Quick Navigation

Report Overview

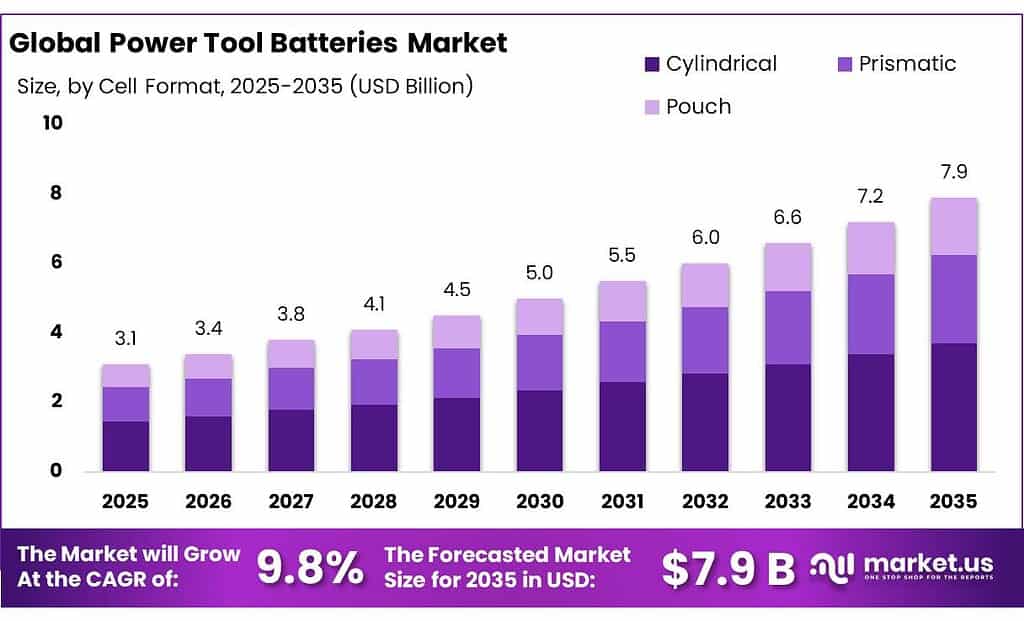

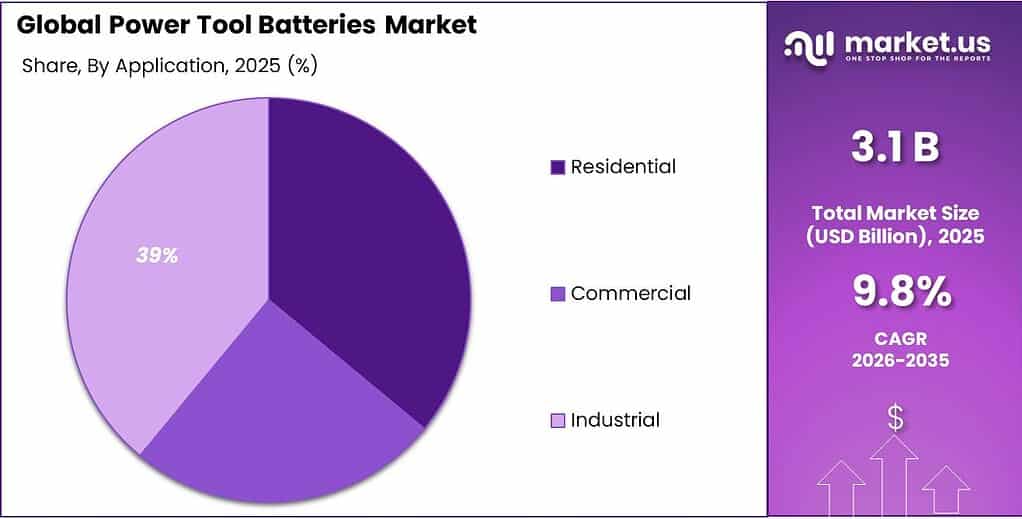

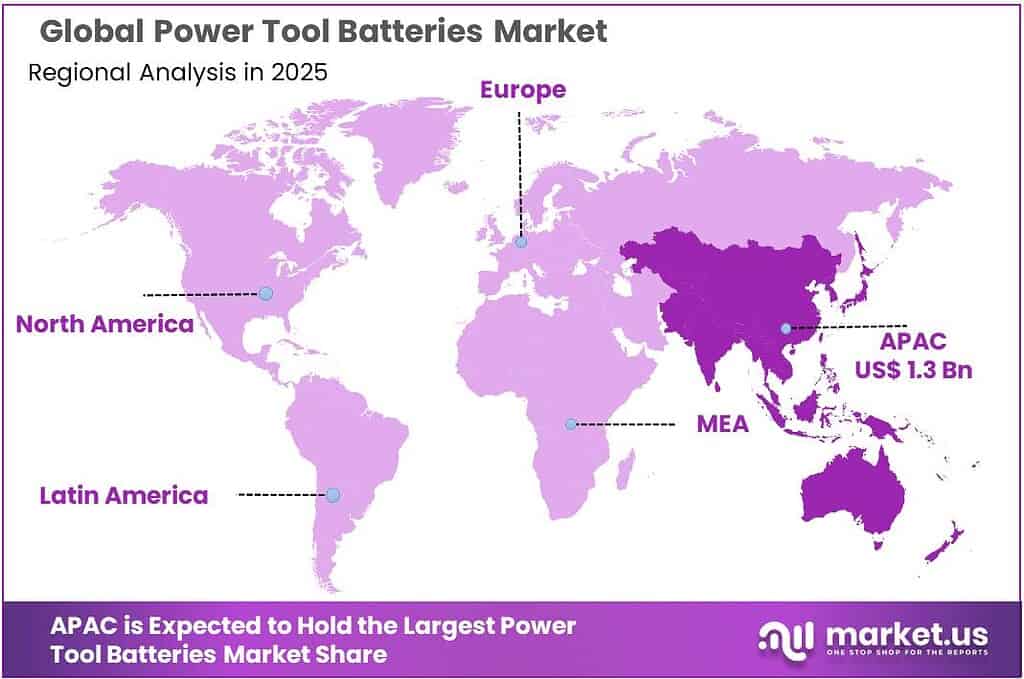

The Global Power Tool Batteries Market size is expected to be worth around USD 7.9 Billion by 2035, from USD 3.1 Billion in 2025, growing at a CAGR of 9.8% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 44.8% share, holding USD 1.3 Billion revenue.

Power tool batteries form the energy backbone of the cordless tools ecosystem, and the category is increasingly defined by lithium-ion chemistry, platform compatibility, and lifecycle management rather than by simple replacement demand. The broader battery economy is expanding at industrial scale, which is benefiting power tool batteries through better cell availability, falling input costs, and faster innovation cycles.

- The International Energy Agency reported that lithium-ion battery pack prices fell 20% in 2024, the steepest decline since 2017, while EV battery demand stood at about 1 TWh in 2024 and is projected to exceed 3 TWh by 2030 under stated policies, creating strong scale efficiencies that also support smaller industrial applications such as cordless tools.

Bosch states that its AMPShare cross-brand professional battery system has sold more than 85 million batteries, highlighting how interoperability is becoming a central competitive lever. Bosch also notes that its Power Tools business generated around €5 billion in sales revenue in 2025, while the wider Bosch Group’s Consumer Goods segment, which includes power tools, delivered €20.3 billion in 2024. Hilti reported CHF 6.4 billion in 2024 sales, with more than 80 new products and services launched during the year and CHF 466 million invested in R&D, equal to 7.2% of group sales.

The main demand drivers are productivity, mobility, labor efficiency, and safety. Contractors increasingly prefer cordless systems because they reduce setup time, remove dependency on temporary power access, and support safer operation in confined or elevated work areas. In parallel, regulation is pushing the market toward traceability and circularity. In the European Union, new waste-battery rules published on July 4, 2025 established recycling-efficiency targets effective by December 31, 2025 of 65% for lithium-based batteries, rising to 70% by 2030; material recovery targets reach 90% for cobalt, copper, lead, and nickel and 50% for lithium by 2027.

Government and regulatory initiatives are also reshaping the opportunity set. The EU’s Batteries Regulation entered into force on 17 August 2023, and the European Commission published additional waste-battery recycling rules on 4 July 2025, with those rules entering into force on 24 July 2025. The framework also sets a 63% portable battery collection target by 2027 and 73% by 2030, while lithium-based battery recycling efficiency must reach 65% by 31 December 2025 and 70% by 31 December 2030.

In the United States, the Department of Energy announced $25 million across 11 projects in December 2024 to advance next-generation battery manufacturing technologies. These actions favor suppliers that can deliver compliant, recoverable, high-cycle batteries with stronger traceability.

Key Takeaways

- Power Tool Batteries Market size is expected to be worth around USD 7.9 Billion by 2035, from USD 3.1 Billion in 2025, growing at a CAGR of 9.8%.

- Lithium-ion held a dominant market position, capturing more than a 76.3% share.

- Cylindrical held a dominant market position, capturing more than a 47.4% share.

- 12 to 18 V held a dominant market position, capturing more than a 48.3% share.

- Industrial held a dominant market position, capturing more than a 39.1% share.

- Asia Pacific emerged as the dominant regional market in 2025, accounting for 44.8% of the global power tool batteries market, with an estimated value of USD 1.3 billion.

By Type Analysis

Lithium-ion dominates the power tool batteries market with a 76.3% share, driven by longer runtime and fast charging convenience.

In 2025, Lithium-ion held a dominant market position, capturing more than a 76.3% share. This strong position mainly comes from its practical advantages in everyday power tool use. Users prefer lithium-ion batteries because they are lightweight, charge faster, and deliver steady power output during long working hours. These batteries also support cordless tool performance much better, which makes them a natural fit for drilling, cutting, fastening, and other heavy-duty applications.

By Cell Format Analysis

Cylindrical cell format leads the market with a 47.4% share, supported by durability and strong fit in cordless power tools.

In 2025, Cylindrical held a dominant market position, capturing more than a 47.4% share. This leadership is largely linked to its strong mechanical design, reliable thermal stability, and easy integration into a wide range of cordless power tools. Manufacturers continue to favor cylindrical cells because they offer consistent energy delivery, better resistance to physical stress, and dependable performance under demanding job site conditions. Their standardized shape also makes battery pack assembly simpler and more cost-efficient, which supports large-scale production.

By Voltage Class Analysis

12 to 18 V leads the voltage class segment with a 48.3% share, thanks to its ideal balance of power and portability.

In 2025, 12 to 18 V held a dominant market position, capturing more than a 48.3% share. This voltage range remains the most widely used in power tools because it offers the right mix of performance, battery life, and ease of handling. It is highly preferred across common tools such as drills, drivers, grinders, and saws, where users need enough power for daily tasks without adding extra weight. Professional users as well as DIY customers continue to choose this range because it supports both medium-duty and demanding applications while maintaining good runtime.

By Application Analysis

Industrial application dominates with a 39.1% share, driven by heavy daily tool usage across manufacturing and construction sites.

In 2025, Industrial held a dominant market position, capturing more than a 39.1% share. This segment continues to lead because power tools are used extensively in manufacturing plants, construction projects, automotive workshops, and maintenance operations where reliable battery performance is essential. Industrial users demand longer runtime, fast recharging, and consistent power output to support continuous operations and reduce downtime. The shift toward cordless tools in factories and job sites has further increased battery demand, as they improve mobility, worker convenience, and operational efficiency.

Key Market Segments

By Type

- Lithium-ion

- Nickel-Cadmium

- Nickel-Metal Hydride

- Others

By Cell Format

- Cylindrical

- Prismatic

- Pouch

By Voltage Class

- Up to 12 V

- 12 to 18 V

- Above 18 V

By Application

- Residential

- Commercial

- Industrial

Emerging Trends

Smart battery management and ultra-fast charging are the latest trends shaping power tool batteries

A major latest trend in the power tool batteries market is the rapid move toward smart battery management systems (BMS) and fast-charging technology. In 2025, the global power tool batteries market reached USD 2.86 billion, showing how strongly users are shifting toward advanced cordless ecosystems. The trend is no longer only about storing more energy; it is now about making batteries intelligent. New battery packs increasingly include embedded chips that monitor temperature, voltage, current flow, overload conditions, and charge cycles in real time.

This helps users improve battery life, reduce overheating risk, and track usage more efficiently across industrial job sites. At the same time, faster charging has become a practical requirement for professionals who cannot afford downtime during drilling, cutting, fastening, or demolition work. In simple terms, the newest trend is smarter batteries that charge quicker, last longer, and communicate tool health data clearly, making cordless tools more reliable in 2025 and 2026.

Shift toward 21700 cells and connected battery platforms is improving high-load performance

Another important trend is the growing use of 21700 high-performance cells and connected battery platforms in professional-grade power tools. Recent 2025 industry technology updates show that 21700 cells are becoming mainstream because they provide better energy density, stronger discharge output, and improved heat management compared to older 18650 formats.

This matters greatly for high-load tools such as impact wrenches, grinders, rotary hammers, and circular saws where stable power delivery is critical. In parallel, connected battery systems with Bluetooth-enabled monitoring are gaining traction, allowing fleet managers and industrial users to track battery level, temperature, charging status, and even tool location. In 2026, the fast-charge lithium-ion battery industry is estimated at USD 13.19 billion, highlighting the broader technology push behind rapid charging and intelligent battery platforms.

Drivers

Rising cordless tool adoption in construction and manufacturing is driving battery demand

One of the biggest drivers for the power tool batteries market is the fast shift from corded tools to cordless tools across construction, industrial maintenance, and manufacturing work. In 2025, the global cordless power tools industry was valued at USD 14.40 billion, showing how quickly battery-powered systems are becoming the preferred choice in daily operations.

The main reason behind this growth is simple: workers need mobility, less downtime, and easier handling on busy job sites. Battery-powered tools remove the need for direct power access, making them highly useful in remote areas, large infrastructure projects, and warehouse environments. This directly increases the need for high-capacity, fast-charging battery packs.

Government infrastructure and industrial modernization programs are accelerating battery use

Another major growth driver is the rise in government-backed infrastructure expansion and industrial modernization programs, especially across emerging economies and developed manufacturing hubs. In 2025, the broader power tools market was estimated at USD 36.7 billion, reflecting strong equipment demand from construction upgrades, transport projects, and factory automation.

Governments are increasing spending on roads, rail, housing, renewable installations, and smart factories, all of which require portable drilling, cutting, fastening, and demolition tools. This creates direct demand for dependable battery systems that can support heavy-duty field operations. In many public projects, cordless tools are increasingly preferred because they improve worker movement, reduce cable-related safety risks, and improve task speed.

Restraints

High raw material price volatility is a major restraint for power tool batteries

One of the biggest restraining factors for the power tool batteries market is the unstable pricing of key battery minerals such as lithium, cobalt, and nickel. These materials directly affect the cost of lithium-ion battery packs used in cordless drills, saws, grinders, and industrial tools. In 2025, the International Energy Agency highlighted that critical mineral supply chains remain highly concentrated, which keeps pricing exposed to mining disruptions, trade restrictions, and geopolitical risks.

For battery makers supplying the power tool industry, this creates difficulty in maintaining stable product pricing and profit margins. When raw material costs rise unexpectedly, manufacturers often face higher pack production costs, which eventually impacts tool prices for end users. This is especially challenging in price-sensitive professional and DIY markets where buyers compare cordless and corded tool costs closely.

Supply concentration and limited domestic processing increase cost pressure

Another strong restraint is the limited domestic refining and processing capacity for battery-grade minerals in many countries. Government-backed supply chain studies, including NITI Aayog’s critical minerals publication, note that the production of lithium, nickel, cobalt, and manganese precursors remains limited in several regions, increasing dependence on imports and overseas processing hubs. Reuters also noted that China controls about 90% of raw material processing for lithium-ion battery types, which shows how dependent global battery manufacturing still is on a concentrated supply chain.

For the power tool batteries market, this creates a major restraint because any disruption in exports, logistics, or policy changes can quickly affect battery cell availability and pricing. In simple terms, even when demand for cordless tools is strong, manufacturers may struggle with supply continuity and cost predictability. This dependency increases lead times, weakens inventory planning, and can reduce adoption among industrial buyers looking for stable procurement in 2025.

Opportunity

Battery recycling and second-life use is opening a major growth path for power tool batteries

One of the biggest growth opportunities for the power tool batteries market is the fast development of battery recycling and second-life ecosystems. In 2026, government-backed circular economy efforts in India highlighted that lithium-ion battery demand is projected to rise from 29 GWh in 2025 to 248 GWh by 2035, creating a large future stream of reusable and recyclable battery materials.

This is a major opportunity for power tool battery makers because recovered lithium, nickel, and cobalt can be reused in new battery packs, helping reduce raw material dependence and improve supply security. For manufacturers of cordless drills, saws, grinders, and industrial tools, this creates room to lower long-term battery costs while improving sustainability goals. Government focus on stronger Extended Producer Responsibility (EPR), formal recycling systems, and chemistry-wise standards is also supporting investment in advanced recovery infrastructure.

Circular economy policies and green jobs expansion create long-term industry upside

Another strong opportunity comes from policy-led circular economy expansion and the economic value linked to battery reuse. Recent trusted industry-backed circular battery studies in India show that battery circularity could unlock a ₹75,500 crore opportunity and create more than 106,000 direct green jobs by 2050.

This is highly relevant for the power tool batteries market because similar lithium-ion chemistries are widely used across cordless equipment. As recycling technology improves, manufacturers can tap into secondary raw materials, refurbished cells, and repurposed storage systems for industrial-grade tools. Government initiatives around waste battery collection, safer transport, refurbishment, and recycling standards are making this opportunity more practical year by year.

Regional Insights

Asia Pacific dominates the power tool batteries market with a 44.8% share, reaching USD 1.3 billion through strong industrial and construction demand

Asia Pacific emerged as the dominant regional market in 2025, accounting for 44.8% of the global power tool batteries market, with an estimated value of USD 1.3 billion. The region’s leadership is strongly supported by its massive manufacturing ecosystem, rapid urban development, and continued expansion in construction and industrial activities.

Countries such as China, India, Japan, and South Korea continue to generate strong demand for cordless drills, impact drivers, grinders, and demolition tools, all of which rely heavily on advanced lithium-ion battery packs. The fast growth of residential and commercial infrastructure projects, along with rising factory automation, has significantly increased battery replacement and new pack demand across the region.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bosch remains one of the strongest names in the power tool batteries market, supported by its wide 18V and 12V lithium-ion battery platforms used across professional and DIY tools. In 2025, Bosch’s parent group generated EUR 90.3 billion in revenue, reflecting its strong industrial scale and R&D capability. Its battery systems are known for fast charging, thermal protection, and cross-tool compatibility across 100+ tools, which strengthens customer retention and replacement battery sales. The company’s continuous investment in smart battery management and durable pack design keeps it highly competitive in industrial applications.

Hilti Corporation holds a premium position in the power tool batteries market, especially in construction and heavy-duty industrial use. Its 22V Nuron battery platform, launched for high-load professional tools, has strengthened its battery ecosystem with better runtime and cloud-based tool tracking. Hilti reported around CHF 6.4 billion in sales in 2025, supported by strong demand from infrastructure and commercial construction. The company focuses on high-cycle lithium-ion packs, durable battery casings, and intelligent fleet management systems, making it a strong player in contractor-focused battery solutions where uptime and productivity are critical.

Panasonic Corporation plays an important role in the power tool batteries market through its strong lithium-ion cell manufacturing expertise. In 2025, Panasonic Holdings reported nearly JPY 8.5 trillion in revenue, supported by its global battery and electronics business. The company’s cylindrical lithium-ion cells are widely used in high-performance battery packs for industrial tools, offering strong energy density and long cycle life. Its numerical strength lies in advanced 18650 and 21700 cell production, which supports reliable battery pack assembly for premium cordless tool systems. Panasonic’s scale in cell innovation continues to support stable growth in professional battery-powered tools.

Top Key Players Outlook

- Bosch Ltd

- Hilti Corporation

- Hitachi Ltd

- Makita Corporation

- Panasonic Corporation

- Ryobi Limited

- Samsung SDI Co. Ltd

- Sony Group Corporation

- Stanley Black & Decker Inc.

- Techtronic Industries Company Limited

Recent Industry Developments

In 2025, Bosch Ltd continued to strengthen its position in the power tool batteries sector through its advanced 18V and 12V lithium-ion battery ecosystem, widely used across professional and DIY cordless tools.

In 2025, Hilti Corporation further strengthened its position in the power tool batteries sector through the expansion of its 22V Nuron battery platform, which has become a major growth engine across professional construction tools.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.1 Bn |

| Forecast Revenue (2035) | USD 7.9 Bn |

| CAGR (2026-2035) | 9.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Lithium-ion, Nickel-Cadmium, Nickel-Metal Hydride, Others), By Cell Format (Cylindrical, Prismatic, Pouch), By Voltage Class (Up to 12 V, 12 to 18 V, Above 18 V), By Application (Residential, Commercial, Industrial) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bosch Ltd, Hilti Corporation, Hitachi Ltd, Makita Corporation, Panasonic Corporation, Ryobi Limited, Samsung SDI Co. Ltd, Sony Group Corporation, Stanley Black & Decker Inc., Techtronic Industries Company Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |