Quick Navigation

Report Overview

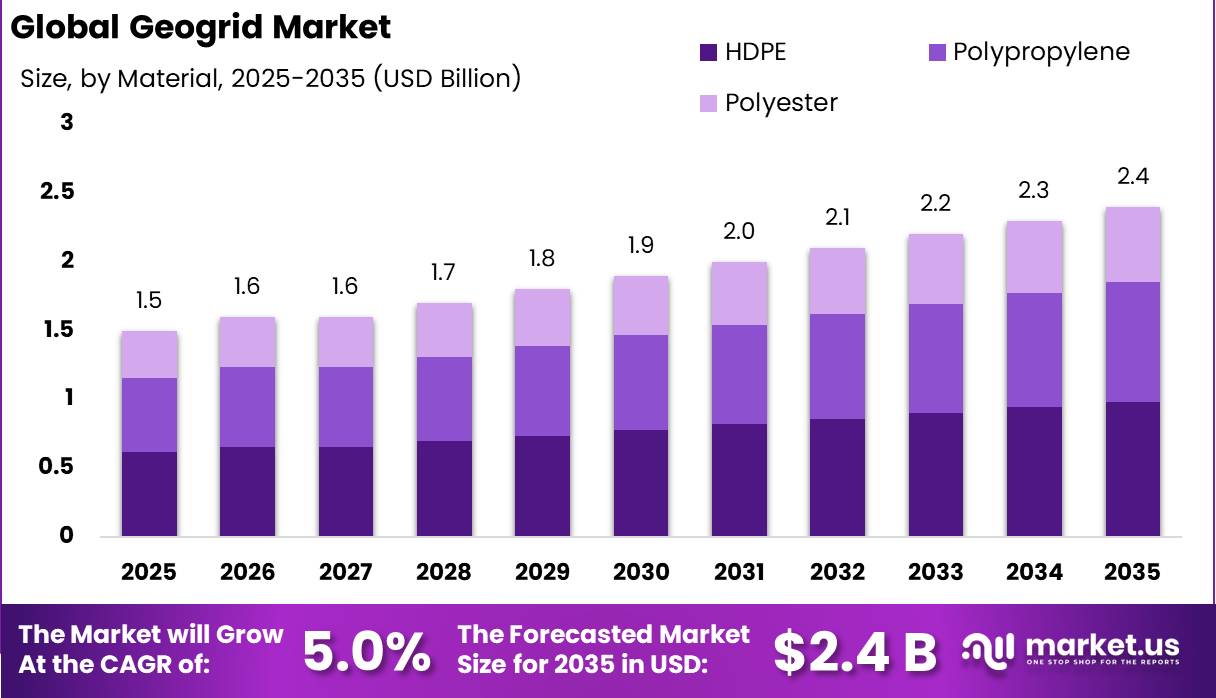

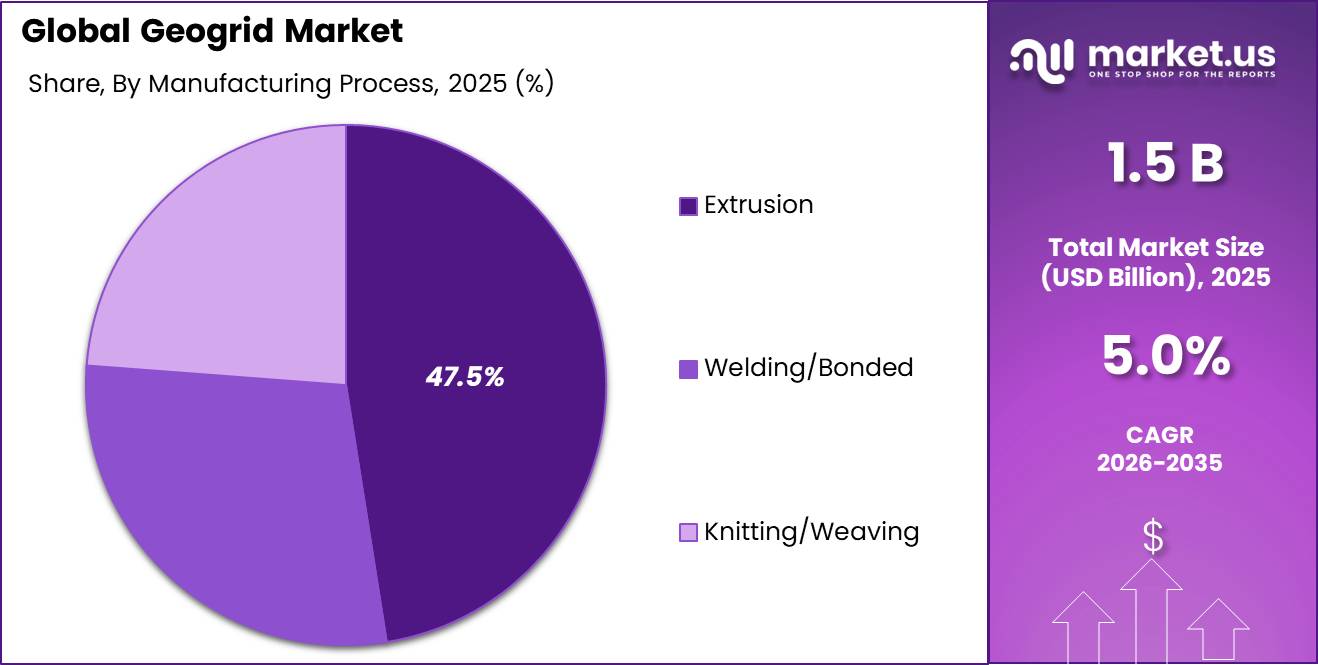

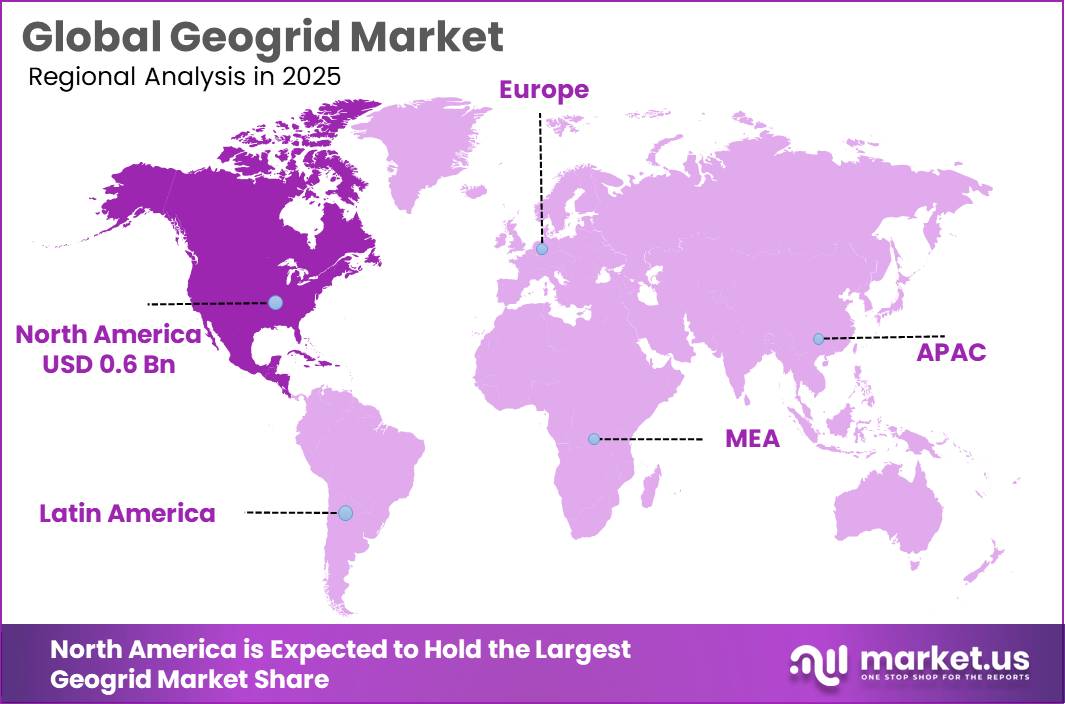

The Global Geogrid Market size is expected to be worth around USD 2.4 Billion by 2035, from USD 1.5 Billion in 2025, growing at a CAGR of 5.0% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 41.7% share, holding USD 0.6 Billion revenue.

Geogrids are entering a stronger industrial phase as infrastructure owners use polymer reinforcement to stabilize weak soils, reduce aggregate use, improve pavement life, and control erosion across roads, rail, ports, energy sites, landfills, and agricultural access infrastructure. Demand is supported by global soil and resilience pressures: FAO states that 95% of food comes from soil, 33% of Earth’s soils are already degraded, and erosion can cut crop yields by up to 50%.

Key Takeaways

- Geogrid Market size is expected to be worth around USD 2.4 Billion by 2035, from USD 1.5 Billion in 2025, growing at a CAGR of 5.0%.

- HDPE held a dominant market position, capturing more than a 40.90% share in the geogrid market.

- Uniaxial held a dominant market position, capturing more than a 44.20% share in the geogrid market

- Extrusion held a dominant market position, capturing more than a 47.50% share in the geogrid market.

- Road construction held a dominant market position, capturing more than a 48.30% share in the geogrid market.

- North America held a dominant position in the global geogrid market, accounting for 41.70% of total market share and reaching a market value of USD 0.6 Billion.

The industrial scenario is increasingly shaped by climate-resilient construction rather than only cost saving. OECD, World Bank and UN Environment analysis estimates that USD 6.9 trillion per year in infrastructure investment is needed by 2030 for SDG- and Paris-aligned infrastructure. In Europe, soil erosion is estimated at 1 billion tonnes per year, with 24% of soils affected by water erosion and 32% of agricultural land facing unsustainable erosion, creating a strong policy case for erosion-control and ground-stabilization materials.

Driving factors include road rehabilitation, rail modernization, renewable-energy access roads, landfill expansion, slope protection, and lower-carbon construction. Tensar states that its InterAx geogrid was developed by 12 global teams with over 10,000 R&D hours, while its sustainability claims focus on reducing aggregate extraction, transport, excavation, and construction emissions. Tensar also reports geogrid applications across public roads, ports, railways, energy, airports, waste, mining, walls, slopes, and marine works.

Government initiatives are likely to support future opportunities. The U.S. Infrastructure Investment and Jobs Act invests USD 350 billion in highway programs over 5 years through FY2026, supporting bridge, road, safety, and resilience work where geogrids can be specified for subgrade stabilization. The European Commission also selected 94 transport projects for nearly EUR 2.8 billion in Connecting Europe Facility grants in 2025, focused on railways, inland waterways, maritime routes, and TEN-T resilience.

In 2025, HUESKER Group completed the acquisition of Sineco International, effective April 3, 2025, strengthening its drainage, dewatering, and erosion-control portfolio; industry coverage also noted wider 2025 HUESKER investments including NaBento production restart and expansion of Dülmen production facilities.

By Material Analysis

HDPE dominates with 40.90% share due to its strong durability and broad use in reinforcement applications

In 2025, HDPE held a dominant market position, capturing more than a 40.90% share in the geogrid market by material. This leadership was supported by the material’s strong balance of durability, flexibility, and cost efficiency across a wide range of civil engineering and infrastructure projects. HDPE geogrids continued to see steady demand in road construction, retaining walls, railway stabilization, landfill systems, and soil reinforcement applications where long-term performance is important.

By Product Analysis

Uniaxial dominates with 44.20% share driven by its strong performance in soil reinforcement and retaining structures

In 2025, Uniaxial held a dominant market position, capturing more than a 44.20% share in the geogrid market by product. Its leading position was mainly supported by growing use in applications that require reinforcement strength in a single direction, especially in retaining walls, steep slopes, embankments, and foundation stabilization projects. Uniaxial geogrids remained a preferred choice because of their ability to handle high tensile loads while improving soil stability and structural support over long periods.

By Manufacturing Process Analysis

Extrusion dominates with 47.50% share supported by efficient production and consistent product performance

In 2025, Extrusion held a dominant market position, capturing more than a 47.50% share in the geogrid market by manufacturing process. The segment maintained its leadership due to its ability to produce geogrids with consistent strength, structural uniformity, and reliable long-term performance across demanding construction environments. Extrusion remained widely adopted because it allows manufacturers to create durable geogrid structures through a streamlined production process while supporting large-scale output requirements.

By Application Analysis

Road construction dominates with 48.30% share due to growing infrastructure development and long-term pavement performance

In 2025, Road construction held a dominant market position, capturing more than a 48.30% share in the geogrid market by application. This leading position was supported by increasing demand for durable and cost-efficient transportation infrastructure across urban and regional development projects. Geogrids continued to play an important role in road construction by improving load distribution, strengthening weak subgrades, and extending pavement life.

Key Market Segments

By Material

- HDPE

- Polypropylene

- Polyester

By Product

- Uniaxial

- Biaxial

- Triaxial

By Manufacturing Process

- Knitting/Weaving

- Welding/Bonded

- Extrusion

By Application

- Road construction

- Railroad

- Soil Reinforcement

- Others

Emerging Trends

Low-Carbon and Material-Efficient Construction is Becoming a Major Geogrid Trend

One of the latest trends shaping the geogrid industry is the move toward low-carbon and material-efficient construction. Across the building and infrastructure sector, project owners are no longer focusing only on strength and speed—they are also looking at how much material is consumed and how much carbon is created during construction.

Geogrids are increasingly being selected because they help improve soil performance while reducing the amount of aggregate and excavation needed. Recent engineering research published in 2025 showed that geogrid-reinforced pavement structures can reduce asphalt layer thickness by 15–30% and granular layer thickness by 20–30%, depending on ground conditions. The same study found that geogrid use lowered embodied carbon by 6–24% across different soil categories.

Construction Projects are Moving Toward Longer-Life Infrastructure Solutions

Another clear trend is the growing preference for infrastructure systems that last longer and require fewer repairs. In construction today, durability is becoming as important as upfront cost. Geogrids are being used to strengthen foundations, stabilize roads, and support earth structures in ways that reduce maintenance over time.

According to sustainability project examples published by Tensar, geogrid-supported infrastructure solutions achieved an estimated 57% reduction in environmental cost and around 80,000 kg CO₂e savings in a road project. Another infrastructure application recorded an estimated 75% reduction in carbon emissions, 75% faster construction time, and 65% lower construction cost compared with conventional methods.

Drivers

Rising Infrastructure Development and Road Modernization Continue to Drive Demand for Geogrids

Geogrids are seeing stronger demand because governments and infrastructure agencies are investing more in building and upgrading roads, transport corridors, and public infrastructure. As road networks expand and construction standards become more focused on durability, materials that improve soil stability and extend pavement life are becoming more important. Geogrids help reduce ground movement, improve load distribution, and lower long-term maintenance requirements, making them a practical solution in modern infrastructure projects.

According to OECD transport infrastructure data, road infrastructure continues to receive a major share of public infrastructure investment across many economies. In 2015, spending on new roads exceeded 0.5% of national GDP in 15 out of 32 OECD countries, and crossed 1% in countries such as Estonia, Hungary, and Korea. This reflects the continued priority given to transportation networks and road expansion.

Government Infrastructure Programs and Long-Term Asset Performance Support Geogrid Adoption

Government-led infrastructure programs are also creating favorable conditions for geogrid usage. Public authorities are placing greater emphasis on improving asset life while reducing future repair costs. Since geogrids strengthen weak soil and improve structural performance, they are becoming a preferred reinforcement material in transport and land development projects.

According to the World Bank, transportation and water-related projects approved under infrastructure programs reached USD 5.71 billion in FY2024 through IBRD and IDA operations. In addition, OECD estimates highlighted that total global infrastructure investment requirements across transport, energy, water, and telecommunications are expected to reach USD 71 trillion by 2030, showing the scale of future construction demand.

Restraints

High Construction Material Costs and Budget Pressure Limit Wider Geogrid Adoption

One of the major restraining factors for the geogrid market is the rising cost of construction materials and increasing project budget pressure. Although geogrids help improve long-term infrastructure performance and reduce maintenance needs, their adoption can become challenging when contractors and developers focus heavily on controlling upfront project expenses.

According to recent construction industry insights, construction material prices increased by around 2.1%–2.5% year-over-year in 2025 and remained significantly above pre-pandemic levels across several key building materials including concrete, steel products, and other structural inputs. Higher material costs create pressure across the full construction value chain and often delay the adoption of advanced reinforcement solutions. When budgets tighten, project owners may postpone investments in engineered materials despite their long-term operational benefits.

Infrastructure Cost Management and Regulatory Challenges Slow Project-Level Decisions

Another factor restricting geogrid growth is the increasing complexity of infrastructure cost management and project approval processes. Construction projects today are under stronger pressure to balance cost, compliance, and performance targets. While geogrids can improve structural efficiency, the additional design assessment, material selection process, and approval timelines may slow implementation in some projects.

According to World Bank studies on construction and infrastructure development, periods of unusually high demand for infrastructure and industrial projects have historically created market premiums of nearly 15 percentage points above normal material, equipment, and labor escalation levels. This cost pressure directly affects procurement decisions and project timelines. Governments continue supporting resilient infrastructure development through stronger construction standards and regulatory frameworks, but budget constraints still influence technology selection during execution stages.

Opportunity

Growth in Road and Transport Infrastructure

One major growth opportunity for geogrid is the rising investment in road and transport infrastructure. Geogrids help strengthen weak soil, reduce aggregate use, and improve the life of roads, working platforms, and rail foundations. This matters because governments are spending heavily on long-life transport assets. In the U.S., the Federal Highway Administration says the Infrastructure Investment and Jobs Act provides $350 billion for highway programs over 5 years.

In Europe, the European Commission selected 94 transport projects for nearly €2.8 billion in Connecting Europe Facility grants in 2025. These projects support railways, inland waterways, maritime routes, and connected mobility. As construction owners look for faster building methods and lower maintenance costs, geogrid use can grow in road bases, embankments, retaining walls, and access routes.

Opportunity from Cost and Material Savings

Geogrid also has a strong opportunity because it can reduce material use while improving ground performance. Tensar states that its subgrade stabilization solution can reduce aggregate volumes by up to 50% compared with traditional capping layer or subbase designs. This is important at a time when contractors face pressure to cut transport, quarrying, fuel use, and project delays.

The UK’s official infrastructure pipeline shows about £718 billion of planned capital investment over the next 10 years, including £252 billion publicly financed and £466 billion delivered through private or mixed financing. Such large construction pipelines create room for geogrids in roads, energy sites, logistics parks, airports, and heavy-duty working areas.

Regional Insights

North America dominated the Geogrid Market with a 41.70% share, accounting for USD 0.6 Billion due to strong infrastructure investment and road modernization activities

In 2025, North America held a dominant position in the global geogrid market, accounting for 41.70% of total market share and reaching a market value of USD 0.6 Billion. The region maintained its leadership due to continuous investment in transportation infrastructure, road rehabilitation programs, and growing demand for advanced ground stabilization solutions across construction projects. The widespread use of geogrids in road construction, retaining walls, embankments, and soil reinforcement applications supported consistent market demand throughout the region.

The United States remained the primary contributor to regional growth, supported by large-scale infrastructure development and increasing focus on extending the service life of roads and highways. Public infrastructure initiatives and funding programs continued to encourage the use of durable construction materials that improve structural performance while reducing long-term maintenance costs. Geogrids gained wider acceptance because they help strengthen weak soil conditions, improve load-bearing capacity, and lower lifecycle expenses in infrastructure projects.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Tensar International Corporation is recognized as one of the earliest developers and commercial pioneers of geogrid technology for soil reinforcement and ground stabilization applications. The company operates with 600+ employees globally, maintains offices across 10+ countries, and supports infrastructure projects through engineering-led design solutions. Tensar’s innovation profile is supported by 115 patents across geogrid and related technologies and includes extensive full-scale performance testing. Recent validation studies included 20 full-scale bearing-capacity tests with loading conditions ranging from 198 kN to 950 kN, reinforcing its technical positioning in road, foundation, and working-platform applications.

HUESKER Synthetic GmbH is a long-established geosynthetics manufacturer with operations spanning geogrids, geotextiles, environmental engineering, mining, hydraulic engineering, and infrastructure reinforcement. Founded in 1861, the company has more than 160 years of industrial history. Historical records show operations reached 1,172 looms and 613 employees as early as 1913, demonstrating early manufacturing scale. HUESKER serves multiple global markets and is structured across 7 business areas, supplying engineered reinforcement solutions for roads, foundations, environmental works, and industrial applications.

Top Key Players Outlook

- Tensar International Corporation (US)

- Huesker Synthetic GmbH (DE)

- Strata Systems, Inc. (U.S.)

- Maccaferri Inc. (U.S.)

- NAUE GMBH & CO. KG. (Germany)

- GSE Environmental (U.S.)

- BOSTD Geosynthetics Qingdao Ltd. (China)

- TENAX Corporation (U.S.)

- ACE Geosynthetics (TW)

- S i A Pietrucha Sp. z o.o. (Poland)

- Strata Systems, Inc.

Recent Industry Developments

In 2025, ACE Geosynthetics continued to build its geogrid position through product development, project work, and international expansion rather than any widely reported merger or acquisition. The company, established in 1996, exports to more than 70 countries and works with more than 40 engineering experts. In geogrids, its ACEGrid® GN product offers tensile strength of 20 kN/m to 1000 kN/m in uniaxial grades and 10 kN/m to 300 kN/m in biaxial grades.

In 2026, NAUE supplied about 150,000 m² of Combigrid® and Secugrid® for a port development project, supporting soft ground stabilization linked to renewable energy infrastructure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.5 Bn |

| Forecast Revenue (2035) | USD 2.4 Bn |

| CAGR (2026-2035) | 5.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (HDPE, Polypropylene, Polyester), By Product (Uniaxial, Biaxial, Triaxial), By Manufacturing Process (Knitting/Weaving, Welding/Bonded, Extrusion), By Application (Road construction, Railroad, Soil Reinforcement, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Tensar International Corporation, Huesker Synthetic GmbH, Strata Systems, Inc., Maccaferri Inc., NAUE GMBH & CO. KG., GSE Environmental, BOSTD Geosynthetics Qingdao Ltd., TENAX Corporation, ACE Geosynthetics, S i A Pietrucha Sp. z o.o., Strata Systems, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |