Quick Navigation

Report Overview

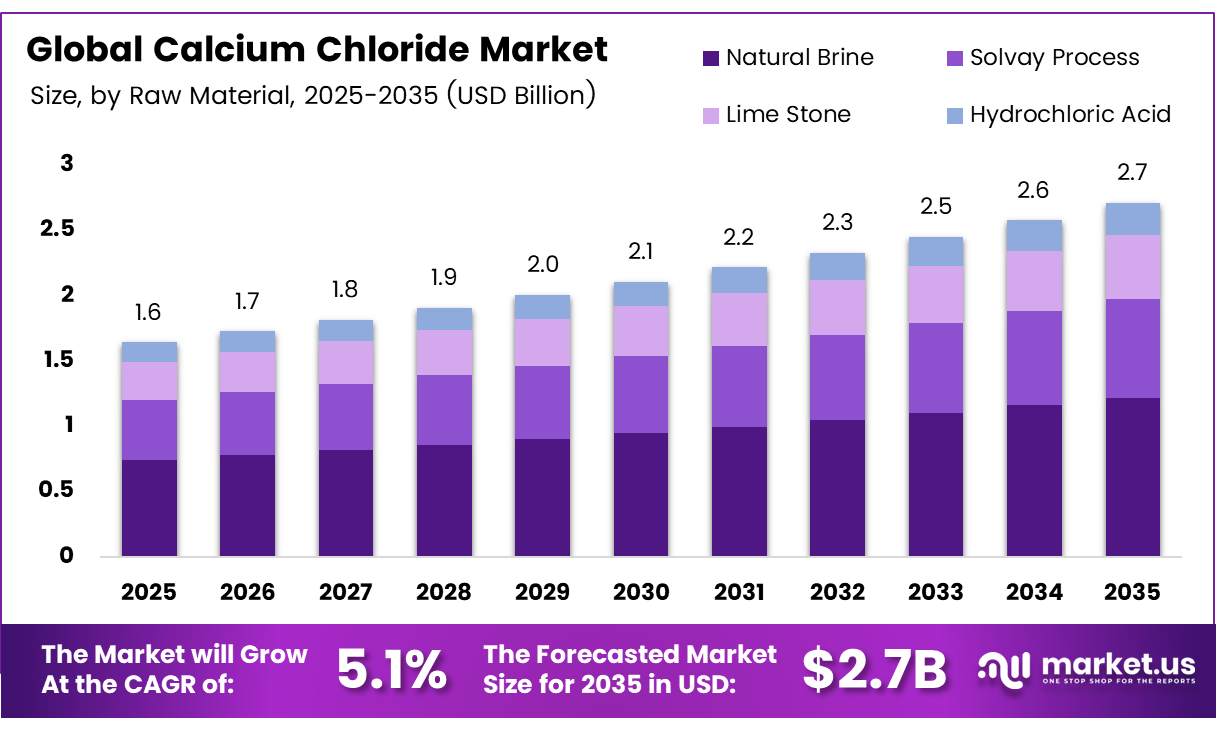

The Global Calcium Chloride Market size is expected to be worth around USD 2.7 billion by 2035 from USD 1.6 billion in 2025, growing at a CAGR of 5.1% during the forecast period 2026 to 2035.

Calcium chloride is an inorganic salt with a broad industrial footprint spanning de-icing, oil and gas well completion, dust suppression, construction acceleration, and food preservation. Its hygroscopic properties and exothermic dissolution behavior make it irreplaceable in cold-climate infrastructure and oilfield operations. No single substitute matches its performance across this range of end uses.

De-icing and dust control applications anchor the largest share of volume consumption, particularly across North American highway networks, airports, and mining haul roads. However, oil and gas drilling fluids represent the highest-value end use, where formulation precision and fluid density directly affect wellbore stability. This dual demand base insulates the market from single-sector downturns.

DOWFLAKE Xtra contains at least 83% calcium chloride — about 10% higher than standard 77%–80% flakes — helping reduce logistics and application costs. A 28% calcium chloride solution provides freeze protection down to -46°F, making it the preferred choice for municipal and airport de-icing in extreme winter conditions.

Industrial consumption of calcium chloride extends into concrete acceleration, where fast-setting requirements in cold-weather construction drive consistent demand. Food-grade applications in processed foods, beverages, and industrial refrigeration add a non-cyclical revenue layer. Together, these end uses create a demand profile that is both broad and structurally stable.

Pharmaceutical and water treatment applications represent a structural diversification away from weather-sensitive demand. As developing economies scale wastewater management infrastructure and adopt calcium chloride in medical formulations, the market gains new volume that does not correlate with seasonal de-icing cycles. This broadens the addressable revenue base well beyond its traditional industrial core.

Key Takeaways

- The Global Calcium Chloride Market is valued at USD 1.6 billion in 2025 and forecast to reach USD 2.7 billion by 2035 at a CAGR of 5.1% during the forecast period 2026 to 2035.

- Hydrated Solid leads with a 47.7% market share in 2025.

- Natural Brine holds the dominant position with a 51.2% share.

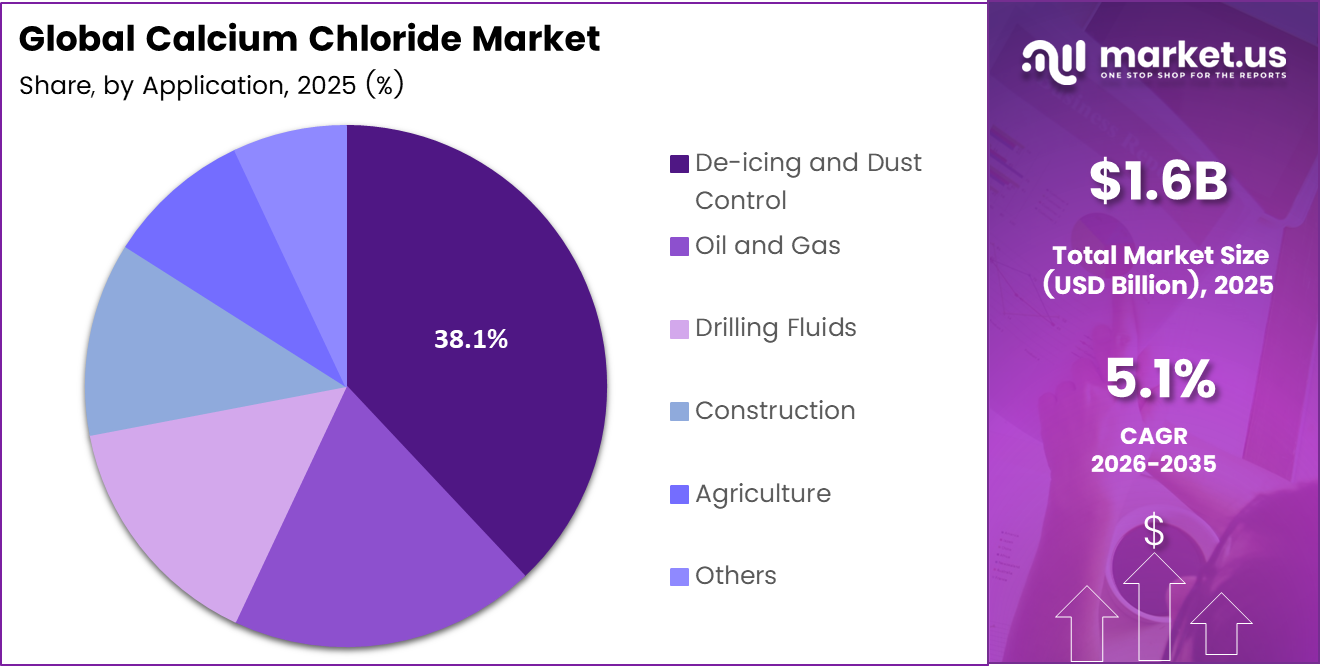

- De-icing and Dust Control accounts for the largest share at 38.1%.

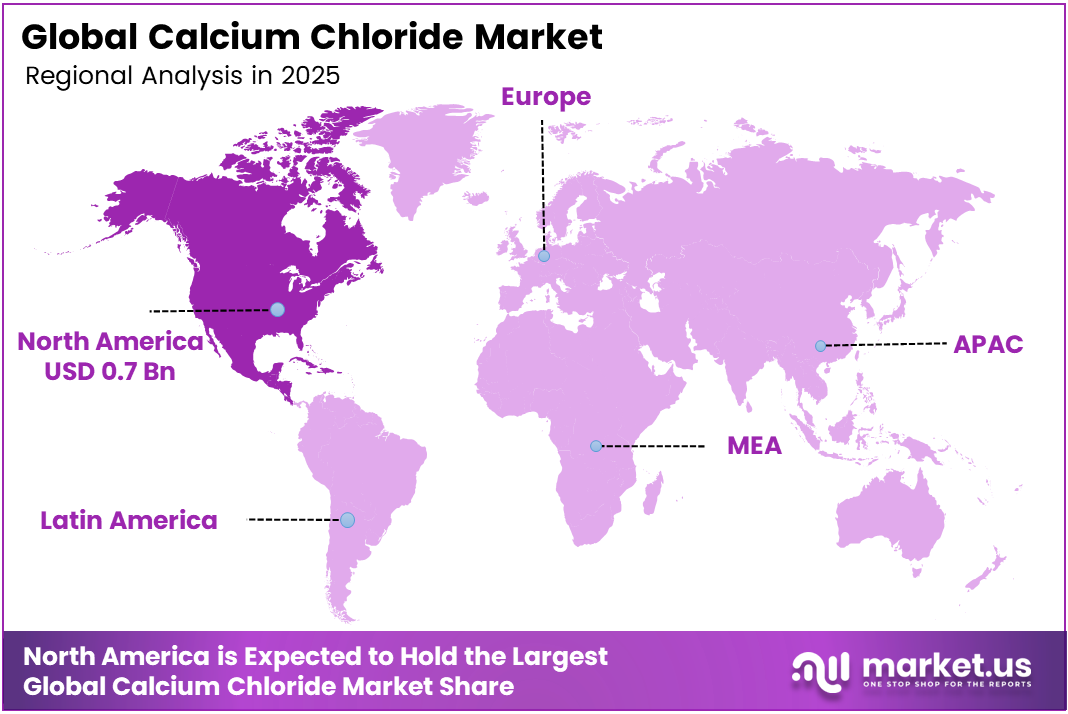

- North America dominates regional demand, holding a 41.4% share valued at approximately USD 0.7 billion.

Form Analysis

Hydrated Solid dominates with 47.7% due to ease of handling, storage, and precise dosing.

In 2025, Hydrated Solid held a dominant market position in the By Form segment of the Calcium Chloride Market, with a 47.7% share. Solid flake and pellet formats offer longer shelf life, easier bulk transport, and established application protocols across de-icing, construction, and industrial desiccation. These handling advantages make hydrated solids the default procurement choice for buyers managing large, distributed operations.

Liquid calcium chloride serves as the operationally preferred format for large-scale, continuous applications where manual spreading is impractical. Pre-diluted solutions eliminate on-site mixing, reduce application time, and enable precise coverage rates. Municipalities and mining operators favor liquid formats for highway dust control and anti-icing pre-treatment, especially when deploying automated spray equipment across extended road networks.

Raw Material Analysis

Natural Brine dominates with 51.2% due to low extraction cost and abundant availability.

In 2025, Natural Brine held a dominant market position in the By Raw Material segment of the Calcium Chloride Market, with a 51.2% share. Brine extraction delivers calcium chloride at lower energy and capital cost compared to synthetic routes, making it structurally competitive across commodity-grade applications. Regions with large underground brine deposits — particularly in North America — give domestic producers a sustained cost advantage over import alternatives.

Solvay Process routes produce calcium chloride as a co-product of soda ash manufacturing. This positions Solvay-derived supply as inherently volume-linked to soda ash demand cycles. When soda ash production scales, calcium chloride output increases regardless of direct market demand — a structural quirk that periodically pressures spot pricing and complicates long-term supply planning for buyers.

Application Analysis

De-icing and Dust Control dominate with 38.1% due to mandatory winter road maintenance requirements.

In 2025, De-icing and Dust Control held a dominant market position in the By Application segment of the Calcium Chloride Market, with a 38.1% share. Cold-climate regulations mandate road treatment performance standards that calcium chloride satisfies more effectively than rock salt at low temperatures. This regulatory compulsion, combined with recurring seasonal demand, creates a non-discretionary procurement cycle that underpins consistent volume consumption year over year.

Oil and Gas applications use calcium chloride primarily in completion fluids, packer fluids, and workover operations. Density-adjustable brine systems allow wellbore pressure management without formation damage. Demand in this segment tracks closely with upstream drilling activity and rig count, making it the most cyclical application in the portfolio but also the highest value per unit volume.

Key Market Segments

By Form

- Hydrated Solid

- Liquid

- Others

By Raw Material

- Natural Brine

- Solvay Process

- Lime Stone

- Hydrochloric Acid (HCL)

By Application

- De-icing and Dust Control

- Oil and Gas

- Drilling Fluids

- Construction

- Agriculture

- Others

Emerging Trends

High-Purity Formulations and Sustainable Production Redefine Calcium Chloride Supply Standards

Manufacturers are shifting production toward high-purity and food-grade calcium chloride grades to serve specialty industrial, pharmaceutical, and food processing markets. Standard commodity output no longer satisfies regulatory specifications in these segments. WellCal brine fluids meet turbidity below 20 NTU and iron below 10 ppmw — illustrating how tightly buyers specify quality parameters in premium applications.

Liquid calcium chloride formulations gain preference in large-scale municipal and industrial operations because automated spray systems require consistent solution properties. Producers supplying liquid grades at verified concentrations and densities secure long-term supply agreements with infrastructure agencies.

Sustainable manufacturing investment accelerates as buyers and regulators scrutinize the carbon footprint of chemical production. Chemical manufacturers pursue strategic collaborations with infrastructure agencies to lock in multi-year contracts, providing volume predictability that justifies capital investment in lower-emission production processes.

Drivers

Oil and Gas Drilling Demand and Cold-Climate Infrastructure Mandates Sustain Calcium Chloride Volume Growth

Calcium chloride demand in oilfield operations remains structurally anchored by its role in completion fluids, workover operations, and hydraulic fracturing. Oil and gas operators require density-controlled brines that protect formations while maintaining wellbore pressure. Calcium chloride concrete acceleration can reduce concrete set time by as much as two-thirds — a performance benefit that directly reduces construction project cycle time and labor cost in cold-weather operations.

Road maintenance agencies across cold-climate regions designate calcium chloride as a primary de-icing agent because its performance at sub-zero temperatures exceeds alternatives. Mining operations specify calcium chloride for haul road dust suppression to protect equipment and comply with air quality standards. Both end uses generate non-discretionary, contract-based purchasing cycles that provide stable volume regardless of broader economic conditions.

Food-grade calcium chloride consumption expands alongside processed food production and industrial refrigeration infrastructure. Beverage manufacturers and food processors use it for preservation, firmness control, and pH management across regulated food supply chains. This non-cyclical demand layer complements weather-sensitive and energy-sector volumes, strengthening the overall demand base for producers competing across multiple end-use markets simultaneously.

Restraints

Raw Material Cost Volatility and Environmental Concerns Create Structural Pressure on Producer Margins

Calcium chloride production depends on raw material inputs — brine extraction, soda ash co-production, and HCl availability — all of which carry independent price volatility. Energy costs compound this exposure, as evaporation and processing steps are energy-intensive.

Ready-to-use calcium chloride deicer costs 3–8 times more per lane mile than salt brine and approximately 6 times more than granular salt. This cost differential restricts widespread adoption among budget-constrained municipal buyers. It forces procurement decisions toward cheaper alternatives in regions where performance differentiation at extreme temperatures is less critical.

Environmental and corrosion concerns associated with excessive calcium chloride application on roads and bridges create regulatory scrutiny and reputational risk. Runoff into waterways affects aquatic ecosystems, and chloride accelerates corrosion on vehicles, infrastructure, and reinforcing steel.

Growth Factors

Water Treatment Infrastructure, Pharmaceutical Adoption, and Smart City Investment Open New Revenue Channels

Water treatment facilities and wastewater management infrastructure represent a structural expansion opportunity for calcium chloride suppliers. Liquid calcium chloride products are supplied in 28%–42% concentrations — a formulation range that matches the dosing flexibility water treatment operators require across variable source water quality conditions.

Pharmaceutical manufacturers in developing economies increasingly incorporate calcium chloride into intravenous solutions, electrolyte formulations, and diagnostic reagents. As healthcare infrastructure scales across Asia Pacific, Latin America, and parts of Africa, regulated-grade demand for calcium chloride rises independent of industrial or seasonal cycles.

Smart city infrastructure programs drive sustained procurement for dust control, surface stabilization, and concrete acceleration in urban construction. Governments committing to long-term infrastructure development plans generate multi-year demand visibility that justifies capacity expansion by calcium chloride producers.

Regional Analysis

North America Dominates the Calcium Chloride Market with a Market Share of 41.4%, Valued at USD 0.7 Billion

North America holds a 41.4% share of the global calcium chloride market, valued at approximately USD 0.7 billion in 2025. Cold-climate road maintenance regulations, a dense highway network, and a mature oilfield services industry create compounding demand across the region’s two largest application segments simultaneously.

Europe sustains consistent calcium chloride consumption through established de-icing procurement programs in northern and central countries, combined with a developed food processing and pharmaceutical manufacturing base. Regulatory frameworks around road safety and chemical production quality push buyers toward certified, traceable supply chains.

Asia Pacific represents the fastest-expanding geographic market for calcium chloride, driven by large-scale construction activity, growing oilfield operations, and expanding food processing industries across China, India, and Southeast Asia. Infrastructure investment programs in China and India generate sustained demand for concrete acceleration and dust control.

The Middle East drives calcium chloride demand primarily through oilfield completion fluid requirements, where the region’s active upstream drilling programs consume substantial brine volumes. Gulf Cooperation Council countries invest heavily in water treatment and industrial infrastructure, creating incremental demand beyond oilfield applications.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Occidental Petroleum Corp. anchors its calcium chloride business through vertically integrated brine extraction and a diversified product portfolio spanning de-icing, oilfield brines, and food-grade formulations. Its direct access to large underground brine reserves gives it a structural feedstock cost advantage. This vertical integration allows Occidental to compete on both price and specification across commodity and premium application segments simultaneously.

Tetra Technologies, Inc. positions itself as a specialized oilfield completion fluid provider with deep technical expertise in calcium chloride brine formulation. Its focus on high-density clear brine fluids for well completion and workover operations targets the highest-value segment in the market. This specialization insulates Tetra from price competition in commodity de-icing markets while aligning it directly with upstream oil and gas investment cycles.

B. J. Services competes in the oilfield services segment, where calcium chloride functions as a critical input for hydraulic fracturing and completion operations. Its established relationships with upstream operators provide contracted volume visibility that reduces revenue exposure to spot market fluctuations. Service integration — combining chemical supply with application expertise — raises the switching cost for operator clients.

Solvay S.A. produces calcium chloride primarily as a by-product from its soda ash manufacturing operations. This structural position means Solvay’s calcium chloride output scales with soda ash demand, providing inherent cost efficiency but introducing volume correlation risk. Solvay’s chemical manufacturing expertise and global distribution infrastructure allow it to serve regulated food-grade and pharmaceutical applications where product certification is a prerequisite for market entry.

Key Players

- Occidental Petroleum Corp.

- Tetra Technologies, Inc.

- B. J. Services

- Solvay S.A.

- Tangshan Sanyou Group Co., Ltd.

- Qingdao Huadong Calcium Producing Co., Ltd.

- Tiger Calcium Services

- Ward Chemicals

- Weifang Haibin Chemical Co., Ltd

- Weifang Taize Chemical Industry Co., Ltd

- Zirax Ltd

Recent Developments

- In Oct. 2025, OxyChem remains a major calcium chloride player: its site says it is the world’s largest producer of calcium chloride, used in ice control, dust suppression, road stabilization, oilfield services, agriculture, water treatment, refrigeration, and industrial processing. Occidental announced it would sell OxyChem to Berkshire Hathaway, a major ownership change affecting the calcium chloride business.

- In 2025, TETRA’s Form 10-K says its Completion Fluids & Products segment manufactures liquid and dry calcium chloride, with facilities in the U.S. and Finland, and about 1.0 million equivalent liquid tons/year calcium chloride production capacity. It also says calcium chloride products serve energy plus water treatment, industrial, cement, food processing, road maintenance, ice melt, agricultural, and consumer markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.6 Billion |

| Forecast Revenue (2035) | USD 2.7 Billion |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Hydrated Solid, Liquid, Others), By Raw Material (Natural Brine, Solvay Process, Lime Stone, Hydrochloric Acid (HCL)), By Application (De-icing and Dust Control, Oil and Gas, Drilling Fluids, Construction, Agriculture, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Occidental Petroleum Corp., Tetra Technologies, Inc., B. J. Services, Solvay S.A., Tangshan Sanyou Group Co., Ltd., Qingdao Huadong Calcium Producing Co., Ltd., Tiger Calcium Services, Ward Chemicals, Weifang Haibin Chemical Co., Ltd., Weifang Taize Chemical Industry Co., Ltd., Zirax Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |