Quick Navigation

Report Overview

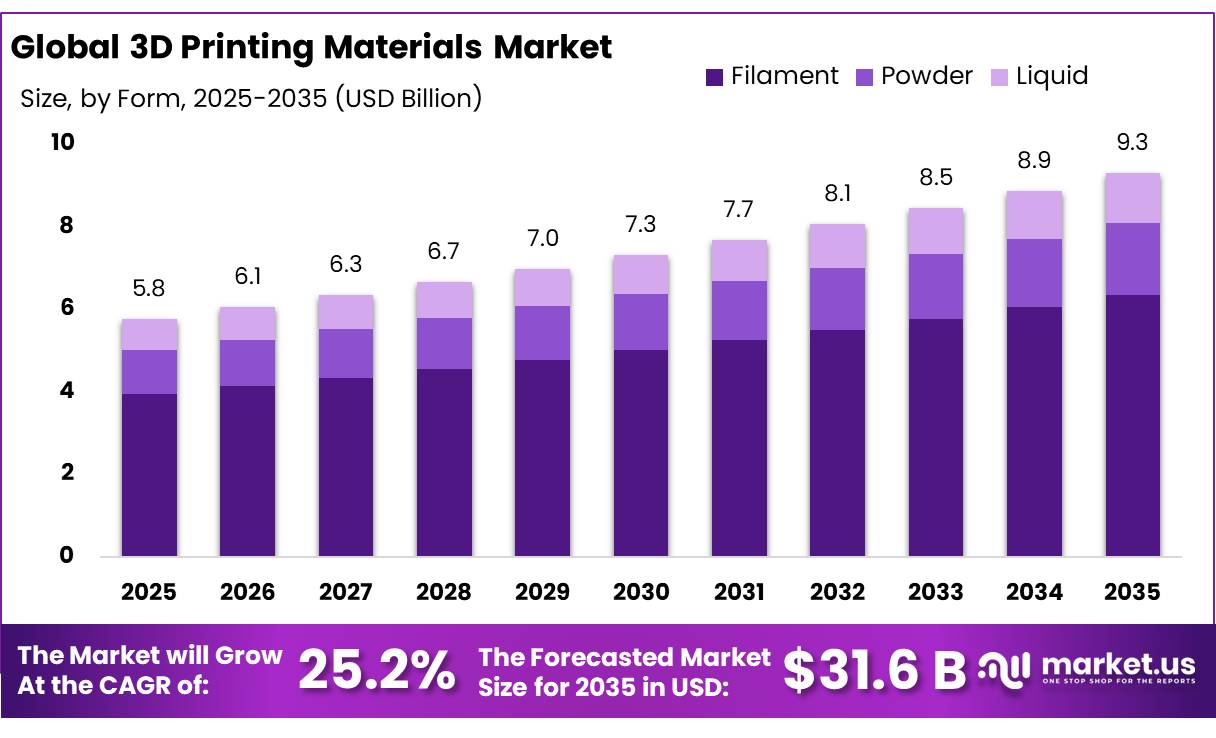

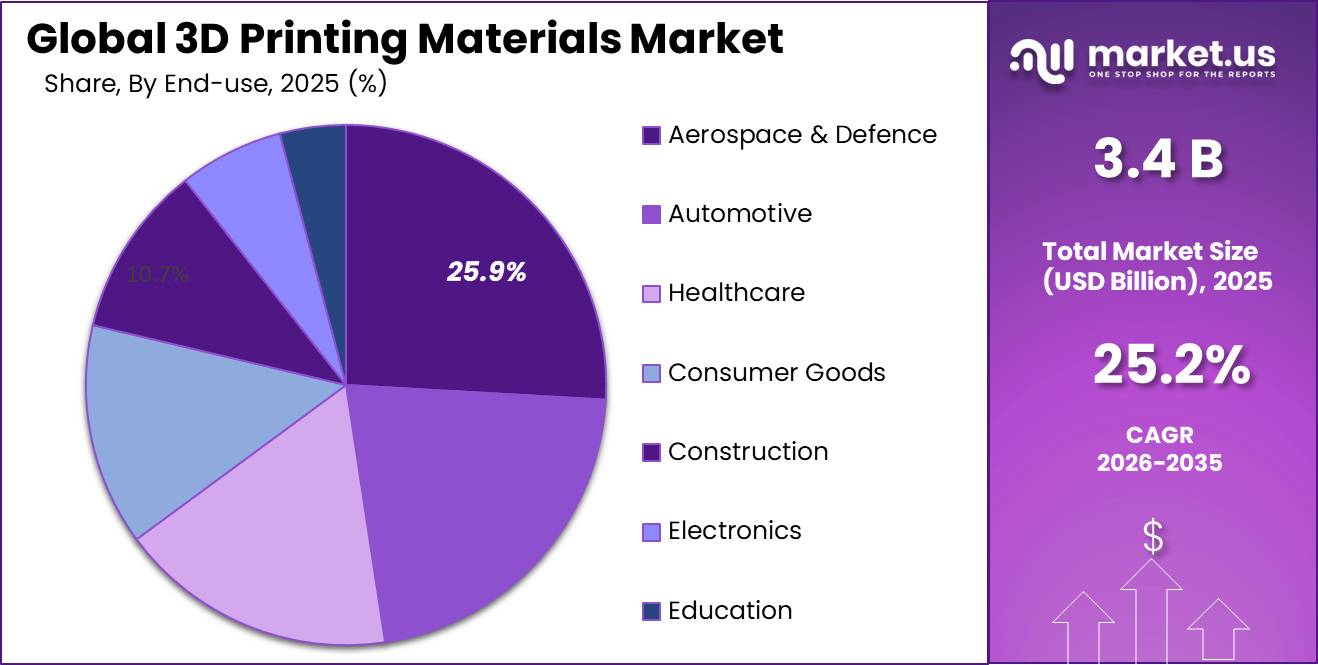

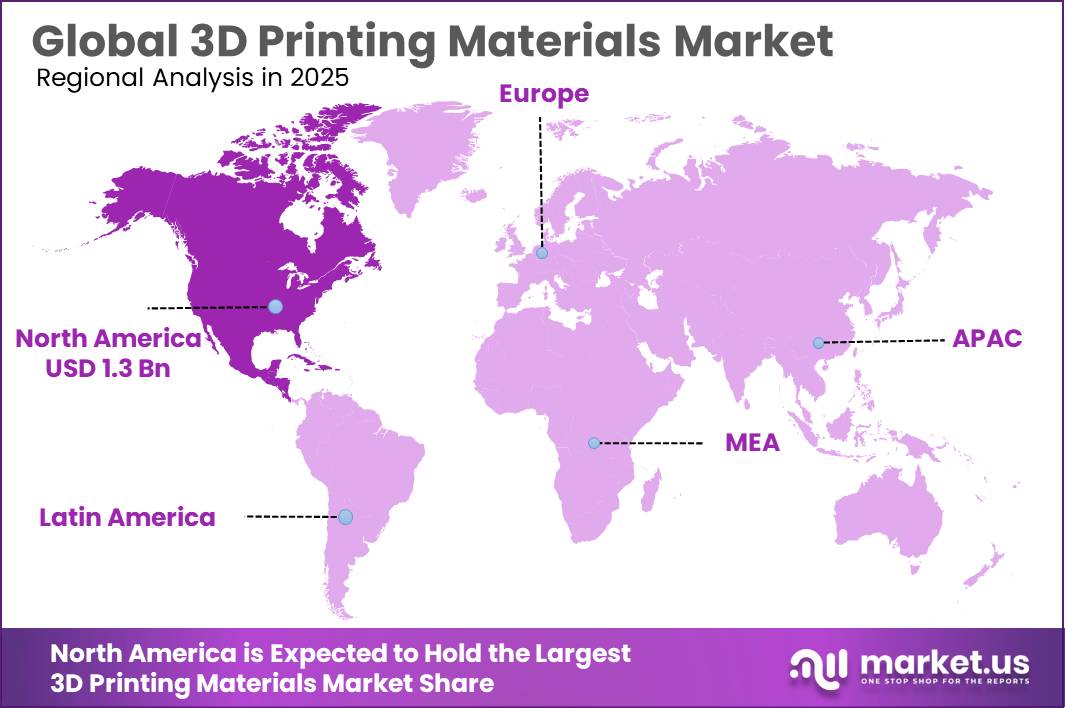

The Global 3D Printing Materials Market size is expected to be worth around USD 31.6 Billion by 2035, from USD 3.4 Billion in 2025, growing at a CAGR of 25.2% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 40.30% share, holding USD 1.3 Billion revenue.

3D printing materials are moving from prototyping use toward certified industrial production, where polymers, photopolymers, metals, ceramics and composite-filled materials are selected for strength, heat resistance, biocompatibility, light weight and design freedom. The sector is supported by additive manufacturing’s ability to reduce energy use by 25% and cut waste and material costs by up to 90% compared with traditional manufacturing, according to the U.S. Department of Energy.

The public-sector investment in advanced manufacturing. In the U.S., Manufacturing USA expanded from 14 institutes to 17 institutes by December 2024, with Commerce, Defense, and Energy sponsoring R&D and workforce programs that include 3D-printed aircraft parts and advanced materials. NIST’s AM-Bench 2025 received 85 challenge submissions, reflecting active work on validated AM process data, materials modelling, and production reliability.

Key driving factors include supply-chain localization, design freedom, light-weighting, material efficiency, and higher use of certified materials in regulated industries. Demand is especially strong where AM can produce complex internal channels, patient-specific medical parts, high-temperature metal structures, and low-volume industrial components. 3D Systems’ Q4 2025 revenue rose 16% sequentially, helped by stronger printer and materials sales, indicating that installed printer growth is expected to pull recurring material consumption.

Government support is also strengthening the sector. The U.S. Department of Energy notes that additive manufacturing can reduce energy use by 25% and cut waste and material costs by up to 90% compared with traditional manufacturing, making it attractive for sustainability-driven industries. The U.S. AM Forward initiative was also designed to help smaller U.S.-based suppliers increase additive manufacturing adoption, improving domestic supply-chain resilience.

In Europe, the European Patent Office reported that global patent filings in 3D printing technologies grew at an average annual rate of 26.3% between 2013 and 2020, nearly eight times faster than all technology fields, showing strong innovation momentum.

BASF’s historical role in AM materials remains important because its former Forward AM business built a broad portfolio across powders, plastic filaments, metal filaments, and photopolymers. However, BASF had already carved out this 3D printing business; Forward AM states it became Forward AM Technologies in 2024 after a management buyout and entered a new chapter in 2025 as Mass Additive Manufacturing GmbH within the Stratasys group.

Key Takeaways

- 3D Printing Materials Market size is expected to be worth around USD 31.6 Billion by 2035, from USD 3.4 Billion in 2025, growing at a CAGR of 25.2%.

- Filament held a dominant market position, capturing more than a 68.30% share in the 3D Printing Materials Market.

- Plastic held a dominant market position, capturing more than a 48.30% share in the 3D Printing Materials Market.

- Aerospace & Defence held a dominant market position, capturing more than a 25.90% share in the 3D Printing Materials Market.

- North America held the dominant position in the global 3D Printing Materials Market, accounting for 40.30% of total market share and reaching a value of USD 1.3 Bn.

By Form Analysis

Filament Leads the 3D Printing Materials Market with 68.30% Share in 2025

In 2025, Filament held a dominant market position, capturing more than a 68.30% share in the 3D Printing Materials Market by form type. The segment maintained its leadership due to its broad compatibility with widely adopted additive manufacturing technologies, especially fused deposition modeling (FDM) and fused filament fabrication (FFF). Filament materials continue to be preferred across industrial production, prototyping, educational applications, automotive component development, and consumer manufacturing because of their ease of processing, lower operational complexity, and cost efficiency compared with other material forms.

By Type Analysis

Plastic dominates with 48.30% share driven by versatility and broad industrial adoption

In 2025, Plastic held a dominant market position, capturing more than a 48.30% share in the 3D Printing Materials Market by type. This leadership was supported by the material’s wide usability across multiple additive manufacturing technologies and its ability to serve both industrial and consumer-level applications. Plastic materials remained the preferred choice for manufacturers due to their balance of performance, affordability, ease of processing, and availability across different printing platforms.

By End-User Analysis

Aerospace & Defence dominates with 25.90% share supported by demand for lightweight and precision-built components

In 2025, Aerospace & Defence held a dominant market position, capturing more than a 25.90% share in the 3D Printing Materials Market by end-user. The segment maintained its leading position due to increasing use of additive manufacturing technologies for producing lightweight, high-performance, and complex components that are difficult to manufacture using conventional methods. Aerospace and defence organizations continued to adopt 3D printing materials to improve design flexibility, shorten production cycles, and reduce overall material waste.

Key Market Segments

By Form

- Powder

- Filament

- Liquid

By Type

- Plastic

- Metal

- Ceramic

By End-User

- Automotive

- Aerospace & Defence

- Healthcare

- Consumer Goods

- Construction

- Electronics

- Education

Market Dynamics

Driver Analysis - Rising Demand For Customized Food Production Solutions

One of the major driving factors supporting growth in the 3D Printing Materials market is the increasing demand for customized and efficient food production technologies. Food manufacturers are exploring additive manufacturing to create products with improved design flexibility, portion control, and personalized nutrition. This shift is creating new opportunities for advanced printable materials that can deliver consistency, food safety, and production efficiency.

The food industry has been moving toward more flexible manufacturing systems as consumer demand becomes more personalized. According to the Food and Agriculture Organization (FAO), global food production will need to increase by nearly 50% by 2050 to meet future consumption requirements. This long-term pressure is encouraging industries to adopt technologies that reduce waste and improve production efficiency, including additive manufacturing and specialized printing materials. As a result, demand for food-compatible 3D printing materials and related innovations continues to gain attention from manufacturers and research institutions.

Government and institutional support is also helping accelerate material development for advanced manufacturing. Across several developed economies, public programs continue funding digital manufacturing and material innovation to improve production sustainability and supply resilience. These initiatives are encouraging manufacturers to invest in next-generation printable polymers and engineered materials that can support precise production while reducing unnecessary material consumption.

At the industry level, material efficiency is becoming a stronger business priority. Recent industrial examples show that additive manufacturing can significantly reduce raw material use compared with traditional production approaches. In advanced manufacturing applications, material-saving approaches have demonstrated reductions of up to 50% in raw material usage, highlighting the broader value of efficient 3D printing materials across production environments.

Restraint Analysis - Limited Food-Grade Certification Restrains 3D Materials Adoption

One of the major restraining factors for the 3D Printing Materials industry is the limited availability of certified food-grade and food-contact-safe materials. While additive manufacturing is expanding into packaging, customized food tools, food processing components, and edible product applications, material approval requirements remain strict. This slows commercialization and increases compliance costs for manufacturers.

Food organizations and regulatory authorities continue to place strong emphasis on food safety. The U.S. Food and Drug Administration (FDA) requires that materials used in food-contact applications meet strict safety and migration standards before they can be commercially used. Food-contact materials must not transfer harmful substances into food during production, storage, or use. This requirement becomes more complex in 3D printing because approval depends not only on the base material but also on the complete printing process, post-processing, cleaning conditions, and final product performance.

Government and regulatory initiatives are also becoming stricter. In the European market, Regulation (EC) No. 1935/2004 requires that food-contact materials should not endanger human health or alter food composition. In the United States, FDA regulations under 21 CFR Sections 174–190 govern indirect food additives and food-contact substances used in manufacturing processes. These frameworks improve consumer protection but extend qualification timelines for new 3D printing materials entering food-related industries.

Opportunity Analysis - Expanding Personalized Food Production Creates Material

One major growth opportunity for the 3D Printing Materials industry is the rising adoption of personalized food production and customized food manufacturing. Food companies, research institutions, and public agencies are increasingly exploring 3D printing technologies to create customized nutrition, reduce food waste, and improve production flexibility. This shift is creating new demand for food-safe polymers, edible printing materials, biodegradable packaging inputs, and advanced additive manufacturing materials.

The food sector is gradually moving toward customization. According to the Food and Agriculture Organization (FAO), nearly 13% of food produced globally is lost after harvesting and before retail, creating pressure to improve efficiency and reduce waste across food systems. 3D printing technologies support precise material usage and allow producers to manufacture food structures layer by layer, helping reduce excess raw material consumption. This creates opportunities for material manufacturers to develop specialized food-contact and edible-grade printing materials.

Healthcare and nutrition trends are also supporting growth. The U.S. National Institutes of Health (NIH) has highlighted increasing interest in personalized nutrition solutions, where foods can be designed for age, dietary requirements, and medical conditions. 3D food printing enables controlled ingredient placement and customized portions, increasing the need for reliable and certified printing materials for food applications.

Emerging Trend Analysis - Food-Grade And Sustainable Materials Shape 3D Printing

One of the latest trends in the 3D Printing Materials industry is the growing shift toward food-grade, bio-based, and sustainable materials. Manufacturers are increasingly developing materials that support food-contact applications while also reducing environmental impact. This trend is becoming important because food manufacturers want faster production methods, lower material waste, and better compliance with food safety rules. At the same time, consumers and regulators are encouraging safer and more sustainable manufacturing systems.

Recent studies on food manufacturing show that 3D food printing technologies are creating opportunities for customized production and ingredient efficiency. Research published in 2025 highlighted that 3D food printing supports innovation across food design and manufacturing processes while opening possibilities for controlled ingredient use and reduced waste.

Government and regulatory initiatives continue to support this movement. Food-contact regulations in the United States and Europe are encouraging manufacturers to adopt validated workflows, cleaner processing methods, and documented material traceability. As a result, food-safe thermoplastics and recyclable material systems are expected to gain wider industrial acceptance in the coming years. Rather than focusing only on printing speed, the industry is increasingly prioritizing material safety, sustainability, and regulatory readiness, making this one of the strongest emerging directions in the global 3D Printing Materials market.

Regional Insights

North America dominated the 3D Printing Materials Market with a 40.30% share, valued at USD 1.3 Bn.

North America held the dominant position in the global 3D Printing Materials Market, accounting for 40.30% of total market share and reaching a value of USD 1.3 Bn. The region maintained leadership due to its strong industrial manufacturing base, early adoption of additive manufacturing technologies, and continuous investment in advanced material development.

Government-backed initiatives also contributed to regional growth. Public investment programs supporting advanced manufacturing, domestic supply chain resilience, and industrial innovation encouraged wider adoption of additive manufacturing technologies. These initiatives created favorable conditions for research into next-generation materials with improved durability, sustainability, and production capability.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2026, Stratasys strengthened its additive manufacturing materials business through new product development and capacity expansion. The company introduced ULTEM™ 1010 filament, PolyJet ToughONE™ White, and additional software upgrades to improve production output and material accuracy. Stratasys also expanded manufacturing infrastructure through a new facility and broader digital production capabilities. Its portfolio continued operating across 5 industrial printing technologies, supporting aerospace, healthcare, automotive, and industrial applications.

In 2026, 3D Systems focused on industrial-scale additive manufacturing materials and production solutions. The company launched the SLA 825 Dual, delivering a 22% larger build volume and up to 25% faster printing speed compared with earlier models. The development targeted aerospace, precision manufacturing, and tooling applications.

In 2026, EOS expanded its industrial materials position through partnership-led manufacturing investment. The company supported U.S. production growth through deployment of advanced systems including the EOS M4 ONYX and the first AMCM M 8K platform featuring an 800 × 800 × 1,200 mm build volume and 8 laser configuration.

Top Key Players Outlook

- Stratasys

- 3D Systems, Inc.

- BASF

- EOS GmbH

- Arkema

- The ExOne Company

- Materialise NV

- Höganäs AB (Sweden)

Recent Developments

Höganäs AB: In 2026, Höganäs remained a key metal powder supplier for additive manufacturing. The company serves around 3,000 customers in 75 countries, has annual production capacity of 500,000 tonnes, operates 15 production plants, and employs around 2,300 people, supporting AM powders for aerospace, medical, automotive, and industrial uses.

Stratasys: In 2026, Stratasys moved deeper into production-grade 3D printing materials through a planned USD 42.5 million all-cash acquisition of MarkForged, adding high-performance polymer, composite, and metal filament capability. Markforged generated about USD 70 million revenue in 2025, and the deal is expected to close in the second half of 2026.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.4 Bn |

| Forecast Revenue (2035) | USD 31.6 Bn |

| CAGR (2026-2035) | 25.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Powder, Filament, Liquid), By Type (Plastic, Metal, Ceramic), By End-User (Automotive, Aerospace And Defence, Healthcare, Consumer Goods, Construction, Electronics, Education) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Stratasys, 3D Systems, Inc., BASF, EOS GmbH, Arkema, The ExOne Company, Materialise NV, Höganäs AB (Sweden) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |