Quick Navigation

Report Overview

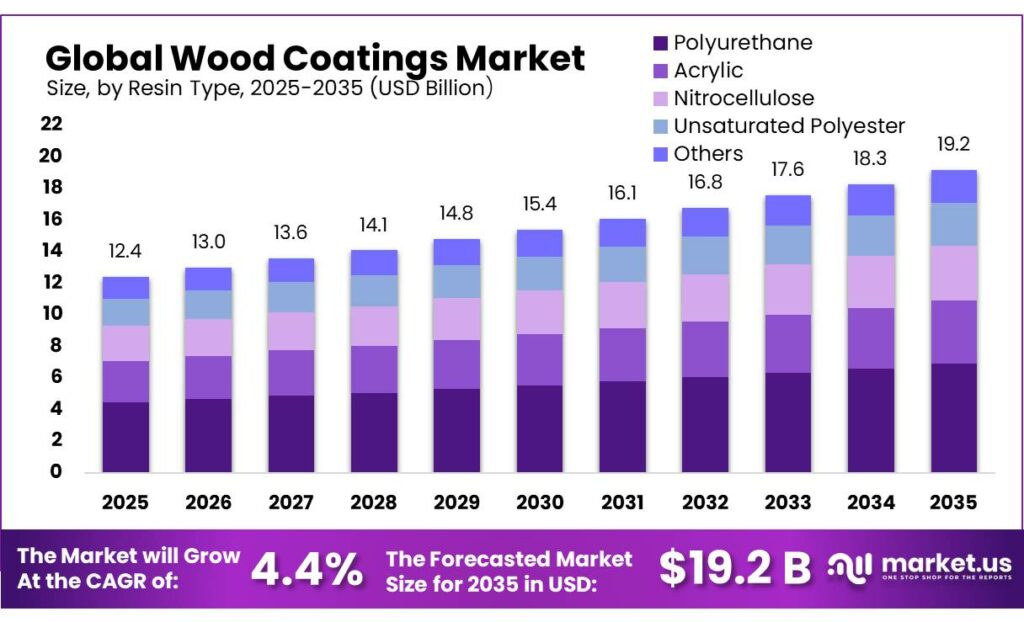

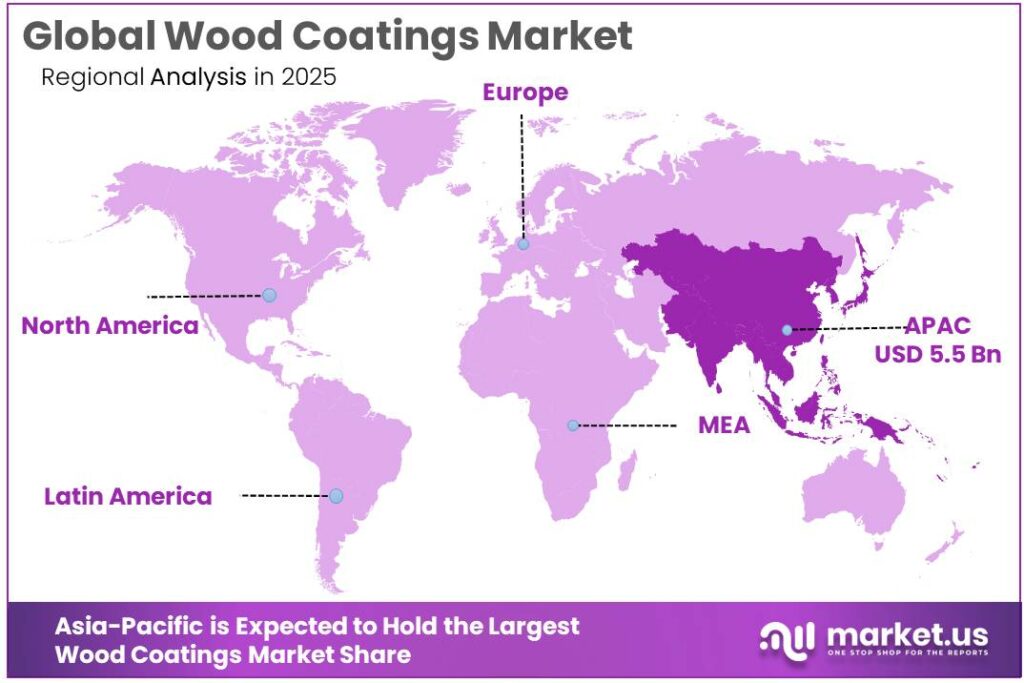

The Global Wood Coatings Market size is expected to be worth around USD 19.2 Billion by 2035, from USD 12.4 Billion in 2025, growing at a CAGR of 4.4% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 44.9% share, holding USD 5.5 Billion revenue.

Wood coatings remain a core specialty within the wider industrial coatings value chain, used to protect and enhance furniture, cabinetry, flooring, joinery, panels, and other interior and exterior wood substrates. The sector is shaped by performance requirements such as abrasion resistance, moisture protection, appearance retention, faster curing, and lower-emission chemistries, while demand is tied closely to residential construction, furniture production, remodeling activity, and compliance-led substitution toward waterborne, UV-curable, and other cleaner systems.

The market is supported by large multinational suppliers with broad finishing portfolios, including The Sherwin-Williams Company and PPG Industries, Inc., both of which participate through industrial coatings platforms rather than as stand-alone wood-only businesses. Sherwin-Williams reported record 2024 consolidated net sales of $23.10 billion, and noted that its Performance Coatings Group includes industrial coatings for wood finishing.

The industrial scenario remains fundamentally linked to wood-processing and downstream furnishing activity. In the European Union, wood-based industries employed 3.1 million people, equivalent to 10.5% of total manufacturing employment, while both wood products and furniture manufacturing each accounted for more than 900,000 jobs, underscoring the scale of coated wood demand across industrial supply chains.

In the United States, end-use momentum remains meaningful: 1,019,000 single-family homes and 608,000 multifamily units were completed in 2024, while 93% of owner-built single-family homes and 73% of completed multifamily units used wood framing. The same Census release also showed 686,000 new single-family homes sold in 2024 at a median price of $420,300, reinforcing continued pull-through for factory-finished wood components and site-applied protective systems.

Demand drivers remain centered on housing, refurbishment and design-led product differentiation. In the United States, privately owned housing starts reached a seasonally adjusted annual rate of 1,487,000 in January 2026, up 9.5% from January 2025, while single-family starts were 935,000, showing that new-build and downstream interior installation activity remain important demand anchors for wood finishes.

In Europe, the European Commission’s Renovation Wave still provides a structural tailwind, targeting the renovation of 35 million buildings by 2030 and at least doubling the annual rate of energy renovations. That matters for wood coatings because renovation cycles directly support demand for coated interior doors, decorative panels, millwork and replacement furniture.

Wood coatings demand is being supported by recovering wood-panel output, renovation activity, and the need for faster-curing, lower-energy finishing technologies, but it still faces pressure from uneven furniture demand and cautious manufacturing spending. In the United States, privately owned housing completions ran at a seasonally adjusted annual rate of 1,651,000 in January 2025, showing that a substantial installed pipeline for interior wood applications remained in place entering the year.

Key Takeaways

- Wood Coatings Market size is expected to be worth around USD 19.2 Billion by 2035, from USD 12.4 Billion in 2025, growing at a CAGR of 4.4%.

- Polyurethane held a dominant market position, capturing more than a 36.8% share.

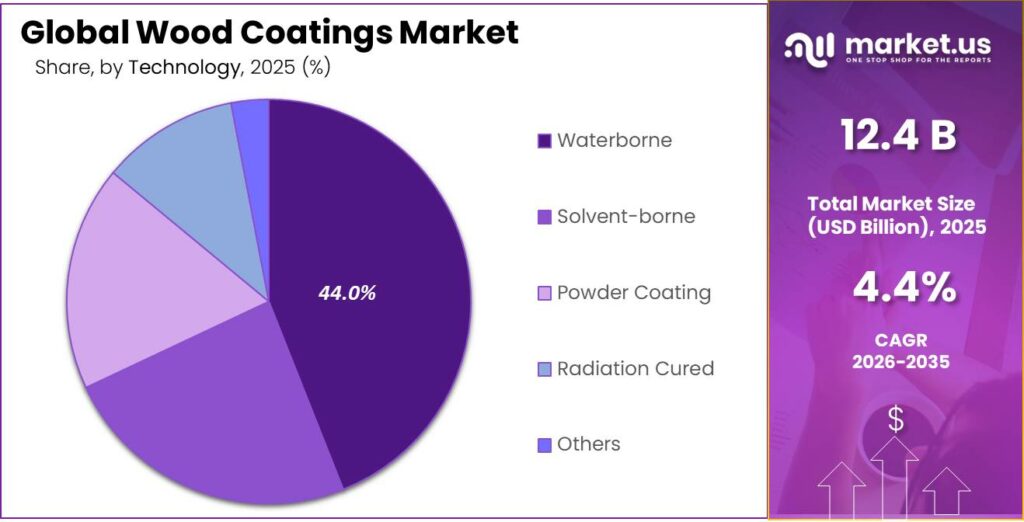

- Waterborne held a dominant market position, capturing more than a 44.6% share.

- Furniture held a dominant market position, capturing more than a 49.7% share.

- Asia-Pacific held the dominant position in the global wood coatings market, accounting for 44.9% share and reaching nearly USD 5.5 billion.

By Resin Type Analysis

Polyurethane dominates with 36.8% thanks to its strong finish, durability, and wide use across furniture and flooring applications.

In 2025, Polyurethane held a dominant market position, capturing more than a 36.8% share. This leadership was mainly supported by its strong performance in wood protection and finishing applications, where durability, scratch resistance, and long-lasting gloss are highly valued.

Polyurethane-based wood coatings remained a preferred choice across residential furniture, cabinets, wooden flooring, and interior décor products because they provide a smooth finish while helping surfaces withstand moisture, stains, and regular wear. Its popularity was especially strong in premium wood furniture and high-traffic flooring areas, where end users look for coatings that maintain appearance over time with minimal maintenance.

By Technology Analysis

Waterborne leads with 44.6% as demand rises for low-odor, eco-friendly, and easy-to-apply wood finishes.

In 2025, Waterborne held a dominant market position, capturing more than a 44.6% share. This strong position was driven by the growing shift toward environmentally safer wood coating solutions across furniture, flooring, cabinets, and decorative wood products. Waterborne coatings became widely preferred because they offer low VOC emissions, reduced odor, and faster drying compared to many conventional solvent-based alternatives, making them suitable for both industrial production lines and indoor residential use.

Their ability to deliver clear finishes, good color retention, and strong resistance against scratches and household chemicals supported wider adoption in premium furniture and interior wood applications.

By Application Analysis

Furniture dominates with 49.7% as rising demand for stylish, durable, and long-lasting wood finishes keeps this segment in the lead.

In 2025, Furniture held a dominant market position, capturing more than a 49.7% share. This leading share was mainly driven by the consistent demand for coated wood surfaces in residential and commercial furniture, where appearance, durability, and surface protection play an important role.

Wood coatings used in furniture applications remained highly preferred for tables, chairs, wardrobes, beds, office desks, and modular storage units because they enhance grain visibility while protecting against scratches, stains, moisture, and daily wear. The growth of home renovation trends, premium interior décor preferences, and rising urban housing developments further supported the demand for high-quality coated furniture products.

Key Market Segments

By Resin Type

- Polyurethane

- Acrylic

- Nitrocellulose

- Unsaturated Polyester

- Others

By Technology

- Waterborne

- Solvent-borne

- Powder Coating

- Radiation Cured

- Others

By Application

- Furniture

- Joinery

- Flooring & Decking

- Siding

- Others

Emerging Trends

Low-VOC Waterborne and UV-Cured Coatings are Emerging as the Biggest Latest Trend

One of the most visible latest trends in the wood coatings market is the fast shift toward low-VOC waterborne and UV-cured coating technologies. This trend is being shaped by indoor air quality concerns, faster production cycles, and stricter environmental standards. The U.S. EPA notes that VOC concentrations indoors can be 2 to 5 times higher than outdoor levels, and during activities such as painting they may rise to 1,000 times background outdoor levels, which is pushing furniture and wood finish manufacturers toward safer formulations.

Because of this, in 2025 and continuing into 2026, manufacturers are increasingly choosing waterborne acrylics and UV-cured systems for furniture, cabinets, and wooden flooring. These technologies offer faster curing, lower odor, better scratch resistance, and improved gloss retention, making them highly suitable for premium interiors. Government-backed green building codes and indoor air safety standards are also encouraging the use of coatings with reduced solvent content.

Bio-Based and Sustainable Wood Finishes are Becoming a Premium Industry Trend

Another major trend shaping the wood coatings market is the growing move toward bio-based and sustainable coating formulations linked with certified wood value chains. Global forestry and wood-product programs are increasingly promoting responsible timber use, which is creating demand for coatings that align with sustainability goals. The FAO reports that global exports of wood and paper products reached USD 486 billion in 2024, showing the continued scale of wood processing industries that now require greener finishing materials.

In response, wood coating manufacturers in 2025 and 2026 are introducing bio-based resins, plant-derived binders, and renewable additives to reduce fossil-based raw material use. Government initiatives around circular economy, green buildings, and sustainable forestry certification are accelerating this trend, especially in Europe and Asia. Furniture exporters and flooring brands are increasingly asking for coatings that support low emissions, recyclability, and safer indoor use.

Drivers

Furniture held a dominant market position, capturing more than a 49.7% share.

One of the biggest growth drivers for the wood coatings market is the steady rise in global furniture production and trade. As more wooden furniture, cabinets, panels, and interior décor products are manufactured, the need for protective and decorative coatings naturally increases. According to the Food and Agriculture Organization, global exports of wood and paper products increased by 1.4% to reach USD 486 billion in 2024, showing a clear recovery in wood product demand across international markets.

This increase directly supports higher use of wood coatings because every finished furniture unit, wooden board, or panel requires surface protection for durability, moisture resistance, and visual appeal. In 2025, this trend remained strong as producers focused more on premium finishes, scratch resistance, and low-VOC decorative layers. The growing use of wooden furniture in residential renovation, office interiors, and hospitality spaces is also adding to coating consumption.

Government Sustainability and Forestry Data Programs are Supporting Long-Term Market Expansion

Another major factor pushing the wood coatings market forward is strong government and international support for sustainable forestry, legal wood trade, and wood-product data transparency.

The FAO’s 2025 forestry production update shows that the global forestry database now tracks production and trade across roundwood, sawnwood, wood-based panels, pulp, and furniture-linked wood products, helping industries plan supply chains more efficiently. In addition, FAO reports that around 1.20 billion hectares of forest land globally in 2025 is managed primarily for wood and non-wood forest product production.

Restraints

Stringent VOC Emission Rules are Limiting Growth in Conventional Wood Coatings

One major restraining factor for the wood coatings market is the tightening of VOC (volatile organic compound) regulations across major countries. Traditional solvent-based wood coatings are widely used for their fast drying and rich finish, but they release higher VOC levels, making compliance increasingly difficult for manufacturers.

For example, the U.S. Environmental Protection Agency states that national VOC standards for consumer and commercial coatings are designed to reduce emissions by 90,000 tons per year, creating direct pressure on coating producers to reformulate products. In addition, South Coast Air Quality Management rules set wood coating VOC limits at 275 g/L, which restricts the use of many solvent-heavy formulations in furniture and flooring applications.

Higher Compliance and Raw Material Reformulation Costs are Pressuring Manufacturers

Another important restraint is the rising cost of compliance linked with low-VOC reformulation. Governments are not only limiting emissions but also tightening category-specific rules for wood finishes. For instance, clear wood varnishes in some regulated markets are capped at 150 g/L VOC, while lacquers can go up to 550 g/L, forcing manufacturers to redesign multiple product lines based on application type.

This creates added costs in resin selection, additives, lab validation, packaging updates, and worker training. Companies also need to adopt new curing technologies and application systems to maintain finish quality after reducing solvent content. For furniture exporters, these compliance costs become even more challenging because standards vary by country and region.

Opportunity

Sustainable Wood Construction and Furniture Demand is Creating Strong Growth Opportunity

One major growth opportunity for the wood coatings market is the rising global use of wood in sustainable construction and modern furniture manufacturing. As green buildings, engineered wood panels, modular furniture, and premium interiors become more common, the need for protective coatings is increasing steadily. FAO reported that global exports of wood and paper products rose by 1.4% to reach USD 486 billion in 2024, showing healthy momentum in wood product trade and finished furniture demand.

This directly opens long-term opportunities for wood coatings, especially in furniture, cabinets, flooring, and decorative wall panels where appearance and durability are equally important. In 2025, the use of cross-laminated timber and other engineered wood systems in buildings also supported coating demand because these surfaces require moisture resistance, UV protection, and extended life cycles. Governments and global forestry bodies are actively promoting wood as a low-carbon alternative to steel and concrete, which is encouraging more timber use in housing and commercial spaces.

Government-Led Sustainable Wood Value Chains are Opening New Premium Coating Segments

Another strong opportunity comes from government-backed sustainable wood programs and certified forestry value chains. The FAO-led Sustainable Wood for a Sustainable World (SW4SW) initiative, launched in 2018, is working with governments, the World Bank, ITTO, and industry partners to strengthen sustainable wood production and expand markets for wood-based value chains.

These initiatives are increasing the use of certified wood in furniture exports, interior panels, doors, and eco-friendly home décor, all of which need high-performance coatings. In 2025 and 2026, this trend is creating premium demand for low-VOC and safer coating systems that align with environmental building standards.

Regional Insights

Asia-Pacific Dominates the Wood Coatings Market with 44.9% Share, Reaching USD 5.5 Billion

Asia-Pacific held the dominant position in the global wood coatings market, accounting for 44.9% share and reaching nearly USD 5.5 billion in value. The region’s leadership is mainly supported by its strong furniture manufacturing ecosystem, rapid residential construction growth, and rising demand for decorative interior wood products across China, India, Vietnam, Indonesia, Japan, and South Korea.

Countries across the region continue to expand production of wooden furniture, cabinets, flooring, doors, and modular interiors, all of which require high-performance coatings for durability, moisture protection, and premium visual appeal. The region also benefits from large export-oriented furniture hubs, especially China and Vietnam, which significantly increase the use of polyurethane, acrylic, and waterborne wood coating systems.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Sherwin-Williams Company remains one of the strongest players in the wood coatings market, supported by its wide industrial coatings portfolio and strong retail presence. In 2025, the company operated 4,853 stores, employed 64,249 people, and reported net income of USD 2.57 billion, highlighting its financial strength and broad market reach. Its wood coatings business benefits from strong demand in furniture, cabinetry, and flooring applications, especially across North America and Europe.

PPG Industries, Inc. is a leading global coatings company with a strong presence in industrial wood finishes, furniture coatings, and protective decorative solutions. The company operates in more than 70 countries, generated USD 4.08 billion in Q3 2025 sales, and has around 46,000 employees globally. Its strength in wood coatings comes from advanced finishing systems used in cabinets, office furniture, flooring, and architectural wood products.

Akzo Nobel N.V. holds a strong position in the wood coatings market through premium brands such as Sikkens and International, widely used in furniture and joinery finishes. The company reported €10.668 billion in revenue, maintained operations in 150+ countries, and employed 35,200 people. Its wood coatings portfolio is especially strong in Europe and Asia-Pacific, where demand for sustainable decorative finishes remains high.

Top Key Players Outlook

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Diamond Paints

- KANSAI HELIOS

- BASF SE

- Axalta Coating Systems, LLC

- Asian Paints

- Eastman Chemical Company

Recent Industry Developments

Sherwin-Williams reported USD 23.6 billion in revenue, USD 3.81 billion in operating income, and USD 2.57 billion in net income in 2025, showing strong financial backing for innovation and expansion in wood coatings. It also operated 4,853 stores globally with 64,249 employees, giving it excellent supply reach across North America, Europe, and Asia-Pacific.

Nippon Paint Holdings reported consolidated revenue of ¥1,774,231 million, up 8.3% year-on-year, while operating profit reached ¥257,104 million, showing strong financial support for product innovation and premium wood coating technologies.

RPM reported record full-year sales of USD 7.37 billion in fiscal 2025, while adjusted EBIT reached USD 976 million, reflecting strong operational support for specialty coating innovation.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 12.4 Bn |

| Forecast Revenue (2035) | USD 19.2 Bn |

| CAGR (2026-2035) | 4.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Resin Type (Polyurethane, Acrylic, Nitrocellulose, Unsaturated Polyester, Others), By Technology (Waterborne, Solvent-borne, Powder Coating, Radiation Cured, Others), By Application (Furniture, Joinery, Flooring And Decking, Siding, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., Diamond Paints, KANSAI HELIOS, BASF SE, Axalta Coating Systems, LLC, Asian Paints, Eastman Chemical Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |