Quick Navigation

Report Overview

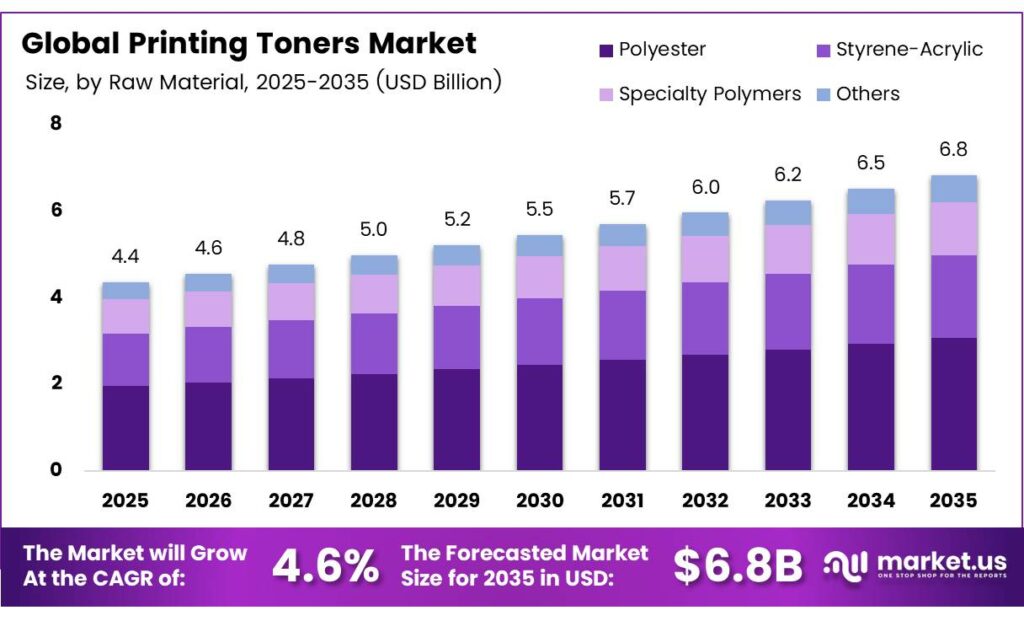

The Global Printing Toners Market size is expected to be worth around USD 6.8 billion by 2035 from USD 4.4 billion in 2025, growing at a CAGR of 4.6% during the forecast period 2026 to 2035.

Printing toners are dry powder mixtures used in laser printers and photocopiers to produce text and images on paper. They combine polymer resins, carbon black, and charge-control agents. This composition directly determines print quality, fusing efficiency, and operational cost per page — three metrics that enterprise procurement teams evaluate before committing to toner supply agreements.

Hongcai Color Tech, using low-fusing-temperature toner in office printers running eight hours per day, can cut electricity bills by up to 30% compared with conventional toner systems. This figure tells buyers that toner selection is no longer just a supply decision — it is an energy cost decision. Vendors offering LFT-compatible solutions hold a pricing conversation that competitors using standard toner formulations cannot easily match.

A total cost of ownership analysis cited by Hongcai Color Tech found that combining lower electricity use, longer component life, and reduced cartridge use can yield overall printing cost reductions of up to 40% in high-volume environments. For enterprise procurement teams managing thousands of printing devices, a 40% cost reduction is a procurement-level event — not a product feature.

Laser printing adoption in corporate and educational institutions continues to expand toner consumption volumes. Bulk printing requirements in emerging economies add a second demand layer, particularly across South and Southeast Asia. These economies are investing in printing infrastructure at a pace that outpaces legacy markets, reshaping where volume growth originates over the next decade.

Key Takeaways

- The Global Printing Toners Market was valued at USD 4.4 billion in 2025 and is forecast to reach USD 6.8 billion by 2035 at a CAGR of 4.6% during the forecast period 2026 to 2035.

- Polyester leads with a 41.3% share due to its thermal stability and cost efficiency in laser printing applications.

- Vials hold the dominant position with a 27.5% share among toner packaging formats.

- Polymers dominate with a 65.9% share, reflecting their widespread use in standard and specialty toner formulations.

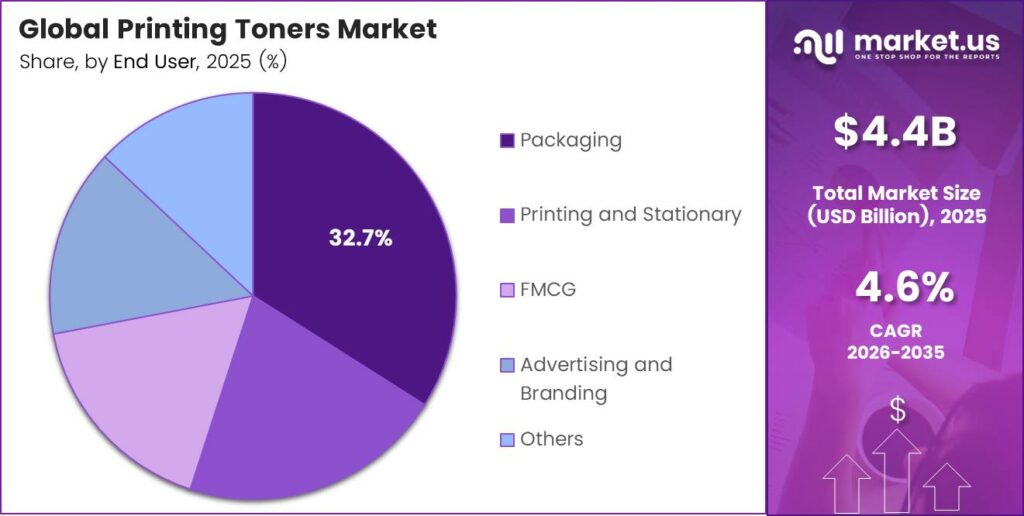

- The Packaging segment leads with a 32.7% share, driven by high-volume label and packaging print demand.

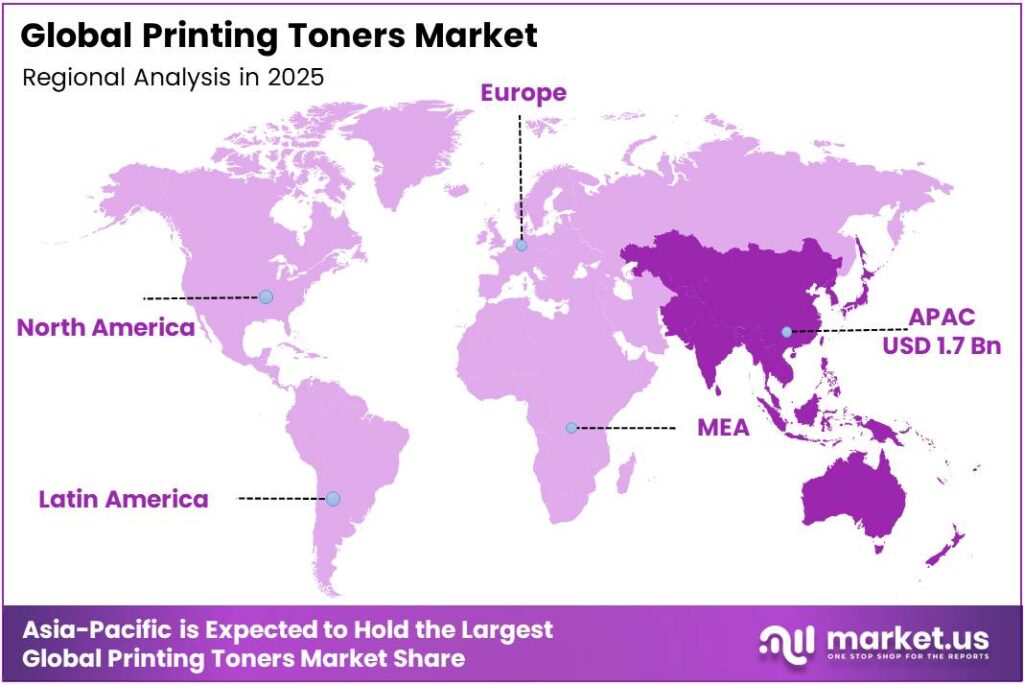

- Asia-Pacific dominates the regional landscape with a 39.1% share, valued at USD 1.7 billion.

Product Analysis

Polyester dominates with 41.3% due to superior thermal stability and cost efficiency.

In 2025, Polyester held a dominant market position in the By Raw Material segment of the Printing Toners Market, with a 41.3% share. Its thermal bonding properties align precisely with standard laser fusing temperatures, reducing print defects and cartridge failure rates. For toner manufacturers, polyester resin availability and processing consistency lower production costs, which translates directly into competitive cartridge pricing at scale.

Styrene-Acrylic serves as the preferred alternative resin where gloss finish and color vibrancy are prioritized over pure cost efficiency. It performs strongly in color laser applications used in advertising and creative printing. However, its higher input costs relative to polyester limit its penetration in price-sensitive bulk print environments, keeping it positioned as a specialty rather than a volume-driving material.

Packaging Type Analysis

Vials dominate with 27.5% due to precision dosing and contamination control in toner handling.

In 2025, Vials held a dominant market position in the By Packaging Type segment of the Printing Toners Market, with a 27.5% share. Their sealed format minimizes toner dust exposure during storage and transfer, a critical factor for both occupational safety compliance and print consistency. This functional advantage makes vials the default choice for high-precision toner applications where contamination directly affects output quality.

Cartridges carry the highest integration value in the packaging segment, combining toner storage with a printer-ready delivery mechanism. Their all-in-one design reduces handling steps for end users, making them the dominant format in office and consumer printing environments. Cartridge format locks toner consumption to replacement cycles, which creates predictable demand patterns — a structural advantage for suppliers managing inventory.

Material Analysis

Polymers dominate with 65.9% due to process versatility and broad compatibility across printer platforms.

In 2025, Polymers held a dominant market position in the By Material segment of the Printing Toners Market, with a 65.9% share. Polymer-based toners work across laser, LED, and digital printing systems without requiring hardware modification, making them the default material for both OEM and compatible toner producers. Their formulation flexibility allows manufacturers to tune particle size and charge properties for specific printer models, reducing cross-compatibility failures at scale.

Glass materials in toner applications serve specialized industrial and security printing sectors where standard polymer toners cannot meet substrate adhesion or temperature resistance requirements. Glass-based toner formulations fuse permanently to ceramic and glass surfaces, creating a niche in industrial marking, electronics labeling, and decorative printing. Their higher production cost and narrow application range keep volume limited, but they serve markets where no polymer alternative meets technical specifications.

End-User Analysis

Packaging dominates with 32.7% due to high-volume label and barcode printing requirements in logistics.

In 2025, Packaging held a dominant market position in the By End User segment of the Printing Toners Market, with a 32.7% share. E-commerce logistics and retail supply chains require continuous, high-speed label printing where toner-based systems deliver the throughput and durability that inkjet alternatives cannot consistently match. This structural dependency on printed labels ties packaging-sector toner demand directly to shipping volume growth, creating a demand floor that remains insulated from paperless workflow trends.

Printing and Stationery encompasses commercial print shops, copy centers, and office supply retailers that maintain toner-intensive operations across multiple device types. This segment sustains volume through contracted replenishment agreements rather than individual purchases, which stabilizes revenue predictability for suppliers. However, managed print service expansion is gradually shifting consumable procurement control from end users to service providers in this segment.

Key Market Segments

By Raw Material

- Polyester

- Styrene-Acrylic

- Specialty Polymers

- Others

By Packaging Type

- Vials

- Cartridges

- Ampoules

- Prefilled Syringes

- Infusion Solutions Bottles

- Infusion Solutions Bags

- Containers

- Others

By Material

- Polymers

- Glass

By End User

- Packaging

- Printing and Stationery

- FMCG

- Advertising and Branding

- Others

Emerging Trends

High-Yield Cartridges and IoT-Enabled Toner Monitoring Redefine Operational Efficiency Standards

Remanufactured and compatible toner cartridges now command attention in cost-sensitive markets where original equipment pricing creates budget pressure. The HP 336X high-yield toner delivers 13,700 pages per cartridge — a yield that illustrates how high-output formats reduce per-page cost and cartridge swap frequency simultaneously.

IoT-enabled toner monitoring systems integrate directly with managed print service platforms, allowing suppliers to trigger automatic toner replenishment before devices run empty. This shift moves toner procurement from reactive ordering to predictive inventory management.

Nanotechnology-based toner formulations deliver finer particle sizes that improve image resolution and reduce toner consumption per page. Creative industries applying toner for high-definition advertising materials and branded print collateral represent the clearest early adopter base for nano-toner products as they scale from specialty to broader commercial availability.

Drivers

Laser Printing Expansion Across Commercial, Industrial, and Institutional Sectors Accelerates Toner Consumption

Commercial and industrial sectors have expanded high-speed digital printing deployments to meet throughput demands that analog systems cannot fulfill. HP Planet Partners has recycled more than 1 billion print cartridges globally across over 60 countries, demonstrating the scale at which institutional laser printing generates consumable throughput that suppliers must service continuously.

Corporate and educational institutions operate laser printing fleets under managed service contracts that guarantee toner replenishment on a scheduled basis. This procurement model insulates supplier revenue from demand variability and ensures that fleet expansion — not reduction — drives contract renewal negotiations.HP reported collecting 11,039 metric tonnes of cartridges and containers through its Planet Partners program.

Bulk printing requirements in emerging economies create a second demand driver that operates independently of mature market trends. Businesses in South and Southeast Asia, Latin America, and parts of Africa are expanding printing capacity to support documentation-intensive commerce, regulatory compliance, and retail operations. This infrastructure build-out translates into volume toner purchases at price points that favor cost-efficient bulk supply formats over premium OEM cartridges.

Restraints

Environmental Regulations on Chemical Toner Production and Paperless Workflow Adoption Constrain Market Expansion

Regulatory agencies in North America and Europe have tightened controls on volatile organic compounds and chemical emissions linked to toner production and printer operation. Traditional toner systems require fusing temperatures of around 200°C, a thermal threshold that drives both energy consumption and regulatory scrutiny over component longevity and emissions per device cycle.

Paperless workflow adoption in enterprise environments reduces total print volume across document-intensive functions, including invoicing, HR documentation, and internal communications. Cloud document management platforms and electronic signature adoption have removed paper steps from processes that previously generated consistent toner consumption.

Compliance costs create an asymmetric burden between large OEM toner producers and smaller compatible cartridge manufacturers. Larger firms absorb reformulation investment across high production volumes, while smaller producers face margin compression when regulatory changes require material substitutions. This dynamic reduces supplier diversity over time, concentrating market share among firms with the R&D capacity to continuously reformulate ahead of regulatory deadlines.

Growth Factors

Eco-Friendly Toner Formulations and Managed Print Services Open Durable Revenue Channels for Suppliers

Eco-friendly and recyclable toner formulations address the intersection of regulatory pressure and enterprise sustainability commitments. Cartridge reuse reduces CO₂ emissions by 45% to 60% compared to non-reuse options — a reduction magnitude that sustainability-oriented procurement teams can quantify against their corporate carbon targets and use to justify supplier switching decisions.

Managed print services create a recurring revenue structure that ties toner replenishment to device monitoring contracts rather than ad hoc purchasing. Suppliers embedded in managed service agreements gain predictable volume commitments and reduced price competition because switching costs extend beyond toner pricing to include service reintegration.

Technological advancement in color printing expands toner consumption within creative industries that previously relied on offset printing for high-quality output. Xerox has manufactured 1.7 million toner units using recovered cartridge materials, with select products containing up to 47% post-consumer recycled plastic.

Regional Analysis

Asia-Pacific Dominates the Printing Toners Market with a Market Share of 39.1%, Valued at USD 1.7 Billion

Asia-Pacific holds 39.1% of the global printing toners market, valued at USD 1.7 billion. China, Japan, South Korea, and India anchor this position through large-scale commercial printing, packaging manufacturing, and electronics documentation requirements. The region’s manufacturing density creates embedded toner demand at an industrial scale, while expanding SME sectors in India and Southeast Asia add a fast-growing secondary consumption layer that mature markets do not replicate.

North America maintains a substantial market position driven by high laser printer penetration in corporate environments and institutional procurement through managed print service contracts. The region’s regulatory framework around chemical emissions has pushed the adoption of reformulated toner products, creating a product differentiation opportunity for compliant suppliers. Enterprise document security requirements also sustain demand for toner-based printing in regulated sectors, including finance, healthcare, and legal services.

Europe’s printing toner demand reflects the region’s dual emphasis on operational efficiency and environmental compliance. EU chemical regulations drive reformulation investment among suppliers serving this market, while sustainability procurement standards in large corporates and public sector bodies accelerate adoption of eco-formulated and recycled-content toner products. Germany, France, and the UK represent the highest-volume markets, with commercial print and packaging applications generating consistent toner consumption at scale.

Latin America represents a volume growth region where affordable printing infrastructure expansion drives toner demand across the SME and government sectors. Brazil and Mexico lead regional consumption, supported by growing retail, logistics, and documentation-intensive commerce. Price sensitivity shapes supplier strategy here — compatible and remanufactured toner cartridges capture a significant share because total cost of ownership arguments resonate strongly with budget-constrained institutional and commercial buyers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

HP Inc. holds the broadest cartridge ecosystem in the global printing toner market, with products spanning consumer, SME, and enterprise laser printing. HP’s strategic advantage lies in its closed-loop supply model — its Planet Partners recycling program operates across more than 60 countries, creating a reverse logistics network that competitors without comparable infrastructure cannot replicate at an equivalent scale or credibility.

ACM Technologies positions itself within the compatible and remanufactured toner segment, serving distributors and resellers that supply cost-sensitive commercial print environments. Its strategic value derives from manufacturing flexibility — producing cartridges compatible with multiple OEM printer platforms allows ACM to serve accounts that have mixed-brand device fleets. This multi-platform compatibility reduces the barrier to adoption for buyers seeking alternatives to single-OEM supply dependency.

Xerox Corporation differentiates through its circular economy manufacturing model. Xerox has produced toner units using recovered cartridge materials, and some of its toner products contain post-consumer recycled plastic. This positions Xerox not merely as a toner supplier but as a compliance partner for enterprise buyers with mandatory recycled-content procurement requirements — a positioning that price-only competitors cannot access.

Panasonic approaches the toner market through integration with its broader document management and office automation product portfolio. Toner supply connects to Panasonic’s device ecosystem, where consumable compatibility and quality assurance are embedded in long-term service agreements. This device-centric strategy creates account retention through integration rather than price competition, giving Panasonic pricing stability in segments where commodity toner suppliers compete primarily on margin.

Key Players

- HP Inc.

- ACM Technologies

- Xerox Corporation

- Panasonic

- IMEX Co. Ltd.

- Lotte Fine Chemicals

- Toshiba

- Epson

- Canon

- Citizen-Systems

- Konica Minolta

- IBM

- Brother International Corporation

- Lexmark

Recent Developments

- In 2025, HP officially launched the new HP EvoCycle toner cartridge in France, describing it as the lowest carbon footprint cartridge in its range. The cartridge is manufactured using reused and recycled materials from returned genuine HP cartridges. While critical components like the drum and toner are new, the plastic housing and other parts are part of a circular loop.

- In 2025, ACM Technologies is described as a leading wholesale distributor of OEM and compatible ink and toner cartridges. Imaging industry publication ENX Magazine reported that ACM Technologies acquired Nectron International on January 6, 2025. This acquisition was also described as strategic for the wholesale distribution of ink and toner cartridges.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.4 Billion |

| Forecast Revenue (2035) | USD 6.8 Billion |

| CAGR (2026-2035) | 4.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Polyester, Styrene-Acrylic, Specialty Polymers, Others), By Packaging Type (Vials, Cartridges, Ampoules, Prefilled Syringes, Infusion Solutions Bottles, Infusion Solutions Bags, Containers, Others), By Material (Polymers, Glass), By End User (Packaging, Printing and Stationery, FMCG, Advertising and Branding, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | HP Inc., ACM Technologies, Xerox Corporation, Panasonic, IMEX Co. Ltd., Lotte Fine Chemicals, Toshiba, Epson, Canon, Citizen-Systems, Konica Minolta, IBM, Brother International Corporation, Lexmark |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |