Quick Navigation

Report Overview

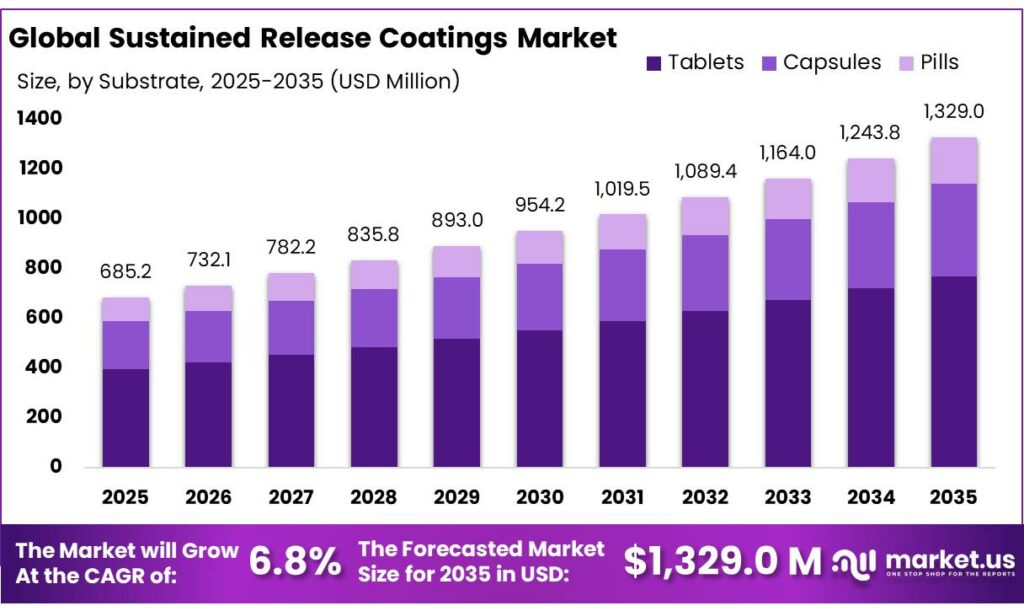

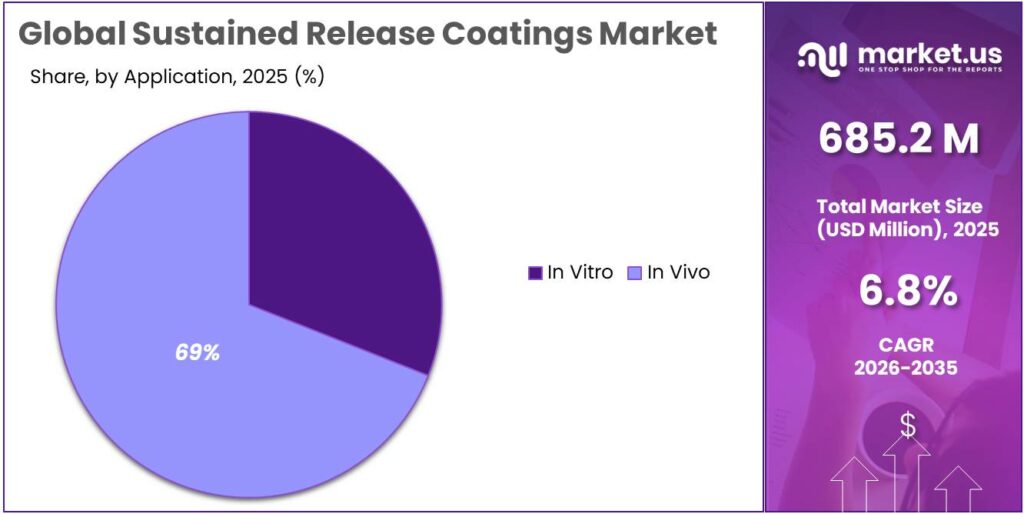

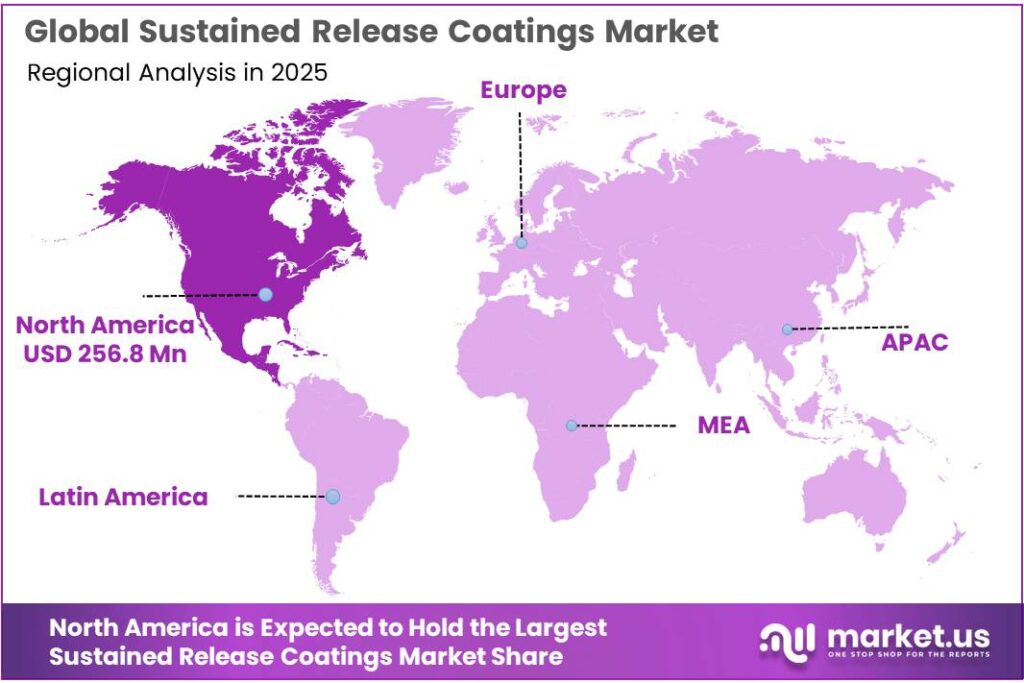

The Global Sustained Release Coatings Market size is expected to be worth around USD 1,329.0 Million by 2035, from USD 685.2 Million in 2025, growing at a CAGR of 6.8% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 37.5% share, holding USD 256.8 Million revenue.

Sustained release coatings represent a specialized but increasingly strategic segment of the drug-delivery value chain, especially in oral solid dosage forms such as film-coated tablets, pellets, multiparticulates, and capsules. Their industrial role is to modulate release kinetics, improve dosing convenience, reduce peak-to-trough variability, and support lifecycle management for complex formulations.

The category is gaining stronger commercial relevance because oral solids remain the industry’s manufacturing backbone: the U.S. FDA states that 9 out of 10 prescriptions filled in the United States are for generic drugs, while FDA’s Office of Generic Drugs says generics account for more than 90% of prescriptions, reinforcing the scale of formulation platforms where coating functionality matters.

From an industrial scenario perspective, the market is being shaped by the intersection of pharmaceuticals and health-focused consumer products rather than by commodity coatings. On the consumer-health side, the Council for Responsible Nutrition reported in 2024 that 75% of U.S. adults take dietary supplements; within that base, magnesium usage rose to 23% of supplement users and prebiotic usage reached 7%, indicating a broader shift toward condition-specific and performance-oriented products where differentiated release can add value.

The principal growth drivers are regulatory standardization, patient-centric dosing, and the technical rise of complex oral solids. In 2025, the FDA issued the draft M13B guidance on additional-strength biowaivers for immediate-release solid oral dosage forms on 24 February 2025, while WHO published its Biowaiver List for immediate-release solid oral dosage forms on 15 April 2025. Although these are not sustained-release guidelines per se, they signal a broader regulatory push toward more structured, science-based evaluation of solid dosage performance.

In parallel, EMA’s Q&A for co-processed excipients used in solid oral dosage forms gives risk thresholds such as more than 30%, 45%, and 60% formulation share in example classifications, showing how deeply excipient functionality and formulation architecture are entering regulatory scrutiny.

The Council for Responsible Nutrition stated that approximately 75% of U.S. adults used dietary supplements in 2024, and 91% of supplement users considered supplements essential to maintaining health. In Europe, food supplements remain tightly governed under Directive 2002/46/EC, while EFSA notes that food supplements may also contain permitted food additives, including coating agents, under Regulation (EC) No 1333/2008. This regulatory structure supports demand for coating systems that can deliver functionality without compromising compliance.

Evonik remains one of the clearest reference points in sustained release coatings through its EUDRAGIT platform. The company states that EUDRAGIT has been used for 70 years, is linked to over 23,000 patents, and appears in more than 10,000 scientific publications, underscoring both IP depth and formulation maturity. Its 2025 development trajectory was notable: Evonik continued technical market activation through its March 2025 and May 2025 EUDRAGIT workshops and, later in October 2025, launched EUDRACAP colon functional capsules in GMP quality for clinical and commercial use.

Key Takeaways

- Sustained Release Coatings Market size is expected to be worth around USD 1,329.0 Million by 2035, from USD 685.2 Million in 2025, growing at a CAGR of 6.8%.

- Tablets held a dominant market position, capturing more than a 58.9% share.

- Ethyl & Methyl Cellulose held a dominant market position, capturing more than a 34.7% share.

- In Vivo held a dominant market position, capturing more than a 69.1% share.

- North America holds a leading position in the sustained release coatings market, accounting for a dominant 37.5% share, valued at USD 256.8 million.

By Substrate Analysis

Tablets dominate with 58.9% driven by ease of formulation and widespread pharmaceutical use

In 2025, Tablets held a dominant market position, capturing more than a 58.9% share. This strong lead is mainly because tablets are the most commonly used dosage form in the pharmaceutical industry, making them a natural fit for sustained release coatings. Manufacturers prefer tablets due to their stability, ease of large-scale production, and compatibility with different coating technologies. Sustained release coatings help improve patient compliance by reducing dosing frequency, which is especially important for chronic treatments where tablets are widely prescribed.

By Polymer Material Analysis

Ethyl & Methyl Cellulose leads with 34.7% thanks to reliable release control and versatility

In 2025, Ethyl & Methyl Cellulose held a dominant market position, capturing more than a 34.7% share. These polymers are widely used because they provide consistent and controlled drug release, which is a key requirement in sustained release coatings. Their compatibility with a wide range of active pharmaceutical ingredients makes them a preferred choice for manufacturers. They are also valued for their stability and ease of processing, helping companies maintain uniform coating quality during large-scale production.

By Application Analysis

In Vivo dominates with 69.1% as real-time drug performance drives demand

In 2025, In Vivo held a dominant market position, capturing more than a 69.1% share. This segment leads because testing and performance evaluation inside the human body remains the most reliable way to understand how sustained release coatings behave in real conditions. Pharmaceutical companies depend heavily on in vivo studies to confirm drug release patterns, absorption, and overall effectiveness before moving forward with approvals. These coatings are designed to control how a drug is released over time, and only in vivo applications can truly validate that performance.

Key Market Segments

By Substrate

- Tablets

- Capsules

- Pills

By Polymer Material

- Ethyl & Methyl Cellulose

- Polyvinyl & Cellulose Acetate

- Methacrylic Acid

- PEG

- Others

By Application

- In Vitro

- In Vivo

Emerging Trends

Shift toward advanced and functional coating technologies is shaping the next phase of growth

One of the most noticeable trends in sustained release coatings is the move toward more advanced and functional coating systems. Earlier, coatings were mainly used for protection or appearance, but now they are designed to actively control how a drug behaves inside the body. New technologies like multi-layer coatings and pH-sensitive polymers are becoming more common, allowing medicines to release at specific points in the digestive system.

At the same time, industries like food and nutrition are also using similar coating approaches. For example, encapsulation technologies are being widely adopted to protect vitamins and probiotics, showing how controlled release is expanding beyond pharmaceuticals. The global microencapsulation market alone reached around USD 15.63 billion in 2025, reflecting strong demand for controlled delivery systems across industries.

Growing use of natural and sustainable polymers is becoming a key industry trend

Another important trend is the rising focus on natural and sustainable coating materials. With increasing awareness around environmental impact and safety, manufacturers are shifting toward plant-based and biodegradable polymers. Materials like alginates, guar gum, and other natural gums are gaining attention because they are safer, more sustainable, and still effective in controlling drug release.

This shift is also influenced by trends in the food industry, where clean-label and natural ingredients are becoming a priority. Encapsulation techniques are now widely used in food products to improve shelf life and stability of ingredients like flavors and nutrients. According to industry data, polymers account for around 28% of coating material use in encapsulation technologies in 2025, showing their strong and growing role across sectors.

Drivers

Rising demand for oral medicines is pushing sustained release coating adoption

One of the biggest driving factors for sustained release coatings is the growing use of oral medicines across the world. Most treatments today are designed to be simple and easy for patients, and oral dosage forms like tablets and capsules fit perfectly into that need. According to research backed by health studies, around 90% of pharmaceutical formulations are taken orally, showing how dominant this route has become. At the same time, about 73% of medicines are administered through the oral route, which highlights how widely it is used in everyday treatment.

Sustained release coatings help by controlling how slowly or quickly a drug is released, reducing the need for repeated dosing. This becomes very useful for patients managing long-term conditions like diabetes or heart disease. In 2025 and 2026, pharmaceutical companies continued focusing on patient-friendly drug formats, and coatings became a key part of that strategy. The more oral medicines grow, the more important these coatings become in making treatments effective, convenient, and easier to follow.

Government support and essential medicine programs are strengthening long-term demand

Another important driver comes from global healthcare systems and government-backed medicine programs. Organizations like the World Health Organization continue to push access to safe and effective medicines worldwide. As of 2025, the WHO Model List includes over 520 essential medicines, and more than 150 countries follow this list to guide their healthcare systems.

Governments are also investing more in improving access to chronic disease treatments, which typically require long-term medication use. Sustained release coatings support this by reducing dosing frequency and improving patient adherence, especially in large public health programs.

Restraints

High manufacturing cost and strict regulatory requirements slow down adoption

One of the major restraining factors for sustained release coatings is the high cost involved in manufacturing and compliance. Developing these coatings is not a simple process—it requires specialized equipment, controlled environments, and skilled handling. For example, pharmaceutical coating often involves complex steps like solvent evaporation, temperature control, and precise layering, all of which increase operational expenses.

Governments and global health organizations continue to push for affordable medicines, but this creates pressure on manufacturers to balance cost and quality. According to the World Health Organization, over 150 countries rely on its essential medicines list, meaning affordability is a key expectation in drug supply systems.

Process complexity and risk of product failure limit large-scale use

Another key challenge is the complexity of the coating process itself and the risk of errors during production. Sustained release coatings require very precise control over thickness, material composition, and environmental conditions. Even small variations can affect how the drug is released in the body, which can lead to product recalls or failures. Industry insights highlight that increasing product recalls remain a concern in pharmaceutical coating markets, showing how sensitive the process can be.

In addition, continuous coating systems may produce waste at the beginning and end of production cycles, adding to inefficiencies and cost burdens. Governments are encouraging better manufacturing practices and quality standards, but this also means companies must invest more in monitoring systems and validation processes. For many manufacturers, especially in cost-sensitive markets, this level of complexity becomes a barrier rather than an advantage.

Opportunity

Growing burden of chronic diseases is opening strong opportunities for sustained release coatings

One of the biggest growth opportunities for sustained release coatings comes from the rising number of people living with long-term diseases. Conditions like diabetes, heart disease, and obesity are increasing at a fast pace, and they usually require continuous medication over long periods. According to the World Health Organization, noncommunicable diseases caused at least 43 million deaths globally in 2021, accounting for around 75% of all non-pandemic deaths

In 2025 and 2026, healthcare systems have been focusing more on long-term disease management rather than just short-term treatment. Governments and global health bodies are also pushing programs for better chronic disease care, which supports the use of advanced drug delivery systems. As the number of patients continues to grow, the need for more efficient and patient-friendly medicines creates a clear opportunity for sustained release coatings to expand further.

Rising diabetes and obesity cases are creating demand for better drug delivery systems

Another strong opportunity is linked to the rapid increase in lifestyle-related diseases like diabetes and obesity. According to the International Diabetes Federation, around 590 million people worldwide are living with diabetes, which is about 1 in 9 adults. At the same time, the WHO reports that 2.5 billion adults were overweight in 2022, including over 890 million living with obesity. These numbers are expected to grow further in the coming years.

Governments are also introducing awareness programs and treatment guidelines to control these diseases, which indirectly supports advanced drug delivery technologies. In 2026, pharmaceutical companies are focusing more on improving patient adherence, especially for chronic therapies, and sustained release coatings play a key role in that. As more people require daily or lifelong treatment, the demand for controlled and efficient drug release solutions is likely to rise steadily, opening new growth paths for this market.

Regional Insights

North America dominates with 37.5% share valued at USD 256.8 Mn driven by strong pharmaceutical infrastructure

North America holds a leading position in the sustained release coatings market, accounting for a dominant 37.5% share, valued at USD 256.8 million. The region’s leadership is largely supported by its well-established pharmaceutical ecosystem, especially in countries like the United States and Canada. The presence of advanced research facilities, strong regulatory frameworks, and high healthcare spending continues to create a favorable environment for the adoption of sustained release coating technologies. In addition, the region benefits from early adoption of advanced drug delivery systems, which has significantly improved treatment outcomes and patient compliance.

The United States plays a central role in this dominance, as it contributes a major portion of global pharmaceutical activity. In fact, the U.S. accounts for nearly 50% of global pharmaceutical sales, which directly supports the demand for innovative drug delivery solutions like sustained release coatings. The growing burden of chronic diseases, including cardiovascular conditions and diabetes, has also increased the need for long-acting medications, further driving demand across the region.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE remains one of the largest players in the sustained release coatings market, backed by its massive global chemical operations. In 2025, the company reported total sales of €59.7 billion, showing its strong financial base and wide product reach across pharmaceuticals and specialty chemicals. Its Nutrition & Care segment alone generated over €6.5 billion, supporting excipients and coating materials used in drug delivery. BASF’s global workforce of over 110,000 employees and presence in multiple industries help it maintain a stable supply chain and continuous innovation in coating technologies.

Evonik is a key player known for its expertise in specialty polymers and drug delivery systems. In 2025, the company generated €14.1 billion in revenue, with a net income of around €265 million, reflecting its strong position in high-value chemical segments. Evonik operates in over 100 countries and employs more than 31,000 people, allowing it to support pharmaceutical manufacturers globally. Its focus on advanced excipients and controlled release technologies makes it a preferred partner for sustained release coating solutions.

Top Key Players Outlook

- BASF SE

- Evonik

- Colorcon

- Coating Place, Inc.

- Teva Pharmaceutical Industries Ltd.

- Pfizer, Inc.

- Sun Pharmaceutical Industries Ltd.

- Novartis AG

- AstraZeneca

- GlaxoSmithKline plc

- AbbVie Inc.

Recent Industry Developments

Colorcon holds a specialized and strong position in the sustained release coatings sector, mainly through its film coating systems and modified release technologies used in oral solid dosage forms. In 2025, the company generated around USD 170 million in revenue, showing its steady presence as a focused pharmaceutical excipient provider

Evonik plays a very focused and technology-driven role in the sustained release coatings sector, mainly through its advanced drug delivery solutions and specialty polymers. In 2025, the company reported total sales of €14.1 billion, with a net income of €265 million, showing stable financial strength despite market pressures

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 685.2 Mn |

| Forecast Revenue (2035) | USD 1,329.0 Mn |

| CAGR (2026-2035) | 6.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Substrate (Tablets, Capsules, Pills), By Polymer Material (Ethyl And Methyl Cellulose, Polyvinyl And Cellulose Acetate, Methacrylic Acid, PEG, Others), By Application (In Vitro, In Vivo) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BASF SE, Evonik, Colorcon, Coating Place, Inc., Teva Pharmaceutical Industries Ltd., Pfizer, Inc., Sun Pharmaceutical Industries Ltd., Novartis AG, AstraZeneca, GlaxoSmithKline plc, AbbVie Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |