Quick Navigation

Report Overview

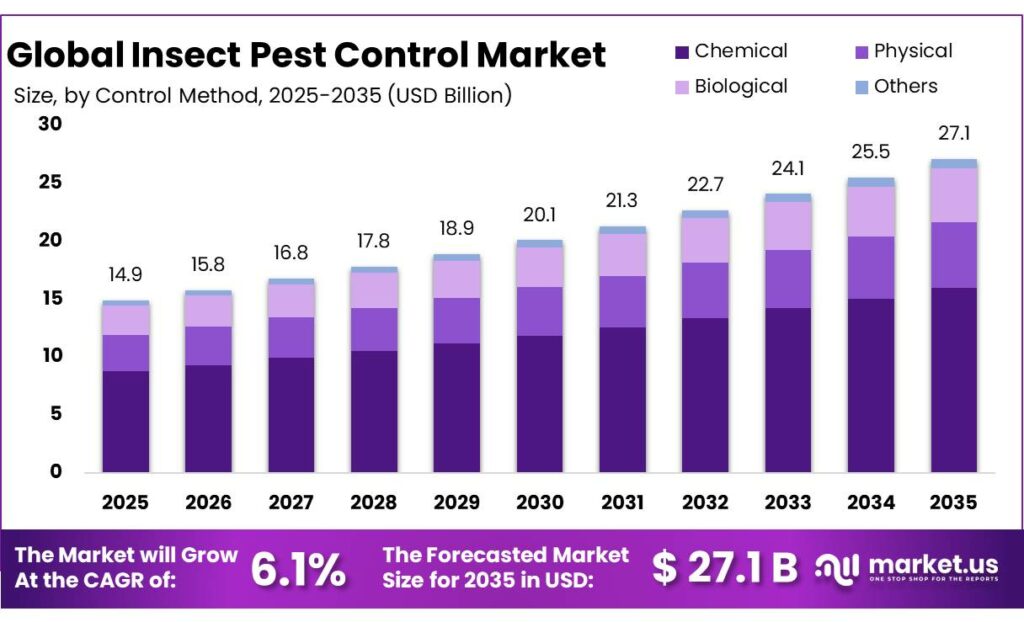

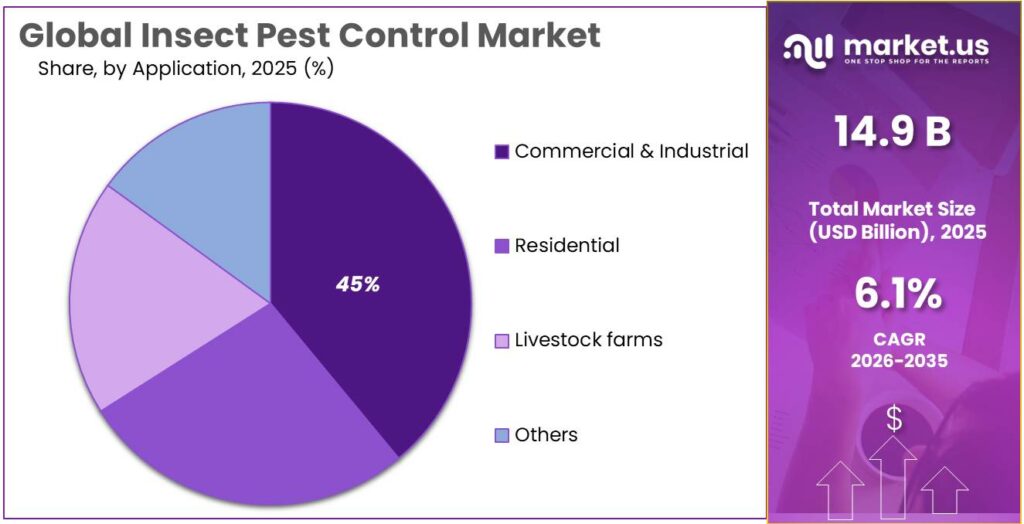

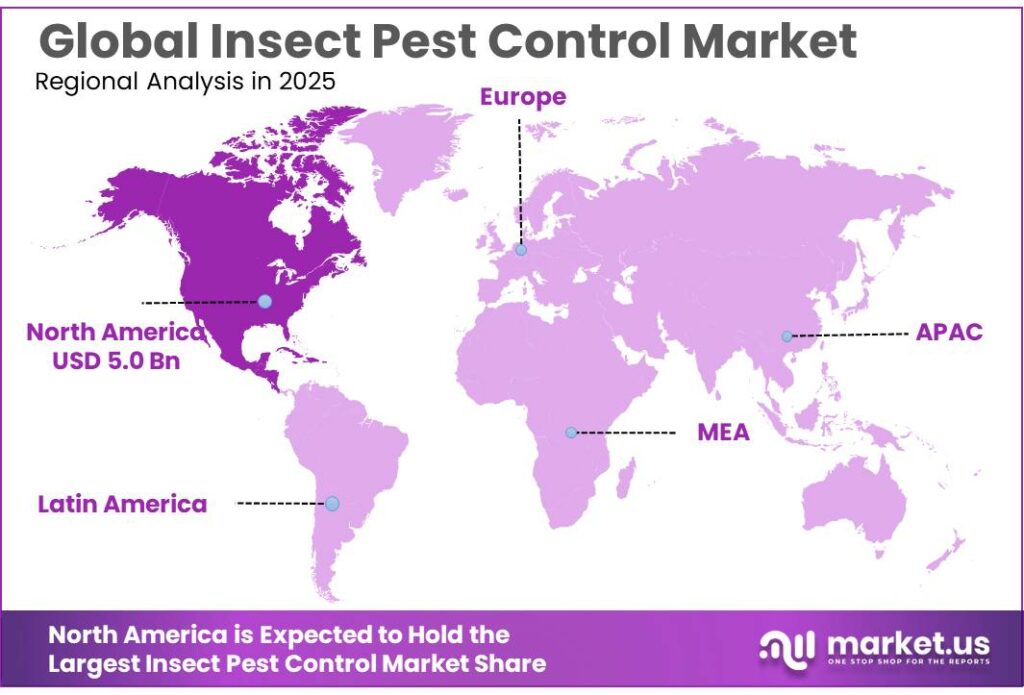

The Global Insect Pest Control Market size is expected to be worth around USD 27.1 Billion by 2035, from USD 14.9 Billion in 2025, growing at a CAGR of 6.1% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 34.1% share, holding USD 5.0 Billion revenue.

The industrial outlook for insect pest control remains fundamentally tied to food security, yield protection, and phytosanitary compliance. FAO states that up to 40% of global crops are lost every year to plant pests and diseases, while these losses cost the global economy more than USD 220 billion annually. That scale of avoidable loss keeps insect pest control positioned as a core input market for commercial agriculture, horticulture, stored-grain systems, and public plant-health programs rather than a discretionary spend.

Regulatory pressure is accelerating that transition. In the European Union, the policy direction remains clear: the Farm to Fork framework calls for a 50% reduction in the use and risk of chemical pesticides, and also a 50% reduction in more hazardous pesticides by 2030; separately, the European Commission reports that the use of more hazardous pesticides was already down 27% in 2018–2023 versus the 2015–2017 baseline. This is pushing suppliers to reposition portfolios toward lower-residue, targeted, and IPM-compatible solutions.

Demand is also being supported by non-agricultural use cases. The WHO reports that vector-borne diseases account for more than 17% of all infectious diseases and cause more than 700,000 deaths annually, while malaria alone is associated with an estimated 249 million cases and more than 608,000 deaths each year. That keeps household insecticides, professional vector control, and public-sector mosquito management commercially important alongside crop protection. In effect, insect pest control is no longer just a farm-input category; it is increasingly a cross-sector resilience industry.

In the United States, the EPA announced that it had registered 15 new biopesticide active ingredients since January 2025, a useful signal that biological and reduced-risk products are moving faster into the commercial pipeline. That trend supports opportunities in microbial insecticides, pheromone-based disruption, precision application, and combined chemical-biological programs.

Key Takeaways

- Insect Pest Control Market size is expected to be worth around USD 27.1 Billion by 2035, from USD 14.9 Billion in 2025, growing at a CAGR of 6.1%.

- Dry held a dominant market position, capturing more than a 65.3% share.

- Termites held a dominant market position, capturing more than a 23.6% share.

- Chemical held a dominant market position, capturing more than a 59.8% share.

- Residential held a dominant market position, capturing more than a 39.9% share.

- North America held the dominant position in the global insect pest control market, accounting for 34.1% of the total market share, valued at USD 5.0 billion.

By Form Analysis

Dry dominates with 65.3% thanks to easy handling, longer shelf life, and better storage convenience.

In 2025, Dry held a dominant market position, capturing more than a 65.3% share. This strong position was mainly supported by its practical use across insect pest control applications where easy storage, simple transportation, and longer product stability matter most. Dry-form products are widely preferred because they are convenient to apply, especially in agricultural fields, warehouses, and household pest treatment areas where moisture-sensitive conditions can affect performance. Users also find dry solutions more economical for bulk usage, as they are easier to pack, store for extended periods, and use when needed without special handling requirements.

By Insect Type Analysis

Termites lead with 23.6% as rising structural damage concerns continue to drive steady treatment demand.

In 2025, Termites held a dominant market position, capturing more than a 23.6% share. This segment remained a key part of the insect pest control market due to the growing need to protect residential, commercial, and industrial properties from costly structural damage. Termite infestations are often difficult to detect in the early stages, which makes preventive inspections and timely treatment highly important for property owners. As a result, demand stayed strong for termite-focused control solutions across both urban housing and large commercial buildings. In 2025, the segment also benefited from increasing awareness among homeowners about long-term wood protection and foundation safety, especially in regions with warm and humid climates where termite activity is more common.

By Control Method Analysis

Chemical control leads with 59.8% because it delivers fast action and dependable results across large-scale pest problems.

In 2025, Chemical held a dominant market position, capturing more than a 59.8% share. This segment continued to lead the insect pest control market due to its quick effectiveness, wide availability, and ability to handle a broad range of insect infestations in residential, commercial, agricultural, and industrial settings. Chemical-based control methods remained the preferred choice for immediate pest elimination, especially in situations where infestations spread rapidly and require fast intervention. In 2025, users continued to rely on chemical solutions for their proven performance against common insects such as termites, mosquitoes, ants, cockroaches, and flies.

By Application Analysis

Residential use leads with 39.9% as households continue to prioritize safe and regular insect protection.

In 2025, Residential held a dominant market position, capturing more than a 39.9% share. This segment remained at the forefront of the insect pest control market as homeowners increasingly focused on maintaining clean, healthy, and pest-free living spaces. Rising concerns over insects such as mosquitoes, cockroaches, ants, termites, and bed bugs continued to support steady demand for residential pest control solutions throughout 2025. The segment’s growth was also supported by higher awareness of hygiene, family health, and property protection, especially in urban homes and apartment complexes where infestations can spread quickly.

Key Market Segments

By Form

- Dry

- Liquid

By Insect Type

- Termites

- Cockroaches

- Bedbugs

- Mosquitoes

- Flies

- Ants

- Others

By Control Method

- Chemical

- Physical

- Biological

- Others

By Application

- Commercial & Industrial

- Residential

- Livestock farms

- Others

Emerging Trends

Smart monitoring and bio-based IPM are becoming the latest defining trend in insect pest control

One of the most important latest trends in the insect pest control market is the rapid move toward smart pest monitoring combined with integrated biological control systems. In 2025, this trend became stronger as growers and pest management teams increasingly adopted digital alert systems, sensor-based traps, and data-driven treatment planning. FAO’s 2025 global pest management guidance highlighted digital alert systems, robotics, and biopesticides across 8 global priority pests and pathogens, showing how fast the industry is shifting from reactive spraying to precision prevention.

This change is happening because pest pressure is rising sharply, with FAO reporting that pests, weeds, and diseases now cause USD 220 billion in annual losses to the global agri-food sector. In simple terms, users now want to know when and where insects appear before they spread. Smart traps, IoT sensors, and AI-supported field alerts help reduce unnecessary chemical use while improving treatment timing.

Government-led IPM programs are pushing eco-friendly trend adoption at scale

A second major trend is the wider adoption of government-backed Integrated Pest Management (IPM) and biodiversity-first control methods. FAO’s latest guidance shows that across earlier IPM field programs, pesticide use was reduced by 25% on average, while crop yields improved by 13% and farm profit increased by 20%. In several crops such as rice, cabbage, cotton, and tea, pesticide use was cut by 80% to 92%, which clearly shows why this approach is becoming a major industry trend.

Governments and agricultural agencies are now using these outcomes to support farmer training, digital surveillance, and biological control adoption programs. FAO also estimates that plant pests and diseases still reduce 20% to 40% of global crop yields every year, which keeps pressure high for more sustainable and scalable solutions.

Drivers

Rising global crop losses are pushing stronger demand for insect pest control

One of the biggest driving factors for the insect pest control market is the growing pressure to protect food production from heavy crop losses caused by insects and other plant pests. Across global agriculture, this issue has become more serious as farmers work to improve yields on limited land. According to FAO, up to 40% of global food crops are lost every year due to plant pests, creating a major burden on food security and farm income.

This number clearly shows why insect pest control solutions remain essential across cereals, fruits, vegetables, and storage facilities. In simple terms, when such a large share of crops is damaged before reaching consumers, growers naturally increase spending on prevention and treatment solutions. This includes field spraying, baiting, fumigation, and integrated pest monitoring systems. The need becomes even stronger in countries where agriculture supports exports and rural livelihoods.

Government-backed plant health programs and farmer training are strengthening market growth

Another major growth driver comes from government initiatives and trusted agricultural institutions promoting plant health and pest prevention. FAO has expanded farmer support through its Farmer Field School programs, which have improved the livelihoods of over 12 million farmers globally. These programs help farmers identify insect outbreaks early, choose the right control method, and reduce avoidable crop losses.

Governments in many countries are also investing in plant protection missions, food security schemes, and awareness campaigns around invasive pests, termites, locusts, and storage insects. Such programs increase adoption of both chemical and biological pest control solutions at the farm and household level. In addition, the global food chain already loses 13.2% of food after harvest before retail, according to FAO food loss data, and insect infestation during storage remains one of the key reasons.

Restraints

Rising insecticide resistance is reducing treatment effectiveness and slowing market confidence

One major restraining factor for the insect pest control market is the fast-growing problem of insecticide resistance, where insects no longer respond to products that once worked effectively. This creates a serious challenge for both agricultural and public health pest control programs. According to FAO, two-thirds of countries face major problems with pesticide resistance in agriculture, which directly limits the long-term effectiveness of chemical insect control solutions.

When farmers, warehouse operators, and pest control service providers repeatedly use the same active ingredients, insects gradually adapt, making treatments weaker over time. This leads to higher application frequency, increased costs, and lower trust in standard chemical solutions. In simple terms, when the same spray no longer gives the same result, users become cautious about spending more. This resistance issue is especially difficult in high-value crops and grain storage, where even small infestations can create major losses.

Regulatory pressure and safer pest management rules are limiting chemical product expansion

Another strong restraint comes from stricter government regulations and international safety frameworks around pesticide use. FAO and WHO continue to strengthen the International Code of Conduct on Pesticide Management, with recent joint reviews focused on resistance, environmental safety, and human health risks.

As regulators tighten rules on residues, soil impact, water contamination, and safe dosage levels, many traditional insect control products face slower approvals or usage restrictions. This directly affects how quickly manufacturers can expand chemical product portfolios. FAO also notes that up to 40% of global crop production is still lost to pests and diseases, yet excessive pesticide dependence has pushed governments toward safer, lower-risk solutions.

Opportunity

Biological pest control adoption is creating the biggest growth opportunity for insect pest control

One of the strongest growth opportunities in the insect pest control market is the rapid shift toward biological and biodiversity-friendly pest control solutions. Farmers, food producers, and public agencies are increasingly looking for safer alternatives to heavy chemical use, especially as resistance and residue concerns continue to rise. FAO highlighted in 2025 that pests, weeds, and diseases now cause nearly USD 220 billion in losses annually to the global agri-food sector, which is pushing faster adoption of innovative biological control methods.

This scale of loss is creating clear room for bio-based insect control products such as microbial sprays, parasitoids, predators, pheromone traps, and biopesticides. In practical farming, these methods are becoming attractive because they help protect crop quality while supporting export compliance and food safety standards. The opportunity is especially strong in fruits, vegetables, greenhouse crops, and grain storage, where residue-free treatment is highly valued.

Government IPM programs and FAO-backed sustainable guidelines are accelerating future demand

Another major opportunity comes from government-backed Integrated Pest Management (IPM) and sustainable agriculture initiatives. In May 2025, FAO released new pest management guidelines covering eight global priority pests and diseases, with strong emphasis on biopesticides, robotics, digital alert systems, and eco-friendly crop protection practices.

This is a major long-term market opportunity because such trusted frameworks directly influence farmer adoption, subsidy structures, and national crop protection policies. Governments are increasingly funding pest surveillance systems, farmer training, and safer pesticide transition programs, which expands the use of advanced insect control technologies. FAO also continues promoting biological control for transboundary plant pests through early warning and cross-country coordination programs, helping suppliers enter larger agricultural markets.

Regional Insights

North America dominated the insect pest control market with a 34.1% share, reaching USD 5.0 billion, supported by strict food safety standards and large-scale residential demand.

North America held the dominant position in the global insect pest control market, accounting for 34.1% of the total market share, valued at USD 5.0 billion. The region’s leadership is strongly supported by the United States and Canada, where demand remains consistently high across residential, commercial, food processing, agriculture, and public health applications. One of the strongest regional growth drivers is the strict regulatory environment around hygiene and pesticide safety, led by agencies such as the U.S. Environmental Protection Agency (EPA), which continues to maintain rigorous pesticide registration and consumer safety standards.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bayer remains one of the strongest players in insect pest control, supported by its 2025 annual revenue base of around €46.6 billion, with Crop Science contributing a major share globally. The company’s strength comes from insecticides, termite control formulations, mosquito management products, and advanced biological crop protection tools. Its wide global distribution across North America, Europe, and Asia gives it strong market penetration.

BASF holds a strong competitive position with 2025 group revenue of nearly €68.9 billion, supported by a solid agricultural solutions portfolio. In insect pest control, BASF is highly active in professional pest management chemicals, residual sprays, bait systems, and grain protection solutions. The company’s numerical strength is supported by strong innovation spending and broad product registrations across developed and emerging regions.

Korea Henkel Home Care Co. Ltd. maintains a focused presence in the household insect pest control space, supported by Henkel’s global 2025 sales base of around €21.5 billion. The company performs strongly in home-use sprays, cockroach baits, ant gels, and mosquito repellents across Asian consumer markets. Its numerical strength is linked to brand trust in home care and easy retail availability.

Top Key Players Outlook

- Bayer

- BASF

- Sumitomo Chemical

- Korea Henkel home care Co. Ltd.

- FMC Corporation

- Syngenta

- ADAMA

- Rentokil Initial Group

- Terminix

- Rollins, Inc.

Recent Industry Developments

In 2025, Bayer remained one of the most influential companies in the insect pest control sector, supported by its strong Crop Science platform and broad crop protection portfolio. The company’s Crop Science sales reached €21.622 billion in 2025, showing a 1.1% year-on-year increase, which reflects stable demand for insecticides, seed treatments, vector control solutions, and integrated pest management technologies.

In 2025, BASF continued to hold a strong position in the insect pest control sector through its Agricultural Solutions business, which reported €9,587 million in total segment sales. Within this, the company generated €1,089 million specifically from insecticides, showing the clear scale of its direct involvement in insect pest management across agriculture and professional applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 14.9 Bn |

| Forecast Revenue (2035) | USD 27.1 Bn |

| CAGR (2026-2035) | 6.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Dry, Liquid), By Insect Type (Termites, Cockroaches, Bedbugs, Mosquitoes, Flies, Ants, Others), By Control Method (Chemical, Physical, Biological, Others), By Application (Commercial And Industrial, Residential, Livestock farms, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bayer, BASF, Sumitomo Chemical, Korea Henkel home care Co. Ltd., FMC Corporation, Syngenta, ADAMA, Rentokil Initial Group, Terminix, Rollins, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |