Quick Navigation

Report Overview

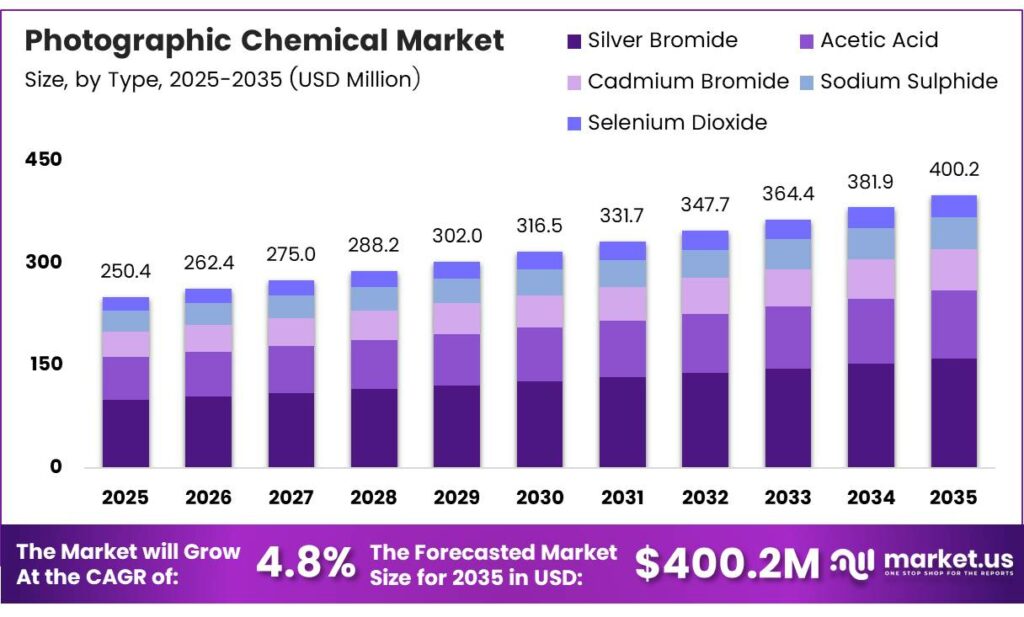

The Global Photographic Chemical Market size is expected to be worth around USD 400.2 million by 2035 from USD 250.4 million in 2025, growing at a CAGR of 4.8% during the forecast period 2026 to 2035.

Photographic chemicals remain technically irreplaceable in several precision applications. Silver bromide, acetic acid, sodium sulphide, and selenium dioxide each serve distinct processing functions that digital substitution cannot replicate at the same resolution or tonal depth. This chemical specificity creates a structurally defensible market even as overall analog volumes contract.

Regulatory pressure on hazardous chemical disposal and the shift toward digital imaging represent structural headwinds. However, growth in scientific research imaging, forensic analysis, and luxury fine art printing is creating new procurement channels that partially offset volume losses in mainstream commercial photography.

Processing efficiency data reinforces the market’s technical depth. A 5-litre concentrate of ILFORD Rapid Fixer can process 600 rolls of 35mm film, 2,000 RC prints, and 1,000 fibre prints at 8×10 inches. This throughput capacity signals that fixer chemistry supports high-volume commercial workflows — not just niche artisan use — sustaining bulk procurement by professional processing facilities.

Key Takeaways

- The Global Photographic Chemical Market was valued at USD 250.4 million in 2025 and is forecast to reach USD 400.2 million by 2035 at a CAGR of 4.8% during the forecast period 2026 to 2035.

- Silver Bromide leads the By Type segment with a 34.2% share.

- Color Processing leads the By Processing Method segment with a 43.8% share.

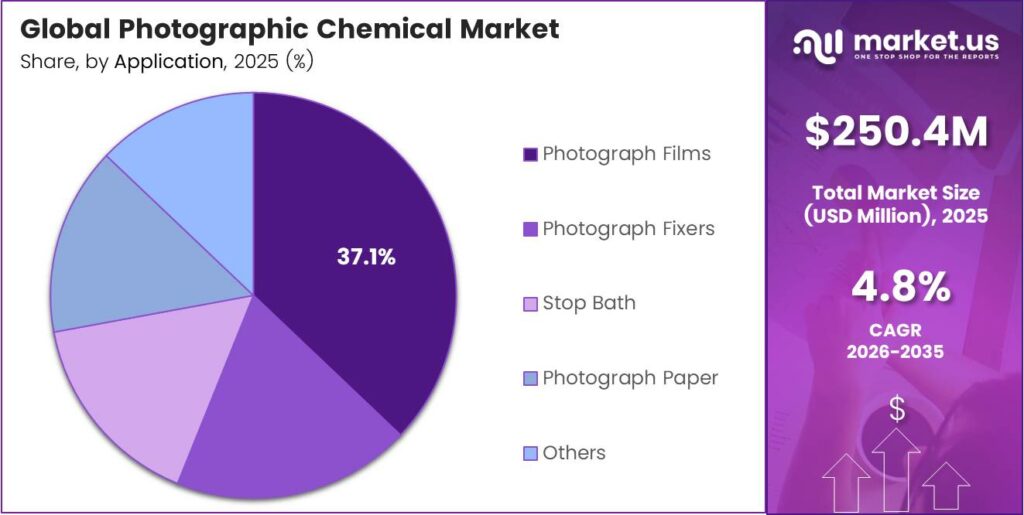

- Photograph Films account for 37.1% of the By Application segment, the largest single application category.

- Business end-users represent 62.7% of total demand, confirming commercial applications as the primary revenue driver.

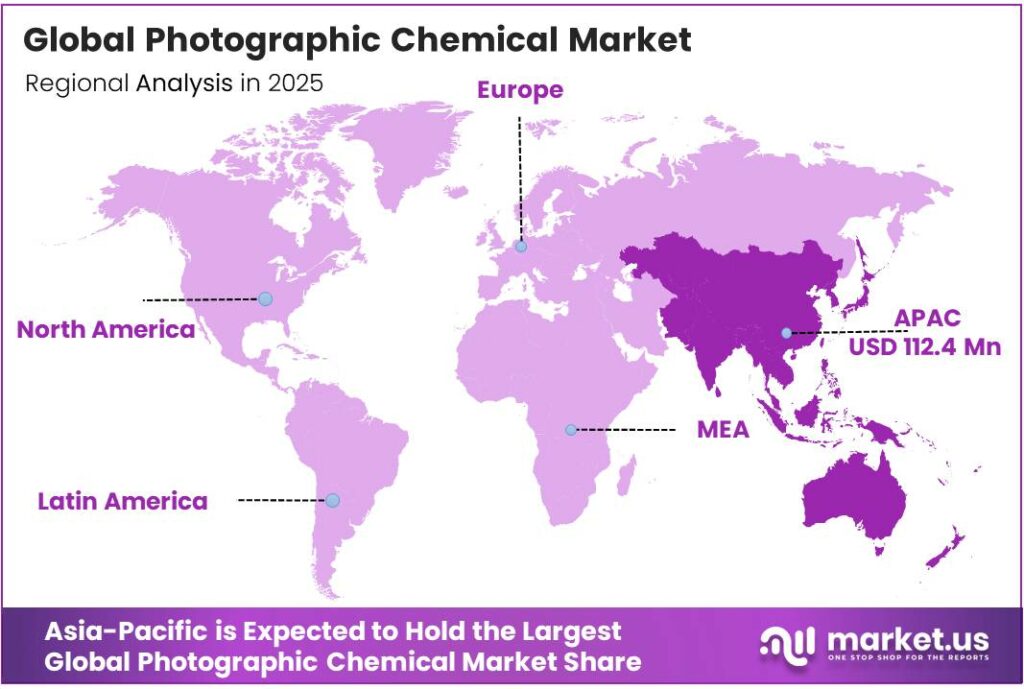

- Asia-Pacific holds the largest regional share at 44.9% of the global market.

Product Analysis

Silver Bromide dominates with 34.2% due to its irreplaceable role in light-sensitive emulsions.

In 2025, Silver Bromide held a dominant market position in the By Type segment of the Photographic Chemical Market, with a 34.2% share. Its light-sensitivity properties remain technically unmatched for black-and-white and color film emulsions. Moreover, no synthetic alternative replicates its tonal resolution, making it structurally entrenched in both professional film manufacturing and archival print production.

Acetic Acid serves as the foundational stop bath compound across both color and black-and-white processing workflows. It halts developer activity instantly, preventing over-development and protecting fixer chemistry from premature exhaustion. Consequently, its procurement is directly tied to processing volume — every film roll and print processed consumes acetic acid at a fixed ratio, creating predictable industrial demand.

Processing Method Analysis

Color Processing dominates with 43.8% due to a broad professional and commercial application base.

In 2025, Color Processing held a dominant market position in the By Processing Method segment of the Photographic Chemical Market, with a 43.8% share. Standard C-41 color processing requires temperature control at 38°C with an active processing time of 15–20 minutes, demanding precise chemical formulation and consistent replenishment. This technical complexity sustains professional-grade chemical procurement and limits casual substitution.=

Black and White Reversal Processing serves as the entry point for specialty slide and transparency film production, primarily used by cinematographers and fine art practitioners. Reversal chemistry requires additional bleaching and re-exposure steps, increasing chemical volume per roll compared to negative processing. Consequently, reversal processing commands premium chemical pricing and generates higher per-unit revenue for suppliers.

Application Analysis

Photograph Films dominates with 37.1% due to sustained volume procurement by professional film shooters.

In 2025, Photograph Films held a dominant market position in the By Application segment of the Photographic Chemical Market, with a 37.1% share. Film-based capture generates direct and recurring chemical demand across developer, stop bath, and fixer stages for every roll processed. Moreover, the expanding film shooting community — from professional photojournalists to fine art practitioners — sustains consistent consumption volumes that support predictable supplier revenue.

Photograph Paper drives chemical demand in darkroom printing, where developer and fixer consumption scales directly with print output volume. The distinction between RC and fibre-based paper affects fixer consumption significantly — fibre prints require longer fixing times, increasing chemical use per print. Additionally, the luxury fine art print market’s preference for fibre-based paper is sustaining above-average chemical consumption per unit output.

End Use Analysis

Business dominates with 62.7% due to sustained institutional and commercial procurement cycles.

In 2025, Business held a dominant market position in the By End-use segment of the Photographic Chemical Market, with a 62.7% share. Commercial buyers — including professional processing labs, medical imaging centers, industrial inspection facilities, and archival institutions — purchase chemicals in volume under recurring contracts. This procurement structure provides chemical suppliers with revenue predictability that consumer-facing sales cannot replicate.

Consumer end-users represent a structurally smaller but commercially strategic segment. Home darkroom enthusiasts, independent analog photographers, and fine art students constitute the core consumer buyer base. However, the growing cost advantage of home processing, lower than lab fees, is drawing new participants into chemical purchasing, gradually expanding this segment’s volume contribution beyond its current minority share.

Key Market Segments

By Type

- Silver Bromide

- Acetic Acid

- Cadmium Bromide

- Sodium Sulphide

- Selenium Dioxide

- Others

By Processing Method

- Color Processing

- Black and White Negative Processing

- Black and White Reversal Processing

- Others

By Application

- Photograph Films

- Photograph Fixers

- Stop Bath

- Photograph Paper

- Others

By End-use

- Business

- Consumer

Emerging Trends

Analog Revival and Smart Lab Integration Reshape Chemical Demand Patterns

Younger demographics are adopting film photography at measurable rates, converting cultural nostalgia into consistent chemical purchasing. This generational shift is not marginal — it is creating new processing communities that sustain demand for developer, fixer, and stop bath chemistry beyond the traditional professional base.

Smart lab technologies are entering photo processing workflows, enabling automated temperature control, chemical replenishment monitoring, and batch tracking. Standard C-41 processing demands precise 38°C temperature control across 15–20 minutes of active chemistry. This precision requirement is driving the adoption of automated processing equipment that integrates directly with chemical management systems.

Sustainable packaging and storage innovation is emerging as a competitive differentiator among photographic chemical suppliers. The replenishment rate of 600 ml per 30.5 m of 35mm film highlights how concentrated efficiency directly affects packaging volume requirements — making sustainable format design a commercially relevant product feature.

Drivers

Medical Imaging Demand and Analog Revival Sustain Chemical Processing Volume

High-resolution imaging requirements in medical diagnostics and industrial inspection sustain demand for silver bromide-based chemistry at precision-grade specifications. These institutional buyers cannot substitute digital capture where regulatory or archival standards mandate chemical-based output. Consequently, medical and industrial procurement anchors the business end-use segment’s 62.7% market share with low price sensitivity.

Professional artists and photographers are actively returning to analog film workflows, converting aesthetic preference into chemical procurement. ECP-2 fixer consumes approximately 66% less chemical per unit than ECN-2 fixer — 200 ml versus 600 ml per 100 feet of 35mm film. This efficiency differential lowers the per-roll cost of analog processing, making the economics of film photography more accessible to both professional and prosumer buyers.

Printing, packaging, and specialty imaging processes generate parallel chemical demand outside traditional photography. Archival and restoration activities — preserving historical photographic collections in museums and private archives — require film-grade chemical quality and consistent supply. Moreover, ILFOSTOP’s operational specifications — 10-second processing at 1+19 dilution — demonstrate that modern stop bath chemistry delivers precision control that supports high-throughput institutional workflows.

Restraints

Digital Imaging Transition and Hazardous Chemical Regulations Compress Market Volume

The broad commercial migration toward digital capture has structurally reduced the total addressable market for photographic chemicals over the past two decades. Mainstream photography studios, news agencies, and consumer labs have largely eliminated analog processing from their workflows. This volume loss is permanent in those segments, concentrating chemical demand among a narrowing base of specialized institutional and professional buyers.

Environmental regulations governing the disposal of silver-bearing fixer solutions, cadmium compounds, and acetic acid effluents impose compliance costs that increase operational barriers for smaller processing labs. The spiral tank washing method — using 5, 10, and 20 inversion cycles — reduces water consumption compared to continuous flow washing.

Regulatory divergence across geographies further complicates supply chain planning for chemical manufacturers. What is permissible in one jurisdiction may require reformulation or alternative compounds in another. Therefore, manufacturers serving both Asian and European markets must maintain multiple product variants, increasing production complexity and raising the minimum viable scale for profitable chemical manufacturing in this market.

Growth Factors

Eco-Friendly Formulations and Niche Application Expansion Open New Revenue Channels

Development of low-toxicity and biodegradable photographic chemical alternatives directly addresses the regulatory constraints limiting market participation. Manufacturers who bring compliant formulations to market first gain access to institutional buyers — hospitals, universities, government archives — that currently restrict or avoid chemical-based processing due to environmental policy mandates.

Fine art and luxury photographic printing represent a premium segment where buyers prioritize chemical quality over cost. Rotary film processors use up to 60% less chemistry per roll and process up to 8 rolls simultaneously. This throughput efficiency means that high-volume fine art studios can operate profitably at lower chemical consumption rates — improving margins for both the studio and the chemical supplier serving them.

Expansion into scientific research, forensic analysis, and hybrid imaging techniques combining chemical and digital methods creates demand outside traditional photography markets. ILFOTOL wetting agent at 1+200 dilution — 5 ml per litre — illustrates how precision low-concentration formulations serve technical applications beyond standard darkroom use.

Regional Analysis

Asia-Pacific Dominates the Photographic Chemical Market with a Market Share of 44.9%, Valued at USD 112.4 Million

Asia-Pacific holds a dominant 44.9% share of the global photographic chemical market, valued at USD 112.4 million in 2025. The region’s position reflects concentrated film manufacturing infrastructure in Japan, active analog photography communities in South Korea and China, and significant medical and industrial imaging procurement across the broader region. These structural advantages compound to sustain both volume and value leadership.

North America maintains a substantial share driven by archival and restoration activities in museums, universities, and federal institutions that mandate chemical-based photographic processes. The analog revival among professional fine art photographers on the US West Coast and in academic programs sustains specialty chemical demand.

Europe represents a historically mature market for photographic chemicals, with Germany, France, and the UK hosting active professional darkroom communities and archival institutions. Strict environmental regulations on chemical disposal create compliance complexity that raises barriers for smaller suppliers.

Latin America presents an emerging opportunity for photographic chemical suppliers as analog photography gains traction among creative professionals in Brazil and Mexico. Distribution infrastructure for specialty chemistry remains underdeveloped compared to North America and Europe, creating a first-mover advantage for suppliers who establish regional logistics partnerships.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Agfa-Gevaert Group maintains a strategic position across both consumer and institutional photographic chemical segments, with an established manufacturing scale that supports consistent formulation quality. Their dual presence in analog and digital imaging chemistry allows them to cross-sell to buyers transitioning between processing methods. This breadth creates defensible customer relationships that smaller specialty manufacturers cannot easily replicate.

BASF approaches the photographic chemical market from a broader specialty chemicals platform, giving it raw material cost advantages that pure-play photographic chemical manufacturers cannot match. Their capacity to reformulate compounds in response to evolving environmental regulations positions them favorably as compliance requirements tighten across European and Asian markets.

FOMA Bohemia spol s.r.o occupies a differentiated position as a European manufacturer serving the professional analog photography community with a focused product range. Their concentration on black-and-white film and chemistry aligns directly with the analog revival trend, where professional and fine art buyers prioritize consistency and provenance over price. FOMA benefits from the premiumization of analog photography without competing on volume economics against larger chemical manufacturers.

Bostick and Sullivan, Inc. targets the niche fine art and alternative process segment with specialty formulations for platinum-palladium, cyanotype, and other historical printing methods. This positioning insulates them from commodity pricing pressure in standard C-41 and black-and-white chemistry markets. Moreover, fine art buyers exhibit lower price sensitivity and greater loyalty to proven formulations, giving Bostick and Sullivan a stable, defensible customer base.

Key Players

- Agfa-Gevaert Group

- BASF

- FOMA Bohemia spol s.r.o

- Bostick and Sullivan, Inc.

- Fujifilm Corporation

- NET Corporation

- Eastman Kodak Company

- Hydrite Chemical Co

Recent Developments

- In 2025, Agfa reported stable-to-stronger performance in Digital Print & Chemicals, while traditional medical film continued to decline. Agfa also accelerated optimization of traditional film manufacturing, realizing €36m annualized savings by year-end 2025.

- In 2025, BASF’s most relevant adjacent development is portfolio restructuring in coatings/surface-treatment chemicals: BASF and Carlyle signed a binding agreement to sell automotive OEM coatings, refinish coatings, and surface treatment units at an €7.7 bn enterprise value. BASF will retain 40% equity and receive about €5.8bn pre-tax cash proceeds.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 250.4 Million |

| Forecast Revenue (2035) | USD 400.2 Million |

| CAGR (2026-2035) | 4.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Silver Bromide, Acetic Acid, Cadmium Bromide, Sodium Sulphide, Selenium Dioxide, Others), By Processing Method (Color Processing, Black and White Negative Processing, Black and White Reversal Processing, Others), By Application (Photograph Films, Photograph Fixers, Stop Bath, Photograph Paper, Others), By End-use (Business, Consumer) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Agfa-Gevaert Group, BASF, FOMA Bohemia spol s.r.o, Bostick and Sullivan, Inc., Fujifilm Corporation, NET Corporation, Eastman Kodak Company, Hydrite Chemical Co |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |