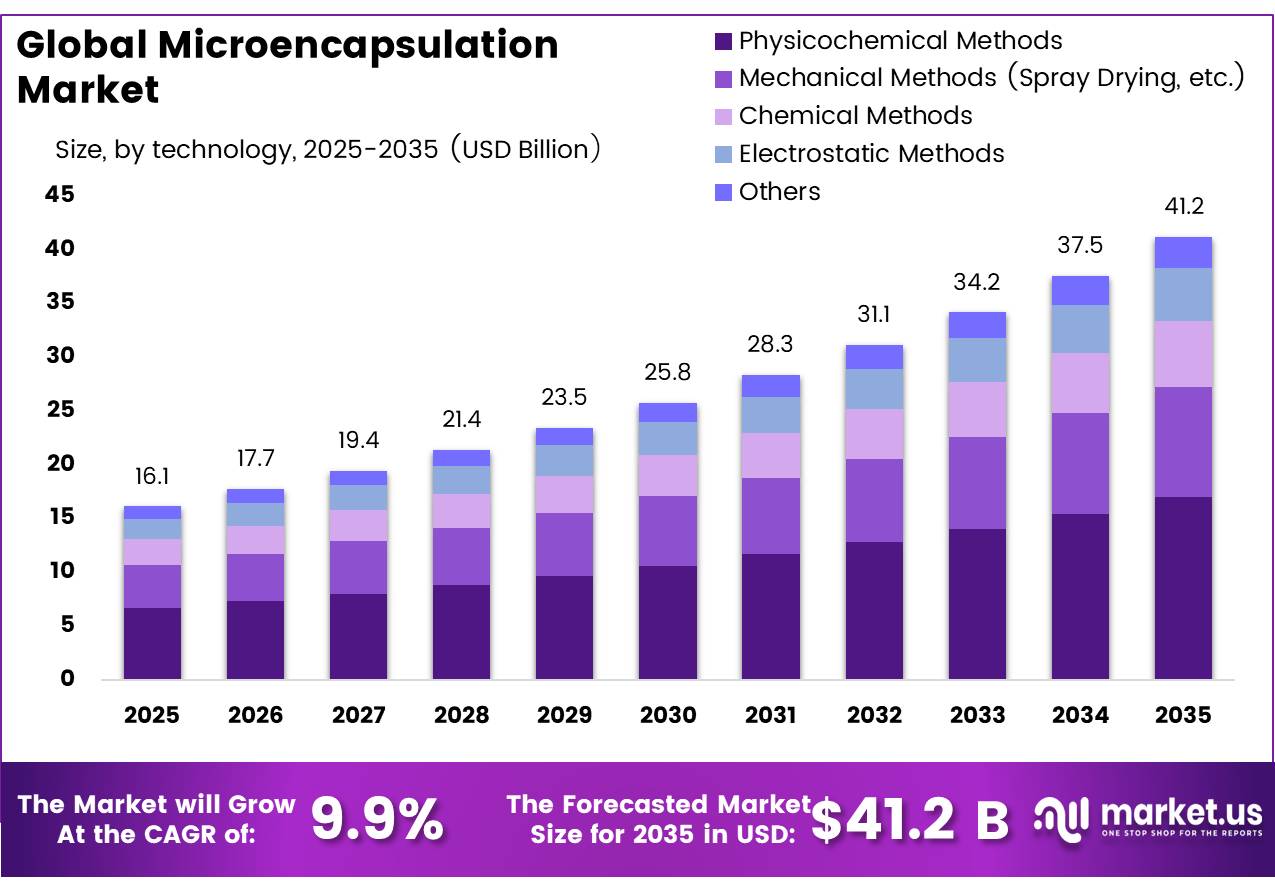

In 2025, the Global Microencapsulation Market was valued at USD16.1 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 9.9%, reaching about USD41.2 billion by 2035.In 2025, North America led the market, achieving over 36.8% share with a revenue of USD 5.9 Billion.

Key Takeaways

- The global microencapsulation market was valued at USD 16.1 billion in 2025.

- The market is projected to grow at a CAGR of 9.9% and is estimated to reach USD 41.2 billion by 2035.

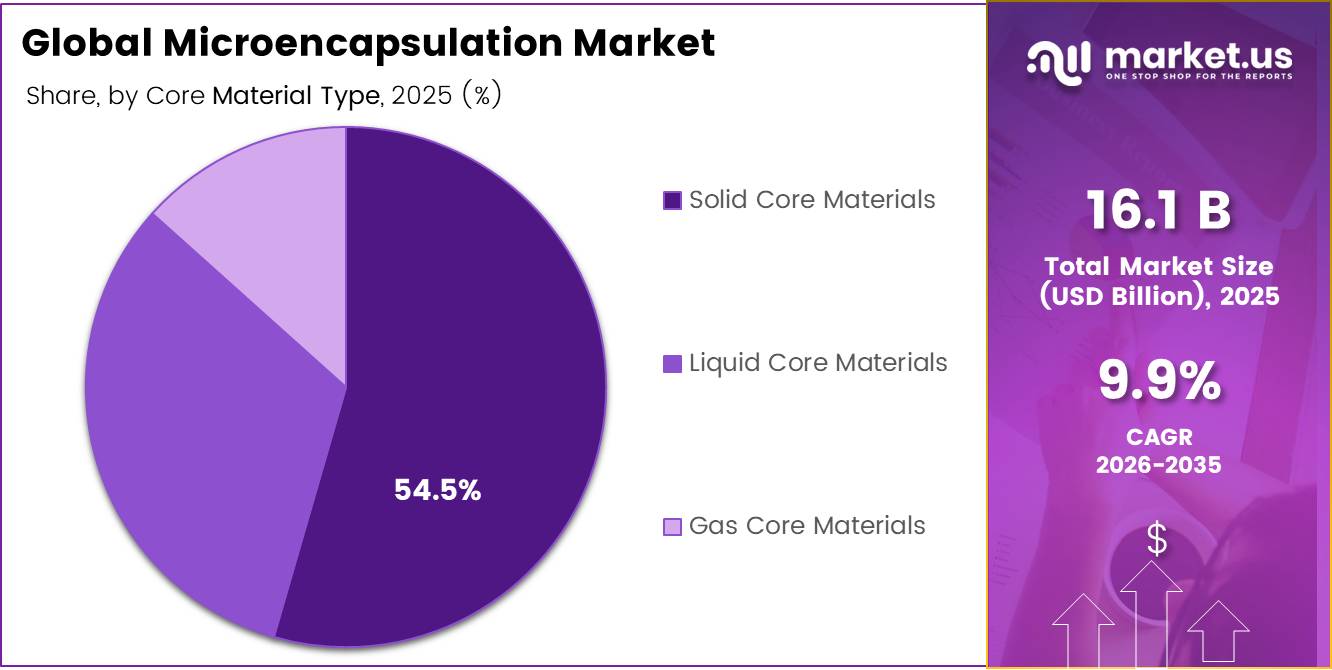

- On the basis of core material type, Solid Core Material dominated the market, constituting 54.5% of the total market share.

- Based on Shell, the Natural polymers dominated the microencapsulation market, with a substantial market share of around 35.9%.

- Based on the Technology, Physicochemical Methods led the market, comprising 41.2% of the total market.

- Among the Application, Pharmaceutical & Healthcare held a major share in the microencapsulation market, 38.5% of the market share.

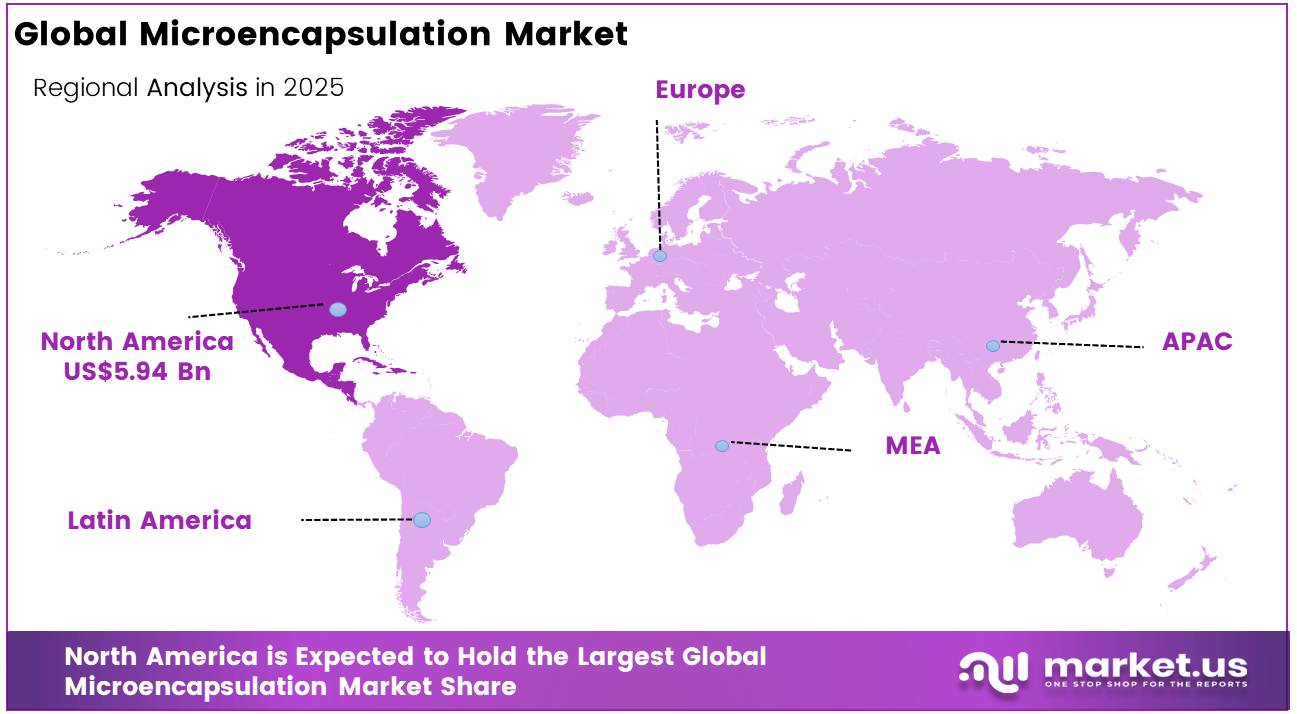

- In 2025, the North America was the most dominant region in the microencapsulation market, accounting for 36.8% of the total global consumption.

The global market for microencapsulation constitutes a strategically important sector in the domain of advanced material and delivery systems, with applications in pharmaceuticals, food and beverages, agricultural products, personal care products, and textile industry. As per estimates provided by the World Health Organization (2024), over 50% of patients enrolled in chronic therapy regime tend to fail in compliance to dosage regimen; microencapsulation technology solves this issue by ensuring extended release property, thus increasing therapeutic efficiency and enhancing patient compliance.

In October 2024, the Government of India implemented its rice fortification scheme worth over Rs 17,000 crore, supporting large-scale nutrient delivery in food products. This is expected to increase the use of microencapsulation technologies that protect vitamins and minerals during processing and storage. WHO’s updated guidance on edible oil fortification with vitamins A and D further supports its use in public nutrition programs.

Microencapsulation Market Segmentation

Core Material Type Analysis

Solid core Material represents dominant Segment in the Market.

The solid core segment dominates a commanding position in the world market for microencapsulation, making up 54.5% of the total market share. The dominance is largely attributed to various applications in the pharmaceutical and nutraceutical industries. In February 2025, a study involving researchers from the National Institutes of Health Office of Dietary Supplements reported that 11.0% of the U.S. population used dietary supplements for perceived immune benefits. This supports microencapsulation demand in solid-format nutrition products, where nutrients are protected for stability and controlled release, while WHO’s 2021 NONCOMMUNICABLE DISEASEs death data strengthens preventive nutrition demand.

Liquid core materials are one of the fastest-growing segments of the market, fueled by increased nutrition-related initiatives on part of governments. In November 2025, the WHO launched its guideline on fortification of edible oils and fats with vitamins A and D, noting that as of 2024, thirty-nine countries mandate or allow voluntary fortification of edible oils with vitamin A, and thirteen countries mandate co-fortification with both vitamins A and D, directly driving demand for liquid-core microencapsulation technologies used in oil-based nutrient delivery systems.

By Shell Analysis

Natural Polymers a significant Shell.

Natural polymers is a leading market segment in the global microencapsulation industry constituting a 35.9% share. This dominance is due to their strong use in food, pharmaceuticals, nutraceuticals, and personal care applications, where safety and biocompatibility are important. Materials such as gelatin, starch, alginate, cellulose derivatives, and gums are widely preferred because they are biodegradable, non-toxic, and effective in protecting sensitive ingredients. Their ability to improve stability, controlled release, and shelf life further supports segment growth.

In March 2025, the FDA issued new rules seeking to amend the GRAS procedure for notification of safety prior to introduction of ingredients into foods, ensuring preferential use of well-regulated substances like starches, gelatin, alginates, and cellulose derivatives in place of novel ingredients. The Department of Health and Human Services (HHS) mandated the FDA to regulate the safety and increase visibility of food ingredients through rigorous safety assessments.

The most rapidly growing segment among shell materials is that of synthetic polymers, as a result of escalating pharmaceutical innovations. The FY2025 budget of the US government called for allocation of a historic USD 2.2 billion for the National Nanotechnology Initiative, resulting in a total investment of over USD 45 billion since 2001, thus spurring FDA-approved synthetic polymers like PLGA and PLA.

Technology Analysis

Physicochemical Methods Are the Most Widely Used Technology.

Physicochemical encapsulation dominates the world microencapsulation industry at 41.2% market share due to its fundamental importance in pharmaceuticals and the development process of novel pharmaceuticals within pipelines by FDA’s CDER. CDER granted approval to 50 novel drugs in 2024 that have never been approved or sold in the United States; most of these require the use of physicochemical techniques such as coacervation, solvent evaporation, and complex emulsion to enable drug-controlled release.

Electrostatic methods stand out as the fastest growing technology segment, fueled by government spending on advanced materials studies. There are over 2 billion individuals worldwide currently suffering from vitamin or mineral deficiency disorders in 2024, hence the institutional drive towards precise nano-encapsulation drug delivery systems through the use of electrospray and electrospinning techniques. U.S. fiscal year 2025 NNI budget request of USD 2.2 billion, with total funding since 2001 surpassing USD 45 billion, accelerates research into electrostatic encapsulation.

Application Analysis

Pharmaceutical and Healthcare Are Mostly Utilized.

The pharmaceutical and healthcare industry dominates application segment share at 38.5%, thanks to consistent government funding of drug innovation research and continuous approval pipelines. The FDA’s Office of Oncologic Diseases approved 17 novel drugs for cancer treatments in 2024, covering gynecological, genitourinary, lung, gastro-intestinal, breast, thyroid, leukemia, lymphoma, and myelodysplastic syndromes, as well as 32 additional approvals to increase the scope of previously approved drug indications. 46 novel drugs were approved by CDER in 2025, further emphasizing the continuous expansion of the pipeline for pharmaceuticals using controlled release techniques with microencapsulation technology. According to a June 2025 report by WHO/Europe, the non-communicable diseases caused around 1.8 million premature deaths annually costing USD 514 billion in Europe.

The fastest growing application segment is Agrochemicals. Between January 2025, EPA was able to reduce their backlog of pesticide regulatory action by over 5,000 cases. In addition, USDA’s 2024 Pesticide Data Program tested 9,872 samples from 19 different commodities. These stringent safety measures have increased the adoption of microencapsulated controlled release technology in the agrochemicals market.

Key Market Segments

By Core Material Type

- Solid Core Materials

- Liquid Core Materials

- Gas Core Materials

By Shell

- Natural Polymers

- Synthetic Polymers

- Carbohydrates

- Lipids

- Gums & Resins

- Proteins

- Others

By Technology

- Physicochemical Methods

- Mechanical Methods (Spray Drying, etc.)

- Chemical Methods

- Electrostatic Methods

- Others

By Application

- Pharmaceutical & Healthcare

- Food & Beverage

- Home & Personal Care

- Agrochemicals

- Feed Additives

- Construction

- Textile

- Others

Drivers

Controlled-release pharma delivery

Personal care remains a stable demand driver for specialty and refined castor oil grades because of its moisturizing, emollient, and plant-based characteristics that align with growing consumer preference for sustainable ingredients. The global personal care ingredients market was valued at USD 13.42 billion in 2025 and is projected to reach USD 18.01 billion by 2032, supported by rising demand for multifunctional and biodegradable formulations. Castor derivatives are widely used in cosmetics, perfumes, surfactants, coatings, and personal care products, while cosmetic- and pharmaceutical-grade castor oils remain competitive in selected applications. Once approved in formulations such as lip care, hair oils, and skin products, demand typically remains consistent and supports premium product positioning.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Controlled-release pharma delivery | +1.9% | North America core, EU, India, Japan | Medium term (2-4 years) |

| Functional food fortification demand | +1.7% | North America, EU, urban APAC, GCC | Short term (≤ 2 years) |

| Probiotic survival and gut-health formats | +1.3% | North America, EU, South Korea, Japan, China | Short term (≤ 2 years) |

| Sensitive ingredient stability needs | +1.2% | Global food, nutraceutical, cosmetic markets | Short term (≤ 2 years) |

| Process scalability and cost optimization | +1.0% | North America, EU, China, India | Medium term (2-4 years) |

| Targeted release in specialty applications | +0.9% | EU, North America, advanced APAC corridors | Long term (≥ 4 years) |

Restraints

Scale-up yield losses

Many microencapsulation projects work well at lab or pilot scale but underperform when transferred to commercial throughput, making yield loss one of the most persistent adoption restraints in the category. For manufacturers, even a 5–10 point loss in encapsulation efficiency or an extra 2–4% reject/rework rate can materially alter unit economics in food and pharma applications, because the most expensive part of the formulation is often the active core itself; this raises effective cost per functional kilogram, delays plant ramp-up, and can postpone capacity expansion until process capability indices and batch reproducibility are proven over multiple campaigns.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High process cost | -1.8% | North America, EU, Japan, advanced APAC | Short term (≤ 2 years) |

| Regulatory approval drag | -1.4% | EU core, North America core, GCC, APAC regulated markets | Medium term (2-4 years) |

| Raw-material price volatility | -1.1% | Global, China-linked supply chains, EU importers | Short term (≤ 2 years) |

| Scale-up yield losses | -1.0% | North America, EU, India, China | Medium term (2-4 years) |

| Customer reformulation reluctance | -0.8% | Global food, pharma, personal care markets | Medium term (2-4 years) |

| Carrier clean-label limits | -0.7% | EU, North America, halal-sensitive APAC and GCC | Long term (≥ 4 years) |

Opportunity

Encapsulation CDMO services

A growing opportunity in the microencapsulation industry is the shift from basic ingredient processing toward a CDMO model, where companies provide formulation and development support in addition to production. By offering services such as feasibility studies, pilot production, scale-up, and validation, companies can increase gross margins by approximately 500–900 basis points compared with traditional toll processing. This model also supports long-term supply agreements and creates stronger customer retention through formulation-based partnerships.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Precision nutrition platforms | +1.9% | North America core, EU, Japan, premium APAC | Medium term (2-4 years) |

| Encapsulation CDMO services | +1.6% | North America, EU, India, China | Short term (≤ 2 years) |

| Pet and animal nutrition | +1.3% | North America, EU, Brazil, China | Short term (≤ 2 years) |

| Microfluidic pharma scale-up | +1.2% | North America core, EU, Japan | Medium term (2-4 years) |

| AI process optimization | +1.0% | North America, EU, China, India | Short term (≤ 2 years) |

| Agrochemical delivery pivot | +0.9% | Latin America, India, China, Southeast Asia | Long term (≥ 4 years) |

Challenges

Scale-up reproducibility gap

The market’s most persistent operational challenge is the difficulty of translating lab-scale encapsulation performance into commercial batches without losing particle uniformity, encapsulation efficiency, release accuracy, or stability, because droplet formation, shell deposition, drying kinetics, solvent removal, and core-shell interaction all behave differently when throughput scales by 10–100x.

In practice, even a 4–8 percentage point drop in encapsulation efficiency or a 2–5% increase in off-spec lots can erase the expected margin benefit of premium delivery systems, especially when the active core is expensive, and repeated pilot reruns can extend commercialization timelines by 6–12 months, delay customer approvals, and push internal CapEx payback beyond acceptable thresholds.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Scale-up reproducibility gap | -1.3% | North America, EU, India, China | Medium term (2-4 years) |

| Specialist equipment bottlenecks | -1.1% | North America, EU, China, Japan | Short term (≤ 2 years) |

| Analytical quality burden | -0.9% | Pharma core, food-grade hubs, EU, US | Medium term (2-4 years) |

| Formulation talent shortage | -0.8% | North America, EU, India, Japan | Long term (≥ 4 years) |

| Digital process immaturity | -0.7% | North America, EU, advanced APAC | Medium term (2-4 years) |

| Multi-input sourcing instability | -0.6% | Global, China-linked and EU-import chains | Short term (≤ 2 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Microencapsulation Manufacturing.

The geopolitical conflicts arising between the two countries are directly affecting the supply chain of encapsulant substances, shell-forming polymers, and APIs vital for the manufacture of microencapsulated formulations. The Congressional Research Service report by the US government stated that around 80% of the world’s drug supply comes from China’s APIs, and a Section 232 national security review is being carried out in April 2025 concerning imported pharmaceuticals and APIs.

A white house executive order passed in August 2025 highlighted that just around 10% of the APIs required for US prescriptions are domestically made. This clearly implies that there is heavy foreign dependency on the pharmaceutical industry.

According to the executive order, HHS would compile a list of approximately 26 medicines and prepare a six months’ domestic reserve of APIs called the Strategic Active Pharmaceutical Ingredients Reserve. Also, in May 2025, President Donald Trump passed an executive order which would work to eliminate the regulatory barriers and promote a local manufacturing facility for prescription drugs and ingredients required in their manufacture.

Regional Analysis

North America Held the Largest Share of the Global Microencapsulation Market.

The dominant geographical region of the global microencapsulation market is North America, with a 36.8% market share. This dominance is due to strong demand from pharmaceuticals, functional foods, dietary supplements, agrochemicals, and personal care products. The region has advanced research facilities, strong healthcare spending, and a well-developed food and nutrition industry. Growing use of controlled-release drug delivery, fortified foods, probiotics, and protected active ingredients continues to support the expansion of microencapsulation technologies across North America.

Asia Pacific region is one of the fastest growing geographical regions driven by mandated government nutrition programs. According to the FAO, IFAD, UNICEF, WFP and WHO joint SOFI 2025 report, stunting prevalence fell to 23.2% in 2024, reducing the number of stunted children globally from 180.4 million in 2012 to 150.2 million in 2024, with Asia Pacific home to the largest share of affected populations, directly driving government-mandated encapsulation-based micronutrient delivery programs across the region.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Innovation-driven companies in the microencapsulation industry are now looking towards technology differentiators, integration with local supply chain networks, and regulatory compliance to ensure competitive positioning. One of the key elements in this context is the move towards the development of high-performance encapsulant materials and controlled release formulations through innovative initiatives that have the backing of the government.

According to the Congressional Research Service, NIH’s total enacted appropriations reached approximately USD 47.5 billion in FY2026, with nearly 83% supporting extramural research and training programs at universities and medical centers through grants, directly sustaining the biomedical research pipeline that underpins microencapsulation-based drug delivery innovation globally.

In addition, there are also geopolitical developments that are influencing the supply chain and logistics management process. In reaction, the FDA initiated the PreCheck Pilot Program based on Executive Order 14293 issued in May 2025.

The Major Players in The Industry

- BASF SE

- Evonik Industries AG

- Balchem Corporation

- 3M Company

- Dow Inc.

- Royal DSM N.V.

- Aveka Group

- International Flavors & Fragrances Inc. (IFF)

- Encapsys LLC (a Syensqo company)

- Givaudan SA

- Firmenich SA

- Symrise AG

- Lycored Corp.

- Cargill, Incorporated

- Ingredion Incorporated

- Lonza Group AG

- Microtek Laboratories, Inc.

- Reed Pacific Pty Ltd.

- TasteTech Ltd.

- Sphera Encapsulation

- Others

Key Development

- In December 2025, Balchem Corporation revealed plans for the construction of a high capacity manufacturing plant in the US, which will house its cutting-edge microencapsulation technologies that can be used for its food ingredients like the BakeShure, ConfecShure, and MeatShure product ranges, with the plant anticipated to commence operations in 2027.

- In December 2024, Lonza Group AG extended its services by catering to the needs of the developers of smart oral biologics capsules, with unique Capsugel® Enprotect® bi-layered capsules and advanced formulations for their use.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$16.1 Bn |

| Forecast Revenue (2035) | US$41.2 Bn |

| CAGR (2026-2035) | 9.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Core Material Type (Solid Core Materials, Liquid Core Materials, Gas Core Materials), By Shell (Natural Polymers, Synthetic Polymers, Carbohydrates, Lipids, Gums & Resins, Proteins, Others), By Technology (Physicochemical Methods, Mechanical Methods (Spray Drying, etc.), Chemical Methods, Electrostatic Methods, Others), By Application (Pharmaceutical & Healthcare, Food & Beverage, Home & Personal Care, Agrochemicals, Feed Additives, Construction, Textile, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BASF SE, Evonik Industries AG, Balchem Corporation, 3M Company, Dow Inc., Royal DSM N.V., Aveka Group, International Flavors & Fragrances, Encapsys LLC (a Syensqo company), Givaudan SA, Firmenich SA, Symrise AG, Lycored Corp., Cargill, Incorporated, Ingredion Incorporated, Lonza Group AG, Microtek Laboratories, Inc., Reed Pacific Pty Ltd., TasteTech Ltd., Sphera Encapsulation, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |