Quick Navigation

Report Overview

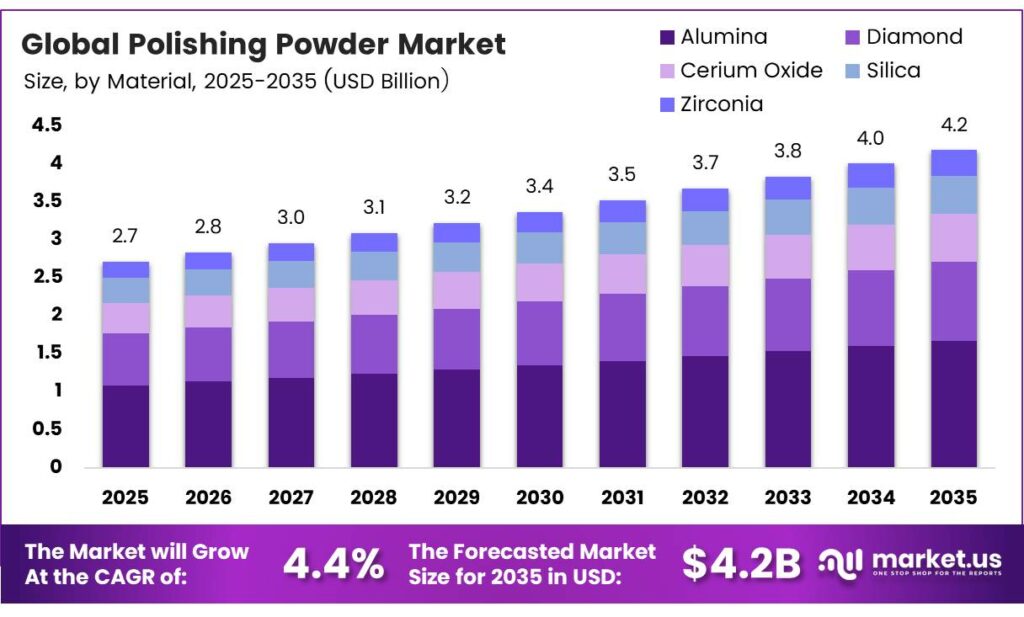

The Global Polishing Powder Market size is expected to be worth around USD 4.2 billion by 2035 from USD 2.7 billion in 2025, growing at a CAGR of 4.4% during the forecast period 2026 to 2035.

Polishing powder refers to abrasive materials — including alumina, cerium oxide, diamond, silica, and zirconia — used to achieve precise surface finishes across manufacturing, electronics, automotive, and aerospace industries. These materials remove microscopic surface irregularities, enabling components to meet strict tolerance and optical standards required in precision engineering.

A multi-stage polishing process using optimized slurry and powder conditions improved overall polishing efficiency by 26.7% compared with a traditional single-stage process for precision optical components, while also shortening overall process time. This finding signals that process design — not just material selection — now drives polishing performance, creating a market opening for suppliers who bundle formulation expertise with application engineering.

Cerium-oxide powder’s combination of fine particle size and high hardness eliminated one finishing step in large-scale glass lines, reducing total polishing steps by approximately 20% in documented production flows. Fewer process steps translate directly into lower labor costs and shorter production cycles — a value proposition that purchasing managers in high-volume glass manufacturing can quantify against competing abrasive solutions.

Key Takeaways

- The Global Polishing Powder Market is valued at USD 2.7 billion in 2025 and is forecast to reach USD 4.2 billion by 2035 at a CAGR of 4.4% during the forecast period 2026 to 2035.

- Alumina holds the dominant share at 34.8% within the polishing powder market.

- Metal Polishing leads with a 29.5% share, reflecting its broad industrial base.

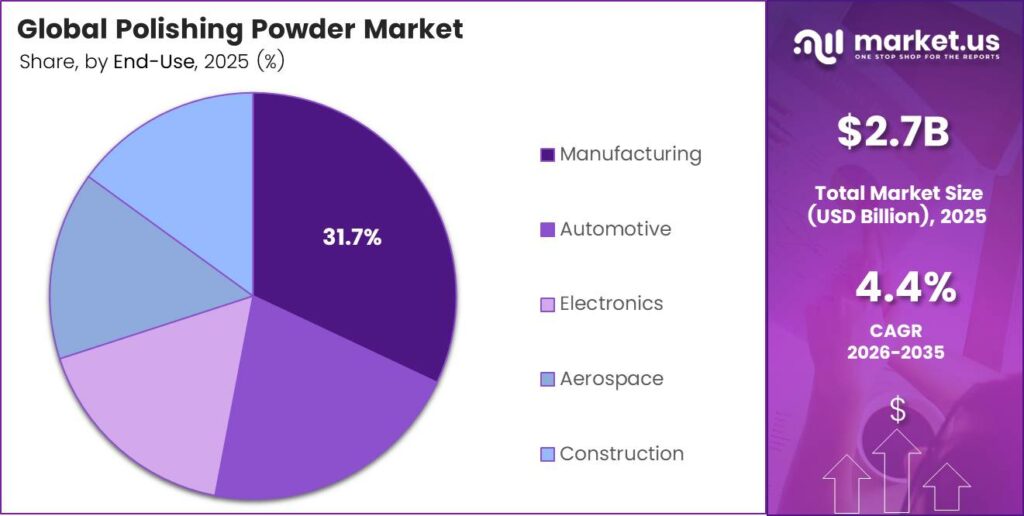

- Manufacturing accounts for 31.7%, the largest share among all end-use segments.

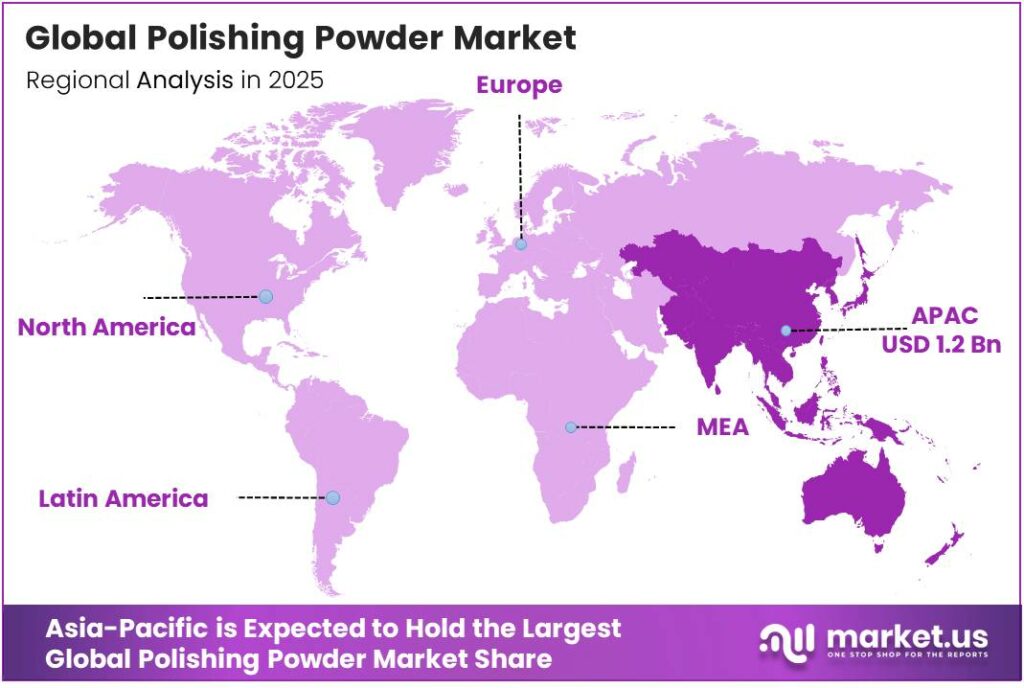

- Asia-Pacific dominates the regional landscape with a 44.6% share, valued at USD 1.2 billion.

Product Analysis

Alumina dominates with 34.8% due to broad industrial compatibility and low cost.

In 2025, Alumina held a dominant market position in the By Material segment of the Polishing Powder Market, with a 34.8% share. Its dominance reflects both cost efficiency and versatility across metal, plastic, and ceramic substrates. Manufacturers in high-volume production environments default to alumina because it delivers reliable material removal rates without requiring specialized equipment or formulation adjustments.

Diamond carries the highest performance ceiling within polishing abrasives. Its extreme hardness enables material removal on substrates — including silicon carbide wafers and advanced ceramics — where alumina and cerium oxide underperform. However, diamond’s cost position limits it to applications where surface specification tolerances justify the premium, making it a specialized tool rather than a volume product.

Application Analysis

Metal Polishing dominates with 29.5% due to the broad manufacturing industry demand for surface-finished metal components.

In 2025, Metal Polishing held a dominant market position in the By Application segment of the Polishing Powder Market, with a 29.5% share. The application spans fabricated metal parts across industrial machinery, consumer goods, and structural components. Its share reflects the sheer volume of metal components requiring surface finishing before assembly — a demand base that remains stable regardless of end-industry cyclicality.

Plastic Polishing serves as the surface-finishing layer for consumer electronics, automotive trim, and optical lens housings. Polishing compounds used on plastic substrates require formulations that remove surface haze without generating heat or micro-cracks. As lightweight plastic components replace metal in automotive and consumer device designs, this application segment captures an expanding share of overall polishing powder consumption.

End-Use Analysis

Manufacturing dominates with 31.7% due to high-volume, multi-material surface finishing requirements.

In 2025, Manufacturing held a dominant market position in the By End-Use segment of the Polishing Powder Market, with a 31.7% share. General manufacturing encompasses metal fabrication, industrial machinery, and precision component production — all of which require surface finishing as a standard production step. Its dominance reflects the breadth of the industrial base rather than a single concentrated demand source.

Automotive end-use combines high volumes with exacting surface specifications. Both structural metal parts and optical sensor housings in modern vehicles require polished surfaces that meet dimensional tolerances and aesthetic standards simultaneously. As electric vehicle production scales and sensor-dense autonomous platforms proliferate, the technical requirements placed on automotive polishing compounds intensify beyond what conventional abrasives can deliver.

Electronics drives the highest per-unit value within polishing powder consumption. Semiconductor wafer planarization, hard drive disk polishing, and display component finishing each represent technically specialized applications with zero tolerance for surface defects. This end-use segment’s commercial weight exceeds its volume share because the cost of a single defective wafer — running into thousands of dollars — makes polishing powder selection a high-stakes procurement decision.

Key Market Segments

By Material

- Alumina

- Diamond

- Cerium Oxide

- Silica

- Zirconia

By Application

- Metal Polishing

- Plastic Polishing

- Glass Polishing

- Automotive Polishing

- Electronic Polishing

By End-Use

- Manufacturing

- Automotive

- Electronics

- Aerospace

- Construction

Emerging Trends

Nano-Grade Formulations and Smart Manufacturing Redefine Polishing Powder Performance Standards

The polishing powder market moves decisively toward ultra-fine and nano-grade abrasive formulations. Precision applications in semiconductors and photonics require surface finishes that coarser grades cannot achieve. Controlling agglomeration and particle-size distribution in polishing powders reduces surface defectivity — scratches and pits — by more than 30% in advanced CMP processes.

Automation integration reshapes how polishing powder formulations are specified and consumed. Smart manufacturing environments generate real-time surface quality data that feeds back into polishing process parameters — adjusting slurry concentration, contact pressure, and powder grade mid-cycle. Co-doped CeO₂ polishing achieves an ultra-low Ra of 0.0117 nm on silicon wafers, a benchmark that manual processes cannot consistently replicate without automation.

Water-based and low-toxicity polishing compounds advance from niche preference to mainstream procurement requirement. Regulatory pressure on chemical waste disposal — particularly in the European Union and California — makes hazardous abrasive formulations a liability rather than a cost-neutral option.

Drivers

Semiconductor Precision Requirements and Multi-Industry Demand Drive Structural Consumption Growth in Polishing Powders

Semiconductor and electronics manufacturing now sets the performance floor for polishing powder quality. As chip architectures shrink below 5 nanometers, surface defects that were previously acceptable become yield-killing. Fluorine-doped CeO₂ powders with improved crystallinity increased the material removal rate by approximately 18–22% versus undoped CeO₂ powders while maintaining comparable surface roughness.

The automotive and aerospace industries reinforce polishing powder demand through volume and specification simultaneously. Meanwhile, a 2025 open-access study on environmentally friendly cerium-oxide-based slurry for K9 glass confirmed that newly formulated slurries achieved surface roughness reduction to the 1–2 nm range while preserving or slightly increasing material removal rate.

Medical device and photonics applications add a structurally distinct demand layer that insulates the market from industrial cyclicality. Surgical instruments, laser optics, and implantable device components require polished surfaces meeting biocompatibility and optical transmission standards that are non-negotiable and specification-locked.

Restraints

Raw Material Price Volatility and Environmental Compliance Costs Compress Margins Across the Polishing Powder Supply Chain

Rare earth price volatility directly threatens polishing powder economics. Cerium, lanthanum, and other rare-earth elements used in high-performance polishing compounds are sourced from geographically concentrated supply chains — exposing formulators to sharp input cost swings when mining output or export policy shifts.

Environmental regulations on chemical-based abrasives tighten the compliance cost structure for polishing powder producers. Increasing Ce³⁺ content on the cerium-oxide surface from 14.2% to 36.5% via photo-oxidative treatment improved polishing behavior — but such advanced surface treatments add process complexity and capital cost that raise barriers for price-competitive suppliers.

These twin pressures — input cost volatility and compliance expenditure — disproportionately burden mid-sized polishing powder manufacturers who lack the vertical integration or R&D resources of large chemical groups. Consequently, market consolidation accelerates as smaller formulators either exit specialty segments or seek acquisition by larger players with stronger balance sheets and established regulatory expertise.

Growth Factors

Sustainable Formulations, Renewable Energy Demand, and Nanotechnology Open New Revenue Pathways for Polishing Powder Suppliers

Eco-friendly polishing powder formulations transition from regulatory compliance tool to market differentiation strategy. Hydrometallurgical flowsheets recover over 90% of cerium and other rare earths from spent polishing powders for reuse — a recovery rate that transforms polishing waste from a disposal liability into a viable secondary raw material stream.

Solar panel manufacturing creates a structurally new demand pool for precision polishing materials. Photovoltaic cell efficiency depends partly on the surface quality of glass covers and silicon wafers — both of which require polishing compounds with controlled particle characteristics.

Nanotechnology-based polishing materials represent the highest-margin growth vector for technically advanced suppliers. Nano-grade abrasives achieve surface finishes impossible with micron-scale particles, enabling applications in quantum computing components, advanced optical coatings, and next-generation semiconductor substrates.

Regional Analysis

Asia-Pacific Dominates the Polishing Powder Market with a Market Share of 44.6%, Valued at USD 1.2 Billion

Asia-Pacific commands 44.6% of the global polishing powder market, valued at USD 1.2 billion. This concentration reflects the region’s position as the world’s primary semiconductor fabrication, consumer electronics assembly, and precision manufacturing hub. China, South Korea, Japan, and Taiwan operate the highest density of CMP-intensive production facilities globally, creating recurring consumable demand that no other region matches in scale or technical specification.

North America holds a structurally strong position driven by its established semiconductor fabrication base and aerospace manufacturing sector. The CHIPS Act and related federal investment programs accelerate new fab construction across Arizona, Ohio, and New York — each facility representing decades of polishing consumables demand.

Europe’s polishing powder consumption centers on automotive manufacturing in Germany, precision optics production in Germany and France, and aerospace component finishing in the UK and France. European procurement increasingly weighs environmental compliance alongside technical performance, creating an early-mover advantage for suppliers with documented low-toxicity formulations.

Middle East and Africa represent an early-stage industrial base for polishing powder consumption. Gulf Cooperation Council economies actively build manufacturing diversification programs — including metals processing and construction materials production — that require surface finishing at scale.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Akzo Nobel NV positions its polishing and surface treatment portfolio around coating chemistry expertise built across decades of industrial coatings supply. Its advantage lies in formulation breadth — the ability to match polishing compound chemistry to substrate-specific requirements across automotive, aerospace, and marine applications. This cross-sector technical library reduces customer switching costs and creates a defensible position that pure-play abrasive manufacturers cannot easily replicate.

Axalta Coatings concentrates its market positioning on automotive refinishing systems, where polishing compounds integrate directly into color-matching and surface restoration workflows. Its strength is channel depth — established relationships with automotive body shops and OEM finishing lines give Axalta distribution access that specialty polishing powder suppliers cannot achieve on their own.

BASF SE approaches the polishing powder market through its advanced materials and specialty chemicals platform, where surface finishing compounds benefit from shared R&D infrastructure with electronic materials and catalysis divisions. This integrated research base allows BASF to simultaneously develop polishing formulations informed by semiconductor process chemistry and materials science — a development capability that standalone polishing powder manufacturers cannot match without an equivalent investment scale.

Arkema Group differentiates through its specialty polymer and functional materials expertise, which underpins polishing compound development for applications requiring precise rheological control — including CMP slurries and optical surface finishing compounds. Arkema’s investment in sustainable chemistry aligns its product development direction with tightening environmental procurement criteria in European and North American markets, positioning it ahead of regulatory transitions that will disadvantage formulators reliant on hazardous chemical inputs.

Key Players

- Akzo Nobel NV

- Axalta Coatings

- BASF SE

- Arkema Group

- Berger Paints India Limited

- Chemetall

- Chugoku Marine Paints Ltd

- DowDuPont

- Evonik Industries AG

- HEMPEL A/S

- Henkel AG & Co. KGaA

- Jotun

- Kansai Paint Co. Ltd

Recent Developments

- In 2025, Akzo Nobel N.V. announced an all-stock merger with Axalta to create a major global coatings company; the combined portfolio includes Powder Coatings. Also proposed separating/acquiring the Powder Coatings operations and International Research Center from Akzo Nobel India.

- In 2025, Axalta Coatings official product portfolio includes thermoplastic and thermosetting powder coatings under brands such as Alesta, Abcite, Plascoat, and Nap-Gard. Axalta launched Alesta e-PRO EV battery coating products for heat protection/electrical insulation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.7 Billion |

| Forecast Revenue (2035) | USD 4.2 Billion |

| CAGR (2026-2035) | 4.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Alumina, Diamond, Cerium Oxide, Silica, Zirconia), By Application (Metal Polishing, Plastic Polishing, Glass Polishing, Automotive Polishing, Electronic Polishing), By End-Use (Manufacturing, Automotive, Electronics, Aerospace, Construction) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Akzo Nobel NV, Axalta Coatings, BASF SE, Arkema Group, Berger Paints India Limited, Chemetall, Chugoku Marine Paints Ltd, DowDuPont, Evonik Industries AG, HEMPEL A/S, Henkel AG & Co. KGaA, Jotun, Kansai Paint Co. Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |