Quick Navigation

Report Overview

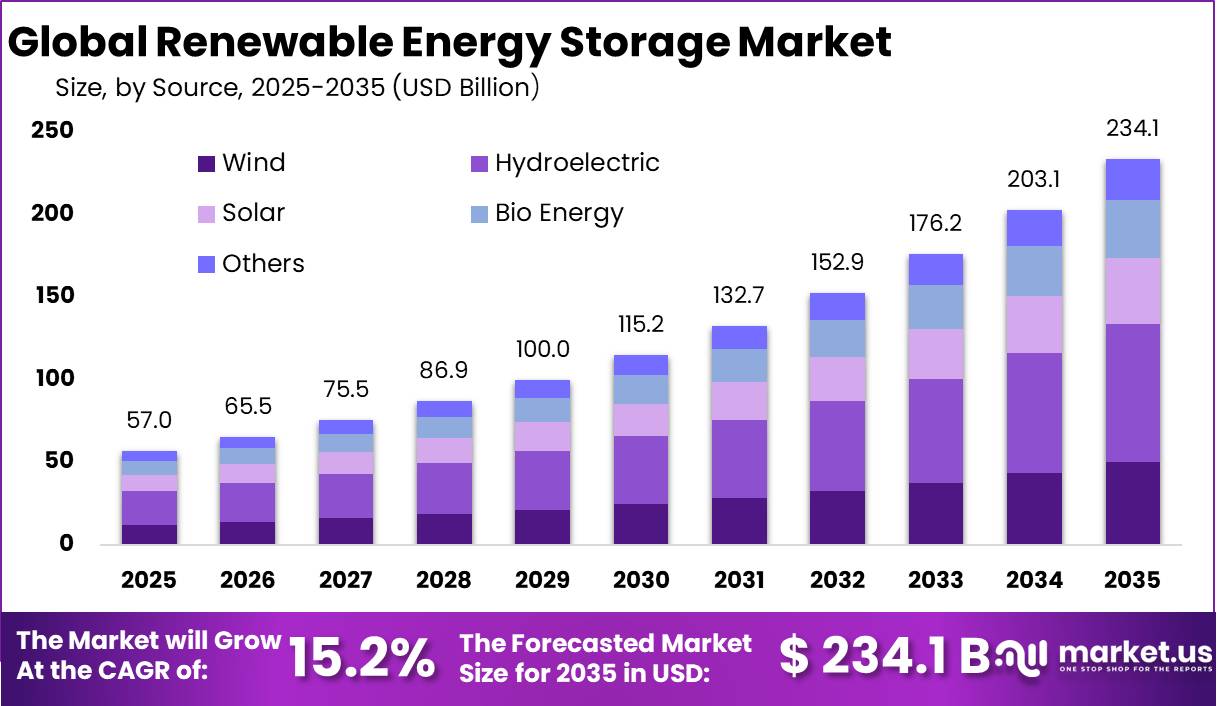

The Global Renewable Energy Storage Market size is expected to be worth around USD 234.1 Billion by 2035, from USD 57.0 Billion in 2025, growing at a CAGR of 15.2% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 37.60% share, holding USD 1.9 Billion revenue.

Renewable energy storage is becoming a core part of the global power system because solar and wind generation need flexible backup when weather changes. In 2025, the industry moved from a support technology to a grid-planning priority, as IEA reported about 108 GW–110 GW of new battery storage capacity added globally, around 40% higher than 2024. IRENA also reported that renewable power capacity rose by 692 GW in 2025, with solar adding 511 GW and wind 159 GW, creating stronger demand for batteries, pumped hydro, thermal storage and hybrid storage systems.

Key Takeaways

- Renewable Energy Storage Market size is expected to be worth around USD 234.1 Billion by 2035, from USD 57.0 Billion in 2025, growing at a CAGR of 15.2%.

- Hydroelectric held a dominant market position, capturing more than a 35.80% share in the Renewable Energy Storage Market.

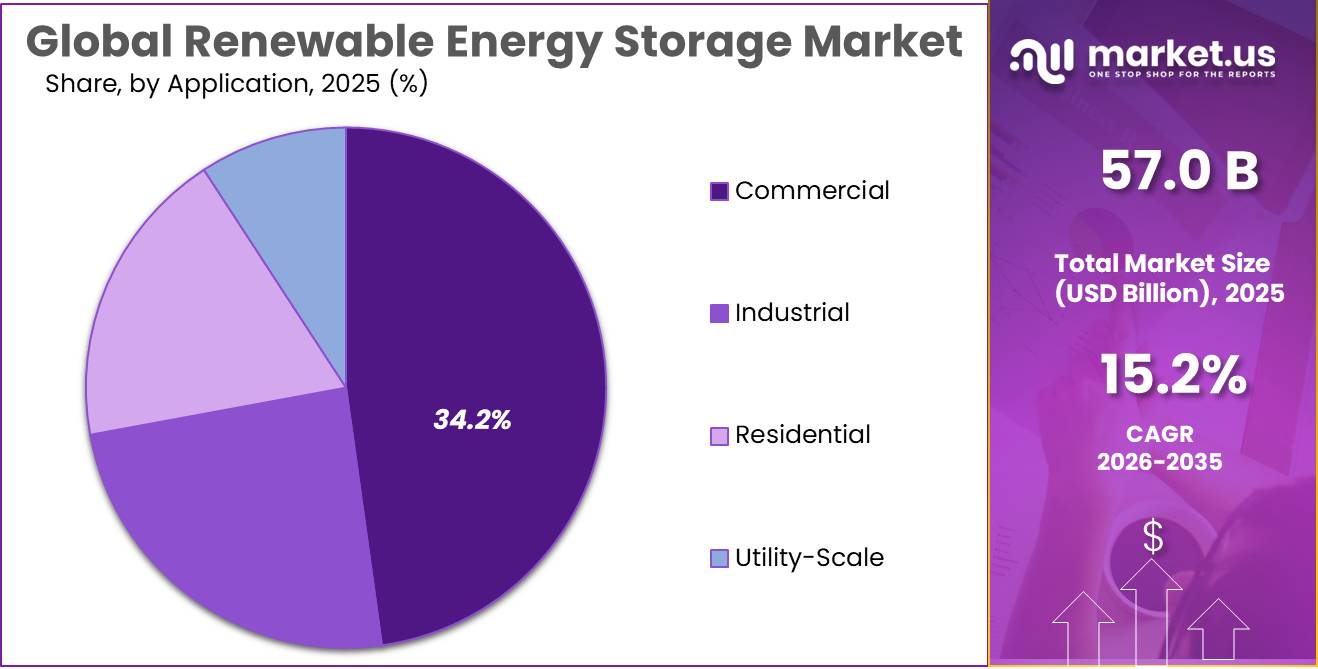

- Commercial held a dominant market position, capturing more than a 47.80% share in the Renewable Energy Storage Market.

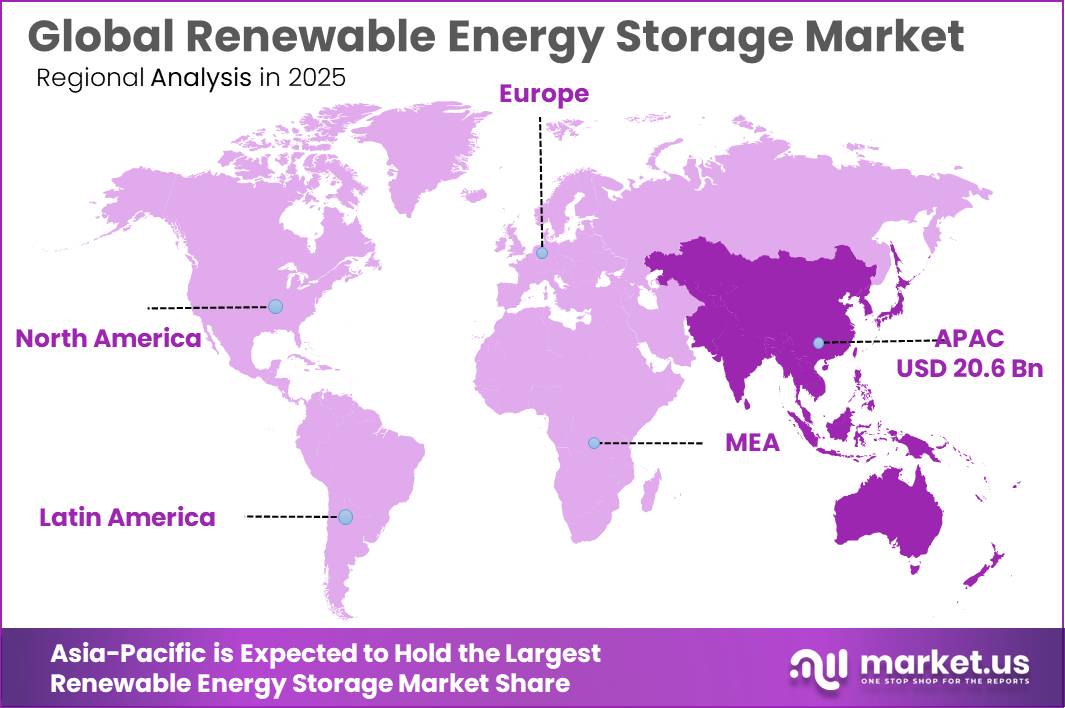

- Asia-Pacific held the dominant position in the Renewable Energy Storage Market, accounting for 36.20% of the global market and reaching a value of USD 20.6 Billion.

The industrial scenario is being shaped by utility-scale batteries, commercial and industrial storage, EV-charging-linked storage, and grid-balancing projects. Renewable energy storage is especially important because renewables already supplied nearly one-third of global electricity generation in 2024, including hydropower at 14%, wind at 8%, and solar PV at 7%. IEA expects battery storage to rise sharply, with storage deployment needing about 25% annual growth to 2030, and battery storage potentially reaching 1,200 GW by 2030 under secure energy transition pathways.

Key driving factors include rising renewable penetration, grid congestion, peak-load management, falling lithium-iron-phosphate battery adoption costs, and government-backed clean energy investment. IEA estimated total energy investment at USD 3.3 trillion in 2025, with around USD 2.2 trillion going to renewables, grids, storage, electrification, efficiency and low-emission fuels. Government support is also visible through the U.S. Department of Energy’s Energy Storage Grand Challenge, which accelerates next-generation storage commercialization, while IEA noted the program has issued 11 proposal calls since 2020.

In Europe, the Renewable Energy Directive targets 42.5% renewable energy in final consumption by 2030, which is expected to push around 70% renewable electricity in the power mix and create stronger demand for short- and long-duration storage. The EU Batteries Regulation also started new battery carbon-footprint and recycling rules from 2025, improving sustainability standards.

In 2025, General Electric’s energy business, GE Vernova, strengthened its grid and electrification position through a USD 5.275 billion agreement to fully acquire the Prolec GE joint venture, with closing expected by mid-2026. The deal supports transformer and grid capacity, which is critical for renewable storage integration. GE Vernova also continued positioning its Power Conversion & Storage business around energy conversion, storage systems, power stability and industrial electrification.

By Source Analysis

Hydroelectric dominates with 35.80% due to its established infrastructure, long-duration storage capability, and grid-scale energy balancing advantages.

In 2025, Hydroelectric held a dominant market position, capturing more than a 35.80% share in the Renewable Energy Storage Market by source. This leadership was supported by the strong integration of pumped hydro energy storage systems across utility-scale power networks and renewable energy projects. Hydroelectric storage continues to remain one of the most mature and commercially proven energy storage technologies, offering large-capacity electricity storage with long operational life and relatively low operating costs over time.

By Application Analysis

Commercial dominates with 47.80% as businesses continue investing in reliable energy storage to manage power demand and improve energy efficiency.

In 2025, Commercial held a dominant market position, capturing more than a 47.80% share in the Renewable Energy Storage Market by application. The segment maintained its leading position due to increasing adoption of energy storage systems across commercial buildings, office complexes, retail facilities, data centers, warehouses, and industrial-commercial campuses seeking greater energy reliability and lower electricity management costs.

Key Market Segments

By Source

- Wind

- Hydroelectric

- Solar

- Bio Energy

- Others

By Application

- Residential

- Industrial

- Commercial

- Utility-Scale

Emerging Trends

Utility-Scale Battery Storage Is Becoming the Biggest Latest Trend

Utility-scale battery storage has become one of the most important latest trends in the Renewable Energy Storage market. In 2025, around 108 GW of new battery storage capacity was deployed worldwide, which was 40% higher than 2024, showing how quickly storage is moving into mainstream power infrastructure.

The IEA also noted that installed battery storage capacity is now 11 times higher than in 2021, mainly because power grids need faster balancing support as solar and wind generation rise. LFP batteries are also gaining strong acceptance, accounting for nearly 90% of deployments, as they are generally cheaper and better suited for frequent charging and discharging.

Clean Energy Investment Is Pushing Storage Into Core Grid Planning

Another major trend is that governments and utilities are treating storage as a core part of clean energy planning, not just a backup solution. According to the IEA, total global energy investment is expected to reach USD 3.3 trillion in 2025, with around USD 2.2 trillion going into clean energy technologies such as renewables, grids, storage, low-emission fuels, efficiency, and electrification.

Battery storage investment has also grown sharply, rising from nearly USD 1 billion in 2015 to an expected USD 66 billion in 2025. This shift shows that storage is becoming essential for reducing renewable curtailment, managing peak demand, and improving grid reliability as more countries expand renewable power capacity.

Drivers

Rising Renewable Power Generation and Grid Stability Needs Are Accelerating Renewable Energy Storage Adoption

The rapid expansion of renewable electricity generation has become one of the strongest driving factors behind the Renewable Energy Storage market. As solar and wind installations continue to increase globally, energy systems require reliable storage infrastructure to balance supply fluctuations and maintain stable electricity delivery.

- According to the International Energy Agency (IEA), renewables are expected to meet more than 90% of global electricity demand growth between 2025 and 2030, while the renewable share in global electricity generation is projected to increase from 32% in 2024 to 43% by 2030.

Government-backed energy transition programs and infrastructure investments are also supporting storage deployment. The IEA reported that global spending on battery storage for the power sector is expected to reach USD 66 billion in 2025, reflecting how storage has moved from a supporting technology to a core part of modern energy systems. Battery storage is increasingly being paired with solar and wind projects to improve reliability, reduce curtailment, and strengthen energy security.

Large-Scale Storage Investments and Cost Improvements Continue to Strengthen Market Growth

Technology advancement and falling storage costs are creating another major growth engine for Renewable Energy Storage. According to IEA analysis, battery storage became the fastest-growing energy technology, with deployment more than doubling and adding 42 GW of battery storage capacity globally during the recent expansion phase. In parallel, lithium-ion battery prices declined from approximately USD 1,400 per kilowatt-hour in 2010 to below USD 140 per kilowatt-hour, improving project economics and accelerating commercial adoption.

Growth continued into 2025 as global battery storage deployment reached approximately 108 GW of new capacity, representing 40% growth compared with 2024 and making installed storage capacity nearly 11 times higher than 2021 levels. Storage systems are increasingly viewed as strategic infrastructure for integrating renewable power while reducing dependence on conventional generation sources.

Restraints

High Initial Investment and Critical Mineral Dependence Remain a Major Barrier for Renewable Energy Storage

One of the key restraining factors for the Renewable Energy Storage market is the high upfront investment required for storage infrastructure and the growing dependence on critical minerals used in battery manufacturing. Although renewable storage technologies continue to advance, project developers and utilities still face significant capital requirements for battery systems, grid integration, installation, and supporting infrastructure.

This challenge becomes more visible in large-scale deployments where project economics remain sensitive to financing conditions and raw material availability. According to the International Energy Agency (IEA), investment growth in critical mineral development slowed to only 5% in 2024, compared with 14% growth in 2023, while real investment growth after inflation was limited to just 2%, indicating increasing caution across supply chains.

Supply Chain Concentration and Raw Material Cost Risks Continue to Limit Expansion

Another major challenge for Renewable Energy Storage is the concentration of mineral refining and processing across limited regions, creating long-term supply risk. According to IEA analysis, raw materials currently account for approximately 50–70% of total lithium-ion battery costs, compared with 40–50% five years earlier, showing how mineral dependency has become increasingly important for storage economics. The agency further notes that a doubling of lithium or nickel prices can increase battery costs by around 6%, reducing cost advantages achieved through manufacturing scale.

- Recent IEA findings indicate that by 2035, the top three suppliers are expected to continue controlling around 82% of refined material supply, increasing vulnerability to trade restrictions, production interruptions, and price fluctuations.

Opportunity

Utility-Scale Energy Storage Expansion Creates a Strong Growth Opportunity for Renewable Energy Storage

One of the strongest growth opportunities for the Renewable Energy Storage market is the rapid expansion of utility-scale renewable projects combined with large-scale energy storage deployment. As electricity systems increase their reliance on solar and wind generation, utilities are investing in storage assets that can improve grid flexibility, reduce renewable curtailment, and maintain supply reliability during peak demand periods.

- According to the International Energy Agency (IEA), global renewable power capacity is expected to expand by more than 5,500 GW between 2024 and 2030, which is nearly equal to the total installed power capacity of major economies combined. This large renewable buildout directly increases the need for energy storage solutions that can balance intermittent generation and strengthen grid performance.

Battery Deployment and Grid Modernization Are Unlocking New Revenue Streams

Storage systems are increasingly being deployed to support energy trading, peak load management, ancillary grid services, and renewable optimization. These additional use cases are improving project economics and creating new revenue opportunities for operators. At the same time, governments and utilities are strengthening transmission networks to accommodate higher renewable penetration, which further increases the value of flexible storage assets.

Regional Insights

Asia-Pacific dominates the Renewable Energy Storage Market with a 36.20% share, reaching USD 20.6 Billion through rapid renewable expansion and grid-scale storage investments.

In 2025, Asia-Pacific held the dominant position in the Renewable Energy Storage Market, accounting for 36.20% of the global market and reaching a value of USD 20.6 Billion. The region maintained leadership due to continued expansion of renewable electricity generation, strong investment in grid modernization, and accelerated deployment of utility-scale energy storage systems. Growing electricity demand, industrial expansion, and long-term decarbonization strategies across major regional economies supported widespread adoption of storage technologies across utility, commercial, and distributed energy applications.

The region’s strong market position was supported by large renewable energy additions and supportive public investment programs. According to the International Energy Agency (IEA), Asia continues to lead global clean energy investment and renewable deployment, with major growth occurring across solar, wind, and integrated storage infrastructure. Increasing renewable penetration created a direct requirement for flexible storage systems capable of balancing intermittent generation and supporting grid reliability.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

General Electric continues to strengthen its role in the Renewable Energy Storage Market through grid modernization, renewable integration, and energy management solutions. Through its energy business operations, the company supports battery storage deployment and digital grid technologies for utility-scale applications. In recent years, GE expanded support for hybrid renewable projects combining storage with wind and solar assets. The company reported revenue exceeding USD 68 billion in 2025, while continuing investment in electrification and energy transition technologies to improve storage efficiency and grid flexibility.

Delta Electronics, Inc. remains active in renewable energy storage through battery energy storage systems, power conversion technologies, and energy infrastructure solutions. The company focuses on commercial and utility-scale energy optimization platforms that improve renewable integration. Delta reported annual revenue of approximately NTD 430 billion and continued investment in energy infrastructure and smart energy solutions. Its storage platforms support higher energy efficiency and improved electricity management across renewable installations.

Hitachi Ltd. supports the Renewable Energy Storage Market through grid automation, digital energy systems, and advanced storage integration technologies. The company’s energy portfolio emphasizes stable renewable adoption through intelligent energy management and transmission support. In fiscal 2025, Hitachi generated approximately JPY 9 trillion in revenue while expanding electrification and sustainable infrastructure initiatives. Its storage-related solutions continue supporting utilities transitioning toward flexible low-carbon energy networks.

Top Key Players Outlook

- General Electric

- Delta Electronics, Inc.

- Hitachi Ltd.

- Siemens AG

- Toshiba

- Trinasolar

- NextEra Energy Resources, LLC

- EVLO Energy Storage inc

- ABB

- HERO FUTURE ENERGIES

Recent Industry Developments

In 2026, Trina Storage reported 6 GWh of BESS orders across Europe, covering more than 65 projects since 2020. Its Elementa 2 Pro system also improved cell cycle life from 10,000 to 12,000 cycles, supporting stronger long-term storage performance. These moves show Trinasolar is shifting from a solar module supplier into a broader renewable energy storage player.

In 2025, Toshiba remained active in the Renewable Energy Storage sector through its SCiB™ lithium-ion battery and battery energy storage system work. The company showcased SCiB™ in 2025 with fast charging up to 80% in 6 minutes and more than 20,000 charge-discharge cycles, supporting storage use in renewable power, mobility, and industrial backup systems. Toshiba also began offering paid samples of its new SCiB™Nb battery in June 2025, with around 70% charge in 5 minutes and over 15,000 cycles, showing clear new product development.

In 2025, Toshiba remained active in the Renewable Energy Storage sector through its SCiB™ lithium-ion battery and battery energy storage system work. The company showcased SCiB™ in 2025 with fast charging up to 80% in 6 minutes and more than 20,000 charge-discharge cycles, supporting storage use in renewable power, mobility, and industrial backup systems. Toshiba also began offering paid samples of its new SCiB™Nb battery in June 2025, with around 70% charge in 5 minutes and over 15,000 cycles, showing clear new product development.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 57.0 Bn |

| Forecast Revenue (2035) | USD 234.1 Bn |

| CAGR (2026-2035) | 15.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source(Wind, Hydroelectric, Solar, Bio Energy, Others), By Application (Residential, Industrial, Commercial, Utility-Scale) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | General Electric, Delta Electronics, Inc., Hitachi Ltd., Siemens AG, Toshiba, Trinasolar, NextEra Energy Resources, LLC, EVLO Energy Storage inc, ABB, HERO FUTURE ENERGIES |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |