Quick Navigation

Report Overview

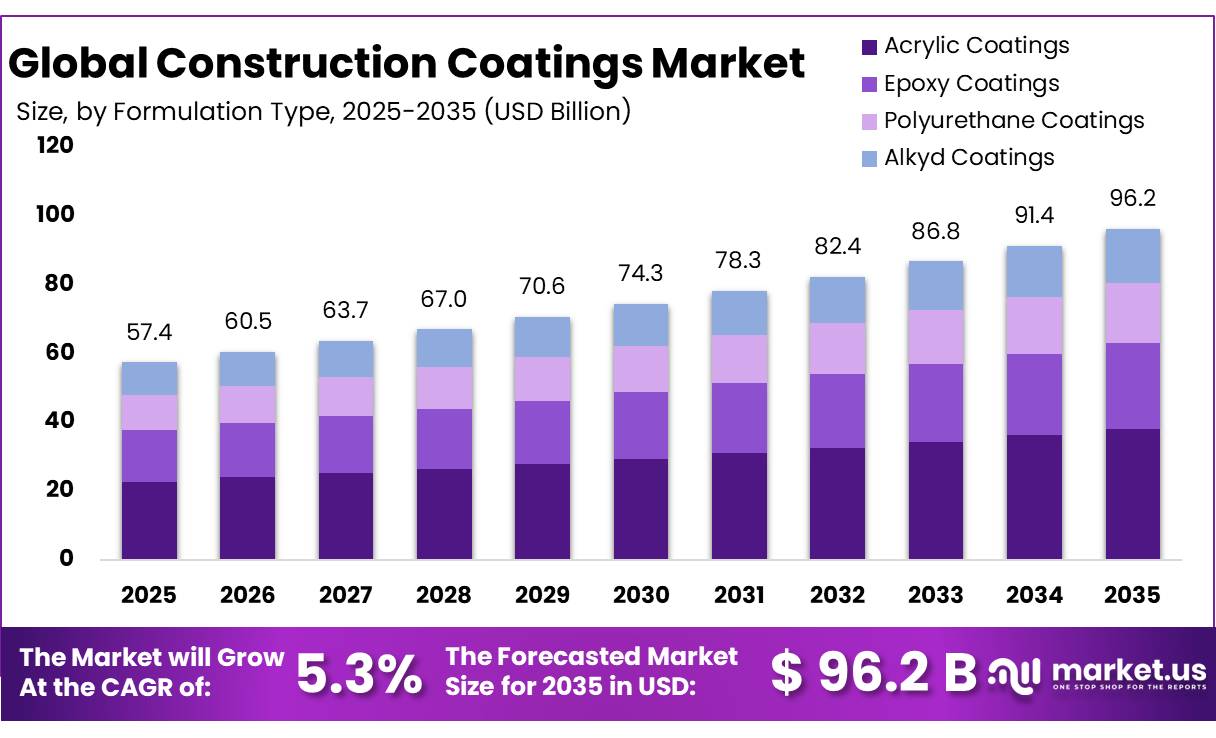

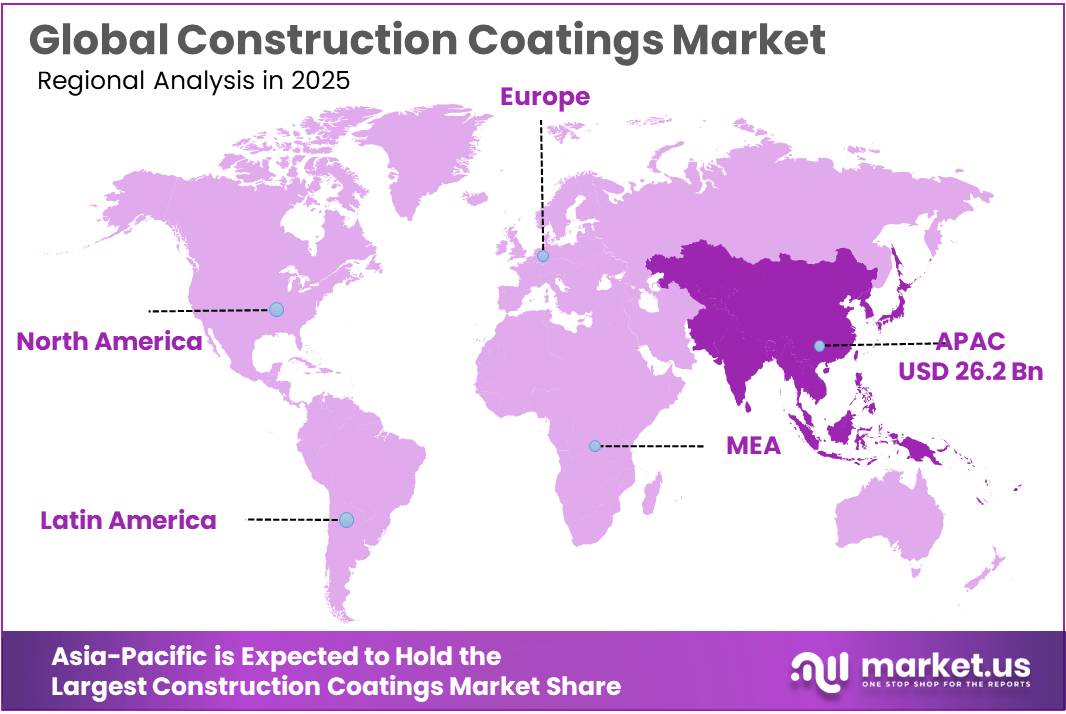

The Global Construction Coatings Market size is expected to be worth around USD 96.2 Billion by 2035, from USD 57.4 Billion in 2025, growing at a CAGR of 5.3% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 45.8% share, holding USD 12.5 Billion revenue.

Construction coatings represent a key part of the paints, protective coatings and architectural coatings industry, serving residential, commercial, infrastructure and industrial buildings through products such as wall coatings, floor coatings, waterproofing systems, roof coatings, metal coatings and protective concrete finishes. The industry scenario remains linked to construction activity, renovation cycles, infrastructure spending and sustainability regulations.

In the U.S., construction spending was estimated at an annual rate of $2,152.4 billion in April 2025, while public construction reached $513.5 billion and highway construction stood at $146.3 billion, supporting demand for durable coatings used on buildings, bridges, roads, public facilities and civil structures.

The sector is being driven by urban redevelopment, repair of aging assets, higher performance requirements and green-building policies. The EU’s revised Energy Performance of Buildings Directive requires new public buildings to be zero-emission from January 1, 2028, and all other new buildings from January 1, 2030, creating opportunities for energy-efficient façade coatings, cool roof coatings, air-barrier coatings and low-VOC systems.

In the U.S., the Bipartisan Infrastructure Law provided $62 billion for FY2025 federal-aid highway and infrastructure programs, strengthening coatings demand across steel, concrete, transport and public infrastructure assets. In the U.S., construction spending in May 2025 stood at an annualized US$2,138.2 billion, while new residential completions reached 1.526 million units annualized, showing continued repainting and finishing demand despite housing pressure.

Demand is being driven by renovation cycles, stricter building-efficiency rules, infrastructure maintenance, and sustainability requirements. The EU’s revised Energy Performance of Buildings Directive entered into force on 28 May 2024, requires national transposition by 29 May 2026, and targets full building-sector decarbonisation by 2050, supporting future demand for energy-saving façade, roof, insulation-compatible, and refurbishment coatings. In the U.S., EPA lead-safe renovation rules require certified firms for renovation work in pre-1978 child-occupied buildings, supporting regulated repainting and surface-preparation demand.

Recent 2025 developments show active portfolio repositioning. Sherwin-Williams announced in February 2025 that it would acquire BASF’s Brazilian architectural paints business for US$1.15 billion, and completed the acquisition on 1 October 2025. PPG, meanwhile, had completed the sale of its U.S. and Canada architectural coatings business for US$550 million in December 2024, shaping its 2025 focus toward higher-return coatings platforms.

Key Takeaways

- Construction Coatings Market size is expected to be worth around USD 96.2 Billion by 2035, from USD 57.4 Billion in 2025, growing at a CAGR of 5.3%.

- Acrylic Coatings held a dominant market position, capturing more than a 39.6% share.

- Water-Based Coatings held a dominant market position, capturing more than a 49.2% share.

- Protective Coatings held a dominant market position, capturing more than a 36.9% share.

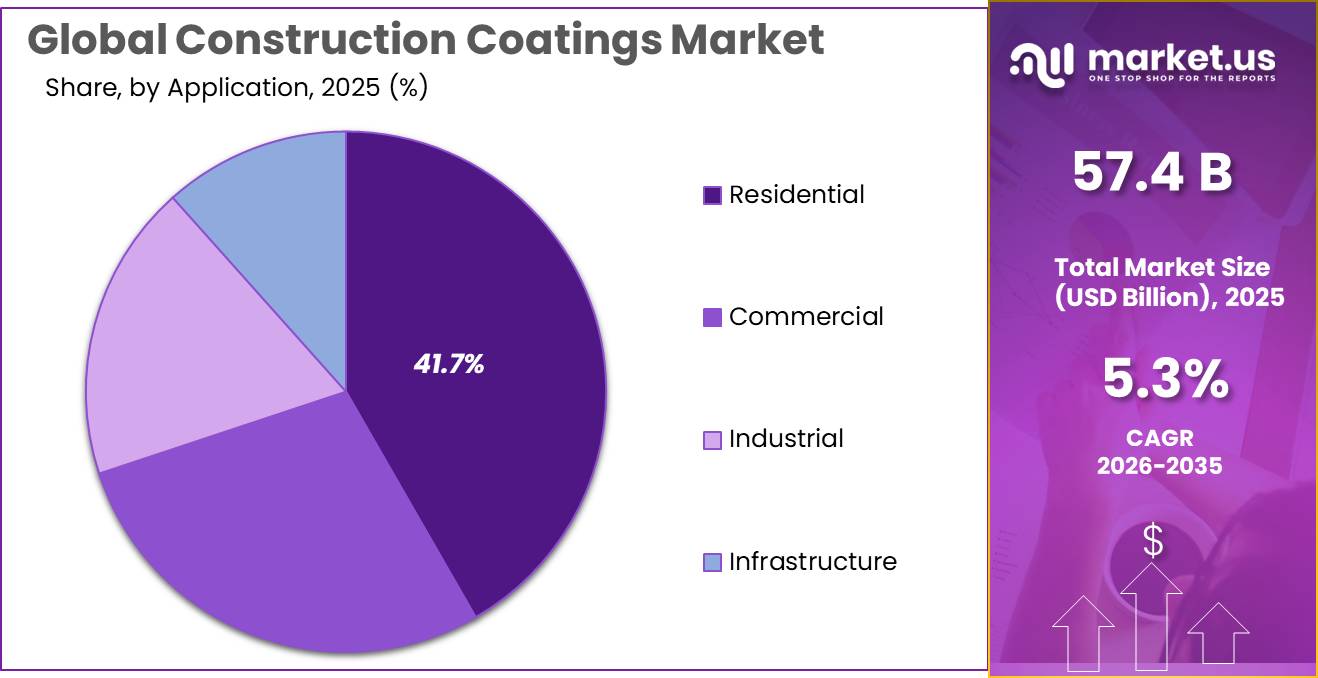

- Residential held a dominant market position, capturing more than a 41.7% share.

- Asia-Pacific remains the dominating region in the global construction coatings market, accounting for approximately 45.80% share, valued at around USD 26.2 billion.

By Formulation Type Analysis

Acrylic Coatings dominates with 39.6% due to its versatility and strong performance across construction applications

In 2025, Acrylic Coatings held a dominant market position, capturing more than a 39.6% share. This strong presence is largely driven by their wide usage in both residential and commercial construction projects, where durability, weather resistance, and ease of application are key priorities. Acrylic-based formulations are preferred for exterior surfaces because they offer excellent UV stability and color retention, making them suitable for varied climatic conditions. Their water-based nature also makes them more environmentally acceptable compared to solvent-based alternatives, which has supported their adoption in regions with stricter environmental norms.

By Product Type Analysis

Water-Based Coatings leads with 49.2% as builders shift toward cleaner and safer coating solutions

In 2025, Water-Based Coatings held a dominant market position, capturing more than a 49.2% share. This leadership is mainly supported by the growing preference for eco-friendly construction materials and stricter regulations around harmful emissions. These coatings release very low levels of volatile organic compounds, making them safer for both workers and occupants. Their easy application, low odor, and faster drying time have made them a practical choice across residential and commercial projects, especially in indoor environments where air quality is a concern.

By Functionality Analysis

Protective Coatings stands strong with 36.9% as durability becomes a top priority in construction

In 2025, Protective Coatings held a dominant market position, capturing more than a 36.9% share. This segment continues to grow as builders focus more on extending the life of structures and reducing maintenance costs over time. These coatings are widely used on concrete, steel, and other structural materials to protect against corrosion, moisture, chemicals, and harsh weather conditions. Their role is especially important in infrastructure projects such as bridges, industrial facilities, and high-rise buildings where long-term performance is critical.

By Application Analysis

Residential segment leads with 41.7% as housing demand keeps construction activity strong

In 2025, Residential held a dominant market position, capturing more than a 41.7% share. This growth is mainly driven by rising housing demand, urban expansion, and increased spending on home improvement projects. Construction coatings are widely used in residential buildings for both interior and exterior surfaces, helping improve appearance while also providing protection against weather, moisture, and wear. Homeowners are also paying more attention to finishes, colors, and long-lasting coatings, which has supported steady demand in this segment.

Key Market Segments

By Formulation Type

- Acrylic Coatings

- Epoxy Coatings

- Polyurethane Coatings

- Alkyd Coatings

By Product Type

- Water-Based Coatings

- Solvent-Based Coatings

- Specialty Coatings

- Powder Coatings

By Functionality

- Protective Coatings

- Decorative Coatings

- Anti-Corrosive Coatings

- Fire-Resistant Coatings

By Application

- Residential

- Commercial

- Industrial

- Infrastructure

Emerging Trends

Shift toward low-VOC and eco-friendly coatings is shaping the latest market trend

One of the most noticeable trends in the construction coatings market is the fast move toward low-VOC and environmentally friendly products. Governments and environmental bodies have been actively pushing for cleaner air standards, which is directly influencing coating choices. For example, the U.S. Environmental Protection Agency introduced regulations that are expected to reduce VOC emissions by about 103,000 megagrams per year (around 113,500 tons) from architectural coatings.

Builders are not only focused on performance but also on indoor air quality and environmental impact. Low-VOC coatings are now being used in homes, offices, and public buildings as a safer alternative. This shift is not temporary—it is becoming a long-term standard as both regulations and customer expectations continue to evolve.

Advanced sustainable technologies are changing how coatings are made

Another important trend is the growing use of advanced technologies to make coatings more sustainable and efficient. Companies are now focusing on reducing carbon emissions during production and improving product performance at the same time. For example, new coating technologies are being developed that can cut carbon emissions by up to 50%, showing how innovation is reshaping the industry.

At the same time, research shows that green chemistry and clean production methods are becoming common approaches in coating development. These methods focus on reducing harmful chemicals and improving safety without affecting durability.

Drivers

Strong push from environmental rules is shaping coating demand

One of the biggest forces behind the construction coatings market is the growing pressure to reduce harmful emissions. Governments and environmental bodies have been tightening rules around volatile organic compounds (VOCs), which are commonly released from traditional coatings. For example, the United States Environmental Protection Agency introduced standards that are expected to cut VOC emissions by about 103,000 megagrams per year (around 113,500 tons) from architectural coatings alone.

By 2025 and moving into 2026, this trend is still shaping the market. Builders and developers are no longer just choosing coatings for looks or durability—they also need to meet environmental standards. This has created steady demand for low-emission coatings, making sustainability not just a preference but a requirement in modern construction projects.

Shift toward sustainable materials is driving long-term growth

Another key driver is the strong move toward sustainable construction practices. Across the building industry, there is a clear shift toward materials that are safer for people and the environment. Coatings are a major part of this change because they are used on almost every surface. Studies show that manufacturers are actively adopting green chemistry, cleaner production methods, and low-VOC technologies to meet this demand.

This shift is also backed by consumer preference. People now expect buildings to use materials that improve indoor air quality and reduce environmental impact. Because of this, water-based and eco-friendly coatings are becoming more common in both residential and commercial spaces. At the same time, governments continue to support these changes through stricter policies and building standards, encouraging wider adoption.

Restraints

Strict environmental rules are increasing compliance costs

One major factor holding back the construction coatings market is the growing burden of environmental regulations, especially around volatile organic compounds (VOCs). Governments have made it clear that coatings must meet strict emission limits to protect air quality and public health. For instance, the U.S. Environmental Protection Agency introduced standards that aim to reduce VOC emissions by about 103,000 megagrams per year (around 113,500 tons) from architectural coatings.

While these rules are important, they create pressure on manufacturers. Companies must invest in new technologies, reformulate products, and adjust production processes to meet these limits. This increases overall costs, especially for smaller manufacturers that may not have the same financial strength as larger players. In many cases, compliance also involves testing, certification, and detailed reporting, which adds time and complexity.

Performance trade-offs with low-emission coatings

Another key restraint is the balance between environmental compliance and product performance. Traditional coatings often rely on solvents that help improve durability, finish quality, and resistance. However, these same solvents are the main source of VOC emissions. Regulations now limit how much VOC can be used, with general limits going up to around 450 grams per liter depending on coating type, forcing manufacturers to reduce or replace these components.

The challenge is that not all low-VOC alternatives can fully match the performance of older formulations, especially in demanding environments like industrial or heavy-duty construction. Some coatings may show reduced adhesion, longer curing times, or lower resistance to extreme conditions. This can make builders hesitant to switch completely, particularly for projects where long-term durability is critical.

Opportunity

Rising adoption of green building is opening new growth space

One of the biggest growth opportunities for construction coatings is the rapid shift toward green building practices. Around the world, builders are focusing more on reducing environmental impact, and coatings play a key role in that transition. Green building aims to improve energy efficiency, reduce waste, and create healthier indoor environments, which naturally increases the demand for low-VOC and eco-friendly coatings.

This shift is not just about preference—it is becoming a standard approach. Studies show that sustainable construction methods can even lower overall building costs by about 0.4% compared to traditional construction, making it both environmentally and economically attractive.

Cost-saving benefits of advanced coatings are boosting demand

Another important opportunity comes from the cost-saving benefits that modern coatings can offer over time. Advanced protective and green coatings are not just about surface finish—they help extend the life of buildings and reduce maintenance needs. For example, certain coating technologies used in building encasement can reduce costs by 25% to 75% compared to full removal or replacement methods, while also improving durability.

This kind of saving is a major advantage, especially for large infrastructure and renovation projects where maintenance costs can be high. Instead of replacing materials, applying high-performance coatings allows structures to last longer with minimal disruption. This is particularly useful in commercial buildings, industrial sites, and public infrastructure where downtime is costly.

Regional Insights

Asia-Pacific Construction Coatings Market Overview (Dominating Region – 45.80%, ~USD 26.2 Billion)

Asia-Pacific remains the dominating region in the global construction coatings market, accounting for approximately 45.80% share, valued at around USD 26.2 billion, driven by strong construction activity, urban expansion, and industrial development across major economies.

The region’s broader paints and coatings industry itself is significantly large, with total market size reaching about USD 86.19 billion in 2026, highlighting the strong base for construction-related coating demand. This dominance is supported by high consumption of architectural coatings, which alone account for nearly 39.82% share of total coatings demand in 2025, reflecting the critical role of building and infrastructure applications.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Sherwin-Williams Company remains one of the largest players in the construction coatings market, supported by strong financial performance and a wide distribution network. In 2025, the company reported revenue of around USD 23.5 billion, reflecting steady growth and global demand for its coatings solutions. It operates over 5,400 stores worldwide and serves both professional and retail customers. Its coatings segment alone contributes nearly USD 19.3 billion, making it a clear industry leader.

PPG Industries, Inc. holds a strong position in the construction coatings market with a diverse product portfolio across architectural, industrial, and protective coatings. In 2025, the company recorded net sales of approximately USD 15.9 billion, showing stable growth driven by pricing and volume gains. Its coatings sales alone stood near USD 15.8 billion, highlighting its core strength in this segment.

Akzo Nobel N.V. is a key global player known for its decorative and performance coatings portfolio. The company generated coatings revenue of about USD 11.16 billion, placing it among the top three globally. Its overall revenue has remained above USD 11 billion, supported by strong demand across infrastructure and industrial applications. Operating in over 150 countries, Akzo Nobel focuses on sustainability and innovation, with well-known brands like Dulux and Sikkens strengthening its presence in the construction coatings market.

Top Key Players Outlook

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc. (Rust-Oleum/Tremco)

- Kansai Paint Co., Ltd.

- Asian Paints Limited

- BASF SE

- Axalta Coating Systems Ltd.

- Hempel A/S

Recent Industry Developments

In 2025, Nippon Paint Holdings Co., Ltd reported consolidated revenue of about ¥887,462 million (around USD 5.8–6.0 billion for its core NIPSEA segment), while total group revenue across segments exceeded ¥1,700,000 million, reflecting steady global demand.

In 2025, RPM reported record sales of USD 7.37 billion, up 0.5%, with net income of USD 688.7 million, diluted EPS of USD 5.35, adjusted EBIT of USD 976.0 million, and adjusted EBIT margin of 13.2%. Its Q4 fiscal 2025 sales reached USD 2.08 billion, up 3.7%, showing solid demand for building maintenance and restoration products. For fiscal 2026, RPM expects sales to grow in the low- to mid-single-digit range, supported by its Construction Products Group and Performance Coatings Group.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 57.4 Bn |

| Forecast Revenue (2035) | USD 96.2 Bn |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Formulation Type (Acrylic Coatings, Epoxy Coatings, Polyurethane Coatings, Alkyd Coatings), By Product Type ( Water-Based Coatings, Solvent-Based Coatings, Specialty Coatings, Powder Coatings), By Functionality (Protective Coatings, Decorative Coatings, Anti-Corrosive Coatings, Fire-Resistant Coatings), By Application (Residential, Commercial, Industrial, Infrastructure) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc. (Rust-Oleum/Tremco), Kansai Paint Co., Ltd., Asian Paints Limited, BASF SE, Axalta Coating Systems Ltd., Hempel A/S |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |