Quick Navigation

Report Overview

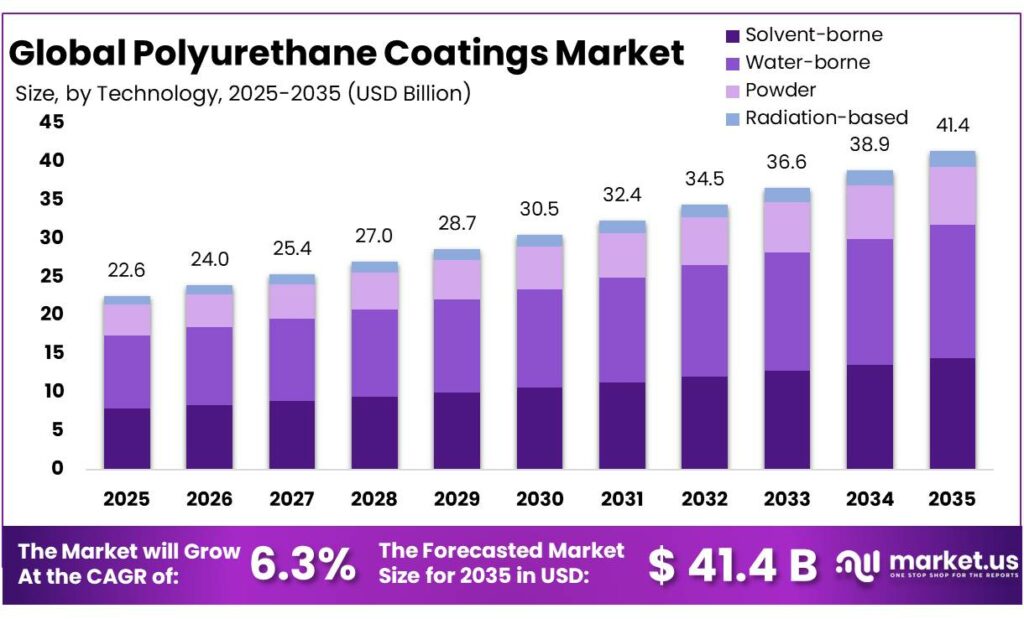

The Global Polyurethane Coatings Market size is expected to be worth around USD 41.4 Billion by 2035, from USD 22.6 Billion in 2025, growing at a CAGR of 6.3% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 35.8% share, holding USD 17.4 Billion revenue.

Polyurethane coatings represent a high-performance segment of the industrial coatings universe, valued for abrasion resistance, flexibility, chemical durability, gloss retention, and weatherability. In practical terms, they are widely specified as topcoats and protective systems across construction assets, transportation equipment, industrial machinery, flooring, and selected food-contact packaging applications where compliance and barrier performance matter.

The industrial backdrop remains supportive because end-use activity is still large: U.S. total construction spending reached a seasonally adjusted annual rate of $2,190.4 billion in January 2026, including $728.2 billion in private nonresidential activity and $148.5 billion in highway construction, all of which sustain demand for protective and finish coatings.

The broader industrial scenario also remains anchored by transportation manufacturing. According to OICA, global motor vehicle production totaled 92,504,338 units in 2024, while Europe produced 17,231,668 units and the EU-27 plus the UK produced 14,307,986 units.

This matters because polyurethane coatings are heavily used where OEMs and component suppliers require appearance retention, scratch resistance, corrosion protection, and long service intervals. In parallel, Sherwin-Williams states that its Performance Coatings Group serves construction, industrial, packaging, and transportation markets in more than 120 countries, underlining the scale and geographic spread of industrial coatings demand.

Demand is also reinforced by food-related industries, which support coatings used in processing environments, equipment surfaces, and compliant packaging systems. The European Commission states that all food-contact materials placed on the EU market must comply with Regulation (EC) No 1935/2004 and Good Manufacturing Practice under Regulation (EC) No 2023/2006, keeping performance and compliance tightly linked in this area.

U.S. supermarkets generated $1 trillion in sales in 2024, grocery stores and food manufacturers employed 6.3 million people, and average weekly household grocery spending reached $170 as of February 2025. That scale supports continued need for durable, cleanable, and regulation-aligned coating technologies in food value chains.

The main growth drivers are therefore a mix of asset protection needs and regulation. The U.S. EPA says its architectural coatings VOC rule is estimated to reduce emissions by 103,000 megagrams per year (113,500 tons per year), which continues to push formulators toward higher-performance, lower-emission systems. In Europe, the Renovation Wave aims to renovate 35 million buildings by 2030 and at least double the annual rate of energy renovations, creating a durable demand base for long-life exterior and interior coating systems compatible with refurbishment and sustainability goals.

Key Takeaways

- Polyurethane Coatings Market size is expected to be worth around USD 41.4 Billion by 2035, from USD 22.6 Billion in 2025, growing at a CAGR of 6.3%.

- Water-borne held a dominant market position, capturing more than a 42.7% share.

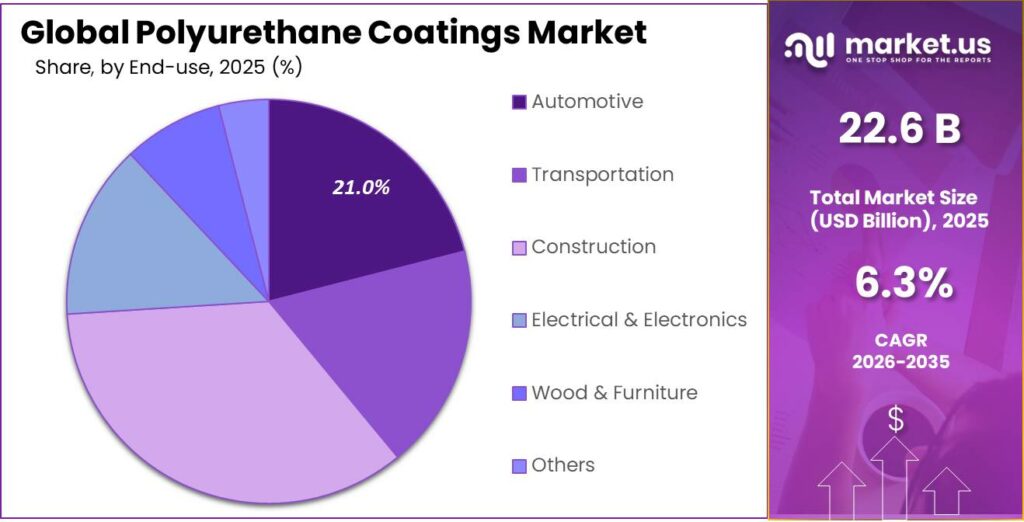

- Construction held a dominant market position, capturing more than a 35.9% share.

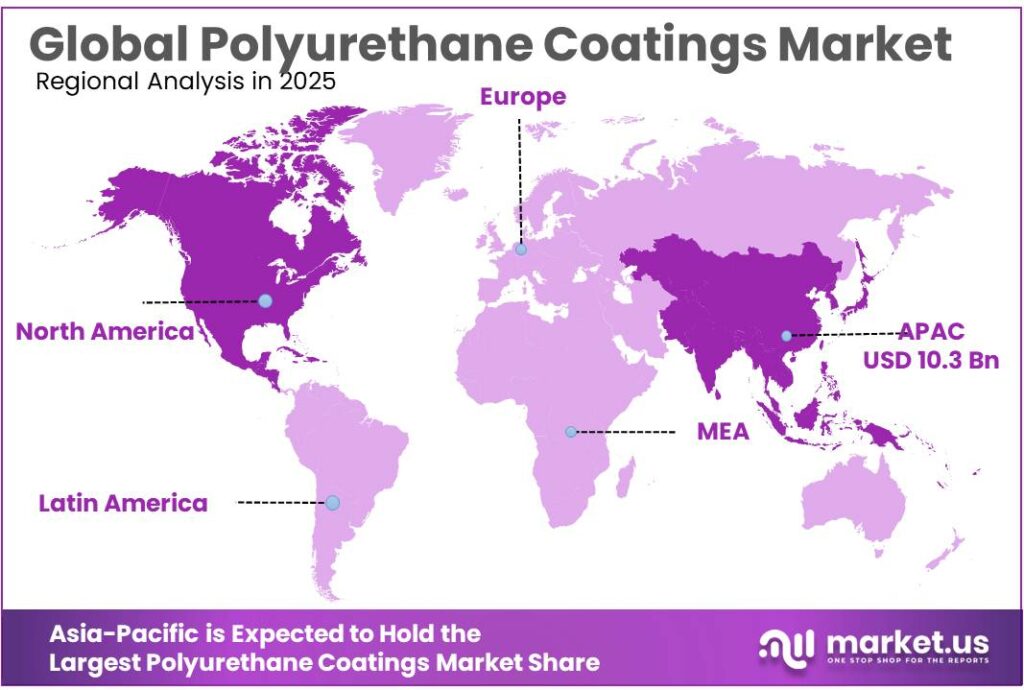

- Asia-Pacific emerged as the dominant region in the polyurethane coatings market, accounting for 45.6% of global revenue and reaching a market value of USD 10.3 billion.

By Technology Analysis

Water-borne leads the polyurethane coatings market with 42.7% share, supported by strong demand for low-VOC and eco-friendly coating solutions.

In 2025, Water-borne held a dominant market position, capturing more than a 42.7% share. This strong position was mainly supported by the growing shift toward environmentally safer coating technologies across construction, automotive, wood finishing, and industrial applications. Water-borne polyurethane coatings are widely preferred because they release lower emissions, have less odor, and are easier to apply in indoor environments compared to conventional solvent-based systems. Their increasing use in furniture, flooring, protective coatings, and decorative surfaces also helped strengthen demand, especially in projects where air quality and regulatory compliance are important.

By End-use Analysis

Construction dominates the polyurethane coatings market with 35.9% share, driven by rising use in durable surface protection and modern building finishes.

In 2025, Construction held a dominant market position, capturing more than a 35.9% share. This leading share was largely driven by the wide use of polyurethane coatings across residential, commercial, and infrastructure projects where long-lasting surface protection is essential. These coatings are commonly used on concrete floors, steel structures, wall panels, roofs, and wooden fixtures because they offer strong resistance to abrasion, moisture, chemicals, and weather exposure. The construction sector continued to favor polyurethane coatings for both interior and exterior applications due to their durability, smooth finish, and ability to extend the life of building materials.

Key Market Segments

By Technology

- Solvent-borne

- Water-borne

- Powder

- Radiation-based

By End-use

- Automotive

- Transportation

- Construction

- Electrical & Electronics

- Wood & Furniture

- Others

Emerging Trends

Water-borne and Bio-based Polyurethane Coatings Are Emerging as the Strongest Latest Trend

One of the most important latest trends in the polyurethane coatings market is the fast shift toward water-borne and bio-based formulations. Across construction, automotive, wood, and industrial applications, manufacturers are moving away from solvent-heavy systems and adopting low-VOC polyurethane coatings that align with sustainability goals. In 2025, the global waterborne coatings market reached USD 98.97 billion, highlighting the scale of this transition toward cleaner coating technologies.

At the same time, the bio-based coatings segment continued to gain traction as resin producers increased the use of renewable feedstocks, plant-derived polyols, and recycled raw materials. Industry sources in 2025 noted that the bio-based coatings market is rising steadily due to stricter environmental standards and growing demand from green building projects.

EV Manufacturing and Smart Protective Coatings Are Reshaping Demand

Another major trend shaping polyurethane coatings is the growing use of smart protective and EV-compatible coating systems. Electric vehicle manufacturing is expanding the use of advanced polyurethane coatings for battery casings, lightweight plastics, interiors, and exterior protective layers that need strong scratch resistance and low emissions.

Drivers

Rising Green Building Activity is Driving Higher Use of Polyurethane Coatings

One of the biggest drivers for polyurethane coatings is the fast growth in green building and infrastructure development. Governments across major economies are pushing low-emission construction materials, which is directly increasing the use of water-borne and durable polyurethane coatings on floors, steel, walls, and wood surfaces. In 2025, the global green coatings industry was valued at USD 143.43 billion, showing how strongly eco-friendly coating demand is expanding across construction and industrial use.

At the same time, the broader polyurethane coatings market reached USD 21.59 billion in 2025, supported by large-scale urban development and refurbishment projects. Government-backed smart city programs, stricter VOC emission standards, and green building certifications are encouraging contractors to choose polyurethane systems because of their durability and lower maintenance needs.

Environmental Regulations and Low-VOC Policies are Accelerating Demand

Another major growth factor is the global push toward low-VOC and safer industrial coatings. Environmental agencies and construction regulators are tightening emission rules, making polyurethane coatings a preferred option due to their long life, abrasion resistance, and growing availability in water-borne grades. The polyurethane coatings market is projected to rise from USD 21.59 billion in 2025 to USD 28.16 billion by 2030, reflecting how compliance-led adoption is becoming a long-term trend.

Industries such as construction, transportation, and heavy equipment are moving toward these coatings because they help reduce repainting cycles and improve asset life. Government initiatives linked to sustainable transport, industrial modernization, and public infrastructure renewal are also adding momentum. In simple terms, the market is growing because companies now need coatings that are both high-performance and environmentally acceptable.

Restraints

Raw Material Price Volatility Remains a Major Restraint for Polyurethane Coatings

One of the biggest restraining factors for the polyurethane coatings market is the constant fluctuation in raw material prices, especially for MDI, TDI, and polyols, which are directly linked to crude oil and petrochemical feedstocks. When the prices of these inputs move sharply, coating manufacturers face immediate pressure on production costs and profit margins.

In early 2026, polyol prices in Asia increased by nearly USD 200–300 per metric tonne, while BASF announced a USD 200 per tonne increase for TDI across Asia-Pacific due to higher energy, logistics, and compliance expenses.

Supply Chain and Petrochemical Dependence Continue to Limit Growth

Another key restraint is the market’s heavy dependence on petrochemical supply chains, which remain highly vulnerable to geopolitical issues, freight disruptions, and refinery-level production cuts. Polyurethane coatings rely on feedstocks such as benzene, toluene, and propylene derivatives, so even a small rise in crude-linked intermediates can quickly impact coating prices.

Recent industry updates showed Brent-linked energy costs rising by around 8% in a short period, creating direct cost-push inflation across polyurethane intermediates and downstream coating formulations.

Opportunity

Renewable Energy Infrastructure Expansion Creates a Strong Growth Opportunity

One of the strongest growth opportunities for polyurethane coatings is the rapid expansion of renewable energy infrastructure, especially in wind and solar projects. Polyurethane coatings are widely used on wind turbine blades, towers, solar mounting structures, and power transmission components because they offer excellent UV resistance, corrosion protection, and long-term weather durability.

Government-backed clean energy programs are creating direct opportunities for polyurethane coatings manufacturers. India’s Ministry of Power highlighted major investment growth in cross-border renewable energy infrastructure and grid modernization under its 2025–26 annual roadmap, which supports stronger demand for protective coatings used in exposed metal and composite assets.

Wind Turbine Protection and Grid Modernization Open New Revenue Potential

Another major opportunity comes from the growing need to protect wind energy equipment and transmission assets from harsh outdoor conditions. Wind turbine blades face continuous exposure to rain erosion, salt spray, dust, and UV radiation, making polyurethane coatings one of the most suitable protective solutions. The wind power polyurethane coatings segment alone was valued at around USD 8.64 billion in 2025, with continued expansion expected from 2026 onward as renewable installations accelerate globally.

At the same time, government-led grid modernization and transmission upgrades are increasing the use of polyurethane coatings on steel poles, substations, and high-performance cable protection systems. India’s energy transition strategy and “One Sun One World One Grid” initiatives are creating long-term infrastructure demand where durable coatings play a key role in reducing corrosion and maintenance cycles.

Regional Insights

Asia-Pacific dominates the polyurethane coatings market with 45.6% share, reaching USD 10.3 billion on the back of strong construction and manufacturing demand

In 2025, Asia-Pacific emerged as the dominant region in the polyurethane coatings market, accounting for 45.6% of global revenue and reaching a market value of USD 10.3 billion. The region’s leadership is strongly supported by its large-scale construction pipeline, automotive manufacturing strength, furniture exports, and expanding industrial base.

The region also benefits from its unmatched manufacturing ecosystem. Asia-Pacific produced nearly 1.84 million tonnes of polyurethane coatings in 2024, reflecting the depth of downstream demand from wood furniture, appliances, automotive, marine, and industrial sectors. Wood and furniture applications alone contributed nearly 32% of total regional polyurethane coatings production, highlighting strong use across decorative and protective finishes.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Akzo Nobel remains a major force in polyurethane coatings through its strong performance coatings portfolio, including marine, protective, wood, and industrial solutions. In 2025, the company reported EUR 10.7 billion in revenue, with performance coatings contributing nearly 62% of adjusted EBITDA, showing the financial strength of its B2B coatings business.

Axalta is one of the most specialized players in high-performance polyurethane coatings, particularly in transportation, refinish, and industrial markets. The company operates in 130+ countries, serves over 100,000 customers, and employs nearly 12,650 people, reflecting its strong global commercial footprint. Its polyurethane systems are widely used in automotive OEM topcoats, commercial vehicles, and industrial metal applications. The planned AkzoNobel merger values the combined business at USD 25 billion, with expected combined annual revenue of USD 17 billion, underlining Axalta’s strategic scale in coatings.

Jotun is a highly respected global coatings player with strong polyurethane coating demand in marine, protective steel, infrastructure, and powder coatings. In 2025, the company reported NOK 34,333 million in revenue and maintained a workforce of 10,933 employees, highlighting its global operating scale. Polyurethane coatings are central to its protective and marine segments, especially for offshore structures, bridges, energy assets, and heavy industrial equipment.

Top Key Players Outlook

- Akzo Nobel N.V.

- Valspar Corporation

- Axalta Coating Systems

- BASF SE

- Jotun

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Willams Company

- Valspar Corporation

- Donau Carbon GmbH

Recent Industry Developments

In 2025, Akzo Nobel N.V. remained one of the strongest companies in the polyurethane coatings sector, supported by its deep presence in Performance Coatings, where polyurethane-based solutions are widely used in marine, protective, automotive refinish, wood, and industrial metal applications. The company reported €10,158 million in total revenue in 2025, while operating income increased to €1,164 million and adjusted EBITDA reached €1,444 million, showing strong profitability improvement despite mixed market conditions.

In 2025, BASF SE continued to hold a strong strategic position in the polyurethane coatings sector, mainly through its advanced automotive OEM coatings, refinish coatings, surface treatments, and polyurethane raw material integration. The company reported €59,657 million in total sales in 2025, while EBIT reached €1,634 million, reflecting stable financial strength in a challenging industrial environment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 22.6 Bn |

| Forecast Revenue (2035) | USD 41.4 Bn |

| CAGR (2026-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Solvent-borne, Water-borne, Powder, Radiation-based), By End-use (Automotive, Transportation, Construction, Electrical And Electronics, Wood And Furniture, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Akzo Nobel N.V., Valspar Corporation, Axalta Coating Systems, BASF SE, Jotun, PPG Industries Inc., RPM International Inc., The Sherwin-Willams Company, Valspar Corporation, Donau Carbon GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |