Quick Navigation

Report Overview

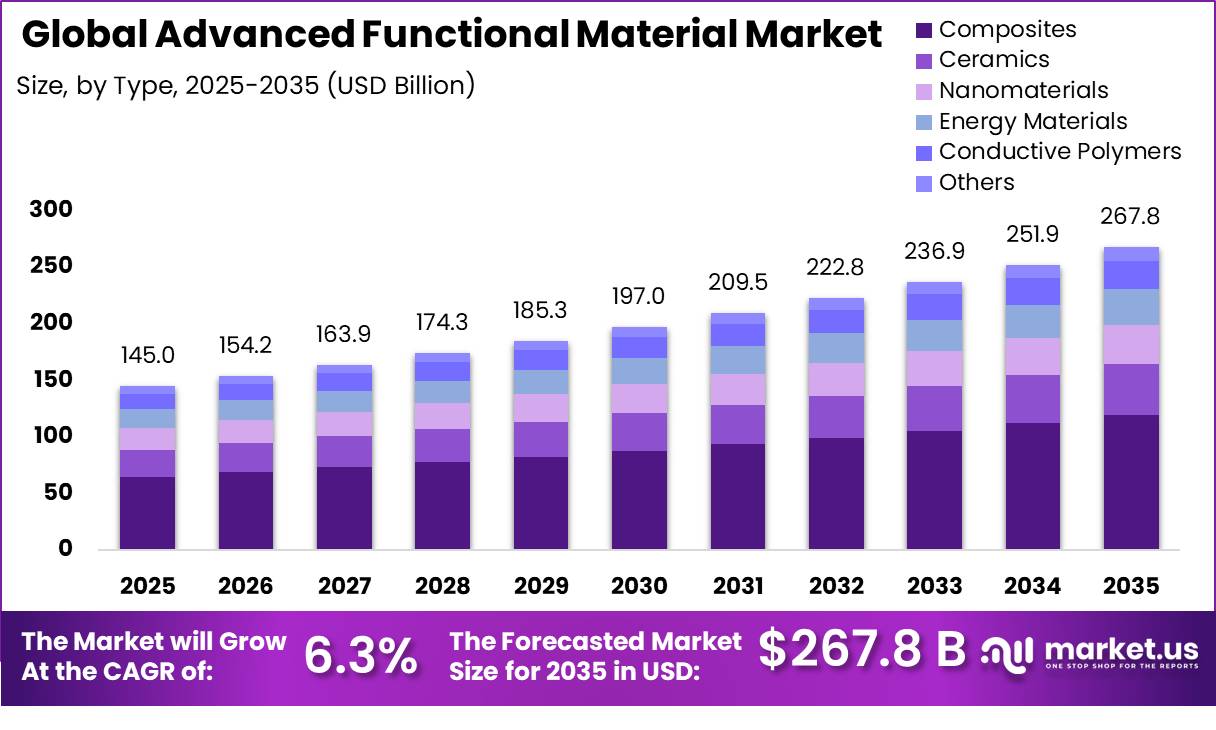

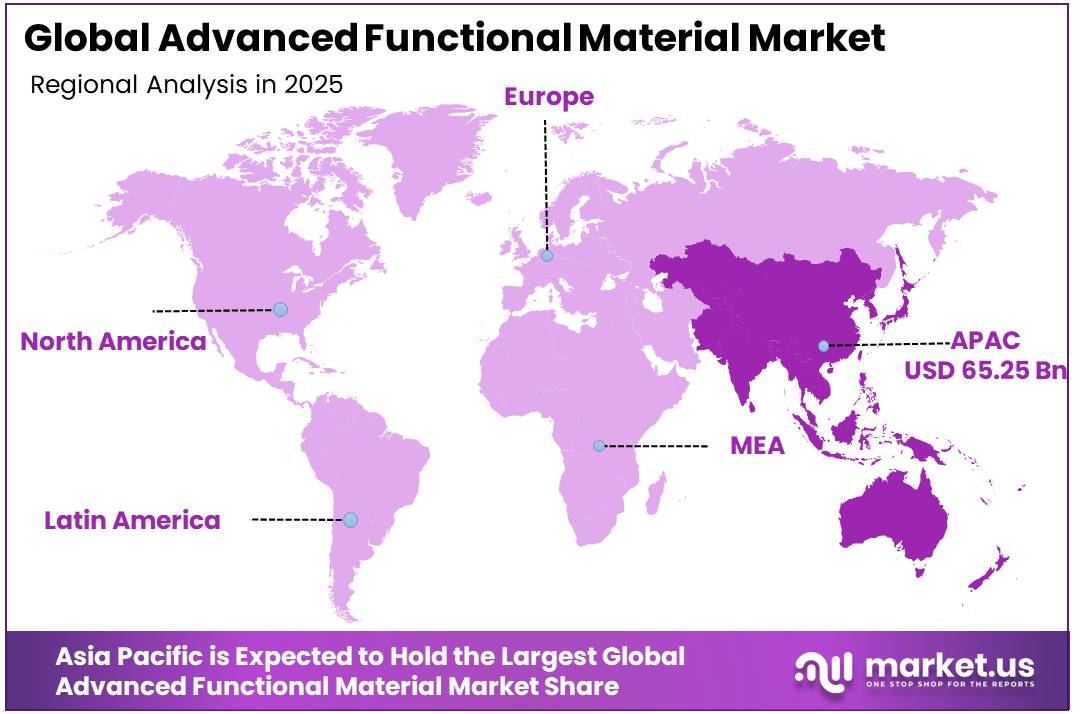

The Global Advanced Functional Material Market size is expected to be worth around USD 267.8 Billion by 2035, from USD 145.0 Billion in 2025, growing at a CAGR of 6.3% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 45.0% share, holding USD 65.25 Billion revenue.

Advanced functional materials represent a broad class of engineered materials designed to deliver specific electrical, thermal, magnetic, optical, catalytic, and mechanical properties that exceed the performance of conventional materials. These materials include advanced ceramics, high-performance polymers, composites, nanomaterials, semiconductor materials, battery materials, and specialty coatings. They have become essential across industries such as electronics, renewable energy, aerospace, healthcare, automotive, and telecommunications.

- According to the International Energy Agency, EV battery deployment reached 1.2 TWh in 2025, nearly 30% higher than 2024 and more than 7 times the 2020 level. This is creating strong demand for cathode, anode, separator, electrolyte, thermal-management, and lightweight composite materials.

- According to the Semiconductor Industry Association (SIA), global semiconductor sales reached US$627.6 billion in 2024, representing a 1% increase compared with 2023. The rapid expansion of artificial intelligence, high-performance computing, and advanced electronic devices has increased the need for specialty semiconductor materials, advanced substrates, and high-purity chemicals.

- The International Energy Agency (IEA) reported that global electric car sales exceeded 17 million units in 2024, accounting for more than 20% of total car sales worldwide, driving demand for advanced battery materials, lightweight composites, and thermal management solutions used in electric vehicles.

Key Takeaways

- The Global Advanced Functional Material Market was valued at USD 145.0 billion in 2025.

- The market is projected to grow at a CAGR of 6.3% and is estimated to reach USD 267.8 billion by 2035.

- Composites are the dominant material type, accounting for 44.7% of the market in 2025, driven by their broad adoption across aerospace, automotive, and electrical applications.

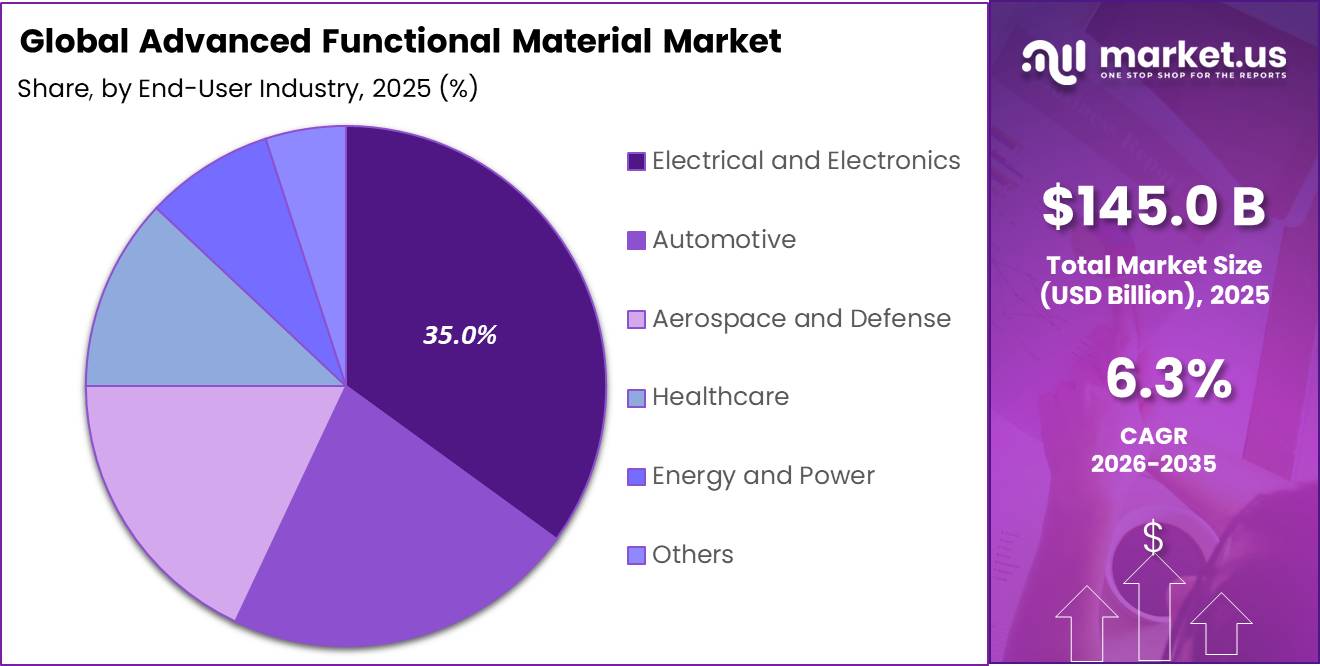

- Electrical and Electronics is the dominant end-user industry at 35.0%, driven by the highest material performance requirements of any end-user sector.

- Asia Pacific holds the largest regional share at 45.0%, driven by the concentration of electronics manufacturing, automotive production, and materials processing across China, Japan, South Korea, and India.

Government support is also reshaping the sector. In the U.S., the Department of Energy’s Battery Materials Processing Grants program has USD 3 billion in funding, with USD 600 million appropriated annually from fiscal years 2022 to 2026. In January 2025, DOE also issued a notice of intent for up to USD 725 million to support domestic battery critical materials, battery components, and advanced batteries. In Europe, the Critical Raw Materials Act targets 10% domestic extraction, 40% processing, and 25% recycling of annual strategic raw material needs by 2030.

- In March 2025, the European Commission also backed strategic raw-material projects, while the EU and private partners planned up to EUR 250 million each by 2030 for the Innovative Advanced Materials partnership.

Advanced Functional Material Market Segmentation

By Type

Composites Represent the Dominant Segment in the Market.

In 2025, Composites accounted for a leading 44.7% share of the Advanced Functional Material market, due to their unmatched combination of high strength-to-weight ratio, design flexibility, and corrosion resistance across aerospace, automotive, wind energy, and electrical applications. Carbon fibre reinforced polymer composites, glass fibre composites, and ceramic matrix composites collectively serve the broadest application base of any advanced functional material category. DOE’s IACMI institute is actively developing lower-cost, higher-speed manufacturing and recycling processes for advanced composites with composites offering 25–70% mass reduction over steel in automotive structural applications.

End-User Industry Analysis

Advanced Functional Material Mainly Utilized in Electrical and Electronics Sector.

In 2025, Electrical and Electronics accounted for a leading 35.0% share of the market by end-user industry, this dominance is driven by sector’s demand for the highest-performance functional materials across semiconductor substrates, printed circuit boards, insulating ceramics, conductive polymers, and electromagnetic shielding composites. Every generation of electronics miniaturisation from consumer devices to AI data centre hardware requires new functional material solutions. AI data centres are driving particularly strong demand for advanced thermal management materials, high-frequency dielectric ceramics, and conductive polymer substrates.

Key Market Segments

By Type

- Composites

- Ceramics

- Nanomaterials

- Energy Materials

- Conductive Polymers

- Others

By End-User Industry

- Electrical and Electronics

- Automotive

- Aerospace and Defense

- Healthcare

- Energy and Power

- Others

Driver Analysis

Additive Manufacturing and Smart Materials Drive Demand

The convergence of industrial-scale additive manufacturing (AM) and smart material adoption is creating a high-value growth path for Advanced Functional Materials (AFM). In 2026, the global additive manufacturing market is estimated at approximately USD 28.27–31.48 billion and is projected to reach USD 59.27–114.45 billion by 2030–2033, growing at a CAGR of 20.3%–24.0%, while metal 3D printing is expanding at over 25% annually.

This is increasing demand for premium metallic powders such as titanium, Inconel 718, cobalt-chrome, and advanced polymers including PEEK and ULTEM, which carry 3–8× higher pricing than conventional materials. At the same time, the smart materials market reached USD 84.78 billion in 2025 and is expected to grow to USD 148.15 billion by 2032, creating strong opportunities across aerospace, healthcare, and defense applications.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI & Semiconductor Expansion | 2.20% | North America (core), APAC — Taiwan, South Korea, Japan (dominant); EU (emerging fab investment) | Short term (≤ 2 years) |

| EV & Energy Storage Transition | 1.90% | APAC (China leading ~60% of battery supply chain); North America (IRA-backed); EU (CRMA-driven) | Short–Medium term (1–4 years) |

| Aerospace & Defense Lightweighting | 1.50% | North America (core OEM spend); EU (NATO rearmament); APAC corridors (India, Japan, South Korea) | Medium term (2–4 years) |

| Green Hydrogen & Energy Transition Materials | 1.20% | EU (Renewable Energy Directive mandate); APAC (China ~60% of operational capacity); South America spill-over (export projects) | Medium–Long term (2–5 years) |

| Regulatory-Driven Circular Design & CRM Compliance | 0.90% | EU (regulatory epicenter); North America (IRA supply-chain localization); APAC secondary compliance pull | Medium–Long term (3–6 years) |

| Additive Manufacturing & Smart Material Integration | 1.10% | North America (40.8% AM market share); EU (defense and aerospace AM); APAC (fastest-growing AM deployment) | Short–Medium term (1–4 years) |

Restraint Analysis

PFAS & Chemical Substance Bans — Reformulation Cost Burden

Growing global restrictions on PFAS chemicals are creating a major challenge for the Advanced Functional Materials (AFM) industry. PFAS substances, widely used in fluoropolymer coatings, membranes, and high-performance dielectric materials, are facing tighter regulations across major markets.

Under the EU REACH proposal, restrictions are expected to begin from December 2026 with transition periods extending to 2027, targeting fluorinated materials above 25 ppb for individual PFAS and 250 ppb combined levels. Reformulation costs are estimated at USD 50,000–500,000 per product line, creating total compliance expenses of USD 5–20 million for mid-sized producers. Additionally, 12–36 month qualification cycles for PFAS-free alternatives may slow AFM market growth through 2029.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China’s Rare Earth Export Controls & CRM Geopolitics | −1.8% | Global; North America & Japan (most acute); EU secondary; South Korea spillover | Short term (≤ 2 years) |

| Prohibitive Scale-Up Costs & Lab-to-Factory Commercialization Gap | −1.4% | Global; North America & EU (highest CapEx exposure); APAC (partial mitigation via state subsidy) | Short–Medium term (1–4 years) |

| PFAS & Chemical Substance Bans — Reformulation Cost Burden | −1.1% | EU (regulatory origin); North America (EPA enforcement); APAC compliance pull | Short–Medium term (1–3 years) |

| US–China Trade Tariff Architecture & Sectoral Import Duties | −1.0% | North America (direct); APAC export-dependent corridors (secondary); EU (trade diversion effects) | Short term (≤ 2 years) |

| Skilled Workforce Scarcity & Talent Pipeline Deficit | −0.7% | North America & EU (most severe); APAC (moderate, partially subsidized) | Long term (≥ 4 years) |

| Regulatory Compliance Overhead & Product Certification Latency | −0.6% | EU (epicenter); North America (EPA/FDA overlay); Global (compliance pull-through) | Medium–Long term (3–6 years) |

Opportunity Analysis

Blue Economy and Carbon Capture Growth Opportunity

The blue economy and carbon capture materials segment represents a long-term growth opportunity for Advanced Functional Materials (AFM), supported by government funding and emerging commercial demand.

In 2026, the EU Sustainable Blue Economy Partnership funded 24 research and innovation projects with a combined investment of €40 million, creating demand for anti-biofouling coatings, corrosion-resistant marine materials, and seawater electrolyzer components. In carbon capture, the U.S. DOE 45Q tax credit offers up to USD 180 per tonne of permanently captured CO₂, supporting adoption of advanced sorbent materials. The carbon capture sorbent materials market is projected to reach USD 2.8–3.5 billion by 2030, creating strong opportunities for early AFM suppliers.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| AI-Accelerated Materials Discovery Platform | 2.10% | North America (core IP base); EU (regulatory application); APAC (deployment scale) | Short–Medium term (1–4 years) |

| Smart Textiles & Flexible Electronics | 1.70% | APAC emerging markets (India, Vietnam, Indonesia); North America (healthcare wearables); EU (defense smart uniforms) | Short–Medium term (2–4 years) |

| Southeast Asia & India Manufacturing Footprint Build-Out | 1.50% | India, Vietnam, Malaysia, Thailand, Indonesia; secondary: Bangladesh, Philippines | Short term (≤ 2 years) |

| Bio-Based Functional Material Substitution | 1.30% | EU (regulatory trigger market); North America (EPA-driven); APAC (voluntary ESG-led substitution) | Medium term (2–4 years) |

| M&A Roll-Up of Specialty Material Niche Producers | 1.20% | North America (acquisition target density); EU (fragmented mid-market); APAC (founder-owned scale-up targets) | Short–Medium term (1–4 years) |

| Blue Economy & Carbon-Capture Materials | 0.90% | EU (regulatory pull + blue economy mandates); North America (DOE-funded carbon capture); APAC (offshore wind corridors) | Long term (≥ 4 years) |

Challenges Analysis

Energy Price Volatility & Production Cost Inflation

Advanced functional material (AFM) manufacturing remains highly energy intensive, creating cost pressure across production operations. Processes such as atmospheric plasma spray consume 15–25 MWh per tonne, advanced ceramic sintering requires 7–12 MWh per tonne at temperatures of 1,200–1,800°C, and CVD thin-film production uses 20–40 kWh per wafer equivalent.

Energy has become the second-largest operating cost after raw materials. Since 2019, industrial electricity prices in parts of Europe increased by up to 150%, while APAC producers maintain a 15–25% cost advantage through controlled tariffs. To reduce exposure, manufacturers are investing USD 30–120 million in renewable PPAs, energy recovery systems, and lower-emission process upgrades.

Challenges Impact Analysis

| Challenge | (~) % Potential CAGR | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Batch-to-Batch Quality Inconsistency | −1.3% | Global; North America & EU (strictest OEM specs); APAC (moderate mitigation via volume tolerance) | Medium term (2–4 years) |

| Energy Price Volatility & Production Cost Inflation | −1.0% | EU (highest exposure); North America (moderate); APAC (subsidized partial insulation) | Long term (≥ 4 years) |

| Multi-Jurisdictional Standards Fragmentation | −0.9% | EU (regulatory epicenter); North America (FDA/EPA divergence); APAC (China GB standards parallel track) | Long term (≥ 4 years) |

| Long OEM Qualification Cycles & Time-to-Revenue Lag | −0.8% | North America & EU (strictest qualification regimes); APAC (faster consumer electronics approvals, slower defense) | Medium–Long term (3–5 years) |

| End-of-Life Recycling & Circular Economy Technical Gap | −0.7% | EU (ESPR mandate enforcement); North America (EPA extended producer liability); APAC (emerging e-waste regulation) | Long term (≥ 4 years) |

| Cybersecurity & IP Leakage in Digital Manufacturing | −0.5% | Global; North America & EU (highest digital process adoption); APAC (dominant threat origin vector) | Medium term (2–4 years) |

Geopolitical Impact Analysis

The Advanced Functional Material (AFM) market — spanning high-performance ceramics, rare-earth permanent magnets, specialty polymers, carbon composites, and engineered coatings — is operating under unprecedented geopolitical strain, with raw material access, production economics, and global distribution all under simultaneous duress. China’s sequential tightening of rare earth export controls represents the most structurally disruptive force: as of April 2025, Beijing imposed licensing requirements on seven heavy rare earth elements (REEs), including dysprosium and terbium — critical inputs in NdFeB permanent magnets used across piezoelectric actuators, magnetostrictive sensors, and functional coating systems.

China produces more than 60% of mined rare earths globally and controls approximately 85% of processing capacity, a near-monopoly that rendered immediate alternatives nonviable. Following the April controls, prices for dysprosium oxide tripled and terbium oxide more than doubled by May 2025, directly inflating input costs across AFM sub-segments from magnetocaloric alloys to hard-coated optical films.

Simultaneously, escalating trade tariff regimes and maritime logistics volatility are compounding AFM manufacturers’ cost structures across procurement, production, and distribution. The United States raised steel and aluminum import tariffs to 25% in March 2025, and the overall average effective U.S. tariff rate reached 18.6% by mid-2025 — the highest level since 1933 — driving an estimated 1.8% broad consumer price-level increase.

For specialty chemical precursors and functional material feedstocks sourced from China, effective duties have surged well above 30%, reshaping sourcing economics for producers of advanced polymer matrices, metallic glass composites, and high-purity alumina substrates. On the logistics front, persistent Houthi attacks in the Red Sea — with over 190 incidents recorded through October 2024 — compelled all major container lines to permanently reroute through the Cape of Good Hope, adding 10 to 20 extra transit days on Asia–Europe corridors.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Advanced Functional Material Market.

In 2025, Asia Pacific dominated the global Advanced Functional Material market, holding about 45% of total global consumption at USD 65.25 billion. This dominance is structural rooted in Asia Pacific’s position as the world’s largest electronics manufacturing hub, the largest automotive production region, and the leading centre for advanced ceramics and nanomaterials processing. China, Japan, South Korea, and India collectively host the majority of global functional ceramics production, conductive polymer manufacturing, and composite materials processing capacity.

North America represents the second-largest regional market anchored by aerospace and defense composite demand, semiconductor functional materials procurement, and DOE AMMTO-backed advanced materials manufacturing investment. Europe holds a significant market position through its automotive lightweighting composite demand, advanced ceramics production in Germany and Finland, and chemical functional materials manufacturing by companies including BASF SE, Evonik Industries AG, Arkema S.A., and Covestro AG.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Global Advanced Functional Material Market is characterised by a fragmented competitive structure at the overall market level, with no single company commanding dominant share across all material types, end-user industries, and geographies. The market is served by large diversified chemical and materials conglomerates, specialised advanced materials companies, and niche functional material producers each competing across specific material categories and application niches. BASF SE, 3M Company, DuPont de Nemours, Evonik Industries AG, Arkema S.A., and Covestro AG represent the largest diversified participants each with broad functional materials portfolios spanning multiple type categories and end-user industries

Kyocera Corporation and Murata Manufacturing lead in functional ceramics for electronics. Momentive Performance Materials leads in silicone-based functional materials. Applied Materials serves semiconductor functional materials applications. Materion Corporation specialises in precision functional materials for aerospace and defense. The overall market rewards materials science innovation capability, manufacturing process scalability, application engineering expertise, and the ability to qualify functional materials within demanding customer specification frameworks across electronics, automotive, and aerospace end-user industries.

The Major Players in The Industry

- 3M Company

- Arkema S.A.

- BASF SE

- Covestro AG

- Evonik Industries AG

- Applied Materials, Inc.

- Huntsman International LLC

- Kyocera Corporation

- Materion Corporation

- Momentive Performance Materials Inc.

- Murata Manufacturing Co., Ltd.

- Ceradyne, Inc.

- Air Products and Chemicals, Inc.

- DuPont de Nemours, Inc.

- Showa Denko K.K.

- Others

Key Development

- In June 2026, Eastman Chemical Company successfully finalized a definitive cross-border commercial acquisition agreement to purchase the specialized Jarylec dielectric brand portfolio from Arkema S.A., expanding its footprint in high-purity electrical insulation and electronic materials.

- In August 2025, Covestro completed the 100% acquisition of Pontacol AG for €28 million, with possible earn-out payments of up to €5 million, adding multilayer thermoplastic adhesive films for automotive, electronics, textiles, and medical technology applications. On the merger and ownership side, ADNOC/XRG completed its takeover offer in December 2025, with related holdings reaching around 95.10% of Covestro’s voting rights, giving the company a stronger long-term capital base for circular and high-performance material growth.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 145.0 Bn |

| Forecast Revenue (2035) | USD 267.8 Bn |

| CAGR (2026-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Composites, Ceramics, Nanomaterials, Energy Materials, Conductive Polymers, Others), By End-User Industry (Electrical and Electronics, Automotive, Aerospace and Defense, Healthcare, Energy and Power, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | 3M Company, Arkema S.A., BASF SE, Covestro AG, Evonik Industries AG, Applied Materials, Inc., Huntsman International LLC, Kyocera Corporation, Materion Corporation, Momentive Performance Materials Inc., Murata Manufacturing Co., Ltd., Ceradyne, Inc., Air Products and Chemicals, Inc., DuPont de Nemours, Inc., Showa Denko K.K., Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |