Quick Navigation

Report Overview

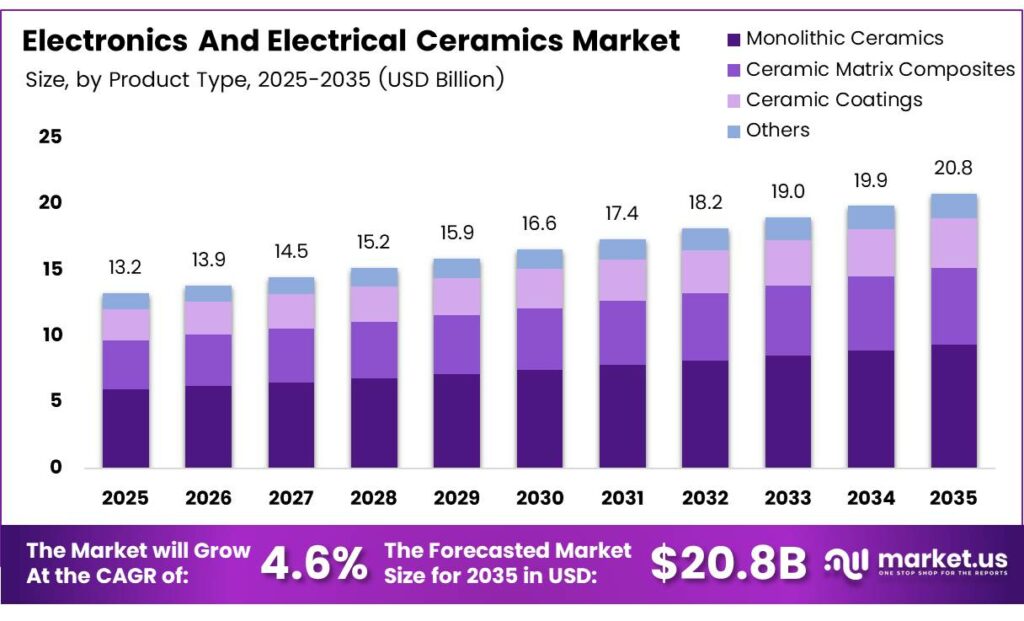

The Global Electronics and Electrical Ceramics Market size is expected to be worth around USD 20.8 billion by 2035 from USD 13.2 billion in 2025, growing at a CAGR of 4.6% during the forecast period 2026 to 2035.

Electronics and electrical ceramics are advanced inorganic materials engineered for critical functions in modern electronic systems. These materials deliver essential properties such as high dielectric strength, thermal stability, and electrical insulation. Manufacturers use them across a wide range of applications, from consumer devices to power infrastructure.

Each AI server is now equipped with approximately 15,000 to 25,000 multilayer ceramic capacitors, and this count continues to rise as AI server performance requirements grow. This signals a structural shift in demand patterns that favors high-volume, high-precision ceramic production facilities.

Murata Manufacturing reported that MLCC capacity utilization reached 90 to 95% in Q4 2025, with similar utilization levels expected to continue into Q1 2026. This near-full capacity operation reflects the intense and sustained demand surge for advanced ceramic components driven by AI and digital infrastructure growth.

Global demand for high-performance ceramics accelerates as electronics become smaller and more powerful. The expansion of 5G networks, electric vehicles, and AI server infrastructure creates strong upstream demand. Moreover, regulatory pressure on energy efficiency and material sustainability shapes product development strategies worldwide.

Key Takeaways

- The Global Electronics and Electrical Ceramics Market is valued at USD 13.2 billion in 2025 and is projected to reach USD 20.8 billion by 2035, at a CAGR of 4.6%.

- Alumina Ceramics holds the leading position with a 48.6% market share.

- Monolithic Ceramics dominates with a 56.8% share.

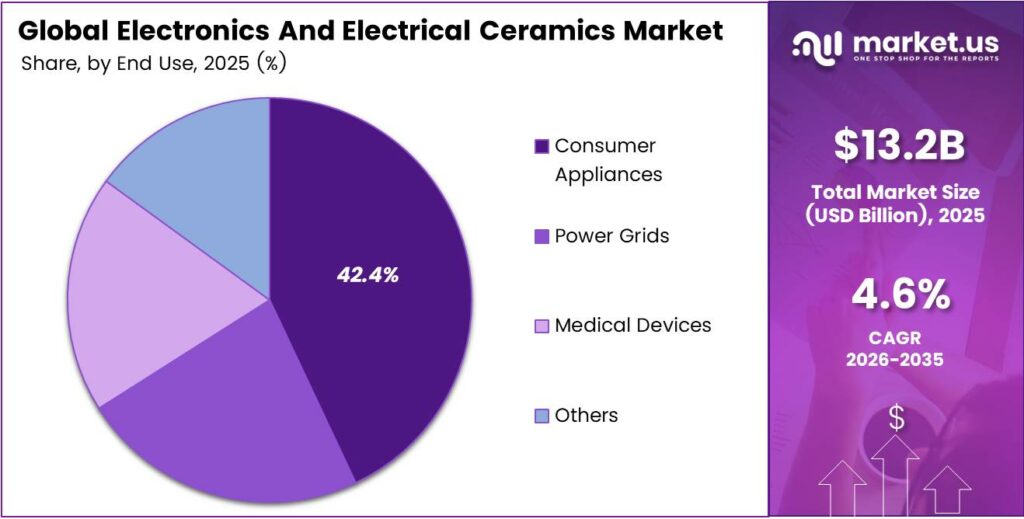

- Consumer Appliances leads with a 42.4% share.

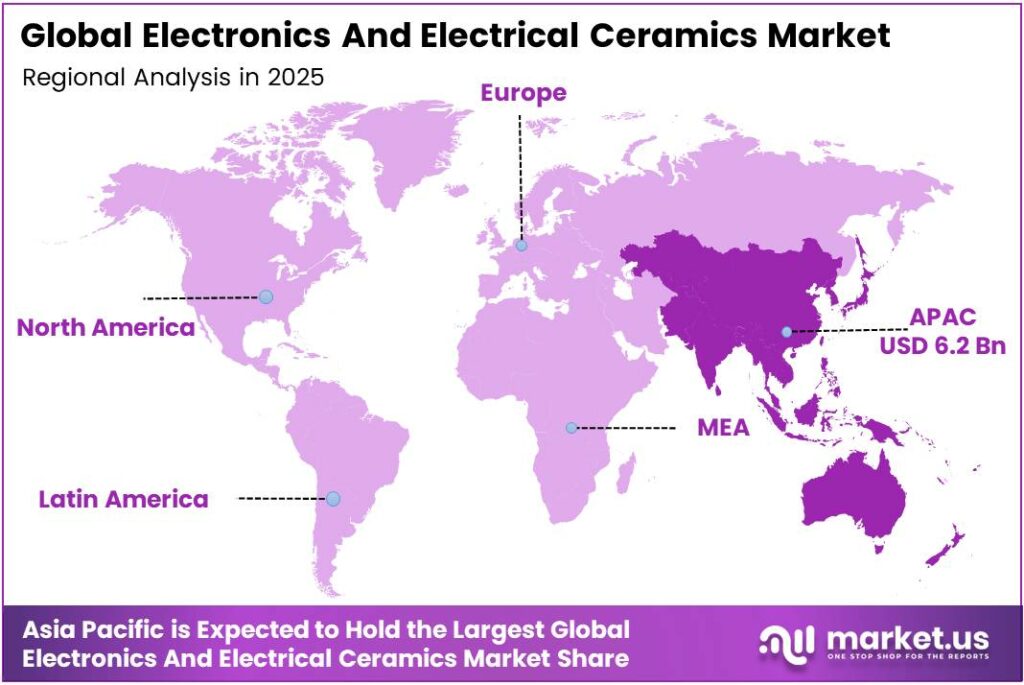

- Asia-Pacific dominates the market with a 47.3% share, valued at approximately USD 6.2 billion.

Material Type Analysis

Alumina Ceramics dominates with 48.6% due to its superior electrical insulation, mechanical strength, and cost-effectiveness across electronics applications.

In 2025, Alumina Ceramics held a dominant market position in the By Material Type segment of the Electronics and Electrical Ceramics Market, with a 48.6% share. Alumina offers outstanding dielectric performance and thermal resistance at a competitive cost. Consequently, electronics manufacturers across consumer and industrial segments rely on this material as a primary substrate and insulation choice.

Titanate Ceramics represent a significant and growing sub-segment within the material type category. These ceramics deliver high dielectric constants essential for capacitor applications. Moreover, their piezoelectric properties make them critical components in sensors, actuators, and ultrasonic devices used across medical, industrial, and consumer electronics platforms.

Zirconia Ceramics serve specialized applications where extreme hardness and fracture toughness are required. Their biocompatibility supports adoption in medical implants and dental devices. Additionally, zirconia-based components find increasing use in fuel cell systems and high-temperature electronic environments where other ceramic materials reach performance limits.

Product Type Analysis

Monolithic Ceramics dominates with 56.8% due to its established manufacturing base, versatility, and broad end-use adoption across electronics industries.

In 2025, Monolithic Ceramics held a dominant market position in the By Product Type segment of the Electronics and Electrical Ceramics Market, with a 56.8% share. These single-phase ceramic components deliver reliable electrical and mechanical performance at scale. Their established supply chains and proven manufacturing processes support consistent adoption across consumer electronics, power systems, and communications infrastructure.

Ceramic Matrix Composites represent the fastest-growing product segment within this category. These advanced materials combine ceramic matrices with reinforcing fibers to achieve superior strength-to-weight ratios. Consequently, aerospace electronics, high-performance computing systems, and advanced power modules increasingly adopt ceramic matrix composites where conventional monolithic ceramics fall short under extreme operating conditions.

Ceramic Coatings address surface engineering requirements across electronics and electrical equipment. These thin-film ceramic layers protect metal substrates from heat, corrosion, and electrical breakdown. Additionally, the coatings market benefits from growing demand in EV battery systems and power semiconductor packaging, where thermal management performance directly influences device longevity.

End-user Industry Analysis

Consumer Appliances dominates with 42.4% due to high-volume production requirements and widespread ceramic component integration in everyday electronic devices.

In 2025, Consumer Appliances held a dominant market position in the By End-user Industry segment of the Electronics and Electrical Ceramics Market, with a 42.4% share. Smartphones, home appliances, televisions, and wearable devices consume large volumes of ceramic capacitors, insulators, and substrates. Therefore, consumer electronics manufacturers remain the single largest driver of ceramics demand by volume globally.

Power Grids represent a strategically important end-use segment driven by global energy transition investments. High-voltage ceramic insulators and dielectric components support grid modernization and renewable energy integration. Moreover, smart grid expansion programs across North America, Europe, and the Asia Pacific drive sustained long-term procurement of advanced electrical ceramics for infrastructure upgrades.

Medical Devices constitute a high-value, high-growth end-user segment within the ceramics market. Biocompatible zirconia and alumina ceramics serve in implants, diagnostic equipment, and imaging systems. Additionally, the global aging population and increased healthcare spending support consistent demand growth for precision ceramic components with strict regulatory compliance and long-term performance stability.

Key Market Segments

By Material Type

- Alumina Ceramics

- Titanate Ceramics

- Zirconia Ceramics

- Silica Ceramics

- Others

By Product Type

- Monolithic Ceramics

- Ceramic Matrix Composites

- Ceramic Coatings

- Others

By End-user Industry

- Consumer Appliances

- Power Grids

- Medical Devices

- Others

Emerging Trends

Miniaturization and High-Density Multilayer Ceramic Packaging Solutions

Miniaturization technologies drive demand for high-density multilayer ceramic packaging across 5G, AI, and wearable device platforms. Manufacturers invest heavily in thinner dielectric layers and finer pitch designs. Moreover, achieved quality factor frequency products of up to 64,200 GHz in optimized ceramic compositions, meeting next-generation filter performance requirements for mmWave 5G applications.

Lead-Free Ceramics and AI-Powered Manufacturing Processes

Regulatory pressure drives the ceramics industry toward lead-free piezoelectric formulations that comply with RoHS and sustainability mandates. Additionally, manufacturers integrate AI-powered design tools and IoT-enabled monitoring systems to optimize ceramic production. These process innovations reduce defect rates, improve yield consistency, and support energy-efficient operations across high-volume electronics ceramics manufacturing facilities.

Drivers

5G Infrastructure and EV Growth Accelerate Advanced Ceramic Component Demand

Global 5G infrastructure rollout drives strong demand for LTCC substrates and high-frequency ceramic filters across base station and handset platforms. Simultaneously, the proliferation of electric vehicles increases thermal-ceramic requirements in traction inverters and battery management systems. Murata’s computer-related business revenue increased by 26.5% in Q3 fiscal year 2025, reflecting AI-server-driven MLCC demand growth.

Consumer Electronics Growth and INNOVATIVE Project Advance Ceramics Adoption

Surging consumer electronics production accelerates MLCC adoption across smartphones, wearables, and smart home devices. The INNOVATILE EU project, active in 2025, targets energy demand reductions of 30 to 35% and greenhouse gas emission cuts of 30 to 35% in porcelain tile manufacturing. These innovations demonstrate that sustainability-focused production improvements support both regulatory compliance and cost-efficiency for ceramics producers globally.

Restraints

Raw Material Cost Volatility Disrupts Electronics Ceramics Supply Chains

Escalating costs and supply volatility for critical raw materials, including high-purity alumina, create significant margin pressure for ceramics producers. Global supply chain disruptions amplify procurement risks for manufacturers dependent on concentrated material sources. Moreover, RAK Ceramics’ 2025 ESG Report confirmed a 10.06% reduction in overall energy consumption for tableware production, highlighting that operational efficiency programs are essential tools for managing rising input costs across ceramic manufacturing facilities.

High Processing Temperatures Limit Production Scalability

High sintering temperatures and complex multi-step processing requirements limit the ability of manufacturers to rapidly scale ceramic production capacity. These technical barriers increase capital expenditure and restrict participation to well-funded producers. Consequently, smaller manufacturers struggle to compete with vertically integrated players who can absorb processing costs through economies of scale and proprietary kiln technology investments.

Growth Factors

Ceramic Electrolytes and Additive Manufacturing Open New High-Value Markets

Development of ceramic electrolytes enables next-generation solid-state batteries for wearable electronics and EV applications. MLCC demand for AI server projects is projected to grow at an average annual rate of approximately 30% through fiscal 2030, with demand forecast to be 3.3 times higher in FY2030 than in FY2025. Furthermore, advances in additive manufacturing support the production of custom high-precision ceramic parts for miniaturized and mission-critical electronic devices.

Supply Chain Localization and Sustainability Innovations Drive Long-Term Expansion

Localization of advanced substrate supply chains for EV and semiconductor manufacturing gains momentum across North America, Europe, and Asia. Wienerberger achieved a 20.7% reduction in Scope 1 and 2 CO₂ emissions by the end of 2025 against a 2020 baseline. Additionally, a low-energy dry granulation process replacing spray drying reduces energy consumption by 45%, demonstrating that sustainability-driven process innovation lowers production costs and strengthens the competitive position of advanced ceramics manufacturers.

Regional Analysis

Asia-Pacific Dominates the Electronics and Electrical Ceramics Market with a Market Share of 47.3%, Valued at USD 6.2 Billion

Asia-Pacific commands the global electronics and electrical ceramics market with a 47.3% share, valued at USD 6.2 billion in 2025. The region benefits from concentrated consumer electronics manufacturing, large-scale EV production, and dominant MLCC supply chains centered in Japan, China, South Korea, and Taiwan. Moreover, aggressive national semiconductor and EV investment programs sustain strong long-term demand for high-performance ceramic substrates and components.

North America represents a significant and strategically important market for advanced electronics ceramics. The United States drives demand through defense electronics, medical devices, semiconductor fabrication, and 5G infrastructure deployment. Additionally, federal investment in domestic semiconductor supply chain resilience supports increased procurement of locally sourced ceramic substrate and insulation materials across government-backed programs.

Europe demonstrates steady growth in electrical ceramics driven by automotive electrification, industrial automation, and renewable energy investments. Germany, France, and Italy lead ceramics consumption within the region. Furthermore, the EU’s sustainability regulations and RoHS compliance requirements actively shape material innovation, pushing manufacturers toward lead-free and energy-efficient ceramic formulations across the power and electronics sectors.

The Middle East and Africa region shows emerging demand for electrical ceramics, particularly in power infrastructure and telecommunications expansion projects. GCC countries invest actively in smart grid modernization and 5G network rollouts, creating upstream demand for ceramic insulators and high-frequency substrates. Consequently, international ceramics suppliers target this region as a growth opportunity complementary to their established markets in Asia and the West.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

3M operates as a diversified materials technology leader with a strong ceramics portfolio spanning electronic substrates, abrasives, and insulation systems. The company leverages its deep materials science expertise to develop ceramic solutions for high-voltage electrical systems and precision electronics. Its global manufacturing footprint and strong R&D investment position it as a reliable supplier to diversified industrial and electronics end markets worldwide.

AdValue Technology specializes in high-purity advanced ceramic components engineered for demanding applications in electronics, medical, and analytical instrument sectors. The company focuses on custom ceramic fabrication using alumina, zirconia, and other specialty oxides. Its customer-centric approach and precision manufacturing capabilities allow it to serve niche but high-value electronics applications where standard off-the-shelf ceramic components cannot meet stringent performance specifications.

CeramTec GmbH holds a prominent position in the global advanced ceramics industry, with a comprehensive product portfolio covering structural, functional, and electronic ceramics. The company serves markets including automotive, medical, and electrical engineering with engineered ceramic components manufactured to tight tolerances. Its innovation focuses on high-performance alumina and zirconia materials, supporting the growing demand from semiconductor packaging and power electronics customers globally.

CoorsTek Inc. ranks among the world’s largest technical ceramics manufacturers, producing engineered ceramic components for semiconductor processing, energy systems, and electronics manufacturing equipment. The company operates a broad global production network that supports a consistent, high-volume supply of precision ceramic parts. Its expertise in alumina, silicon carbide, and other advanced ceramics supports critical upstream processes in semiconductor fabrication and electronic component production.

Top Key Players in the Market

- 3M

- AdValue Technology

- CeramTec GmbH

- CoorsTek Inc.

- Heraeus Group

- IBIDEN

- KCM Corporation

- Kyocera Corporation

- MARUWA Co., Ltd.

- Murata Manufacturing Co., Ltd.

- Saint-Gobain Ceramics

- Sumitomo Chemical Co., Ltd.

- TDK Corporation

Recent Developments

- In 2025, 3M maintains an active Technical Ceramics portfolio focused on advanced ceramic materials and components for demanding electronics and electrical applications, including communications infrastructure (e.g., boron nitride cooling fillers) and transportation/electronics segments.

- In 2025, Post on alumina for extreme durability, heat resistance, and electrical insulation in hostile environments. Post on thick film pastes for AlN substrates and their role in high-volume electronic functionality. Post titled How Advanced Ceramics Are Powering the Next Generation of Electronics (higher speeds/power density in compact devices).

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 13.2 Billion |

| Forecast Revenue (2035) | USD 20.8 Billion |

| CAGR (2026-2035) | 4.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Alumina Ceramics, Titanate Ceramics, Zirconia Ceramics, Silica Ceramics, Others), By Product Type (Monolithic Ceramics, Ceramic Matrix Composites, Ceramic Coatings, Others), By End-user Industry (Consumer Appliances, Power Grids, Medical Devices, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | 3M, AdValue Technology, CeramTec GmbH, CoorsTek Inc., Heraeus Group, IBIDEN, KCM Corporation, Kyocera Corporation, MARUWA Co., Ltd., Murata Manufacturing Co., Ltd., Saint-Gobain Ceramics, Sumitomo Chemical Co., Ltd., TDK Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |