Quick Navigation

Report Overview

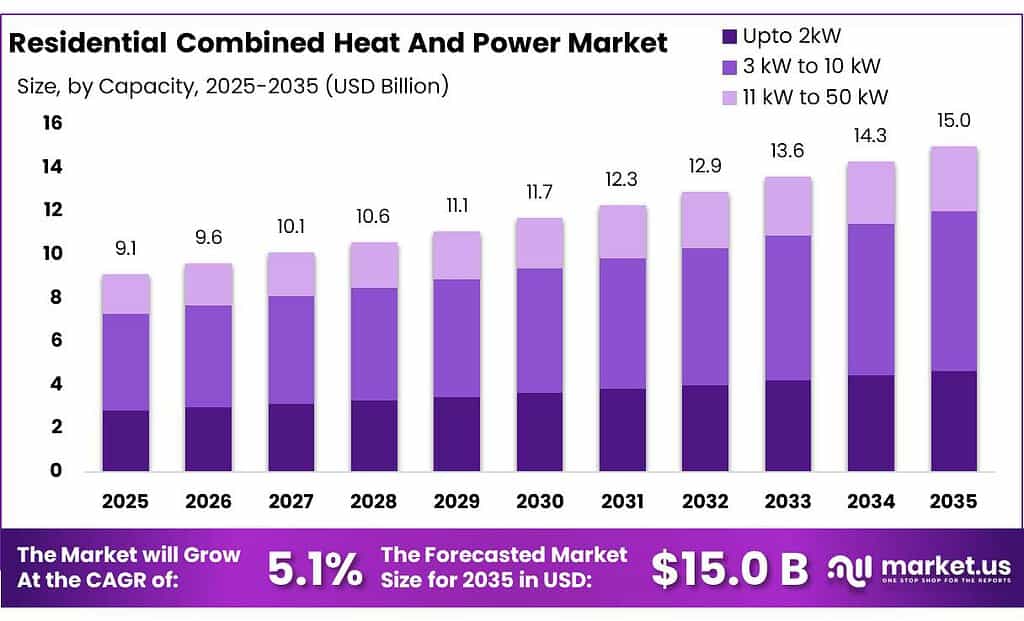

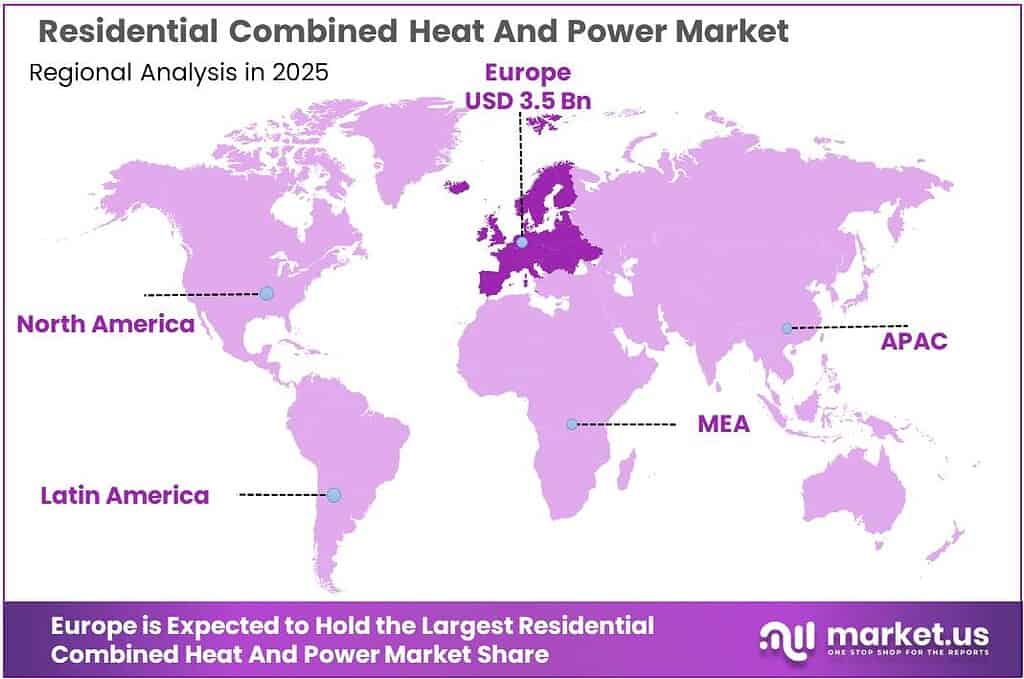

The Global Residential Combined Heat And Power Market size is expected to be worth around USD 15.0 Billion by 2035, from USD 9.1 Billion in 2025, growing at a CAGR of 5.1% during the forecast period from 2026 to 2035. In 2025, Europe held a dominant market position, capturing more than a 38.7% share, holding USD 3.5 Billion revenue.

Residential Combined Heat and Power (CHP), often referred to as micro-CHP, is positioned as a distributed energy solution that generates electricity and useful heat from a single fuel input at the home level. Its industrial relevance comes from its ability to reduce transmission losses, improve site-level efficiency, and support household resilience where heating and hot-water demand are material.

- According to the U.S. EPA, conventional separate heat and grid power typically deliver about 50% to 55% overall fuel efficiency, while CHP systems typically achieve 65% to 80%, with some installations approaching 90%. That efficiency advantage remains the core value proposition for the residential segment.

The industrial scenario is most mature in Japan and parts of Europe, where policy support and dense heating demand have created a clearer use case than in many other regions. Japan’s household fuel-cell ecosystem is the strongest commercialization benchmark: the Ministry of Economy, Trade and Industry stated that more than 490,000 Ene-Farm units were in use as of the end of September 2023.

In Europe, the European Commission-backed BUILD UP platform reported that fuel-cell micro-CHP is already used in over half a million buildings globally, while EU-funded deployment programs installed more than 3,500 units across 10 European countries since 2012, supported by more than €200 million of private investment.

Demand is being reinforced by building decarbonization policy and energy-security priorities rather than by pure equipment replacement cycles alone. In the EU, buildings account for around 40% of energy consumption, around 50% of gas consumption, and roughly 80% of home energy use for heating, cooling, and hot water. The revised Energy Performance of Buildings Directive entered into force on 28 May 2024, and each EU country must adopt a residential trajectory to reduce average primary energy use by 16% by 2030 and 20% to 22% by 2035.

Japan remains the clearest proof-of-scale for residential CHP. Japan’s Agency for Natural Resources and Energy reported that more than 540,000 ENE-FARM residential fuel-cell units were in use in FY2024. The same policy ecosystem has emphasized that household fuel cells can cover roughly 70% of a home’s power demand, while METI documentation has cited potential CO2 reductions of 38%, or about 1,330 kg per year, from Ene-Farm adoption under stated assumptions.

Osaka Gas separately announced cumulative sales of 200,000 Ene-Farm units as of 5 April 2024, with estimated annual CO2 reductions of roughly 370,000 tons, supported by subsidies of up to ¥200,000 per unit at installation.

Key Takeaways

- Residential Combined Heat And Power Market size is expected to be worth around USD 15.0 Billion by 2035, from USD 9.1 Billion in 2025, growing at a CAGR of 5.1%.

- 3 kW to 10 kW held a dominant market position, capturing more than a 49.6% share.

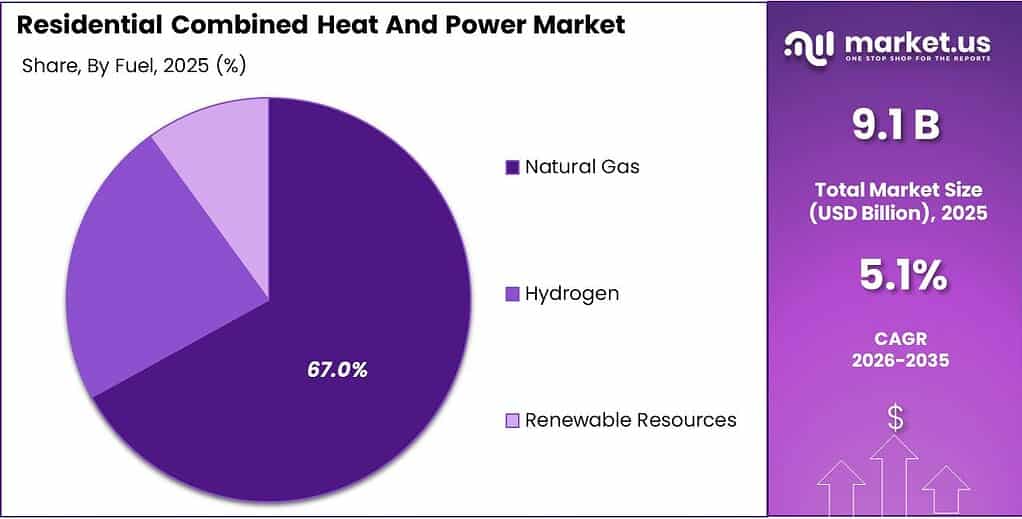

- Natural Gas held a dominant market position, capturing more than a 67.3% share.

- Reciprocating Engine held a dominant market position, capturing more than a 37.4% share.

- Europe held the dominant position in the residential combined heat and power market, capturing 38.7% of the global share, equivalent to nearly USD 3.5 Billion.

By Capacity Analysis

3 kW to 10 kW leads the residential CHP market with 49.6% share, supported by strong demand for efficient home energy systems.

In 2025, 3 kW to 10 kW held a dominant market position, capturing more than a 49.6% share. This capacity range remained the most preferred choice in the residential combined heat and power market because it fits well with the energy needs of individual homes, villas, small apartment blocks, and multi-family residences. Homeowners increasingly favored systems in this range as they offer a practical balance between electricity generation and heat recovery, helping reduce monthly power costs while improving overall energy efficiency.

By Fuel Analysis

Natural Gas dominates the residential CHP market with 67.3% share, driven by its easy availability and efficient home heating performance.

In 2025, Natural Gas held a dominant market position, capturing more than a 67.3% share. This fuel type remained the leading choice in the residential combined heat and power market because of its strong availability across urban and suburban residential networks, especially in regions with established gas pipeline infrastructure. Homeowners widely preferred natural gas-based CHP systems due to their reliable fuel supply, lower operating cost compared to several alternative fuels, and their ability to provide consistent electricity along with space heating and hot water.

By Prime Mover Analysis

Reciprocating Engine dominates the residential CHP market with 37.4% share, supported by its proven reliability and strong household energy output.

In 2025, Reciprocating Engine held a dominant market position, capturing more than a 37.4% share. This prime mover type remained a preferred choice in the residential combined heat and power market due to its dependable performance, mature technology base, and ability to efficiently deliver both electricity and useful heat for household applications. Systems using reciprocating engines were widely adopted in residential settings because they respond well to varying daily energy loads, making them suitable for homes with changing electricity and heating needs throughout the day.

Key Market Segments

By Capacity

- Upto 2kW

- 3 kW to 10 kW

- 11 kW to 50 kW

By Fuel

- Natural Gas

- Hydrogen

- Renewable Resources

By Prime Mover

- Gas Turbine

- Steam Turbine

- Reciprocating Engine

- Fuel Cell

- Microturbine

Emerging Trends

Smart home energy management integration is the latest trend reshaping residential CHP

One of the most important latest trends in the residential combined heat and power market is the integration of CHP units with smart home energy management systems. Homes are no longer using CHP only as a standalone heating and electricity unit. In 2025, the trend is moving toward digitally connected systems that can automatically balance household power demand, heating schedules, battery storage, and even rooftop solar usage. This makes residential CHP much more practical for modern energy-efficient homes.

A strong policy-linked number comes from India’s Bureau of Energy Efficiency, where smart home automation and appliance-level energy management are being actively promoted under residential efficiency roadmaps. In parallel, broader smart home adoption is also supporting this shift, with connected home systems helping households reduce electricity bills by 20–25% annually through automation-based energy control, according to industry-backed smart home trend reporting in 2025.

IoT-based predictive monitoring is improving CHP performance and homeowner confidence

Another major trend is the use of IoT sensors and predictive maintenance tools in residential CHP systems. Modern homeowners increasingly want systems that are easy to monitor through mobile apps and capable of detecting faults before breakdowns happen. This is where the latest trend is clearly visible. Research published in Scientific Reports in 2025 highlights how IoT-enabled residential energy systems are being used for real-time monitoring, adaptive control, and energy optimization inside smart homes.

For residential CHP, this means better runtime efficiency, lower service interruptions, and improved fuel use. The trend is especially strong in premium homes and smart housing projects, where users want complete visibility over electricity generation, heat output, and daily savings. Government-backed smart grid initiatives and connected-home policies are also helping this transition, especially in countries focusing on digital infrastructure and efficient residential buildings.

Drivers

Rising government-backed home energy efficiency programs are strongly accelerating residential CHP adoption

One of the biggest drivers for the residential combined heat and power market is the growing push from governments toward energy-efficient homes and decentralized power systems. Residential CHP fits perfectly into this trend because it can use a single fuel source to provide both electricity and heating, helping households cut overall fuel waste.

The strongest push is coming from building-efficiency regulations, clean heating incentives, and home renovation schemes. According to the International Energy Agency, more than 250 new or updated energy-efficiency policies were introduced in 2025 across countries representing 85% of global energy demand.

Higher fuel efficiency compared with separate heat and power systems is boosting homeowner interest

Another major growth driver is the very high fuel efficiency of CHP compared with conventional residential energy systems. Traditional home setups generate electricity from the grid and heat from separate boilers, which leads to higher combined losses. CHP solves this by capturing the waste heat produced during power generation and using it inside the home. The International Energy Agency notes that CHP systems can reach 75% to 90% total fuel efficiency, far above the 45% to 55% efficiency of separate generation systems.

This large efficiency advantage translates into lower utility bills, better energy security, and reduced carbon emissions for homeowners. It is especially important in regions where governments are promoting electrification and low-carbon heating solutions.

Restraints

High upfront installation cost remains the biggest barrier for residential CHP adoption

The biggest restraining factor for the residential combined heat and power market is the high upfront installation and home integration cost. While CHP systems help save money over time through lower electricity and heating bills, the first investment is still difficult for many homeowners.

Residential buyers often need to cover the unit cost, installation labor, exhaust setup, controls, and in some cases electrical upgrades inside the home. This makes the decision harder, especially in price-sensitive households. A strong reference point comes from the U.S. Department of Energy, which notes that home energy upgrade pathways can include around USD 10,000 per dwelling unit in electrical upgrades alone in some cases.

Limited homeowner financing access slows replacement and retrofit decisions

A second major restraint is the lack of easy consumer financing and subsidy structures specifically designed for micro-CHP systems. Governments across major economies have created strong support for heat pumps and insulation upgrades, but CHP often receives less direct residential incentive support. For example, the International Energy Agency highlights that some residential heating transition programs provide upfront grants of up to CAD 15,000 to reduce adoption barriers for efficient home systems.

Opportunity

Home retrofit programs are creating the biggest growth opportunity for residential CHP

One of the strongest growth opportunities for the residential combined heat and power market is the global rise in home retrofit and building modernization programs. Residential CHP systems fit naturally into retrofit projects because they can replace old boilers while adding on-site electricity generation for the same home.

This is becoming especially important in mature housing markets, where most homes that will exist in 2050 are already built today. The International Energy Agency notes that in advanced economies, around 80% of the 2050 building stock already exists, making retrofitting the main path for future energy upgrades.

Rising heating demand in existing homes opens long-term CHP replacement potential

A second major opportunity comes from the large share of residential energy use linked to space and water heating, especially in colder and developed regions. According to the IEA, in advanced economies space and water heating together account for about 70% of household energy use.

This is a major opening for residential CHP because the technology performs best where homes need regular heat loads throughout the year. Instead of using separate grid electricity and boilers, CHP can serve both needs from one efficient unit, making it attractive for households looking to reduce energy waste.

Regional Insights

Europe dominated the Residential Combined Heat and Power market, accounting for 38.7% share and valued at USD 3.5 Billion, supported by strong home heating infrastructure and favorable energy-efficiency policies.

Europe held the dominant position in the residential combined heat and power market, capturing 38.7% of the global share, equivalent to nearly USD 3.5 Billion. The region’s leadership is strongly linked to its well-established residential heating networks, colder climate conditions, and early adoption of high-efficiency home energy systems.

The region also benefits from strict building energy regulations and long-running government support for cogeneration under energy-efficiency directives. Eurostat data shows that CHP remains deeply integrated into Europe’s energy system, with cogeneration contributing significantly to district and residential heat supply across the EU. In fact, cogeneration technologies currently provide around 15% of the heat used across the EU, highlighting the region’s mature heating ecosystem.

Another major support factor for Europe’s regional dominance is the continued modernization of existing housing stock. A large share of Europe’s homes are older buildings that require heating upgrades, creating a strong replacement market for residential CHP systems. The European Commission also reported that EU gross production of derived heat reached 568 TWh in 2023, showing the scale of heat demand that supports technologies such as residential CHP.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Yanmar remains one of the strongest players in the residential CHP market, supported by its highly efficient gas-engine micro-CHP systems. The company’s residential-scale solutions can achieve up to 88% total system efficiency, while helping end users lower utility expenses by 20% to 50% through on-site heat recovery. Its strong presence in Japan and Europe, combined with decades of distributed energy expertise, gives it an edge in home and small-building installations.

GE Power, now operating under GE Vernova’s energy portfolio, remains an influential technology provider in CHP infrastructure. While its strength is broader across commercial and utility systems, its CHP expertise strongly shapes advanced residential and district-scale innovation. The company highlights that CHP can help users save nearly 40% of fuel compared with separate heat and electricity generation.

Axiom Energy Group has built a strong position in the residential and light commercial CHP space through its EcoPrime 4.4 kW micro-CHP system. The platform can generate 1.2 to 4.4 kWh electricity output while simultaneously producing 13,000 to 47,000 BTU/hr thermal energy, making it well suited for homes and small apartment buildings. Its focus on compact natural gas and propane-based systems supports homeowners seeking lower grid reliance and improved energy resilience.

Top Key Players Outlook

- Yanmar

- GE Power

- Samad Power

- Vaillant Group

- Axiom Energy Group

- Dalkia Aegis, EDF Group

- EC POWER A/S

- Micro Turbine Technology BV

- BDR Thermea Group

- Viessmann Manufacturing Company Inc.

Recent Industry Developments

Vaillant’s long-standing role in this space comes from its early move into residential micro-CHP, including the ecoPOWER 1.0 system for small homes, while its wider CHP range historically extended from 1 kW to 20 kW for residential and light building use.

GE Vernova reported USD 38.1 billion in revenue in 2025, with total orders of USD 59.3 billion, showing the financial strength behind its power technology portfolio.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 9.1 Bn |

| Forecast Revenue (2035) | USD 15.0 Bn |

| CAGR (2026-2035) | 5.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Capacity (Upto 2kW, 3 kW to 10 kW, 11 kW to 50 kW), By Fuel (Natural Gas, Hydrogen, Renewable Resources), By Prime Mover (Gas Turbine, Steam Turbine, Reciprocating Engine, Fuel Cell, Microturbine) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Yanmar, GE Power, Samad Power, Vaillant Group, Axiom Energy Group, Dalkia Aegis, EDF Group, EC POWER A/S, Micro Turbine Technology BV, BDR Thermea Group, Viessmann Manufacturing Company Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |