Quick Navigation

Report Overview

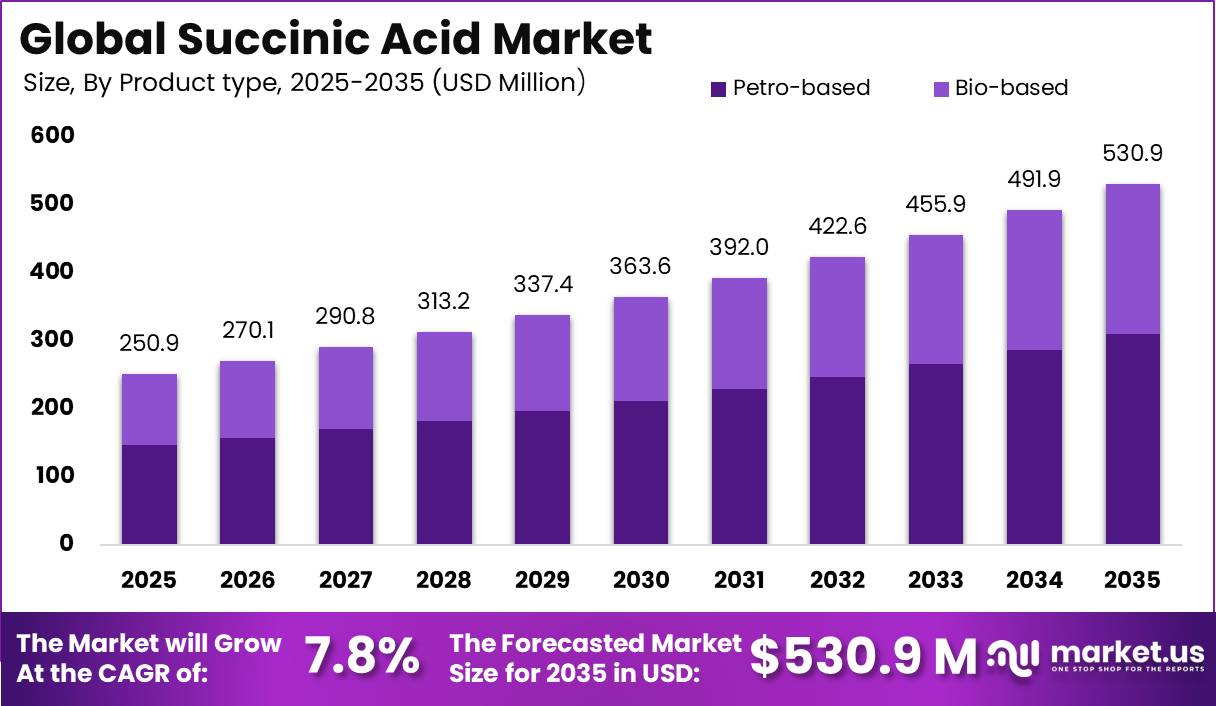

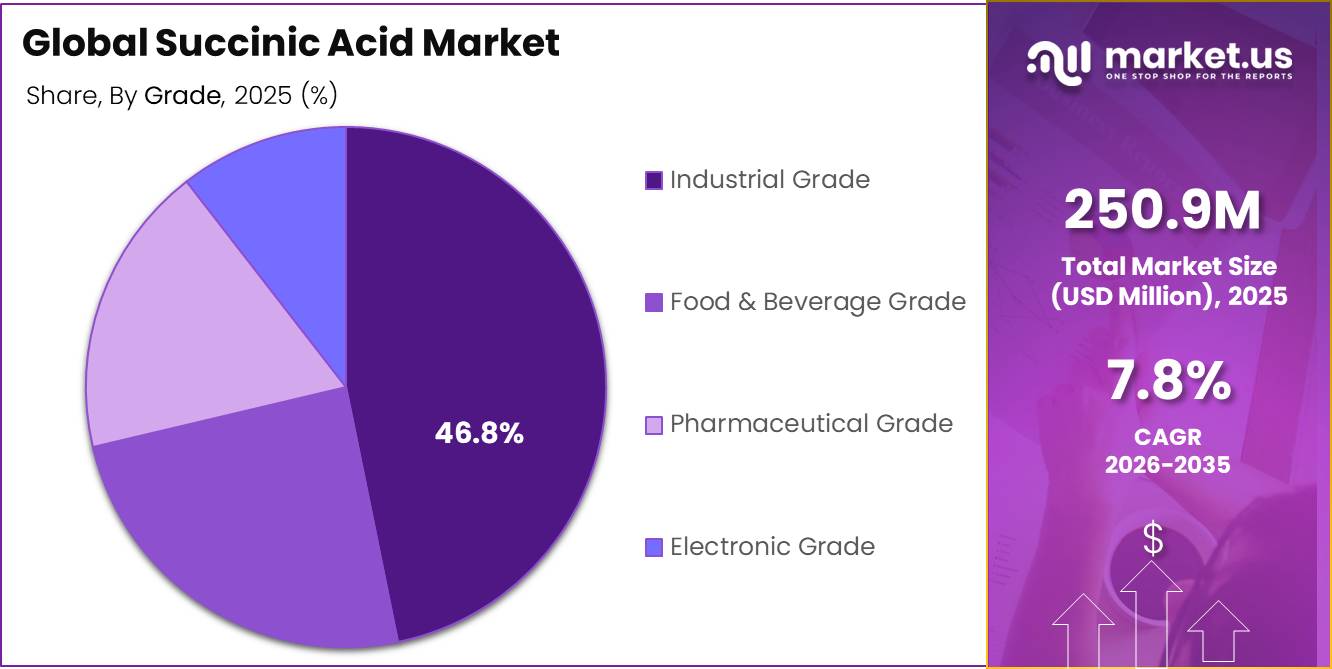

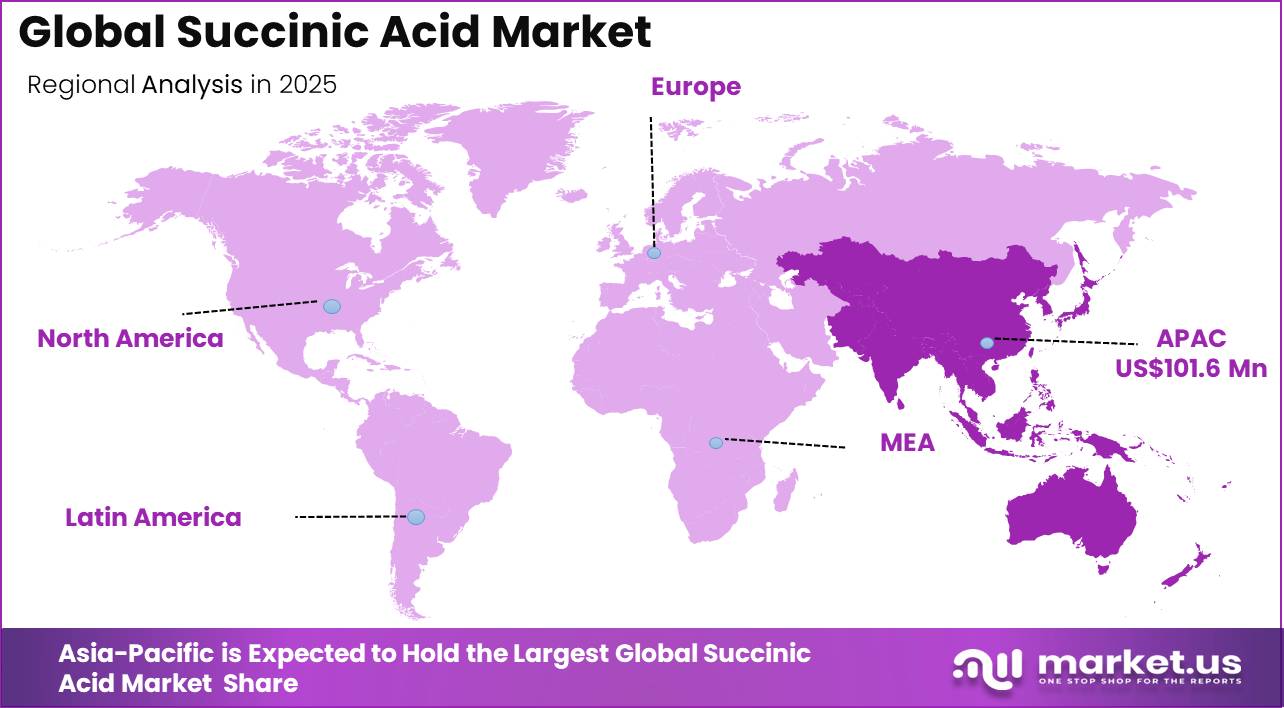

The Global Succinic Acid Market was valued at USD 250.9 Million, and between 2026 and 2035, this market is estimated to register a CAGR of 7.8%, reaching about USD 530.9 Million by 2035. Asia Pacific held a dominant market position, capturing more than a 40.5% share, holding USD 101.6 Million in revenue.

The European Commission’s July 2025 Chemicals Industry Action Plan identified bio-based feedstocks as meaningful alternatives to fossil carbon inputs, positioning renewable chemical intermediates as strategically important to maintaining the EU’s industrial resilience and competitiveness across sectors contributing to over 96% of manufactured goods.

It functions as a key building block for biodegradable polymers, polyurethane dispersions, coating resins, phthalate-free plasticisers, and food-grade additives, while also serving pharmaceutical formulation and personal care markets. Demand is structurally anchored by expanding biodegradable materials adoption, tightening environmental regulations on petrochemical-derived intermediates, and rising corporate sustainability commitments across downstream manufacturing sectors.

Asia Pacific leads succinic acid production, while Europe and North America drive demand for certified bio-based and speciality grades. Innovation focuses on fermentation, waste-based feedstocks, and sustainability certification. Succinic acid remains an important platform chemical used across industrial, pharmaceutical, and consumer applications.

Key Takeaways

- The global Succinic Acid market was valued at USD 250.9 Million in 2025.

- The global market is projected to grow at a CAGR of 7.8% and is estimated to reach USD 530.9 Million by 2035.

- On the basis of product type, petro-based products dominated the market, constituting 58.3% of the total market share.

- Based on the grade, industrial grade led the market, comprising 46.8% of the total market.

- Among the end-use industries, industrial manufacturing held a major share, accounting for 38.2% of the market.

- In 2025, the Asia Pacific was the most dominant region, accounting for 40.5% of the total global consumption.

Product Type Analysis

Petro-based represents the dominant Segment in the Market.

Petro-based succinic acid retains the dominant position in the global market, accounting for 58.3% of total volume, driven by its established cost advantage, mature production infrastructure, and deep integration into industrial polymer, solvent, and plasticiser value chains. This dominance reflects decades of process optimisation within petrochemical manufacturing, which allows large-volume buyers in coatings and resins to source competitively priced intermediates without reformulation investment.

However, bio-based succinic acid, representing 41.7% of the market, is the fastest-growing segment as regulatory mandates and corporate decarbonisation commitments accelerate feedstock substitution decisions.

Roquette’s BIOSUCCINIUM operates through a patented low-pH yeast fermentation process proven to be the most sustainable production route for bio-succinic acid, functioning as a direct drop-in replacement for petro-based succinic acid while also substituting petro-based adipic acid, delivering a measurably improved environmental footprint across polymer and coating applications. This dual substitution capability is directly narrowing petro-based dominance across sustainability-sensitive procurement segments.

Grade Analysis

Industrial Grade a significant Grade.

Industrial grade commands the largest share at 46.8%, reflecting succinic acid’s foundational role as a chemical intermediate in resins, plasticisers, coatings, solvents, and polyurethane production, where purity specifications are functional rather than regulatory. This concentration reflects volume-driven demand from manufacturing sectors that prioritise consistency and cost efficiency over certification requirements.

Food and beverage grade follows at 24.5%, supported by succinic acid’s established role as an acidity regulator and flavour modifier in processed food formulations globally. Pharmaceutical grade, at 18.2%, represents the fastest-growing segment as drug manufacturers increasingly adopt bio-certified excipients to meet green chemistry frameworks and supply chain transparency requirements.

Roquette’s BIOSUCCINIUM S speciality grade is specifically designed for pharmaceutical, cosmetics, and food applications requiring the highest purity standards, carrying Halal, Kosher, and ECOCERT 100% natural origin certifications, credentials that directly address procurement compliance requirements tightening across regulated end markets.

End Use Analysis

Succinic Acid Are Mostly Utilized in industrial manufacturing.

Industrial manufacturing leads end-use demand with a 38.2% share, underpinned by succinic acid’s critical function as a building block for polyurethane dispersions, coating resins, and biodegradable polymer intermediates across large-scale production environments. This dominance is reinforced by the breadth of industrial applications from automotive sealants and adhesives to agricultural film production that depend on succinic acid as a versatile platform chemical.

Packaging is the fastest-growing end-use segment, driven by regulatory pressure on single-use conventional plastics and rising demand for polybutylene succinate-based biodegradable alternatives. CBE JU’s LUCRA project, which kicked off in July 2023 in Ghent, Belgium, is producing succinic acid specifically to manufacture polyester-based polyurethane dispersions and resins, with circular waste valorisation processes designed to cut greenhouse gas emissions, validating industrial manufacturing and packaging as converging demand centres.

Key Market Segments

By Product Type

- Petro-based

- Bio-based

By Grade

- Industrial Grade

- Food & Beverage Grade

- Pharmaceutical Grade

- Electronic Grade

By End Use

- Industrial Manufacturing

- Packaging

- Pharmaceuticals

- Food Processing

- Personal Care & Cosmetics

- Automotive

- Others

Market Dynamics

Challenges

Bio-based succinic acid remains structurally exposed to volatile feedstock economics because production depends on glycerol, glucose, molasses, and lignocellulosic intermediates, whose prices fluctuate with agricultural yields, energy costs, freight rates, and regional processing margins. Published pathway assessments indicate economically viable production at around USD 1.6–2.0/kg under optimised conditions, leaving limited room to absorb raw-material inflation.

A 10%–15% increase in biomass or utility costs can raise plant cash costs by approximately 6%–9%, forcing lower operating rates, delayed contracting, and slower customer qualification. These factors collectively create an estimated -1.3 percentage point drag on market growth.

In a 2026 macroeconomic environment with projected global growth of 3.1% and persistent inflation risks, producers are increasingly adopting dual-feedstock flexibility, regional biomass sourcing agreements, and integrated feedstock pre-treatment strategies. However, these mitigation measures generally require 18–36 months of capital investment, certification, and operational optimisation before delivering meaningful stability.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Feedstock cost volatility | -1.3% | North America corn belt, EU bio-refining clusters, APAC import-dependent sites | Medium term (2-4 years) |

| Purification yield bottlenecks | -1.1% | EU regulatory hubs, North America pilot assets, East Asia fermentation lines | Medium term (2-4 years) |

| Fossil-route price benchmarking | -0.9% | China’s manufacturing base, ASEAN export corridors, and global contract markets | Long term (≥ 4 years) |

| Logistics route instability | -0.8% | EU-Asia lanes, Middle East-linked shipping, global container routes | Short term (≤ 2 years) |

| Carbon compliance uncertainty | -0.7% | EU regulatory hubs, exporters into Europe, and multinational speciality chemicals | Long term (≥ 4 years) |

| Scale-up talent scarcity | -0.6% | North America innovation clusters, Western Europe bioprocess sites, Japan-Korea advanced chemicals base | Long term (≥ 4 years) |

Opportunity

The strongest white-space opportunity lies in downstream integration into polybutylene succinate (PBS) packaging systems, allowing succinic acid producers to capture resin, formulation, and converter value rather than remaining merchant molecule suppliers. This opportunity gained momentum after the EU Packaging and Packaging Waste Regulation entered into force in 2025 and began applying from August 2026, increasing demand for recyclable and compostable packaging solutions while tightening producer responsibility requirements.

Moving downstream into premium PBS grades could add an estimated 220–320 basis points of CAGR above the base market. This strategy can increase realised revenue per tonne by roughly 25%–40%, improve contract visibility through 2–5 year supply agreements, and expand EBITDA margins by approximately 4–7 percentage points through compound-and-sell business models.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| PBS packaging integration | +2.3% | EU, North America core, East Asia | Short term |

| Polyol-to-PU platform entry | +1.7% | EU, North America, China | Medium term |

| High-purity pharma/cosmetics grade | +1.2% | North America, EU, Japan, South Korea | Short term |

| C1 fermentation and carbon credits | +1.5% | EU, China, North America | Medium term |

| Ag-input chelation adjacencies | +0.9% | India, Brazil, Southeast Asia | Medium term |

| Regional roll-up and tolling model | +1.4% | APAC emerging, EU, North America | Short term |

Drivers

China-led biodegradable materials policies and broader Asia-Pacific regulatory momentum are accelerating downstream demand for succinic-acid-based polymers. China’s national single-use plastics reduction plan phases in restrictions through 2024–2025, to broadly prohibit most consumer single-use plastics by 2025.

The wider Asia-Pacific region is experiencing similar pressure for sustainable alternatives. In the Philippines, approximately 500,000 metric tons of plastic waste leak into the environment annually, and an estimated 70%–90% of illegally disposed waste ultimately reaches water bodies.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bio-PBS and compostable plastics pull for succinic acid intermediates | +2.4% | APAC core, EU, North America selective | Medium term (2-4 years) |

| EU packaging compliance and recyclability rules lifting bio-based chemical substitution | +1.7% | EU core, UK spill-over, export-oriented APAC suppliers | Short term (≤ 2 years) |

| Coatings, alkyd resins and polyurethane chain recovery are increasing industrial consumption | +1.3% | China, India, ASEAN, North America, EU industrial belts | Short term (≤ 2 years) |

| Fermentation scale-up and process economics improving bio-succinic competitiveness | +1.5% | North America technology base, EU fermentation hubs, East Asia manufacturing corridors | Medium term (2-4 years) |

| Pharma, food, and specialty formulation demand supporting higher-value grade mix | +0.9% | North America, EU, Japan, South Korea, India | Short term (≤ 2 years) |

| China-led biodegradable materials policy and Asia capacity clustering are accelerating the downstream offtake | +1.2% | China’s core, broader APAC corridors, and Latin America spill-over | Medium term (2-4 years) |

Restraints

Succinic acid demand is increasingly tied to derivative value chains such as 1,4-butanediol (BDO) and polybutylene succinate (PBS), making it vulnerable to trade disruptions even when succinic acid supply itself remains available. The EU launched an antidumping investigation into imported BDO in June 2025 and introduced provisional duties in February 2026.

Reported provisional duty rates reached 106%–114% for China, 52% for Saudi Arabia, and 136%–143% for the United States, before the case moved toward definitive action in June 2026. Since BDO is a key precursor for PBS and other polyester systems, these measures significantly affect downstream production economics.

The resulting disruption can extend qualification cycles by 8–20 weeks and increase downstream resin conversion costs by double-digit percentages in Europe through reformulation, destocking, contract renegotiations, and sourcing changes. Consequently, converters may delay new programs, packaging developers may postpone commercial runs, and investors may slow derivative expansion plans, creating an estimated -1.2 percentage point drag on forecast CAGR over the next 2–4 years.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fermentation feedstock volatility | -1.4% | EU, China, SE Asia, LatAm sugar corridors | Short term (≤ 2 years) |

| Petro-route price undercut | -1.8% | China core, EU imports, North America | Short term (≤ 2 years) |

| BDO/PBS derivative trade friction | -1.2% | EU core, China-EU corridors, Gulf-Europe | Medium term (2-4 years) |

| Freight and lead-time instability | -0.9% | Asia-Europe lanes, EU import hubs, US coasts | Short term (≤ 2 years) |

| High-cost scale-up economics | -1.6% | North America, the EU, Japan, and advanced APAC | Medium term (2-4 years) |

| Downstream adoption lag | -1.1% | EU packaging, North America polymers, APAC converters | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Competing Industrial Strategies Creating a Three-Way Race for Bio-Chemical Leadership

The bio-based chemicals sector has become a geopolitical battleground, with Europe, the United States, and China each pursuing competing industrial strategies that will shape global supply chains for succinic acid and its derivatives.

The European Commission’s 2025 Bioeconomy Strategy explicitly acknowledges that international competition from the United States and China is slowing European bio-based deployment and risks diverting innovation to non-EU markets, a rare admission of competitive vulnerability at the policy level.

The Commission has also noted that India’s bio-economy industry reached USD 130 Million in 2024 and is expected to reach USD 300 Million by 2030, adding a fourth major player to the competitive landscape, while the 2025 Bioeconomy Strategy is designed to mobilise capital for strengthening industrial ecosystems beyond EU borders through international trade and standards frameworks.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Succinic Acid Market

Asia Pacific commands the largest regional share at 40.5%, driven by concentrated demand from China, Japan, South Korea, and India across industrial chemicals, biodegradable packaging, electronics, and food processing sectors. The region’s manufacturing scale, feedstock availability, and government-backed industrial expansion programmes collectively sustain its leadership position, while rapidly growing domestic biodegradable polymer markets are accelerating demand for both petro-based and bio-based grades.

Europe is the fastest-growing region, propelled by binding regulatory frameworks that are systematically expanding the commercial case for certified bio-based succinic acid across chemicals, packaging, and pharmaceutical supply chains. CBE JU’s 2025 review confirmed the inauguration of multiple flagship biorefineries across Europe, with new facilities in Latvia, Spain, and France marking a decisive acceleration in industrial-scale bio-based chemical production, directly expanding succinic acid feedstock and production capacity.

North America sustains demand through government procurement mandates and advanced synthetic biology investment, while Latin America, the Middle East and Africa remain emerging but strategically relevant growth markets.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Succinic acid manufacturers focus on strengthening technological differentiation, production scale efficiency, and supply chain integration to maintain competitiveness. A key priority is continuous process innovation, including the advancement of bio-based fermentation routes using renewable feedstocks such as glucose, sucrose, and agricultural residues that improve yield efficiency, reduce carbon footprint, and meet the sustainability credentials increasingly demanded by downstream polymer, food, and pharmaceutical customers.

Vertical integration with agricultural feedstock suppliers and 1,4-butanediol derivative producers helps secure raw material stability and improve cost control amid volatile corn, cassava, and sugar commodity pricing. Strategic capacity expansion, particularly across Asia Pacific and Europe, enables alignment with concentrated demand from biodegradable polymer, food additive, and pharmaceutical intermediate ecosystems.

Additionally, manufacturers emphasise intellectual property protection around proprietary microbial strains and fermentation process designs, process automation in continuous fermentation and crystallisation operations, and quality standardisation across food-grade and pharmaceutical-grade product tiers to ensure consistency at scale, while forming long-term supply agreements with major bioplastic producers, flavour and fragrance companies, and speciality chemical formulators to reinforce customer lock-in and strengthen positioning in high-value bio-based application segments.

The Following are some of the Major Players in the Industry

- RPI Corp

- Vigon International

- Guangzhou ZIO Chemical Co.

- Roquette Frères

- Mitsubishi Chemical Group

- Nippon Shokubai Co., Ltd.

- Air Water Performance Chemical Inc.

- Anhui Sunsing Chemicals

- Jinan Finer Chemical Co., Ltd.

- Haihang Group

- Henan GP Chemicals Co., Ltd.

- Royal DSM (Reverdia)

- Wenzhou Blue Dolphin New Material Co., Ltd.

- Carl Roth GmbH + Co. KG

- Axiom Chemicals Pvt. Ltd.

- Other Key Players

Key Developments

- In March 2026, Roquette was awarded the EcoVadis Gold Medal and earned a B score for both Climate and Water security in CDP’s annual environmental management assessment, directly reinforcing its BIOSUCCINIUM bio-succinic acid platform’s sustainability credentials across industrial, packaging, and pharmaceutical buyer segments globally.

- In October 2025, Mitsubishi Chemical’s multilayer films containing SoarnoL EVOH resins received RecyClass Technology Approval, strengthening its biodegradable packaging value chain where BioPBS, its succinic acid-derived compostable polymer, serves food packaging and circular economy applications across Asia Pacific markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 250.9 Mn |

| Forecast Revenue (2035) | USD 530.9 Mn |

| CAGR (2026-2035) | 7.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Petro-based and Bio-based), By Grade (Industrial Grade, Food & Beverage Grade, Pharmaceutical Grade, and Electronic Grade), By End-use Industry (Industrial Manufacturing, Packaging, Pharmaceuticals, Food Processing, Personal Care & Cosmetics, Automotive, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa, & Rest of MEA |

| Competitive Landscape | RPI Corp., Vigon International, Guangzhou ZIO Chemical Co., Roquette Frères, Mitsubishi Chemical Group, Nippon Shokubai Co., Ltd., Air Water Performance Chemical Inc., Anhui Sunsing Chemicals, Jinan Finer Chemical Co., Ltd., Haihang Group, Henan GP Chemicals Co., Ltd., Royal DSM (Reverdia), Wenzhou Blue Dolphin New Material Co., Ltd., Carl Roth GmbH + Co. KG, Axiom Chemicals Pvt. Ltd., Other Key Players |

| Customization Scope | Customisation for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |