Quick Navigation

Report Overview

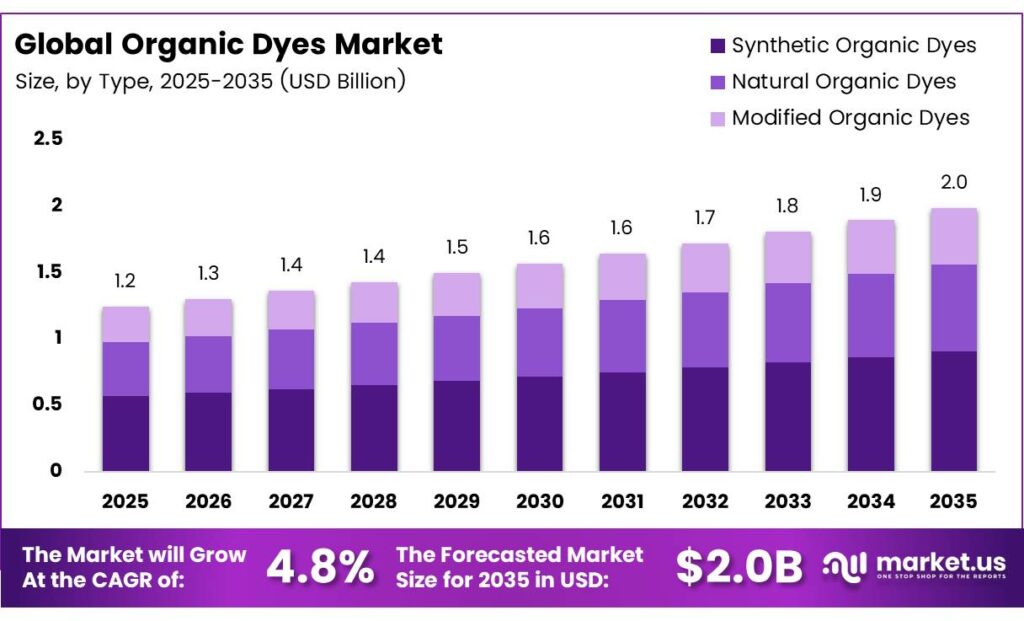

The Global Organic Dyes Market size is expected to be worth around USD 2.0 billion by 2035 from USD 1.2 billion in 2025, growing at a CAGR of 4.8% during the forecast period 2026 to 2035.

Organic dyes are carbon-based colorants used across textiles, food, cosmetics, leather, and paper industries. Unlike conventional synthetic dyes, organic variants offer biodegradability, lower toxicity profiles, and compatibility with tightening environmental regulations. These attributes position organic dyes as a structurally preferred input for manufacturers navigating stricter compliance requirements.

The treatment of organic dye wastewater using both advanced materials and biological approaches. A Pd–In₂O₃/BiVO₄ photocatalyst achieved up to 99% degradation of Rhodamine B within 40 minutes, far outperforming pure In₂O₃, while vanadium-doped tin oxide demonstrated similarly high efficiency across multiple dyes, indicating strong potential for mixed-effluent treatment.

Wastewater treatment performance has also become a commercial differentiator. A review on dye-containing wastewater in textile applications reports that optimized combinations of adsorption, coagulation-flocculation, and advanced oxidation can routinely achieve 85–100% color removal for various organic dye classes. This advances the case for organic dyes in jurisdictions where effluent standards are tightening, giving producers with cleaner discharge profiles a procurement advantage over conventional alternatives.

Key Takeaways

- The Global Organic Dyes Market was valued at USD 1.2 billion in 2025 and is forecast to reach USD 2.0 billion by 2035 at a CAGR of 4.8% during the forecast period 2026 to 2035.

- Synthetic Organic Dyes dominate with a 67.3% share in 2025.

- Petroleum leads with a 43.8% share.

- Powders hold the largest share at 49.6%.

- Colorants lead with a 56.4% share.

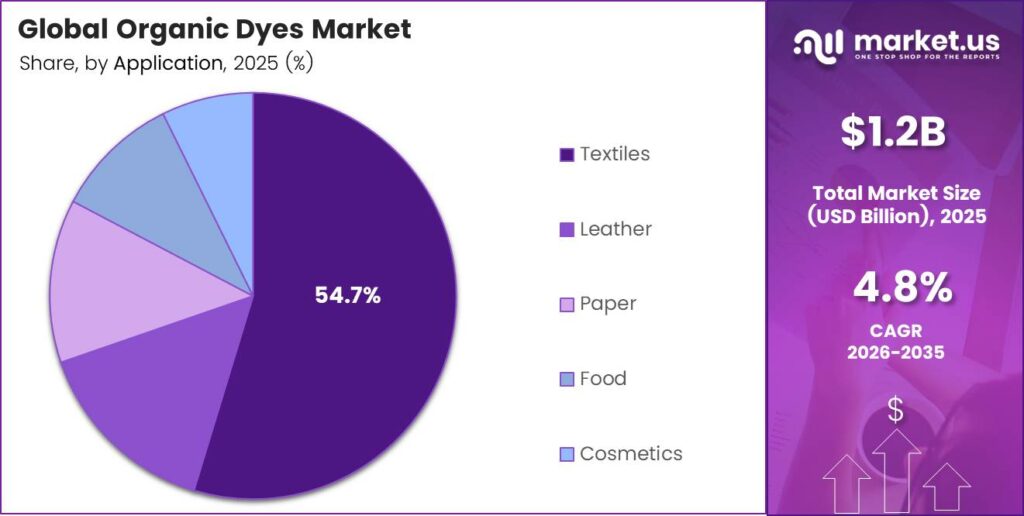

- Textiles account for the dominant share at 54.7%.

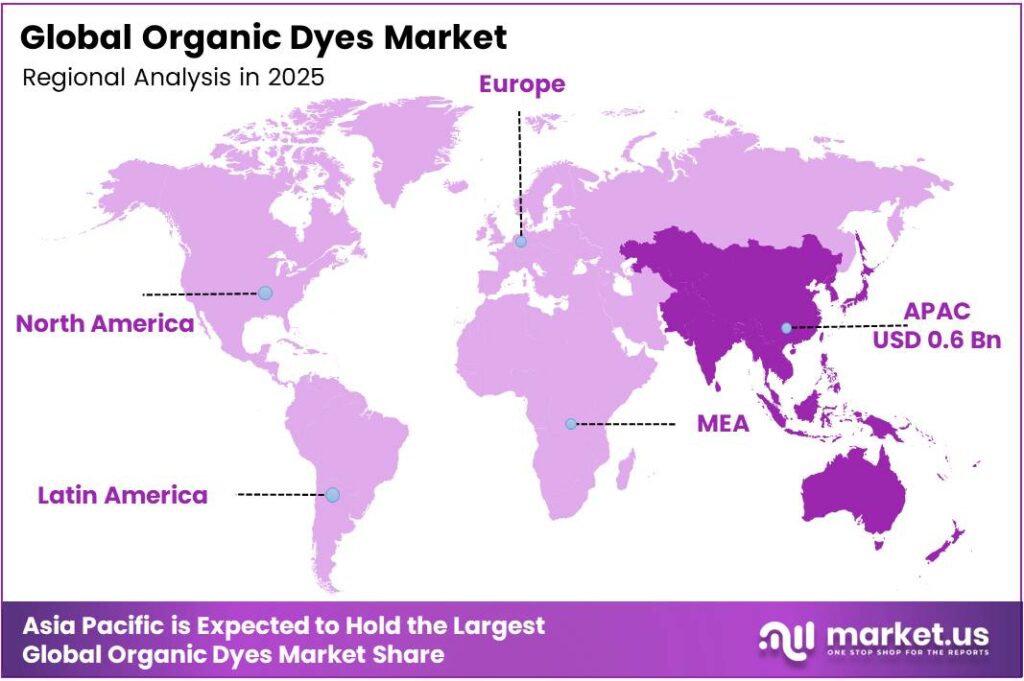

- Asia-Pacific dominates regionally with a 51.2% share, valued at USD 0.6 billion.

Product Form Analysis

Powders dominate with 49.6% due to ease of handling and formulation flexibility.

In 2025, Powders held a dominant market position in the By Product Form segment of the Organic Dyes Market, with a 49.6% share. Powder-form dyes offer manufacturers precise dosing control, extended shelf life, and compatibility across a broad range of dyeing equipment — making them the default procurement choice in high-volume textile and paper operations.

Liquids serve as the preferred format for continuous-flow industrial dyeing processes where rapid dissolution and consistent bath concentration matter most. Liquid organic dyes reduce preparation time on the factory floor, making them particularly valuable in large-scale operations where production downtime carries a direct cost. Their adoption reflects operational efficiency priorities over unit cost considerations.

Type Analysis

Synthetic Organic Dyes dominate with 67.3% due to superior performance consistency and scalability.

In 2025, Synthetic Organic Dyes held a dominant market position in the By Type segment of the Organic Dyes Market, with a 67.3% share. Their dominance reflects a market reality: buyers across textiles, paper, and leather prioritize color fastness and batch reproducibility. Synthetic organic dyes consistently deliver both, giving manufacturers a lower technical risk profile than natural alternatives.

Natural Organic Dyes serve as the primary choice for brands targeting certified sustainable or organic product lines, particularly in premium apparel and cosmetics. Their extraction from plant and animal sources limits scalability, but that supply constraint also supports premium pricing. Natural organic dyes address a buyer segment that trades performance margin for sustainability credentials.

Source Analysis

Petroleum dominates with 43.8% due to established supply chains and high feedstock availability.

In 2025, Petroleum held a dominant market position in the By Source segment of the Organic Dyes Market, with a 43.8% share. Petroleum-derived intermediates provide the chemical building blocks for a majority of synthetic organic dyes, and existing refinery and petrochemical infrastructure keep input costs competitive. This supply chain maturity makes petroleum the default source for large-volume dye manufacturers.

Plants function as the primary natural feedstock for organic dyes targeting sustainability-certified markets. Plant-based sourcing supports traceability claims and aligns with growing retailer requirements for clean supply chain documentation. However, seasonal availability and geographic concentration of key plant species introduce supply variability that petroleum-based sourcing does not carry.

Function Analysis

Colorants dominate with 56.4% due to universal application across all end-use industries.

In 2025, Colorants held a dominant market position in the By Function segment of the Organic Dyes Market, with a 56.4% share. The breadth of their application — spanning textiles, food, cosmetics, paper, and pharmaceuticals — makes colorants the foundational functional category. Every industry that uses organic dyes begins with a colorant need, which structurally anchors their market leadership.

Mordants act as binding agents that fix dyes onto fibers, determining the final wash and light fastness of a dyed product. Without effective mordanting, natural dyes in particular lose commercial viability in demanding textile applications. Mordant demand is therefore directly tied to the performance upgrade cycle within the natural dye segment, making it a key enabler rather than an independent market driver.

Application Analysis

Textiles dominate with 54.7% due to scale, global export demand, and regulatory compliance needs.

In 2025, Textiles held a dominant market position in the By Application segment of the Organic Dyes Market, with a 54.7% share. The textile industry’s scale alone explains this concentration — it absorbs more dye volume than all other applications combined. Moreover, stricter chemical compliance requirements from major apparel brands are redirecting procurement toward organic and biodegradable dye formulations.

Leather applications depend on organic dyes for surface coloration and penetration dyeing across footwear, accessories, and upholstery production. Leather dyeing demands strong substrate affinity and post-processing durability, making performance-optimized organic dye formulations a technical requirement rather than a preference. Export-oriented leather manufacturers in Asia and Latin America represent a structurally growing buyer pool for this segment.

Paper uses organic dyes primarily for decorative, specialty, and packaging applications where consistent color reproduction across large print runs is essential. The shift toward certified-sustainable packaging has created a specific entry point for organic, low-toxicity dyes in food-contact paper and board products. This segment rewards dye producers who can demonstrate food-grade or food-adjacent safety credentials.

Key Market Segments

By Type

- Synthetic Organic Dyes

- Natural Organic Dyes

- Modified Organic Dyes

By Source

- Petroleum

- Plants

- Animals

- Coal Tar

By Product Form

- Powders

- Liquids

- Pastes

- Granules

By Function

- Colorants

- Mordants

- Brighteners

- Dye Adjuvants

By Application

- Textiles

- Leather

- Paper

- Food

- Cosmetics

Emerging Trends

Plant-Based Sourcing, Nanotechnology, and Circular Manufacturing Redefine Organic Dye Value Chains

Manufacturers are shifting dye extraction from petroleum-derived intermediates toward plant-based and microbial sources. This is not purely driven by preference — retail and regulatory procurement requirements now attach traceability and origin certifications to supplier contracts. Producers who establish verified plant-based or microbial supply chains gain a procurement advantage that competitors using conventional feedstocks cannot easily replicate.

Nanotechnology integration is changing organic dye performance benchmarks. Green-synthesized BSE-ZnO nanoparticles achieved 98.88% dye degradation under optimized conditions. This level of photocatalytic performance signals that nano-enhanced organic dye systems are moving from laboratory demonstration to commercially relevant process tools — particularly for industrial wastewater treatment and specialty coating applications.

Circular economy practices are entering dye manufacturing through closed-loop dyebath management and dye recovery systems. Additionally, hybrid organic-inorganic dye systems are advancing as a design framework that combines the environmental profile of organic compounds with the thermal and photostability of inorganic structures.

Drivers

Regulatory Pressure and Sustainability Mandates Accelerate Organic Dye Adoption Across Industries

Regulators in the EU, North America, and key Asian markets are tightening restrictions on toxic and non-biodegradable dye compounds. This is not a gradual shift — it creates hard compliance deadlines that force manufacturers to reformulate. Organic dyes, recognized for lower toxicity and biodegradability, move from optional to operationally necessary under these frameworks.

The textile and packaging industries face the most direct pressure, as brands increasingly require chemical compliance documentation from suppliers throughout the production chain. Consumer preference for naturally derived and sustainably produced goods reinforces this regulatory push at the demand side.

Efficiency gains further strengthen the commercial case. Low-liquor-ratio dyeing at a 1:3 liquor ratio uses just 2.5–3.7 kJ, achieving a 34–38% energy reduction compared to conventional 1:10 ratio dyeing. For cost-sensitive manufacturers, this energy efficiency translates directly into lower production costs, making organic dye systems more financially competitive against conventional alternatives — not just environmentally preferable.

Restraints

Performance Limitations and High Production Costs Slow Natural Organic Dye Scale-Up

Natural organic dyes consistently underperform synthetic alternatives on color fastness and stability — two criteria that industrial buyers treat as non-negotiable. In textiles and leather, where products undergo repeated washing, UV exposure, and mechanical stress, this performance gap translates into product liability risk. Until this gap narrows, natural organic dye penetration into performance-critical applications remains structurally limited.

High production costs compound the problem. Extracting natural dyes from plant and animal sources involves complex, labor-intensive processes with low yield efficiency. These costs create a price premium that buyers in price-sensitive markets — particularly in Asia and Latin America — consistently reject in favor of lower-cost synthetic inputs. The economics of natural extraction do not yet scale to commodity-volume price points.

Advanced treatment composites — such as a chitosan-polyaniline/nano-SiO₂ composite achieving 100% Congo red removal in just 40 minutes, with an adsorption capacity of 394.93 mg/g, Springer — demonstrate what performance benchmarks buyers will eventually demand from dye processes. Natural dye producers who cannot match treatment compatibility requirements face compounding commercial disadvantage as industry standards rise.

Growth Factors

Biotechnology Advances and New Application Frontiers Expand Organic Dye Revenue Pools

Biotechnology is reshaping organic dye production by enabling fermentation-based and enzymatic synthesis routes that bypass the yield constraints of traditional plant extraction. These methods reduce production costs, improve batch consistency, and open scalable supply pathways for natural and modified organic dyes. For manufacturers, this represents a structural cost improvement — not just an incremental efficiency gain.

Pharmaceutical and biomedical imaging applications represent a high-value adjacent market where organic dyes function as diagnostic agents and fluorescent markers. Entry barriers are high due to purity and safety requirements, but so are margins. Dye producers who can achieve pharmaceutical-grade certification access a buyer pool that prioritizes performance over price, fundamentally different from the commodity textile market dynamic.

Dye-sensitized solar cell technology further expands the addressable market into renewable energy. Photocatalytic nanocomposites achieve up to 97.15% dye degradation and 86.72% efficiency in mixed-dye systems. This photocatalytic behavior is precisely the functional property that makes organic dyes viable as light-absorbing sensitizers in solar cell architectures — connecting environmental chemistry performance to clean energy commercialization.

Regional Analysis

Asia-Pacific Dominates the Organic Dyes Market with a Market Share of 51.2%, Valued at USD 0.6 Billion

Asia-Pacific accounts for 51.2% of the global organic dyes market, valued at approximately USD 0.6 billion. This dominance reflects the region’s structural role as the world’s largest textile, leather, and paper manufacturing base. Countries such as China, India, and Bangladesh anchor demand through export-oriented production chains where organic dye inputs are embedded at scale.

North America sustains organic dye consumption through its cosmetics, food, and specialty chemicals sectors, where regulatory compliance and ingredient safety standards directly shape buyer specifications. The U.S. FDA’s stringent approval requirements for food and cosmetic colorants effectively create a high-barrier, premium-priced market structure that rewards certified organic dye producers with stable, defensible revenue.

Europe leads global regulatory frameworks on chemical safety, with REACH and EU BAT standards setting compliance benchmarks that cascade into global supply chains. European manufacturers and importers face the most structured compliance environment for organic dye formulations, making this region a critical proving ground for sustainable dye technologies before they achieve broader international commercial adoption.

The Middle East and Africa represent an early-stage organic dye market, with demand anchored in textile production in North Africa and specialty applications in Gulf countries. Infrastructure development and the slow build-out of regional manufacturing capacity constrain market scale currently.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Gharda Chemicals Ltd. positions itself as a vertically integrated specialty chemicals producer with deep expertise in reactive and disperse dye formulations. Its manufacturing concentration in India provides a cost-competitive base for export-oriented supply into textile markets across Asia, Europe, and the Americas. This integration from intermediates to finished dyes reduces input cost volatility — a structural advantage in commodity-pressured market cycles.

Lanxess AG leverages its global specialty chemicals platform to offer high-performance organic dye solutions for leather, textile, and paper applications. Its focus on sustainable chemistry and compliance-ready formulations directly targets the growing procurement segment where buyers require detailed toxicological and environmental documentation. This regulatory-aligned positioning makes Lanxess a preferred supplier for European and North American buyers facing the strictest chemical compliance environments.

Archroma Management GmbH has built a differentiated market position through its commitment to safer chemistry and textile sustainability platforms. The company’s proprietary low-impact dye systems address the textile industry’s need to reduce water, energy, and chemical consumption simultaneously. This multi-parameter efficiency proposition resonates with apparel brands under pressure to demonstrate measurable improvements across their supplier sustainability scorecards.

DyStar Group operates as one of the largest dedicated textile dye suppliers globally, with an extensive product portfolio spanning reactive, disperse, vat, and acid dye chemistries. Its scale enables consistent global supply across high-volume manufacturing markets while its technical service infrastructure supports customer-side color management and dyeing process optimization. DyStar’s breadth of chemistry coverage reduces switching costs for buyers who source multiple dye classes from a single partner.

Key Players

- Gharda Chemicals Ltd.

- Lanxess AG

- Archroma Management GmbH

- DyStar Group

- Sandoz AG

- Sinochem Holdings

- DIC Corporation

- Crompton Greaves Consumer Electricals Ltd.

- BASF SE

- Kiri Industries Ltd.

- Sahyadri Industries Ltd.

- Clariant

- Atul Ltd.

- Huntsman Corporation

Recent Developments

- In 2025, LANXESS emphasized colorants and pigments at major industry events: K 2025 included advanced color solutions for plastics and heat-stable organic and inorganic pigments; ECS 2025 included organic and inorganic color pigments for paints/coatings.

- In 2025, Archroma’s dye innovation focus includes DENIM HALO, using DIRSOL RD, DENISOL indigo dyes, DIRESUL sulfur dyes, and EarthColors biosynthetic dyes; reported impact reductions include 40–56% water savings, 30–36% energy reduction, and 33–34% CO₂ cuts versus standard processes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.2 Billion |

| Forecast Revenue (2035) | USD 2.0 Billion |

| CAGR (2026-2035) | 4.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Synthetic Organic Dyes, Natural Organic Dyes, Modified Organic Dyes), By Source (Petroleum, Plants, Animals, Coal Tar), By Product Form (Powders, Liquids, Pastes, Granules), By Function (Colorants, Mordants, Brighteners, Dye Adjuvants), By Application (Textiles, Leather, Paper, Food, Cosmetics) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Gharda Chemicals Ltd., Lanxess AG, Archroma Management GmbH, DyStar Group, Sandoz AG, Sinochem Holdings, DIC Corporation, Crompton Greaves Consumer Electricals Ltd., BASF SE, Kiri Industries Ltd., Sahyadri Industries Ltd., Clariant, Atul Ltd., Huntsman Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |