Quick Navigation

Report Overview

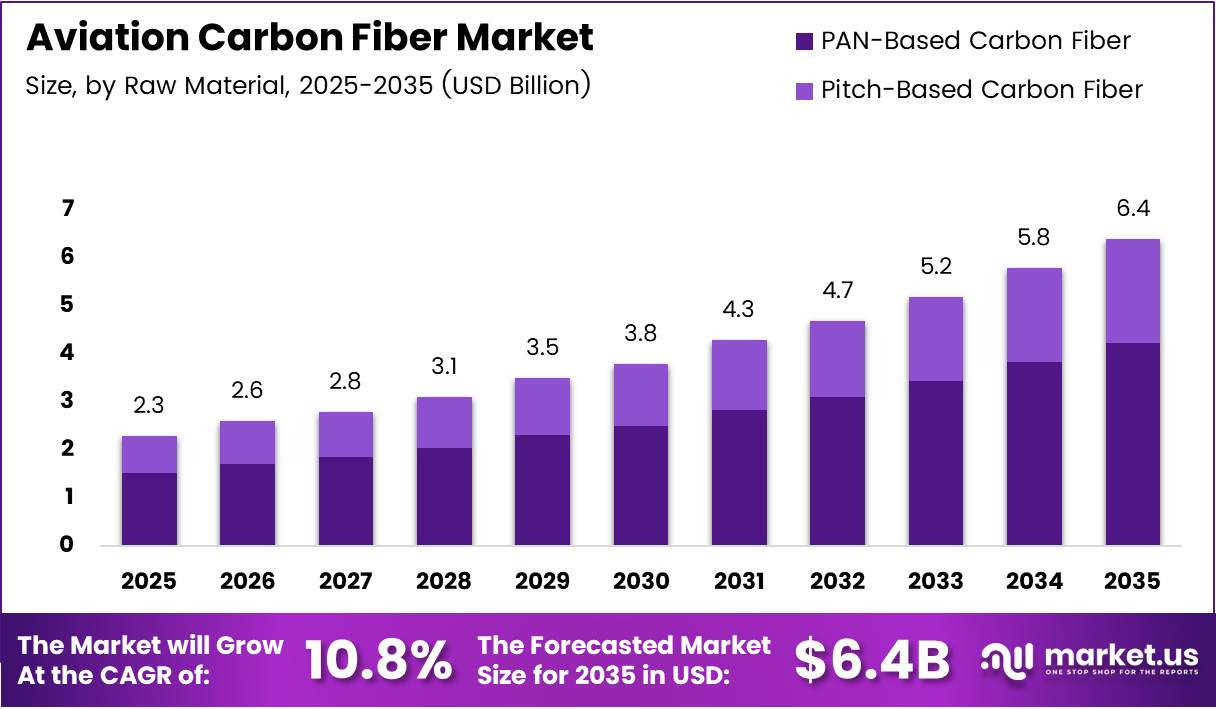

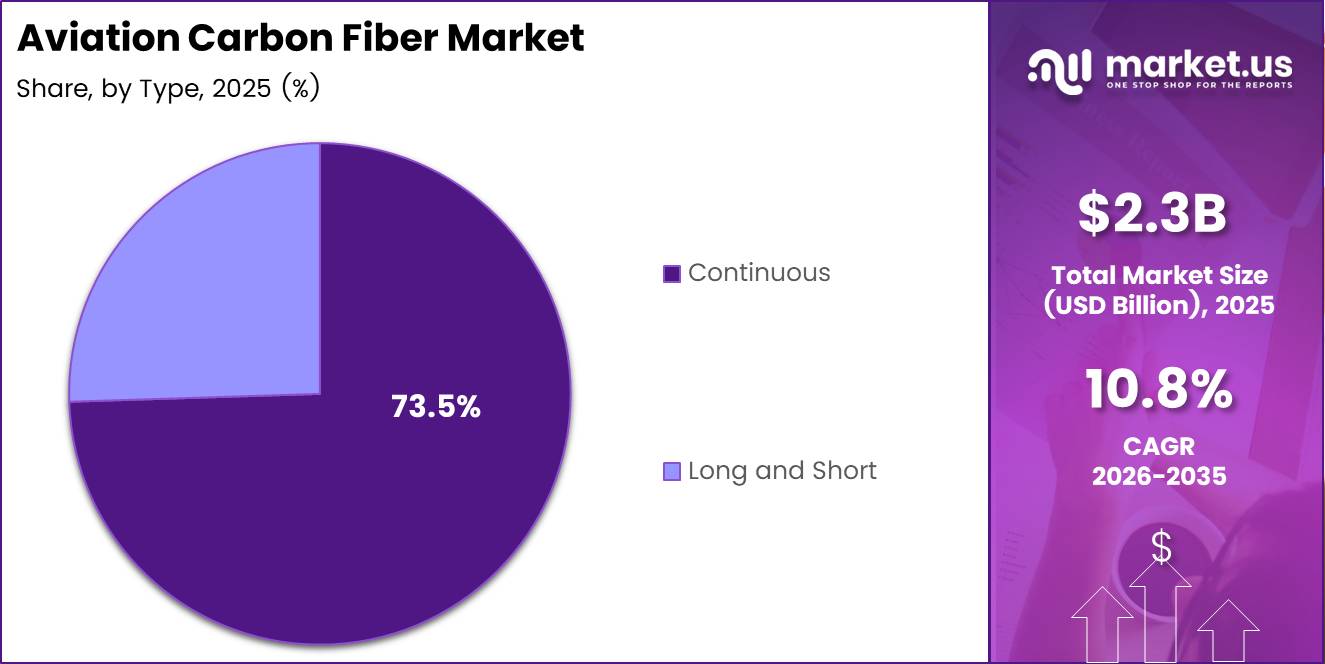

The Global Aviation Carbon Fiber Market size is expected to be worth around USD 6.4 Billion by 2035 from USD 2.3 Billion in 2025, growing at a CAGR of 10.8% during the forecast period 2026 to 2035.

Aviation carbon fiber refers to high-strength, low-weight composite materials used in aircraft structures, engine components, and interior assemblies. Airlines and aircraft manufacturers adopt these materials to reduce structural weight without compromising tensile strength. The market spans raw fiber production, woven fabrics, and finished composite parts used across commercial, military, and emerging aviation segments.

The ckv sector drives the bulk of carbon fiber demand. Aircraft OEMs prioritize materials that reduce operational costs over the service life of each aircraft. Carbon fiber composites meet this need by cutting structural weight, which directly reduces fuel burn per flight hour. This cost-per-flight logic has made composite adoption a procurement priority rather than an engineering preference.

Fleet expansion programs across North America, Europe, and Asia Pacific sustain material demand well into the next decade. Airbus and Boeing backlogs currently extend beyond eight years, locking in composite material procurement volumes well into the forecast period. This pipeline removes demand uncertainty for tier-one carbon fiber suppliers and justifies long-term capacity investment decisions.

Regulatory pressure to cut aviation carbon emissions adds a structural tailwind to composite adoption. International aviation bodies have set binding carbon reduction targets for commercial operators. Airlines under compliance pressure accelerate fleet modernization, which means earlier retirement of metal-heavy legacy aircraft and faster uptake of composite-rich new-generation platforms.

In March 2024, Hexcel Corporation launched its HexTow IM9 24K continuous carbon fiber for aerospace applications, delivering higher tensile strength than earlier grades. This product move signals that suppliers are competing on material performance, not price alone — a dynamic that rewards technically differentiated players and raises quality expectations across the supply chain.

According to a 2025 academic study published by Academic Publishers, replacing aluminium with composite materials, primarily CFRP, in aircraft structures enables a 15–30% reduction in structural weight. This range matters to operators because even a 15% weight reduction translates into measurable fuel cost savings at scale across a commercial fleet operating thousands of cycles per year.

According to Hexcel’s 2026 lightweighting overview, carbon fiber is approximately 5 times stronger than aluminium while being about 30% lighter. This strength-to-weight advantage is not merely a design benefit — it directly enables engine downsizing and range extension without structural trade-offs, making carbon fiber the default material choice for next-generation aircraft programs.

Key Takeaways

- The Global Aviation Carbon Fiber Market was valued at USD 2.3 Billion in 2025 and is forecast to reach USD 6.4 Billion by 2035.

- The market is forecast to expand at a CAGR of 10.8% during the period 2026 to 2035.

- By Raw Material, PAN-Based Carbon Fiber leads with a 87.1% share in 2025.

- By Type, Continuous fiber holds the dominant position with a 73.5% share in 2025.

- By End Use, Commercial aviation accounts for the largest share at 64.3% in 2025.

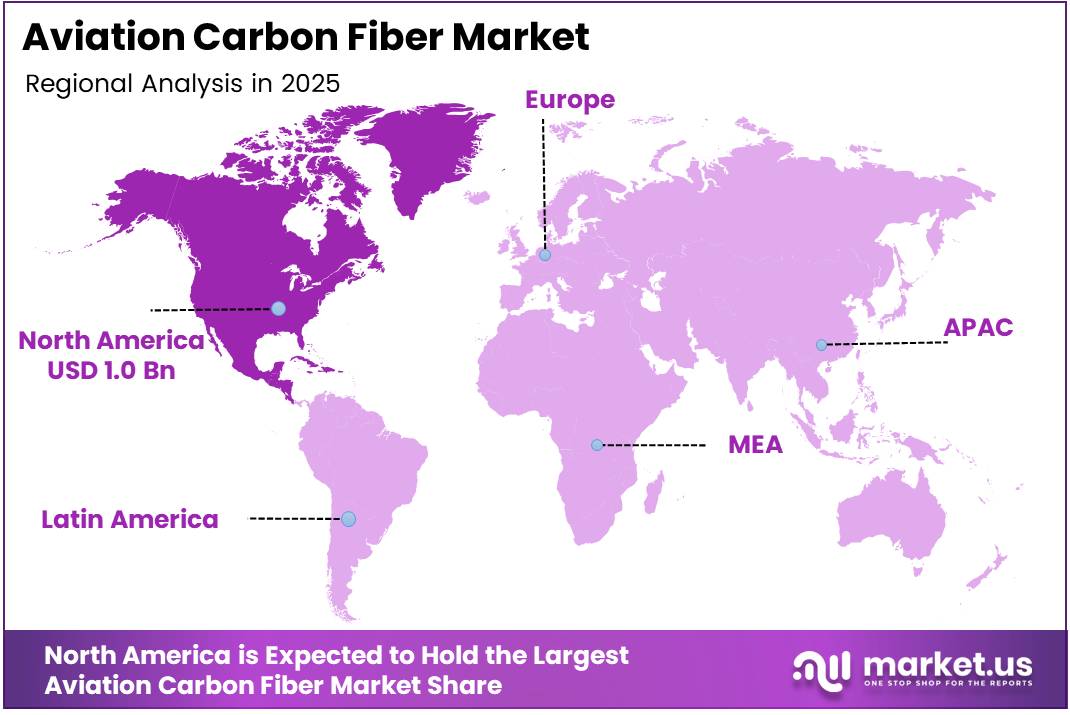

- North America leads all regions with a 43.70% share, valued at USD 1.0 Billion in 2025.

Raw Material Analysis

PAN-Based Carbon Fiber dominates with 87.1% due to superior tensile strength and scalable production.

In 2025, PAN-Based Carbon Fiber held a dominant market position in the By Raw Material segment of the Aviation Carbon Fiber Market, with an 87.1% share. Polyacrylonitrile precursor delivers the consistent fiber strength and modulus that aerospace structural applications demand. Its established global supply chain and compatibility with standard composite manufacturing processes reinforce this dominance across both commercial and military programs.

Pitch-Based Carbon Fiber serves specialized high-modulus applications where stiffness outweighs cost considerations. It finds use in satellite structures and select aerospace thermal management components. However, its higher production cost and narrower processing window limit volume adoption in mainstream commercial airframe manufacturing. In 2024, Mitsubishi Chemical Group expanded its thermoplastic carbon fiber portfolio toward more recyclable composite solutions, signaling that the gap between conventional and advanced fiber types may narrow over the forecast period.

Type Analysis

Continuous fiber dominates with 73.5% due to structural load-bearing requirements in primary airframe components.

In 2025, Continuous carbon fiber held a dominant market position in the By Type segment of the Aviation Carbon Fiber Market, with a 73.5% share. Continuous fiber enables uninterrupted load paths through fuselage frames, wing spars, and nacelle structures — applications where fiber discontinuity would introduce stress concentrations that compromise airworthiness certification. Aircraft OEMs specify continuous fiber for every primary structural component, which locks in its volume share.

Long and Short fiber formats serve secondary and interior applications where complex part geometry makes continuous layup impractical. Short fiber compounds allow injection molding of brackets, fairings, and interior panels, reducing tooling complexity and cycle time. However, their mechanical properties are inherently lower than continuous-fiber laminates, which restricts them to non-structural roles and limits their share of the overall aviation carbon fiber bill of materials.

End Use Analysis

Commercial aviation dominates with 64.3% due to fleet scale and sustained OEM production volumes.

In 2025, Commercial aviation held a dominant market position in the By End Use segment of the Aviation Carbon Fiber Market, with a 64.3% share. The commercial segment benefits from multi-year aircraft production programs at Airbus and Boeing, which create predictable, high-volume composite material pull-through. Each wide-body aircraft program consumes several tonnes of carbon fiber, making commercial OEM contracts the single most valuable revenue stream for tier-one material suppliers.

Military aviation represents a structurally stable but volume-constrained end-use segment. Defense aircraft programs operate under classified procurement cycles with smaller annual unit builds than commercial programs. However, military buyers accept higher material costs in exchange for performance gains, meaning per-unit carbon fiber revenue in defense programs typically exceeds commercial averages. This margin dynamic makes military contracts strategically valuable for suppliers even without volume leadership.

Others — which includes business jets, regional aircraft, and emerging urban air mobility platforms — represents the fastest-expanding portion of the end-use mix. Electric vertical takeoff and landing vehicles require lightweight structures to offset battery mass penalties, making carbon fiber a structural necessity rather than a premium option. As certification timelines for urban air mobility platforms compress, this sub-segment will absorb increasing volumes of advanced composite materials.

Key Market Segments

By Raw Material

- PAN-Based Carbon Fiber

- Pitch-Based Carbon Fiber

By Type

- Continuous

- Long and Short

By End Use

- Commercial

- Military

- Others

Drivers

Fuel Efficiency and Emissions Mandates Accelerate Composite Material Adoption Across Commercial Fleets

Commercial airlines face binding carbon reduction targets set by international aviation regulators. Carbon fiber composites directly address this pressure by cutting structural weight, which reduces fuel burn per flight cycle. Airlines replacing legacy metal-heavy aircraft with composite-rich platforms achieve measurable compliance progress without operational disruption. This regulatory-commercial alignment makes composite specification a fleet strategy decision, not just an engineering preference.

According to a 2025 academic study published by Academic Publishers, replacing aluminium with CFRP in aircraft structures delivers a 15–30% reduction in structural weight, contributing to a 20–25% improvement in fuel efficiency for commercial aviation. This efficiency gain compounds across a fleet of hundreds of aircraft operating thousands of cycles annually — translating regulatory compliance into a direct operating cost advantage for early adopters.

In 2024, Hexcel Corporation continued expanding advanced composite offerings through partnerships with Boeing and Airbus to supply higher-performance carbon fiber materials that enhance aircraft fuel efficiency. Supplier-OEM integration of this depth shortens material qualification timelines and locks in preferred supplier status for the next generation of narrowbody and widebody programs, reinforcing the commercial driver at the supply chain level.

Restraints

High Production Costs and Complex Manufacturing Processes Limit Carbon Fiber Market Scalability

Carbon fiber production requires high-temperature oxidation and carbonization processes with energy-intensive equipment and long cycle times. These cost structures translate into material prices that remain significantly above aluminium on a per-kilogram basis. For secondary structures and interior components, buyers compare this cost premium against marginal weight savings — and frequently choose cheaper alternatives, compressing the addressable market for carbon fiber suppliers.

According to a 2025 aerospace-focused article on carbon fiber composites, carbon fiber composites are approximately 50% lighter than aluminium. While this performance advantage is substantial, the cost-per-kilogram gap means the economics only justify carbon fiber in weight-critical primary structures for most commercial operators. Until production costs fall, the material remains locked out of broader secondary and tertiary aerospace applications that could otherwise expand total market volume.

Complex manufacturing processes also create qualification barriers. Aerospace-grade composite structures require non-destructive testing, autoclave processing, and strict environmental controls throughout fabrication. These requirements increase capital expenditure and limit the number of qualified suppliers capable of meeting OEM specifications. Consequently, new market entrants face long certification timelines, which restricts competitive pressure and slows the supply-side capacity expansion needed to meet long-term demand growth.

Growth Factors

Recyclable Composites and Next-Generation Aircraft Programs Open New Revenue Streams for Material Suppliers

Development of recyclable and sustainable carbon fiber addresses the end-of-life disposal problem that has limited composite adoption in cost-sensitive programs. Thermoplastic matrix systems allow fiber reclamation after part retirement — reducing total lifecycle cost and enabling operators to meet sustainability procurement criteria. Suppliers that commercialize recyclable composite systems first will access a qualification advantage that compounds over the decade-long certification cycles typical of aerospace programs.

Urban air mobility vehicles present a structurally different demand profile from traditional aviation. These platforms require maximum weight reduction to offset battery mass, making carbon fiber a functional necessity rather than a premium upgrade. According to Hexcel’s 2025–2026 aerospace communications, composite-rich aircraft such as the Airbus A350 and Boeing 787 achieve approximately 25% advantages in fuel burn, operating costs, and CO₂ emissions versus prior-generation aircraft — a benchmark that urban air mobility designers now treat as a baseline performance target.

In 2024, Asian producers including Zhongfu Shenying Carbon Fiber Co., Ltd. and Hyosung Advanced Materials increased investment to expand carbon fiber production capacity targeting aerospace demand in Asia Pacific. This regional capacity build-out reduces supply concentration risk for OEMs currently dependent on North American and Japanese suppliers. Emerging-economy aerospace manufacturing expansion simultaneously creates new downstream demand and new upstream supply, restructuring the global carbon fiber value chain.

Emerging Trends

Automation, Hybrid Composites, and Electrification Reshape the Carbon Fiber Application Landscape

Automated Fiber Placement technology reduces manual labor in composite layup by programming robotic arms to place pre-impregnated fiber tows with precision. AFP cuts waste, shortens cycle times, and enables complex curved geometries that manual layup cannot replicate consistently. Manufacturers adopting AFP gain both cost and quality advantages, which are particularly compelling as aircraft production rates ramp toward pre-2020 levels and beyond.

Hybrid composite materials — combining carbon fiber with glass, aramid, or natural fibers — allow engineers to tune structural properties for specific load cases while managing material cost. This approach lets designers deploy carbon fiber only where its strength-to-weight advantage is essential, reducing per-aircraft material spend without sacrificing structural performance targets. The shift toward hybrid architectures broadens the addressable scope for carbon fiber within each aircraft bill of materials.

According to Hexcel, its HexWeb Acousti-Cap sound-attenuating honeycomb used in engine nacelles provides up to 40% noise reduction in the Boeing 737 MAX engine compared to its predecessor, without adding structural weight. This acoustic performance data illustrates that carbon fiber composite innovation extends beyond structural weight reduction — it now encompasses noise, vibration, and operational environment control, expanding the value proposition for aviation carbon fiber suppliers in next-generation and hybrid-electric aircraft programs.

Regional Analysis

North America Dominates the Aviation Carbon Fiber Market with a Market Share of 43.70%, Valued at USD 1.0 Billion

North America holds a 43.70% share of the aviation carbon fiber market, valued at approximately USD 1.0 Billion in 2025. The region benefits from the co-location of major aircraft OEMs, tier-one composite suppliers, and advanced manufacturing infrastructure. Long-standing procurement relationships between US-based defense agencies and domestic composite producers further reinforce North America’s structural leadership in this market.

Europe Aviation Carbon Fiber Market Trends

Europe commands a significant share driven by Airbus’s composite-intensive aircraft programs, particularly the A350 XWB, which uses approximately 53% composite materials by weight. Germany, France, and the UK host vertically integrated aerospace supply chains that support both raw fiber production and finished composite part manufacturing. European aerospace investment in sustainable composite materials also positions the region to lead recyclable carbon fiber adoption.

Asia Pacific Aviation Carbon Fiber Market Trends

Asia Pacific represents the fastest-expanding region for aviation carbon fiber demand, anchored by growing domestic airline fleets in China and India and expanding aerospace manufacturing in Japan and South Korea. Japanese producers maintain deep technical expertise in PAN-based carbon fiber, while Chinese firms accelerate domestic production capacity to reduce import dependence. Regional fleet growth and OEM localization strategies together sustain a multi-year material demand outlook.

Middle East and Africa Aviation Carbon Fiber Market Trends

The Middle East sustains carbon fiber demand through the fleet expansion strategies of major Gulf carriers, which operate composite-heavy widebody aircraft on long-haul international routes. MRO activity at Gulf aviation hubs creates a secondary demand stream for composite repair materials and tooling. Africa remains at an early stage of aerospace manufacturing development, though infrastructure investment in aviation logistics may gradually create downstream composite demand.

Latin America Aviation Carbon Fiber Market Trends

Latin America’s aviation carbon fiber consumption ties primarily to aircraft maintenance, repair, and overhaul activity rather than original equipment manufacturing. Brazil hosts the most developed aerospace manufacturing base in the region, with Embraer’s regional jet programs incorporating composite structures. Growth in low-cost carrier fleets across Brazil and Mexico creates progressive demand for composite replacement parts and repair materials throughout the forecast period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

SGL Carbon SE positions itself at the intersection of carbon fiber raw material production and engineered composite solutions for aerospace. Its vertically integrated structure — spanning precursor fiber, conversion, and finished components — allows the company to control quality at each production stage. This integration reduces defect risk in aerospace-grade materials and supports long qualification cycles that OEMs require before approving new suppliers.

TEIJIN LIMITED combines carbon fiber manufacturing with advanced thermoplastic composite development, targeting the growing demand for recyclable composite structures in aerospace applications. Its dual focus on performance and sustainability aligns with procurement criteria that aerospace OEMs now mandate for next-generation programs. Teijin’s investment in rapid-cycle thermoplastic processing also addresses the throughput bottleneck that limits composite adoption in higher-rate production programs.

Toray Industries Inc. leads global carbon fiber production capacity and holds preferred supplier positions across the major commercial aircraft programs. Its long-term supply agreements with widebody OEMs secure volume off-take that underwrites further capacity investment. Toray’s deep material science capability allows it to develop application-specific fiber grades, ensuring its materials remain specified as OEMs push structural performance targets higher on next-generation designs.

Solvay SA focuses on high-performance aerospace composite systems that combine carbon fiber with advanced resin technologies. Its portfolio includes prepreg materials and structural adhesives qualified for primary and secondary aircraft structures. Solvay’s chemistry expertise allows it to engineer matrix systems that improve damage tolerance and out-of-autoclave processability — both critical requirements as composite manufacturers seek to reduce energy-intensive curing infrastructure costs. In January 2025, Tex-Tech Industries acquired Fiber Materials Inc. to strengthen high-temperature carbon composite capabilities, illustrating the broader industry trend of capability-driven consolidation that Solvay must navigate to defend its specialty composite positioning.

Key Players

- SGL Carbon SE

- TEIJIN LIMITED

- Toray Industries Inc.

- Solvay SA

- Du Pont de Nemours Inc.

- Hexcel Corporation

- Mitsubishi Chemical Corporation

- AVIC Composite Corporation

- Kureha Corporation

- DowAksa SA

Recent Developments

- March 2024 — Hexcel Corporation unveiled its HexTow IM9 24K continuous carbon fiber designed for aerospace applications, offering higher tensile strength and processing efficiency than earlier fiber grades. This product targets primary structural applications where performance-per-kilogram justifies premium material pricing.

- 2024 — Hexcel Corporation continued expanding its advanced composite portfolio through partnerships with Boeing and Airbus to supply higher-performance carbon fiber materials that directly enhance aircraft fuel efficiency. These supply agreements reinforce Hexcel’s position within the two largest commercial aircraft production programs globally.

- 2024 — Mitsubishi Chemical Group expanded its thermoplastic carbon fiber portfolio aimed at more recyclable and cost-efficient composite solutions for aerospace and other mobility applications. This portfolio extension aligns with increasing OEM requirements for end-of-life material reclamation in next-generation aircraft programs.

- January 2025 — Tex-Tech Industries Inc. acquired Fiber Materials Inc. to strengthen its capabilities in high-temperature carbon/carbon composites used in aerospace thermal protection systems and rocket components. This acquisition directly expands Tex-Tech’s addressable scope within aviation and space carbon fiber demand.

- 2024 — Asian producers Zhongfu Shenying Carbon Fiber Co., Ltd. and Hyosung Advanced Materials increased capital investment to expand carbon fiber production capacity, targeting aerospace demand growth in the Asia Pacific region. This capacity build-out signals a structural shift in the global carbon fiber supply map away from its historical concentration in North America and Japan.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.3 Billion |

| Forecast Revenue (2035) | USD 6.4 Billion |

| CAGR (2026-2035) | 10.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (PAN-Based Carbon Fiber, Pitch-Based Carbon Fiber), By Type (Continuous, Long and Short), By End Use (Commercial, Military, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | SGL Carbon SE, TEIJIN LIMITED, Toray Industries Inc., Solvay SA, Du Pont de Nemours Inc., Hexcel Corporation, Mitsubishi Chemical Corporation, AVIC Composite Corporation, Kureha Corporation, DowAksa SA |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |