Quick Navigation

Report Overview

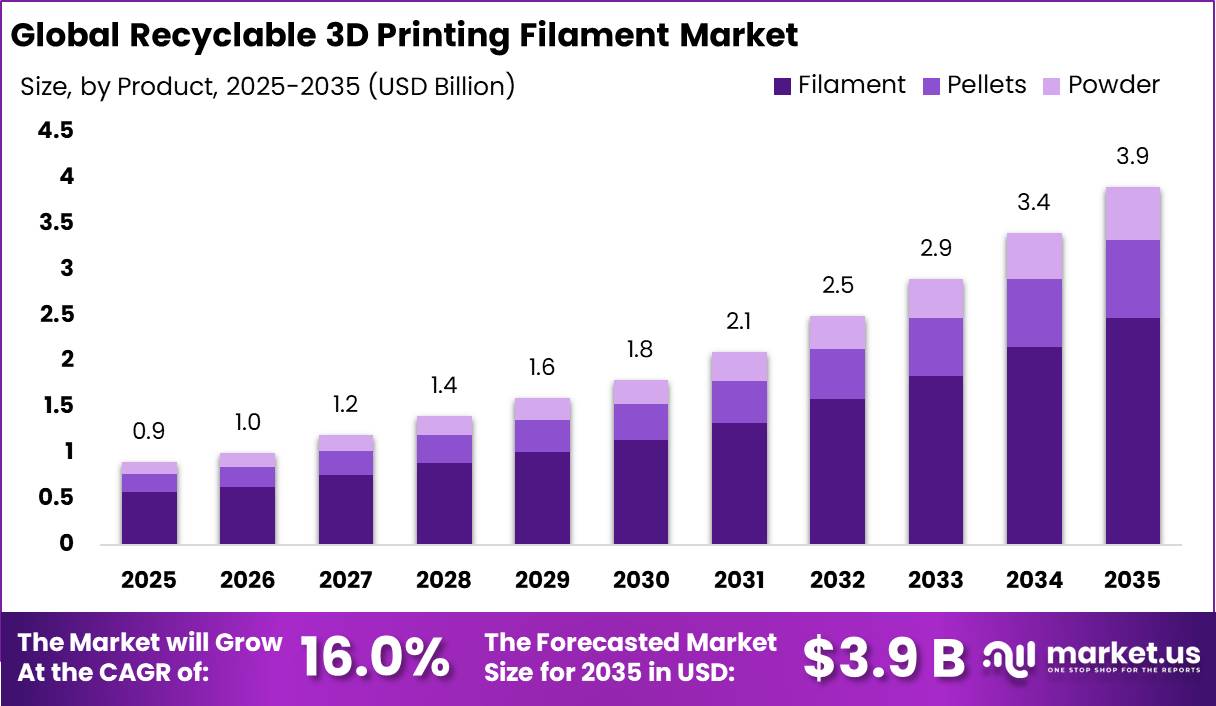

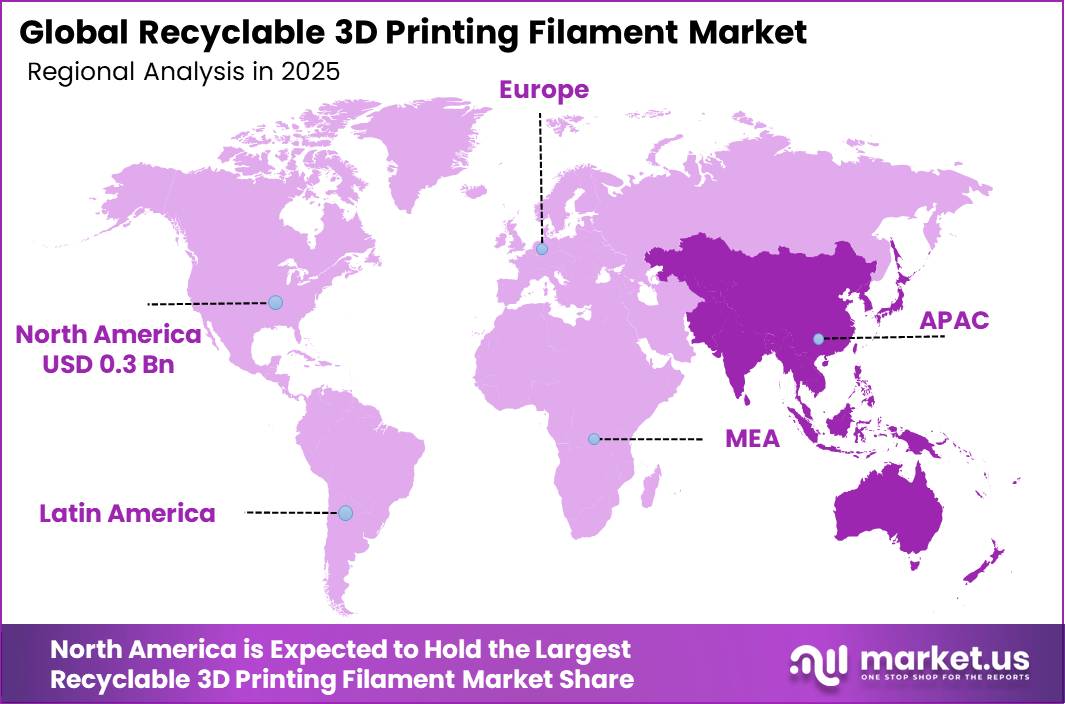

The Global Recyclable 3D Printing Filament Market size is expected to be worth around USD 3.9 Billion by 2035, from USD 0.9 Billion in 2025, growing at a CAGR of 16.0% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 37.4% share, holding USD 0.3 Billion revenue.

Recyclable 3D printing filament is moving from niche prototyping material toward a circular-manufacturing input, as polymer users seek lower-waste feedstock for FFF/FDM printing. The industrial case is supported by the wider plastics gap: OECD reported global plastics production of 460 million tonnes in 2019, plastic waste of 353 million tonnes, and only 9% ultimately recycled.

Key Takeaways

- Recyclable 3D Printing Filament Market size is expected to be worth around USD 3.9 Billion by 2035, from USD 0.9 Billion in 2025, growing at a CAGR of 16.0%.

- Filament held a dominant market position, capturing more than a 63.4% share in the recyclable 3D printing filament market.

- Post-consumer Plastic Waste held a dominant market position, capturing more than a 43.9% share in the recyclable 3D printing filament market.

- Recycled PLA held a dominant market position, capturing more than a 35.3% share in the recyclable 3D printing filament market.

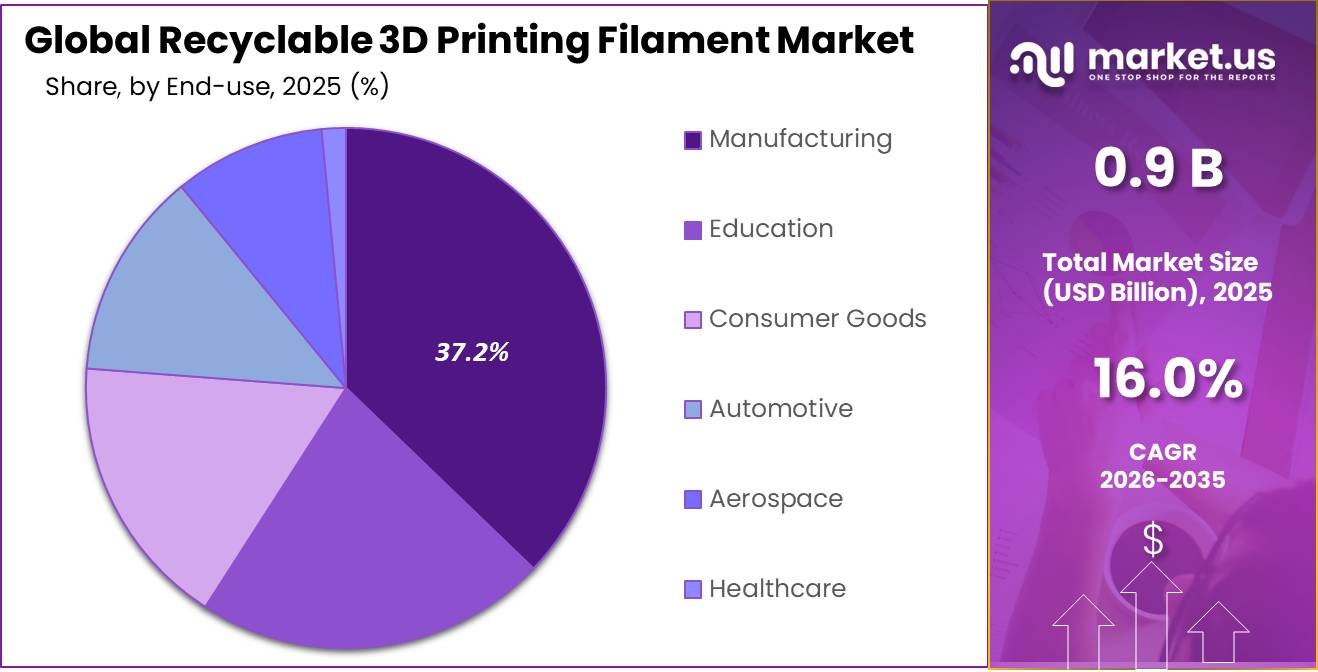

- Manufacturing held a dominant market position, capturing more than a 37.2% share in the recyclable 3D printing filament market.

- North America held a dominant position in the recyclable 3D printing filament market, accounting for 37.4% of the global market share and reaching a market value of nearly USD 0.3 Billion.

The industrial scenario is shaped by manufacturers seeking lower-waste FDM/FFF production, recycled PETG/PLA/PA materials, cardboard or refill packaging, and verified recycled feedstocks. UNEP notes that 19–23 million tonnes of plastic waste leak into aquatic ecosystems annually, strengthening demand for materials that reduce virgin-plastic dependence. UNEP states that more than 400 million tonnes of plastic are produced annually, while 19–23 million tonnes leak into aquatic ecosystems each year, creating policy pressure for recyclable and lower-waste materials.

Driving factors include circular-economy regulation, corporate carbon reduction and localized manufacturing. The EU’s Packaging and Packaging Waste Regulation aims to make all packaging recyclable in an economically viable way by 2030 and reduce reliance on primary raw materials. In the U.S., EPA’s National Recycling Goal targets a 50% recycling rate by 2030, encouraging stronger recycling markets and cleaner material streams.

Government policy is strengthening demand. The European Commission’s Packaging and Packaging Waste Regulation aims to make all EU-market packaging recyclable in an economically viable way by 2030, increase recycled-plastic use, and move the sector toward climate neutrality by 2050. Although these rules are packaging-focused, they influence material buyers, recyclers and polymer processors across adjacent 3D printing supply chains.

Policy pressure is a major driver. The European Commission set a target for 10 million tonnes of recycled plastics to be used in new EU products by 2025, while the EU plastics strategy proposed that at least 55% of plastic packaging should be recycled by 2025. The IEA states petrochemicals are set to account for over one-third of oil-demand growth to 2030 and nearly half to 2050, making recycled polymers strategically relevant for reducing fossil-feedstock intensity.

By Product Analysis

Filament dominates with 63.4% share driven by growing demand for sustainable and reusable 3D printing materials

In 2025, Filament held a dominant market position, capturing more than a 63.4% share in the recyclable 3D printing filament market. The strong position of filament-based materials is mainly linked to their wide usage across consumer printing, industrial prototyping, educational projects, and small-scale manufacturing. Filaments are easy to use, cost-efficient, and compatible with most desktop and industrial 3D printers, which has helped increase their adoption globally. The growing preference for eco-friendly printing solutions has also supported demand, as manufacturers and end users are increasingly choosing recyclable materials to reduce plastic waste and improve sustainability practices.

By Recycled Source Analysis

Post-consumer Plastic Waste leads with 43.9% share supported by rising focus on plastic recycling and sustainable manufacturing

In 2025, Post-consumer Plastic Waste held a dominant market position, capturing more than a 43.9% share in the recyclable 3D printing filament market. The segment gained strong traction as manufacturers increasingly used discarded consumer plastics such as bottles, packaging containers, and household waste to produce recyclable filaments. Growing environmental concerns and stricter waste management practices encouraged companies to adopt post-consumer recycled materials as a sustainable alternative to virgin plastics. The availability of large volumes of reusable plastic waste also supported steady raw material supply for filament production.

By Material Type Analysis

Recycled PLA leads with 35.3% share as users prefer eco-friendly and easy-to-print materials

In 2025, Recycled PLA held a dominant market position, capturing more than a 35.3% share in the recyclable 3D printing filament market. The strong demand for recycled PLA was mainly driven by its biodegradable nature, ease of printing, and wide compatibility with desktop and industrial 3D printers. Many educational institutions, hobby users, and small manufacturing businesses preferred recycled PLA because it offers a balance between print quality, affordability, and environmental sustainability. The material also became popular among companies looking to reduce plastic waste and support eco-friendly production practices.

By End Use Analysis

Manufacturing leads with 37.2% share as industries increase use of sustainable 3D printing materials

In 2025, Manufacturing held a dominant market position, capturing more than a 37.2% share in the recyclable 3D printing filament market. The segment witnessed strong growth due to the increasing use of additive manufacturing for rapid prototyping, customized production, and low-volume part manufacturing. Manufacturers across automotive, consumer goods, electronics, and industrial equipment sectors increasingly adopted recyclable filaments to reduce material waste and improve sustainability in production processes. The ability of recyclable filaments to lower operational costs while supporting environmental goals also contributed to wider industry adoption.

Key Market Segments

By Product

- Filament

- Pellets

- Powder

By Recycled Source

- Post-consumer Plastic Waste

- Post-industrial Plastic Waste

- Marine/Fishing Net Waste

- Bio-based Recyclable Feedstock

By Material Type

- Recycled PLA

- Recycled PET

- Recycled ABS

- Recycled Nylon

- Recycled TPU

- Others

By End Use

- Manufacturing

- Education

- Consumer Goods

- Automotive

- Aerospace

- Healthcare

Emerging Trends

Closed-Loop Recycling Systems are Becoming a Major Trend in Recyclable 3D Printing Filament

One of the latest trends shaping the recyclable 3D printing filament market is the growing use of closed-loop recycling systems. Many companies are now collecting failed 3D prints, industrial plastic scraps, and used packaging materials to produce new filament instead of sending waste to landfills. This trend is gaining attention as industries try to reduce raw material costs and improve sustainability practices. According to the United Nations Environment Programme, the world produces more than 400 million tonnes of plastic every year, while only a small percentage is recycled effectively.

This helped businesses lower material waste and improve production efficiency. The trend is especially strong in automotive prototyping, consumer goods, and industrial product development, where companies are trying to reduce environmental impact without affecting production speed. Governments and environmental organizations are also supporting circular economy projects that promote recycling and material reuse.

Advanced Recycling Technologies are Improving Filament Quality and Expanding Industrial Use

Another important trend in the recyclable 3D printing filament market is the rapid improvement in plastic recycling and purification technologies. Earlier, recycled filaments often faced problems such as inconsistent strength, uneven texture, and poor print quality. However, recent advancements in filtration, extrusion, and sorting systems are helping manufacturers create more reliable recyclable filament materials. According to the World Bank Waste Management Report, global waste generation could reach nearly 3.86 billion tonnes by 2050 without stronger waste management systems.

Government-backed sustainability programs and stricter environmental regulations are also encouraging industries to adopt higher-quality recycled materials. As technology continues improving, recyclable 3D printing filament is becoming more competitive with virgin plastic materials in terms of durability and printing performance, creating new opportunities across industrial and commercial sectors.

Drivers

Rising Plastic Waste Recycling Efforts are Driving Demand for Recyclable 3D Printing Filaments

The growing problem of global plastic waste is becoming one of the biggest reasons behind the rising demand for recyclable 3D printing filament. Governments, environmental agencies, and manufacturers are actively looking for practical ways to reuse discarded plastic instead of sending it to landfills. According to the OECD, only 9% of global plastic waste is currently recycled, while plastic waste generation is expected to nearly triple by 2060.

In 2025 and 2026, manufacturers increasingly used recycled PLA, PETG, and ABS materials made from post-consumer plastic waste like bottles, packaging materials, and industrial scraps. The 3D printing industry has become an important part of sustainable manufacturing because it allows businesses to reuse waste material while reducing dependence on virgin plastics. Educational institutions, automotive companies, and consumer product manufacturers are also supporting this shift by choosing recyclable filament for prototypes and low-volume production.

Government Sustainability Programs and Environmental Policies are Supporting Market Expansion

Government initiatives focused on reducing plastic pollution are strongly supporting the recyclable 3D printing filament market. Many countries are introducing stricter regulations on single-use plastics and encouraging industries to increase the use of recycled materials. According to UNEP, around 19 to 23 million tonnes of plastic waste enter aquatic ecosystems every year. In addition, the United Nations states that more than 400 million tonnes of plastic are produced globally every year, but less than 10% is recycled.

Several local authorities and industrial bodies supported the use of recycled plastics in additive manufacturing to reduce industrial waste and lower carbon emissions. Recyclable 3D printing filament fits well into these sustainability goals because it helps convert plastic waste into valuable manufacturing material. The market is also benefiting from rising public awareness regarding environmental protection and responsible plastic consumption.

Restraints

Inconsistent Material Quality and Recycling Challenges are Limiting Wider Market Adoption

One of the biggest challenges slowing the growth of the recyclable 3D printing filament market is the inconsistent quality of recycled plastic materials. Unlike virgin plastics, recycled materials often vary in strength, purity, color, and durability because they come from different waste sources. This affects print accuracy and performance, especially in industrial applications where precision is important. According to the United Nations Environment Programme (UNEP), the world produces more than 400 million tonnes of plastic waste every year, yet only around 9% is successfully recycled.

Poor-quality recycled filament can cause nozzle clogging, uneven printing, weak layer bonding, and reduced product lifespan. These issues make some industries hesitant to fully switch from virgin filament to recycled alternatives, particularly in aerospace, healthcare, and engineering applications.

Limited Recycling Infrastructure and High Processing Costs Continue to Affect Supply Chains

Another major restraining factor for the recyclable 3D printing filament market is the limited availability of efficient recycling infrastructure across many regions. Although governments are promoting plastic recycling, many countries still lack proper collection, sorting, and processing systems needed to create high-quality recycled plastics for industrial use. According to the OECD Global Plastics Outlook, only 15% of plastic waste is collected for recycling worldwide, and a significant amount is lost during sorting and processing stages.

These additional processing expenses can make recycled filament more expensive than expected, especially for small and medium-sized producers. In some regions, industries still find virgin plastic materials easier and more economical to source in bulk quantities. Transportation and storage of recyclable waste materials further add pressure to supply chains. Until recycling infrastructure improves and processing becomes more cost-efficient, the market may continue facing challenges in achieving large-scale adoption across all industrial sectors.

Opportunity

Expansion of Circular Economy Programs is Creating Strong Growth Opportunities for Recyclable 3D Printing Filament

One of the biggest growth opportunities for the recyclable 3D printing filament market is the global shift toward circular economy practices. Governments and industries are increasingly focusing on reducing waste and reusing plastic materials in manufacturing processes. According to the European Environment Agency (EEA), Europe generates nearly 16 million tonnes of plastic packaging waste annually, and recycling targets are being increased under regional sustainability programs.

The growing popularity of localized manufacturing and low-waste production methods has further increased the importance of recyclable 3D printing materials. Governments are also supporting recycling innovation through grants, research funding, and plastic reduction policies. As industries continue looking for cost-effective and eco-friendly materials, recyclable 3D printing filament is expected to benefit from broader adoption across automotive, consumer goods, and industrial design sectors.

Rising Government Investment in Recycling Infrastructure is Supporting Future Market Growth

Another important growth opportunity for the recyclable 3D printing filament market is the increasing investment in recycling infrastructure and sustainable manufacturing programs. Many governments are introducing policies aimed at improving plastic collection, sorting, and reuse systems. According to the World Bank, global waste generation is expected to rise by 70% by 2050 if no major action is taken.

Better recycling systems also help reduce contamination issues and improve filament consistency, making recyclable materials more attractive for industrial applications. In addition, the growing use of 3D printing in education, healthcare, automotive, and product design is creating fresh demand for environmentally friendly filament options.

Regional Insights

North America dominates the recyclable 3D printing filament market with 37.4% share valued at USD 0.3 Billion

In 2025, North America held a dominant position in the recyclable 3D printing filament market, accounting for 37.4% of the global market share and reaching a market value of nearly USD 0.3 Billion. The region’s leadership is mainly supported by the strong presence of advanced manufacturing industries, growing adoption of sustainable production technologies, and increasing investment in additive manufacturing solutions across the United States and Canada.

The United States remains the largest contributor within North America due to its well-established 3D printing ecosystem and high use of additive manufacturing in aerospace, automotive, healthcare, and industrial prototyping applications. Several manufacturers and research institutions are focusing on recycled PLA, PETG, and ABS filament development to support circular economy goals.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Fillamentum has built a strong position in the recyclable 3D printing filament market through sustainable material innovation and global expansion. The company distributes its products across more than 62 countries and introduced environmentally focused products such as NonOilen®, a 100% biodegradable and recyclable filament, and recycled PA6 filament made from fishing nets. In 2026, the company expanded its recycled PETG portfolio using medical-grade PETG waste streams for cleaner recycling processes. Fillamentum also operates with ISO 9001 and ISO 14001 certifications and continues investing in automation and Industry 4.0 production technologies.

Polymaker remains a major player in sustainable 3D printing materials with a strong focus on recycled and eco-friendly filament development. The company partnered with Covestro to develop Polymaker™ PC-r, a recycled polycarbonate filament produced from discarded 19-liter water bottles. In 2025 and 2026, the company expanded sustainable product lines such as PolyTerra™ and transitioned all filament packaging to 100% recycled cardboard spools. Polymaker also reported planting more than 200,000 trees through its sustainability program and strengthened distribution operations through its Houston facility expansion serving North America markets.

Top Key Players Outlook

- Fillamentum

- Polymaker

- ReDeTec

- 3D Printlife

- ProtoCycler

- FormFutura

- Sulapac Oy

- KiwiFil

- Printerior

- GreenGate3D

- colorFabb BV

- Filabot

- Protoplant

- 3DXTECH

- Filamentive Limited

Recent Industry Developments

In 2025, ProtoCycler, developed by ReDeTec, remained focused on closed-loop recyclable 3D printing filament production through its ProtoCycler V3 desktop filament maker and recycler. The system supports recycling of failed prints, support waste, rafting material, and plastic scraps into new filament, helping users reduce filament costs by up to 80%. Its key product development includes patented MixFlow™ hardware, dual digital diameter feedback sensors, AI-powered control, automatic operation, an optional grinder, and integrated extrusion control.

In 2025, FormFutura strengthened its role in the recyclable 3D printing filament sector through its ReForm recycled filament range, which includes recycled material options such as rPLA, rPET, rTitan, and other recycled grades. The company offers recycled filament products such as ReForm rPLA at €16.52, supports worldwide shipping, and promotes same-business-day shipping for orders placed before 15h CET. Sources: FormFutura, VoxelMatters.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 0.9 Bn |

| Forecast Revenue (2035) | USD 3.9 Bn |

| CAGR (2026-2035) | 16.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Filament, Pellets, Powder), By Recycled Source (Post-consumer Plastic Waste, Post-industrial Plastic Waste, Marine/Fishing Net Waste, Bio-based Recyclable Feedstock), By Material Type (Recycled PLA, Recycled PET, Recycled ABS, Recycled Nylon, Recycled TPU, Others), By End Use (Manufacturing, Education, Consumer Goods, Automotive, Aerospace, Healthcare) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Fillamentum, Polymaker, ReDeTec, 3D Printlife, ProtoCycler, FormFutura, Sulapac Oy, KiwiFil, Printerior, GreenGate3D, colorFabb BV, Filabot, Protoplant, 3DXTECH, Filamentive Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |