Quick Navigation

Report Overview

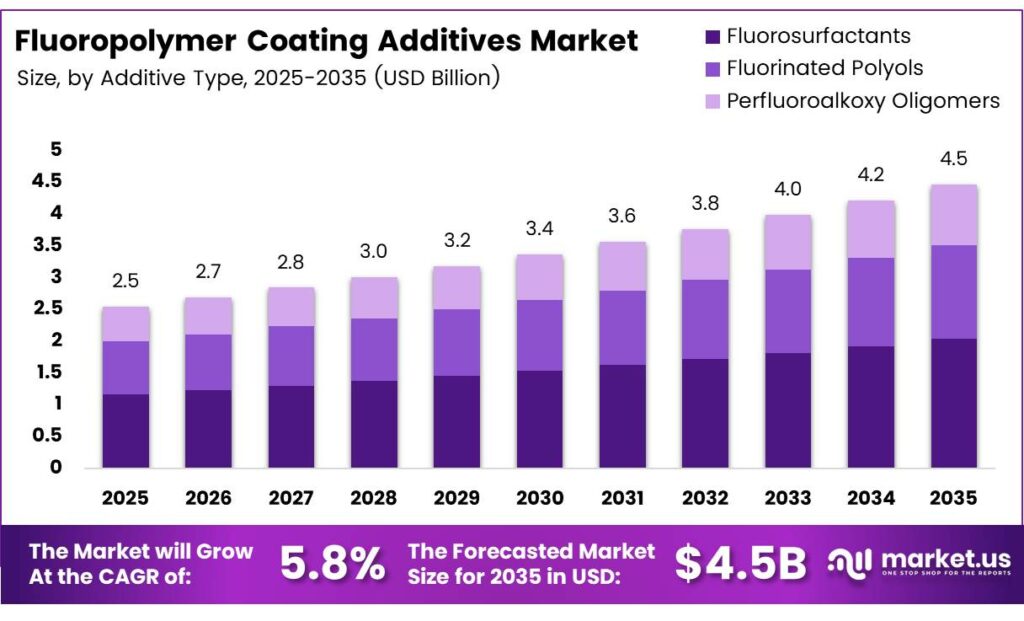

The Global Fluoropolymer Coating Additives Market size is expected to be worth around USD 4.5 billion by 2035 from USD 2.5 billion in 2025, growing at a CAGR of 5.8% during the forecast period 2026 to 2035.

Fluoropolymer coating additives are specialty chemical compounds that enhance surface performance across industrial coatings, paints, textiles, and electronics. These additives deliver non-stick, low-friction, corrosion-resistant, and dielectric properties. Their integration across manufacturing sectors reflects a structural shift toward high-performance surfaces rather than standard commodity coatings.

PTFE micropowders operate up to 260°C and retain cryogenic flexibility down to -200°C. This thermal range, unmatched by most organic additives, explains why aerospace and industrial buyers accept the higher cost — no substitute material covers both extremes within a single coating formulation.

Non-polymeric PFAS account for 94% of PFAS emissions, while fluoropolymers contribute only about 6%. This data point carries major strategic weight — it supports the scientific case for preserving fluoropolymer-based additives under regulatory review, giving compliant manufacturers a credible defense against blanket PFAS bans and positioning high-purity fluoropolymer grades as preferred alternatives.

Key Takeaways

- The Global Fluoropolymer Coating Additives Market is valued at USD 2.5 billion in 2025 and is forecast to reach USD 4.5 billion by 2035 at a CAGR of 5.8% during the forecast period 2026 to 2035.

- Fluorosurfactants lead with a 43.8% market share in 2025.

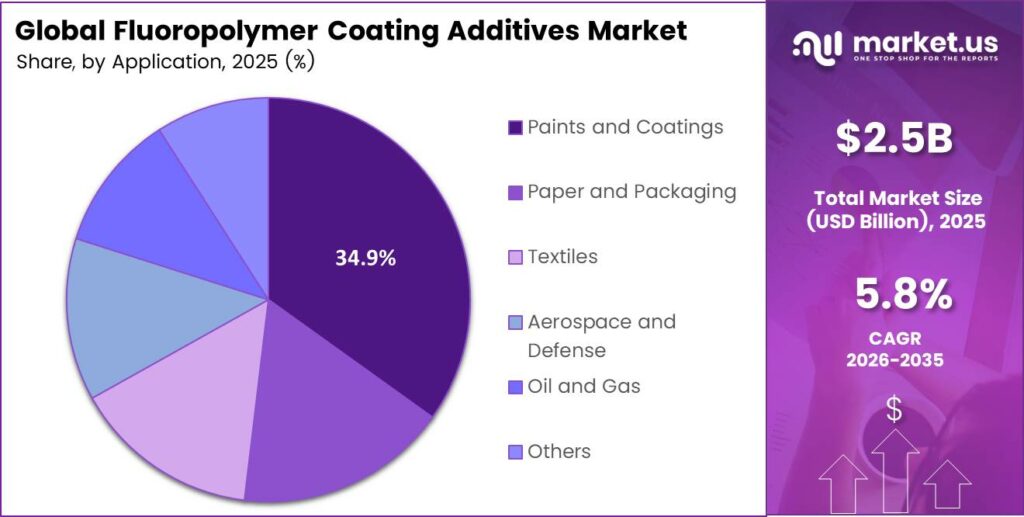

- Paints and Coatings holds the dominant position with a 34.9% share.

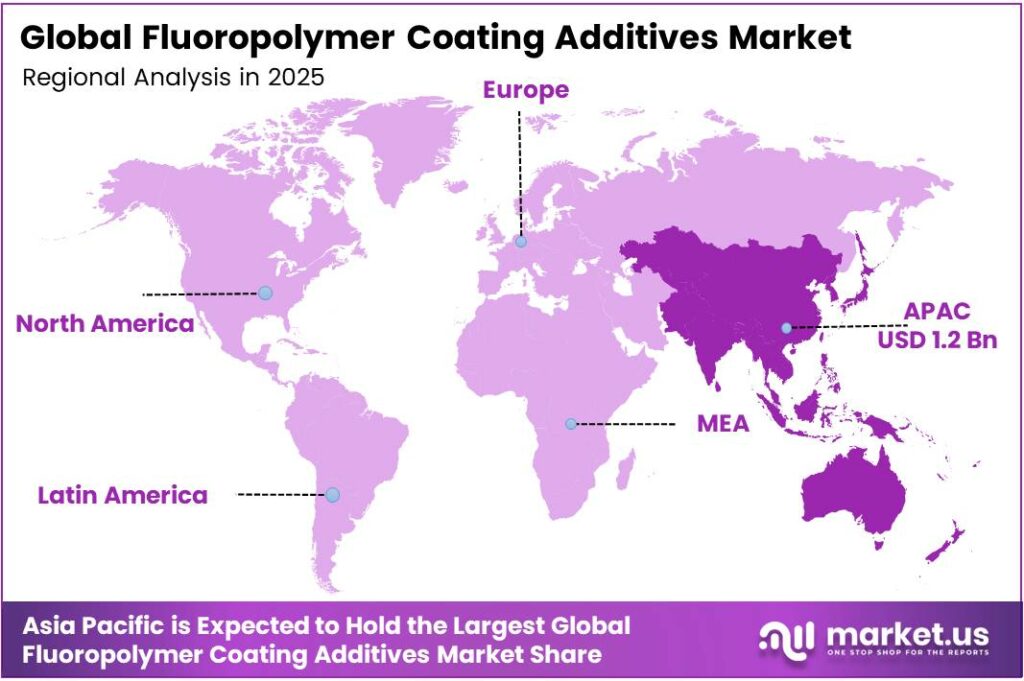

- Asia-Pacific dominates regional markets with a 46.3% share, valued at USD 1.2 billion.

Product Analysis

Fluorosurfactants dominate with 43.8% due to superior surface tension and wetting performance.

In 2025, Fluorosurfactants held a dominant market position in the By Additive Type segment of the Fluoropolymer Coating Additives Market, with a 43.8% share. Their ability to reduce surface tension at very low concentrations makes them irreplaceable in high-precision coating formulations. Industrial buyers in paints, electronics, and packaging consistently specify fluorosurfactants where uniform film formation is non-negotiable.

Fluorinated Polyols serve as reactive building blocks in high-durability coating systems, enabling chemical integration rather than surface-only additive action. Their structural role in polyurethane and epoxy coatings for aerospace and chemical processing environments supports longer service intervals. This functional advantage commands premium pricing and positions fluorinated polyols as preferred inputs among specification-driven buyers.

Application Analysis

Paints and Coatings dominate with 34.9% due to broad industrial and architectural coating demand.

In 2025, Paints and Coatings held a dominant market position in the By Application segment of the Fluoropolymer Coating Additives Market, with a 34.9% share. Industrial and architectural coating manufacturers integrate fluoropolymer additives to deliver anti-scratch, water-repellent, and low-friction surfaces at scale. This segment’s share reflects both the volume of global paint production and the specification shift toward performance-enhanced products.

Paper and Packaging carries strong commercial volume driven by food-contact and moisture-barrier requirements. Fluoropolymer additives allow paper and flexible packaging substrates to resist grease, water, and heat without heavyweight laminate structures. However, tightening food-contact regulations on PFAS compounds now pressure manufacturers to qualify low-PFAS or PFAS-free alternatives, reshaping procurement strategies across this sub-segment.

Textiles represent an application segment undergoing reformulation pressure as brands face consumer and regulatory scrutiny on PFAS-containing durable water repellents (DWR). Fluoropolymer additives historically delivered superior DWR performance unmatched by hydrocarbon alternatives. Consequently, textile producers face a clear fork: invest in next-generation fluoropolymer chemistries meeting new standards, or accept performance trade-offs with non-fluorinated solutions.

Key Market Segments

By Additive Type

- Fluorosurfactants

- Fluorinated Polyols

- Perfluoroalkoxy Oligomers

By Application

- Paints and Coatings

- Paper and Packaging

- Textiles

- Aerospace and Defense

- Oil and Gas

- Others

Emerging Trends

PFAS-Free Technologies, Nanotechnology Integration, and Smart Coatings Redefine Fluoropolymer Additive Development

The shift toward PFAS-free fluoropolymer additive technologies has moved from a regulatory aspiration to an active product development mandate. Major coating manufacturers now allocate R&D budgets specifically to next-generation fluoropolymer chemistries that deliver equivalent surface performance without regulated PFAS structures. Early movers who qualify compliant alternatives before mandated deadlines will capture specification positions that lock out slower competitors.

Nanotechnology integration unlocks performance levels that bulk fluoropolymer additives cannot reach. The OPTOOL anti-smudge fluorine coating reduces glass-substrate coefficient of friction by 50% — a result achieved through nanoscale surface architecture rather than increased fluoropolymer loading. This approach signals that future competitive advantage in coating additives will come from precision material engineering, not simply higher additive concentrations.

Multi-functional coatings that combine anti-fouling and anti-corrosion properties simultaneously represent the next specification tier for industrial and marine buyers. PTFE-0104 micronized PTFE established commercial specifications with a Dv50 particle size of 4–6 μm, Dv90 of 8 μm, and a melting point of 320–330°C. These tight particle size distributions and high thermal thresholds address the precision coating needs of electronics and advanced industrial applications, where inconsistent particle morphology directly degrades coating uniformity and dielectric performance.

Drivers

High-Performance Surface Requirements Across Industrial Sectors Push Fluoropolymer Additive Adoption

Industrial manufacturers across chemical processing, marine, and automotive sectors now specify fluoropolymer coating additives as baseline requirements — not optional upgrades. Non-stick and low-friction surface performance directly reduces energy consumption, maintenance frequency, and equipment replacement costs. This operational calculus makes fluoropolymer additives a cost-justified input in capital-intensive industrial environments.

The thermal performance data reinforces why industrial buyers accept the premium. PTFE micropowders operate up to 260°C and retain cryogenic flexibility down to -200°C. No single competing additive class covers both thermal extremes — which means buyers in aerospace, automotive, and chemical processing face a binary choice: specify fluoropolymers or accept coating failures at temperature boundaries.

Corrosion resistance further amplifies adoption across marine and chemical plant environments. Fluoropolymer-enhanced coatings protect steel and alloy substrates against acids, solvents, and saltwater exposure, where conventional coatings degrade within months. A Graphite/PTFE/PEEK coating with 14 wt% graphite reduced the coefficient of friction by 34.5%, increased bearing capacity by 59.9%, and reduced wear rate by 56.7% — quantifying the structural advantage that drives specification decisions in demanding industrial applications.

Restraints

PFAS Regulatory Restrictions and High Production Costs Constrain Market Expansion

Regulators worldwide treat PFAS compounds as a priority environmental concern, creating direct compliance costs for fluoropolymer additive manufacturers and their customers. Enforceable PFAS limits in drinking water now stand at 4 parts per trillion for PFOA and PFOS — a threshold that reflects zero regulatory tolerance for contamination. Manufacturers face mandatory testing, reformulation investment, and potential product withdrawals if compliance gaps surface.

PTFE Micro-powder PF-598 reached commercial availability with ≥98% whiteness, a D50 particle size of 4.0–5.0 μm, and a bulk density of 250–550 g/L. Its high whiteness and controlled particle distribution make it well-suited for decorative and functional coating applications where optical clarity and surface uniformity are simultaneous requirements — expanding the addressable application base for PTFE micropowder additives.

These dual constraints — regulatory liability and production cost — create a market where only well-capitalized suppliers with compliant product portfolios can sustain participation. Smaller producers lacking the R&D budget to reformulate around PFAS restrictions face product phase-out risk. Therefore, market consolidation among compliant, technically advanced manufacturers will likely intensify as regulatory timelines tighten through the forecast period.

Growth Factors

Renewable Energy, Eco-Friendly Formulations, and Medical Applications Open New Revenue Channels

Renewable energy infrastructure creates a structurally new demand channel for fluoropolymer coating additives. Solar panel backsheets, wind turbine blades, and electrolyzer components require coatings that withstand UV exposure, humidity cycles, and mechanical stress across decades of service life. These performance requirements align directly with fluoropolymer additive capabilities, making the energy transition a genuine volume driver rather than a speculative opportunity.

Innovation in low-VOC and eco-friendly fluoropolymer additive formulations addresses the regulatory headwind directly. A 5% Si3N4-filled PTFE composite reduced wear rate by 95% versus pure PTFE — demonstrating that composite approaches can amplify performance while reducing total fluoropolymer loading per application. This allows formulators to achieve better results with less material, supporting both cost efficiency and environmental compliance simultaneously.

Medical device and pharmaceutical equipment coatings represent a high-margin, specification-locked growth channel. Fluoropolymer additives deliver biocompatibility, chemical resistance, and sterilization tolerance required by regulatory bodies across these industries. Additionally, rapid industrialization in developing economies — particularly across Southeast Asia and India — generates fresh demand for advanced coating solutions in manufacturing facilities that previously relied on lower-specification products.

Regional Analysis

Asia-Pacific Dominates the Fluoropolymer Coating Additives Market with a Market Share of 46.3%, Valued at USD 1.2 Billion

Asia-Pacific holds 46.3% of the global Fluoropolymer Coating Additives Market, valued at USD 1.2 billion. This dominance reflects the region’s concentration of electronics manufacturing, shipbuilding, and chemical processing industries — all of which use fluoropolymer-enhanced coatings as standard operating inputs. China, Japan, and South Korea individually represent high-volume, specification-driven demand anchors that sustain regional leadership through the forecast period.

North America maintains a structurally strong position anchored by mature aerospace, defense, and chemical processing industries that specify high-performance fluoropolymer coatings. EPA regulatory actions, PFAS infrastructure funding, and enforceable drinking water limits accelerate reformulation investment among domestic manufacturers. Compliance-driven product development activity in this region positions

Europe operates under the most restrictive PFAS regulatory framework globally, with proposed EU restrictions covering over PFAS substances reshaping the product landscape. This regulatory intensity accelerates the commercial transition to PFAS-free and low-PFAS fluoropolymer alternatives faster than any other region.

The Middle East and Africa market centers on oil and gas infrastructure protection, where fluoropolymer coatings guard pipelines, offshore platforms, and refinery equipment against chemical corrosion and extreme heat. GCC countries drive the majority of regional consumption through sustained capital expenditure in energy infrastructure. Additionally, desalination plant construction in the region creates a growing application surface for fluoropolymer-enhanced protective coatings.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Flame Spray Coating Company positions itself as a specialist thermal spray solutions provider serving high-wear and high-temperature industrial environments. Its technical depth in fluoropolymer application processes — rather than chemistry alone — creates a service-led competitive model that differentiates from commodity additive suppliers. This approach builds specification loyalty in aerospace and heavy industrial accounts where application precision directly determines coating lifetime.

A & A Thermal Spray Coatings competes through application engineering expertise, serving clients who require customized fluoropolymer coating systems rather than off-the-shelf formulations. Their ability to tailor coating processes for specific substrates and performance requirements makes them a preferred partner for OEM and MRO customers across defense, pumps, and rotating equipment.

Metallisation Limited operates as a technology-focused thermal spray equipment and process provider with fluoropolymer coating capabilities integrated into its broader surface engineering portfolio. Its strength in combining coating chemistry with application technology positions the company to serve clients seeking end-to-end surface performance solutions.

AMETEK Inc. brings scale and materials science capability across its engineered materials divisions to address fluoropolymer additive applications in electronics, aerospace, and industrial markets. Its diversified product portfolio reduces dependence on any single application segment — a structural advantage as individual end markets face regulatory or economic volatility.

Key Players

- A & A Thermal Spray Coatings

- Flame Spray Coating Company

- Metallisation Limited

- AMETEK Inc.

- Praxair S.T. Technology, Inc.

- DuPont

- Dow

- The Chemours Company

- Eastman Chemical Company

- Akzo Nobel N.V.

- ELEMENTIS PLC

- BASF SE

- BYK-Chemie GmbH

Recent Developments

- In 2025, A&A continues positioning around custom metal, ceramic, cermet, and hardfaced thermal spray coatings, with machining/grinding support. Its site also highlights a U.S. Department of Defense Achievement Award and coating applications, including chemical resistance, corrosion protection, thermal barriers, and wear resistance.

- In 2025, Metallisation has a direct fluoropolymer-adjacent application: reinforced cookware systems where arc-sprayed stainless steel or plasma-sprayed ceramic is used to reinforce fluoropolymer coatings and extend working life. It also supplies/backs thermal-spray equipment, guidance, and training for in-house coating operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.5 Billion |

| Forecast Revenue (2035) | USD 4.5 Billion |

| CAGR (2026-2035) | 5.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Additive Type (Fluorosurfactants, Fluorinated Polyols, Perfluoroalkoxy Oligomers), By Application (Paints and Coatings, Paper and Packaging, Textiles, Aerospace and Defense, Oil and Gas, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Flame Spray Coating Company, A & A Thermal Spray Coatings, Metallisation Limited, AMETEK Inc., Praxair S.T. Technology, Inc., DuPont, Dow, The Chemours Company, Eastman Chemical Company, Akzo Nobel N.V., ELEMENTIS PLC, BASF SE, BYK-Chemie GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |