Quick Navigation

Report Overview

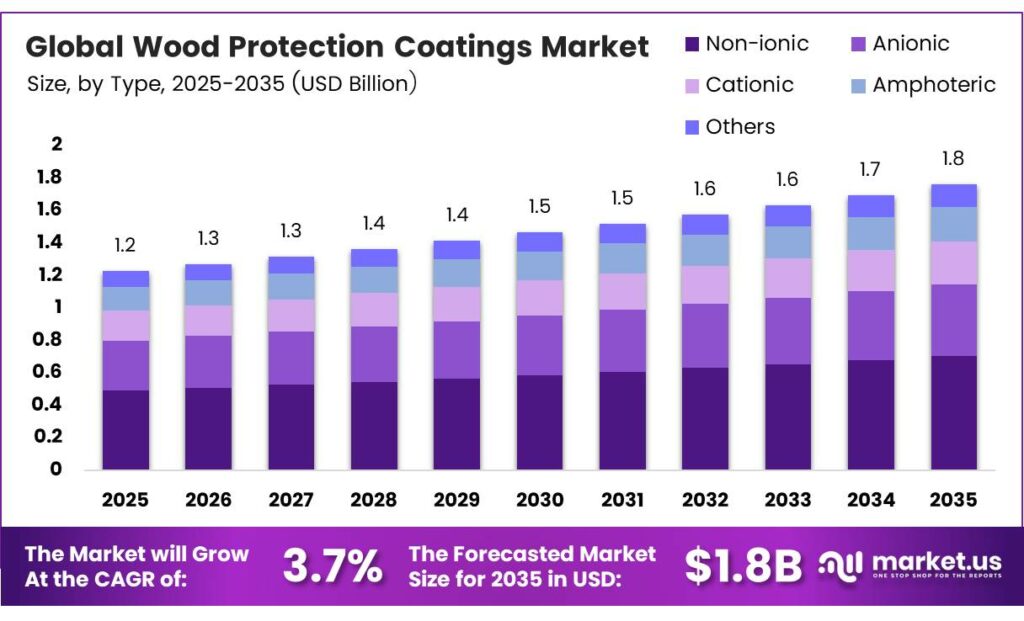

The Global Wood Protection Coatings Market size is expected to be worth around USD 1.8 billion by 2035 from USD 1.2 billion in 2025, growing at a CAGR of 3.7% during the forecast period 2026 to 2035.

Wood protection coatings form a specialized category of surface treatment products designed to shield wood from moisture, UV radiation, biological degradation, and mechanical wear. These coatings serve both functional and decorative roles across residential construction, commercial furniture, and infrastructure projects. The market spans water-based, solvent-based, and bio-based formulation types.

A sustainable two-component wood coating based on renewable polyol technology with VOC below 150 g/L achieved comparable or better film hardness, mar resistance, and dry time than a conventional solventborne benchmark, while reducing solvent emissions by roughly 40–60% versus typical solventborne floor coatings of 350–420 g/L.

A fluorine-free superhydrophobic wood coating achieved static water contact angles above 160° and maintained that performance after 1,000 hours of UV exposure. This level of durability directly addresses the most common failure mode in exterior applications — UV-induced degradation — and signals that next-generation performance coatings will compete on longevity metrics rather than price alone.

Key Takeaways

- The Global Wood Protection Coatings Market was valued at USD 1.2 billion in 2025 and is forecast to reach USD 1.8 billion by 2035 at a CAGR of 3.7% during the forecast period 2026 to 2035.

- Non-ionic Surfactants lead with a 34.2% share in 2025.

- Emulsifiers hold the dominant position with a 31.9% share.

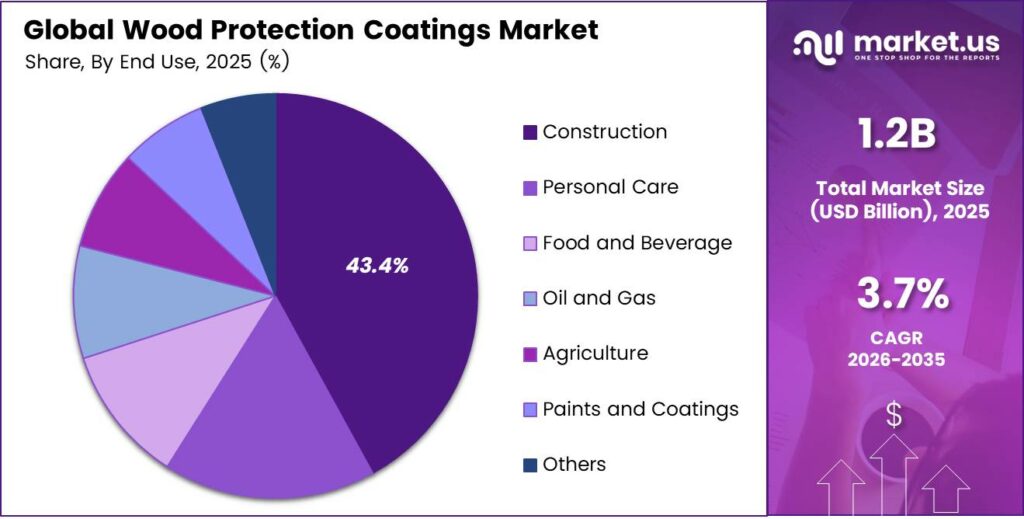

- Construction commands the largest share at 43.4%.

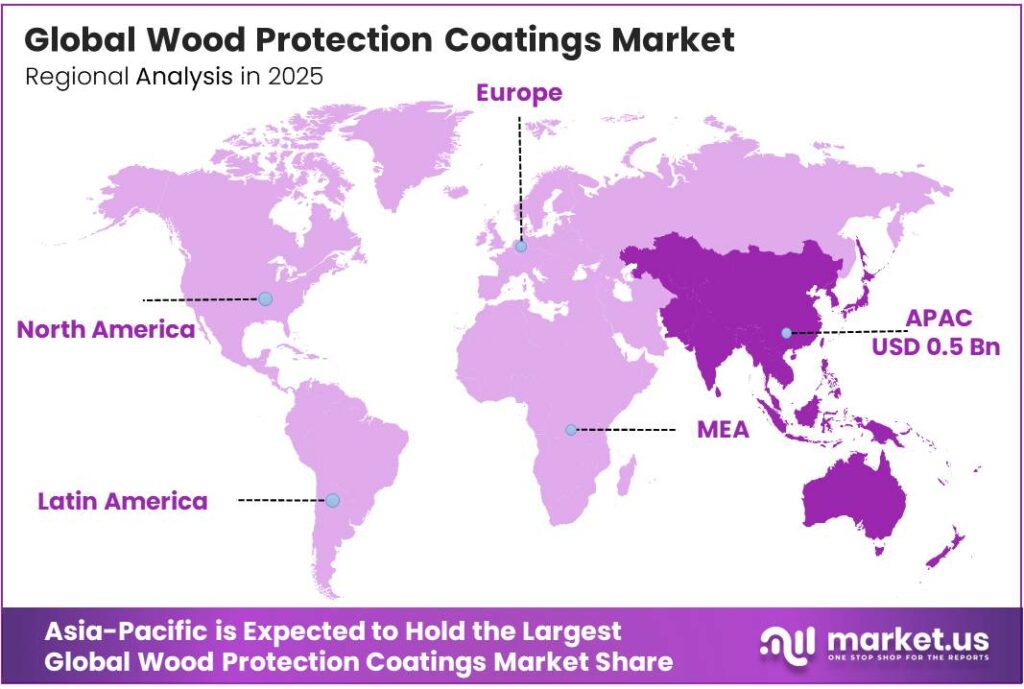

- Asia-Pacific dominates regional consumption with a 44.6% share, valued at approximately USD 0.5 billion.

Product Analysis

Non-ionic Surfactants dominate with 34.2% due to broad compatibility across coating formulations.

In 2025, Non-ionic Surfactants held a dominant market position in the By Type segment of the Wood Protection Coatings Market, with a 34.2% share. Their electrical neutrality makes them compatible with a wide range of coating chemistries, including water-based and emulsion systems. Formulators prefer non-ionic variants because they stabilize emulsions without introducing ionic interference that can disrupt film formation.

Anionic Surfactants carry strong performance credentials in dispersion and wetting applications. They work effectively in alkaline coating environments, making them a standard choice in construction-grade wood primers and sealers. However, sensitivity to hard water and electrolyte concentration limits their use in certain specialty formulations, positioning them as a complementary rather than universal option.

Application Analysis

Emulsifiers dominate with 31.9% due to their central role in water-based coating stability.

In 2025, Emulsifiers held a dominant market position in the By Application segment of the Wood Protection Coatings Market, with a 31.9% share. As the wood coatings industry shifts toward water-based systems under VOC regulations, emulsifiers become structurally essential — they maintain oil-in-water stability that allows resin and pigment systems to remain suspended and film-form correctly on application.

Wetting Agents address the fundamental challenge of applying coatings uniformly on porous wood surfaces. Wood grain and texture create uneven surface energy, causing coatings to bead rather than spread. Wetting agents reduce surface tension, ensuring even coverage and reducing material waste — a direct cost benefit for both industrial applicators and end consumers.

End-User Analysis

Construction dominates with 43.4% due to the high volume use of treated exterior wood.

In 2025, Construction held a dominant market position in the By End-User segment of the Wood Protection Coatings Market, with a 43.4% share. Exterior wood elements — cladding, decking, framing, and joinery — require protective treatment to meet building codes and warranty commitments. Large-scale residential and commercial projects consume coating volumes that dwarf any other end-user category, making construction the anchor segment for every major supplier.

Personal Care represents a distinct and growing consumption avenue for specialty surfactant-based formulations derived from the same chemistry used in wood coating systems. Manufacturers operating across both markets gain formulation synergies and shared raw material supply chains. However, regulatory requirements for personal care applications differ significantly from industrial coatings, requiring separate compliance investments.

Food and Beverage applications demand food-safe coating formulations for wooden packaging, pallets, and processing equipment. This segment prioritizes non-toxic, low-migration chemistry, which aligns with the broader industry shift toward bio-based and water-based systems. Formulators meeting food-contact approvals access a segment that commands premium pricing and long-term supply contracts.

Key Market Segments

By Type

- Non-ionic Surfactants

- Anionic Surfactants

- Cationic Surfactants

- Amphoteric Surfactants

- Others

By Application

- Emulsifiers

- Wetting Agents

- Dispersants

- Foaming Agents

- Stabilizers

- Others

By End-User

- Construction

- Personal Care

- Food and Beverage

- Oil and Gas

- Agriculture

- Paints and Coatings

- Others

Emerging Trends

Water-Based Chemistry, Nanotechnology, and Digital Application Tools Redefine Wood Coating Performance Standards

Water-based and low-VOC formulations are replacing solvent-based systems at an accelerating pace across both professional and retail channels. This shift is not voluntary — regulatory mandates are removing solvent-based options from key markets, forcing the transition. Suppliers investing in water-based chemistry now secure a shelf position that will become structurally protected as compliance windows close for non-conforming competitors.

Nanotechnology integration is delivering measurable performance gains. Water-based varnishes showed higher adhesion after UV aging at 1.18 MPa compared to polyurethane varnishes at 1.05 MPa. This adhesion advantage is significant because coating delamination from UV exposure is the leading cause of premature failure in exterior applications. Superior adhesion under UV stress directly translates to longer recoating cycles and lower total ownership cost for end users.

Digital color matching and advanced application technologies are changing how contractors and consumers select and apply wood finishes. Customized textures and decorative finishes now represent a premium product category with differentiated margin profiles. Suppliers that combine digital specification tools with consistent color-matched formulations can convert specification-stage influence into locked purchase decisions — reducing price competition at the point of sale.

Drivers

Infrastructure Expansion and Construction Activity Create Sustained Volume Demand for Wood Protection Coatings

Residential and commercial construction projects consume protective wood coatings at scale across exterior cladding, decking, windows, and structural timber. Builders specify protective coatings to meet warranty commitments and building code requirements. As urbanization deepens across the Asia-Pacific and emerging markets, construction pipelines translate directly into multi-year forward demand for wood treatment products.

Furniture manufacturers apply protective coatings as a direct margin lever. Coated surfaces justify premium retail pricing by extending product life and enabling aesthetic customization. Moreover, awareness of wood degradation from moisture, UV radiation, and biological threats continues to build among both professional contractors and retail consumers — driving higher coating application rates per project.

Advanced coating systems deliver measurable protection gains. A fluorine-free superhydrophobic wood coating maintained static water contact angles above 160° and retained that performance after 1,000 hours of UV exposure. This evidence supports specifier confidence in premium protective systems, reinforcing willingness to pay for technically validated products over commodity alternatives.

Restraints

VOC Regulations and Raw Material Cost Volatility Compress Margins and Limit Formulation Flexibility

Environmental regulations targeting VOC emissions are forcing formulators to exit solvent-based product lines or invest heavily in reformulation. Countries across Europe and North America have tightened VOC limits, and non-compliant products face delisting from major retail and industrial channels. Compliance costs fall unevenly — larger players absorb them more easily, while smaller formulators face existential pressure.

Raw material price volatility compounds this pressure. Specialty surfactants, resins, and bio-based inputs used in compliant formulations carry higher and less predictable input costs than conventional solvent-based chemistry. When input costs spike, formulators cannot always pass increases to buyers on existing supply contracts, creating direct margin compression across affected product lines.

Research demonstrates that performance is achievable at low VOC levels, but the transition demands technical investment. Applying additional protective layers can extend outdoor wood coating service life from approximately 3 years to approximately 10 years — but achieving this requires optimized multi-layer systems rather than single-coat solutions. Smaller producers without formulation expertise face difficulty replicating these results, widening the gap between leaders and followers in technical capability.

Growth Factors

Bio-Based Formulations, Smart Coating Technologies, and E-Commerce Expansion Open New Revenue Pathways

Bio-based wood coating formulations are moving from laboratory research to commercial viability. UV-resistant coatings incorporating plant-derived bark extracts reduced color change by 40% relative to uncoated wood after accelerated UV exposure, while maintaining comparable gloss to conventional synthetic UV absorbers. This performance parity removes the primary objection to bio-based adoption — the perception of inferior protection.

Smart coatings with self-healing and anti-microbial properties represent the next performance tier for premium market segments. Additionally, a bio-based flame-retardant coating achieved limiting oxygen index (LOI) values above 30% and reduced peak heat release rate by more than 50% in cone-calorimeter tests, validating multifunctional bio-based chemistry as commercially viable.

E-commerce channel expansion creates a structural shift in wood coating distribution. Direct-to-consumer and direct-to-contractor digital channels reduce distributor dependency, improving margins for manufacturers while increasing buyer access in underserved geographies. Emerging economies with rising urbanization and housing construction represent a largely unaddressed volume opportunity for suppliers willing to build digital distribution infrastructure early.

Regional Analysis

Asia-Pacific Dominates the Wood Protection Coatings Market with a Market Share of 44.6%, Valued at USD 0.5 Billion

Asia-Pacific commands 44.6% of the global Wood Protection Coatings Market, valued at approximately USD 0.5 billion. China, India, and Southeast Asian economies drive this position through concentrated furniture manufacturing, large-scale residential construction, and cost-competitive raw material supply chains. The region’s scale advantages mean volume leadership here is structural, not cyclical.

North America represents a high-value, regulation-driven market where VOC compliance standards have already restructured product portfolios toward water-based systems. Mature construction and renovation activity sustains consistent demand for premium exterior wood coatings. Professional contractors and retail DIY channels both remain active buyers, supporting a diversified demand base less vulnerable to single-sector slowdowns.

Europe enforces the world’s most stringent VOC and chemical safety standards, effectively serving as the global benchmark for compliant wood coating formulations. Manufacturers qualifying products for European markets gain regulatory credibility transferable to other tightening jurisdictions. Germany, France, and the UK lead consumption, anchored by active residential renovation markets and well-established professional applicator networks.

Latin America represents an under-penetrated market, with urbanization in Brazil and Mexico outpacing the adoption of wood protection. Construction activity is building the volume base, but awareness of protective coating benefits among contractors remains lower than in mature markets. Suppliers that invest in applicator education alongside product distribution can convert a volume opportunity into a durable market position ahead of better-resourced competitors.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Analysis

BASF positions itself as a full-spectrum chemistry provider across wood coating raw materials, supplying both surfactant systems and specialty resin inputs. Its scale allows simultaneous investment in bio-based reformulation and high-performance additive development — a combination smaller competitors cannot replicate. This breadth gives BASF access to specifications across the construction, furniture, and industrial coatings segments without being dependent on any single buyer category.

Evonik concentrates its competitive advantage on specialty surfactant performance at the formulation level. Its application laboratories work directly with coating manufacturers to optimize surfactant selection and loading — creating technical dependency that extends customer relationships well beyond a transactional supply agreement. This embedded advisory model makes Evonik difficult to displace on cost alone, insulating its margin even in competitive tender processes.

Clariant focuses on sustainable chemistry as its primary differentiation platform within the wood coatings supply chain. By aligning product development with tightening VOC and environmental regulations ahead of mandate deadlines, Clariant converts regulatory pressure into a commercial advantage. Its bio-based and low-emission surfactant portfolio is structured to meet compliance requirements in Europe and North America simultaneously.

Arkema International AG brings advanced material science capability to wood coating applications, particularly through its specialty polymer and resin platforms that underpin high-performance topcoat formulations. Its strategic positioning bridges raw material chemistry and finished coating performance — enabling partnerships with coating manufacturers seeking technically differentiated input materials rather than commodity surfactants. This positions Arkema to benefit from the market’s shift toward premium, multifunctional wood protection systems.

Key Players

- BASF

- Evonik

- Clariant

- Arkema International AG

- Stepan Company

- Nouryon

- Syensqo

- Kao Corporation

- Croda International Plc

Recent Developments

- In 2025, BASF opened a new water-based dispersions production line in Heerenveen, Netherlands, increasing capacity without additional CO₂ emissions; BASF says these dispersions serve industrial and wood coatings. It also launched PFAS-alternative coating additives.

- In 2025, Evonik expanded its coatings additive portfolio with TEGO Wet 290 and TEGO Wet 296, explicitly targeting appearance needs in wood furniture coatings. Evonik also promotes wood-coating additives/resins for gloss control, film formation, scratch resistance, color stability, lower VOCs, and resource efficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.2 Billion |

| Forecast Revenue (2035) | USD 1.8 Billion |

| CAGR (2026-2035) | 3.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Non-ionic Surfactants, Anionic Surfactants, Cationic Surfactants, Amphoteric Surfactants, Others), By Application (Emulsifiers, Wetting Agents, Dispersants, Foaming Agents, Stabilizers, Others), By End-User (Construction, Personal Care, Food and Beverage, Oil and Gas, Agriculture, Paints and Coatings, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BASF, Evonik, Clariant, Arkema International AG, Stepan Company, Nouryon, Syensqo, Kao Corporation, Croda International Plc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |