Quick Navigation

Report Overview

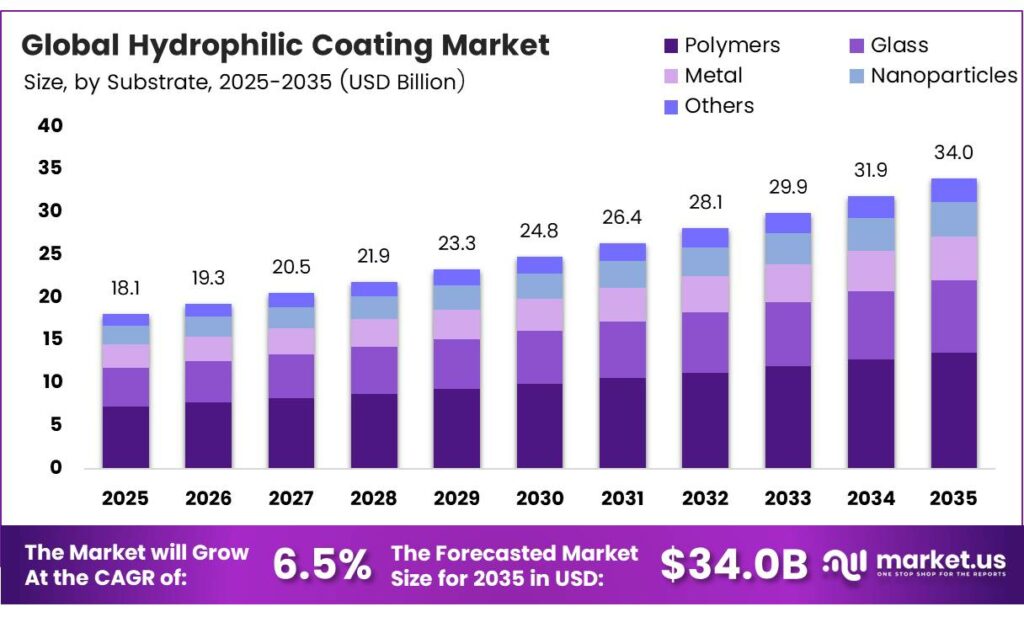

The Global Hydrophilic Coating Market size is expected to be worth around USD 34.0 billion by 2035 from USD 18.1 billion in 2025, growing at a CAGR of 6.5% during the forecast period 2026 to 2035.

The hydrophilic coating market covers surface treatment technologies that attract and retain water molecules on substrates. These coatings reduce friction, improve biocompatibility, and enhance device performance across medical, aerospace, and industrial applications. Manufacturers apply them to polymers, glass, metals, and nanoparticles for diverse end-use functions.

Hydrophilic coatings deliver measurable performance gains that justify their growing adoption. Hydrophilic coating reduces the catheter friction coefficient from 1.3 to 0.03, representing a 53% improvement in lubricity versus unmodified TPU catheters. This performance level signals strong clinical value and drives OEM procurement decisions globally.

Advanced coating chemistries further expand performance benchmarks across substrate types. A hydrophilic PDA-PVP/PEG coating on TPU reduces the water contact angle from 91.3° to approximately 28° and the friction coefficient from 0.4 to around 0.03, while maintaining integrity after 30 minutes of reciprocating sliding. This durability data strengthens market confidence in next-generation coating solutions.

Contract coating outsourcing expands rapidly as MedTech OEMs seek faster regulatory documentation and scale-up support. Moreover, innovations in UV-curable inline cure platforms and dual-function hybrid surface technologies attract significant R&D investment. These trends accelerate market adoption across both established and emerging application segments.

Key Takeaways

- The Global Hydrophilic Coating Market was valued at USD 18.1 billion in 2025 and is projected to reach USD 34.0 billion by 2035, growing at a CAGR of 6.5%.

- Polymers held the dominant position with a 45.2% market share in 2025.

- Dip Coating led the segment with a 46.8% share.

- Water Repellent accounted for the largest share at 36.3%.

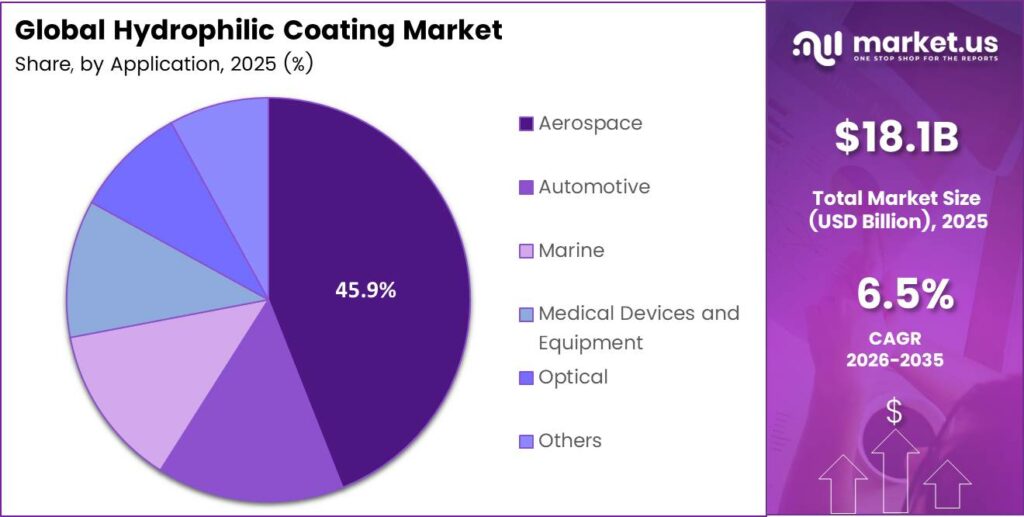

- Aerospace dominated with a 45.9% share.

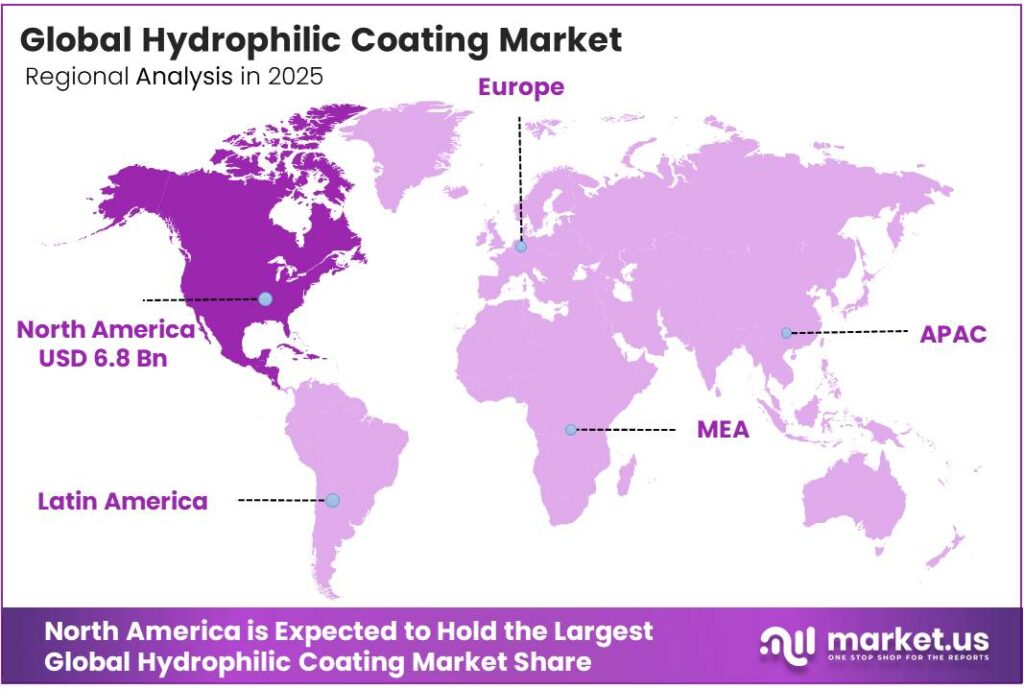

- North America led regional markets with a 37.5% share, valued at USD 6.8 billion in 2025.

By Substrate Analysis

Polymers dominate with 45.2% due to widespread use in medical devices and catheter platforms.

In 2025, Polymers held a dominant market position in the By Substrate segment of the Hydrophilic Coating Market, with a 45.2% share. Polymer substrates offer flexibility, biocompatibility, and ease of processing. Moreover, catheter and tubing manufacturers rely heavily on polymer bases to deliver consistent coating adhesion across complex device geometries.

Glass substrates maintain a steady market presence, particularly in optical and laboratory diagnostic applications. Glass surfaces accept hydrophilic coatings well, enabling anti-fog and anti-reflective functionality. Consequently, optical lens manufacturers and diagnostic equipment producers continue to expand glass-based coating adoption across product portfolios.

Metal substrates serve structural and aerospace applications where surface durability and corrosion resistance are critical. Hydrophilic coatings on metal surfaces improve wettability and reduce friction in high-stress mechanical environments. Additionally, medical implant producers use metal substrates to achieve biocompatible surface performance.

By Technology Analysis

Dip Coating dominates with 46.8% due to its cost efficiency and uniform coating coverage across complex shapes.

In 2025, Dip Coating held a dominant market position in the By Technology segment of the Hydrophilic Coating Market, with a 46.8% share. This method delivers uniform surface coverage across irregular geometries at relatively low operational cost. Moreover, medical device OEMs favor dip coating for catheters and tubings where consistent lubricity is critical.

Spray Coating offers flexibility for large-surface and non-immersible substrate applications. Manufacturers apply spray techniques across aerospace panels, industrial filters, and optical components. Additionally, spray coating enables fast throughput in production environments where dip immersion is impractical or surface coverage speed is prioritized.

Roll Coating serves high-volume flat substrate applications such as film, foil, and sheet materials. This continuous process supports efficient coating of membranes and filtration products. Consequently, industrial filtration and packaging manufacturers increasingly rely on roll coating for scalable, repeatable surface treatment workflows.

By Functionality Analysis

Water Repellent leads with 36.3% due to strong demand across aerospace, automotive, and outdoor industrial markets.

In 2025, Water Repellent held a dominant market position in the By Functionality segment of the Hydrophilic Coating Market, with a 36.3% share. Water repellent coatings prevent moisture accumulation on surfaces exposed to harsh outdoor and operational environments. Moreover, aerospace and automotive OEMs apply these coatings extensively to improve performance and longevity.

Anti-Fogging coatings serve optical, safety, and consumer healthcare applications where surface clarity is essential. Eyewear, face shields, and camera lens manufacturers adopt anti-fog solutions to maintain visual performance. Additionally, cold-chain logistics and food storage operators use anti-fog coatings on packaging to ensure product visibility.

Anti-Reflective coatings address demand from solar energy, display, and precision optical markets. These coatings maximize light transmission and minimize glare across glass and polymer surfaces. Consequently, solar panel manufacturers and display producers invest heavily in anti-reflective surface technologies to enhance system efficiency.

By Application Analysis

Aerospace dominates with 45.9% due to high demand for anti-icing, anti-fog, and friction-reducing surface solutions.

In 2025, Aerospace held a dominant market position in the By Application segment of the Hydrophilic Coating Market, with a 45.9% share. Aircraft manufacturers apply hydrophilic coatings to airfoil surfaces, sensor housings, and optical systems to improve aerodynamic performance. Moreover, anti-icing and anti-fog surface requirements on flight systems drive sustained coating adoption.

Automotive applications benefit from hydrophilic coatings on windshields, sensors, and lighting systems. Electric vehicle manufacturers increasingly specify water-repellent and self-cleaning coatings to reduce maintenance and improve sensor reliability. Additionally, advanced driver-assistance systems require optically clear surfaces that hydrophilic coatings effectively protect.

Marine applications demand coatings that resist biofouling, corrosion, and moisture penetration on hull and equipment surfaces. Hydrophilic coatings reduce drag and improve fuel efficiency for commercial and defense vessels. Consequently, marine OEMs and coating formulators collaborate to develop durable solutions suited to extreme oceanic environments.

Key Market Segments

By Substrate

- Polymers

- Glass

- Metal

- Nanoparticles

- Others

By Technology

- Dip Coating

- Spray Coating

- Roll Coating

- Electrostatic Coating

- Screen Printing

By Functionality

- Water Repellent

- Anti-Fogging

- Anti-Reflective

- Self-Cleaning

- Biocompatibility

By Application

- Aerospace

- Automotive

- Marine

- Medical Devices and Equipment

- Optical

- Others

Emerging Trends

UV-Curable Platforms and Dual-Function Hybrid Coatings Reshape Production

Coating manufacturers actively shift toward UV-curable and rapid inline cure systems that support high-throughput automated production. These platforms reduce cycle time and improve coating consistency at scale. Moreover, dual-function hydrophilic coatings combined with antimicrobial or antithrombotic properties emerge as a high-value innovation category for advanced medical device OEMs.

AI-Enabled Inspection and Sustainable Formulations Drive Industry Transformation

AI-enabled vision inspection systems now detect coating uniformity, thickness variation, and surface defects at production scale with high accuracy. Additionally, global OEM supply chains accelerate the adoption of low-VOC, NMP-free, and REACH-aligned coating formulations. These sustainable chemistry trends align with regulatory pressure and corporate environmental goals across North America, Europe, and the Asia Pacific.

Drivers

Rising Minimally Invasive Procedure Volumes Expand Medical Coating Demand

Global volumes of minimally invasive cardiovascular, neurovascular, and urology procedures grow steadily, creating consistent demand for ultra-low-friction catheter coatings. OEMs require coatings that maintain lubricity through complex navigation pathways. Lubricent UV hydrophilic coating reduces device friction forces by as much as 98% compared to uncoated surfaces, demonstrating the critical performance value these coatings deliver.

Contract Coating Outsourcing and Wearable Biosensor Expansion Fuel Market Growth

MedTech OEMs increasingly outsource coating validation and scale-up to specialized contract coating providers. This trend accelerates product development timelines and reduces regulatory burden. Moreover, hydrophilic surface chemistries expand rapidly into next-generation wearable biosensors, microfluidic diagnostic platforms, and consumable laboratory devices, broadening the addressable market well beyond traditional catheter applications.

Restraints

PFAS and Solvent Regulations Create Significant Reformulation Burden

Regulatory and environmental pressure on PFAS-linked and solvent-heavy coating chemistries intensifies across North America and Europe. Coating manufacturers must reformulate established product lines to meet evolving restrictions, increasing development costs, and validation timelines. According to ISO 10993-1:2025 and EU MDR 2017/745, repeated reprocessing cycles must not cause coating deterioration, driving extensive durability testing requirements for manufacturers.

Coating Delamination and Shelf-Life Instability Limit High-Stress Application Adoption

Performance failure risks from coating delamination, shelf-life instability, and repeated hydration-dehydration cycles challenge adoption in high-stress applications. These failure modes raise quality and safety concerns among device manufacturers and clinical procurement teams. Consequently, OEMs demand rigorous qualification data before approving new hydrophilic coating suppliers or introducing reformulated chemistries into regulated device production.

Growth Factors

PFAS-Free and Advanced Catheter Coatings Open High-Value Commercial Opportunities

Commercial expansion of PFAS-free lumen and inner-diameter hydrophilic coatings addresses growing regulatory and market demand for safer catheter surface solutions. Structural heart, electrophysiology, and robotic endovascular delivery systems represent high-potential penetration targets. Lubricant-impregnated hydrophilic catheter designs cut urethral insertion friction by more than a factor of two, confirming the clinical performance value driving this expansion.

Asia-Based Manufacturing Growth and Cross-Industry Adoption Accelerate Market Expansion

Rapid localization opportunities emerge across Asia-based medical device manufacturing hubs and regional contract coating partnerships. Additionally, cross-industry adoption in industrial filtration membranes, optical anti-fog surfaces, and consumer healthcare devices broadens revenue diversification for coating suppliers. Therefore, manufacturers that establish regional production and partnership networks in Asia capture significant volume growth during the forecast period.

Regional Analysis

North America Dominates the Hydrophilic Coating Market with a Market Share of 37.5%, Valued at USD 6.8 Billion

North America leads the global hydrophilic coating market, holding a 37.5% share valued at USD 6.8 billion in 2025. The United States drives this dominance through its large base of MedTech OEMs, aerospace manufacturers, and advanced contract coating service providers. Moreover, strong regulatory frameworks and high R&D investment sustain innovation and procurement activity across the region.

Europe maintains a significant market position driven by stringent EU MDR 2017/745 compliance requirements and a mature medical device manufacturing ecosystem. Germany, France, and the UK anchor regional demand through established aerospace and medical technology industries. Additionally, European sustainability mandates accelerate the adoption of REACH-aligned, low-VOC coating formulations across OEM supply chains.

Asia Pacific represents the fastest-growing regional market as medical device manufacturing capacity expands rapidly in China, Japan, South Korea, and India. Regional governments support the localization of advanced coating capabilities through industrial policy and investment incentives. Consequently, global coating suppliers establish local partnerships and production facilities to capture growing contract coating outsourcing volumes.

Latin America shows steady growth driven by Brazil and Mexico as the region’s primary medical device and industrial coating markets. Increasing adoption of minimally invasive surgical procedures expands catheter coating demand across major urban healthcare centers. Additionally, growing automotive and industrial manufacturing activity in the region creates supplementary demand for functional surface coating technologies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Surmodics Inc. operates as a leading innovator in hydrophilic surface modification technologies for medical devices. The company focuses on proprietary coating platforms that enhance lubricity, biocompatibility, and device performance for catheter and guidewire applications. Moreover, Surmodics invests actively in expanding its contract coating services to support MedTech OEM customers through regulatory validation and scale-up phases.

Hydromer Inc. specializes in wettability and moisture distribution coatings validated for ISO 10993 biocompatibility compliance. The company develops hydrophilic formulations that support catheter, stent, and implant applications across interventional cardiology and urology markets. Additionally, Hydromer pursues formulation innovation to address evolving regulatory demands and next-generation device platform requirements globally.

Biocoat Inc. delivers hydrophilic coating solutions with a strong focus on medical device lubricity and biocompatibility performance. The company provides both product and contract coating services to OEM customers across the catheter, endoscope, and minimally invasive device segments. Consequently, Biocoat positions itself as a comprehensive surface modification partner supporting device development from prototype through commercial-scale production.

AST Products Inc. provides specialized surface treatment and coating solutions across medical device, industrial, and optical application markets. The company’s expertise spans adhesion promotion, hydrophilic functionalization, and surface characterization services. Therefore, AST Products serves a diverse OEM client base seeking reliable surface modification support for regulated product development and manufacturing compliance.

Top Key Players in the Market

- Surmodics Inc.

- Hydromer Inc.

- Biocoat Inc.

- AST Products Inc.

- Aculon Inc.

- Surface Solutions Group LLC

- Tokyo Ohka Kogyo Co., Ltd.

- BioInteractions Ltd.

- Covalon Technologies Ltd.

Recent Developments

- In 2025, Biocoat’s clearest recent technical development is its Non-PFAS Lumen Coating Method and Apparatus. On its own site, Biocoat said it secured a patent for this thermal-cured hydrophilic coating technology designed for the inner diameters (lumens) of devices such as catheters. The company frames it as a response to mounting scrutiny of PFAS in medical-device manufacturing.

- In 2025, for AST Products, I found much less recent disclosure than for the other three companies. The company is still active in this area through HydroLAST hydrophilic surface treatment, which it says improves wettability and wicking of polymeric biomaterials, and through contract coating work supported by Device Master Files.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 18.1 Billion |

| Forecast Revenue (2035) | USD 34.0 Billion |

| CAGR (2026-2035) | 6.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Substrate (Polymers, Glass, Metal, Nanoparticles, Others), By Technology (Dip Coating, Spray Coating, Roll Coating, Electrostatic Coating, Screen Printing), By Functionality (Water Repellent, Anti-Fogging, Anti-Reflective, Self-Cleaning, Biocompatibility), By Application (Aerospace, Automotive, Marine, Medical Devices and Equipment, Optical, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Surmodics Inc., Hydromer Inc., Biocoat Inc., AST Products Inc., Aculon Inc., Surface Solutions Group LLC, Tokyo Ohka Kogyo Co., Ltd., BioInteractions Ltd., Covalon Technologies Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |