Quick Navigation

- Report Overview

- Key Takeaways

- Equipment Type Analysis

- Service Type Analysis

- Equipment Size and Capacity Analysis

- Rental Engagement Model Analysis

- End-User Analysis

- Key Market Segments

- Emerging Trends

- Drivers

- Restraints

- Growth Factors

- Regional Analysis

- Key Regions and Countries

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

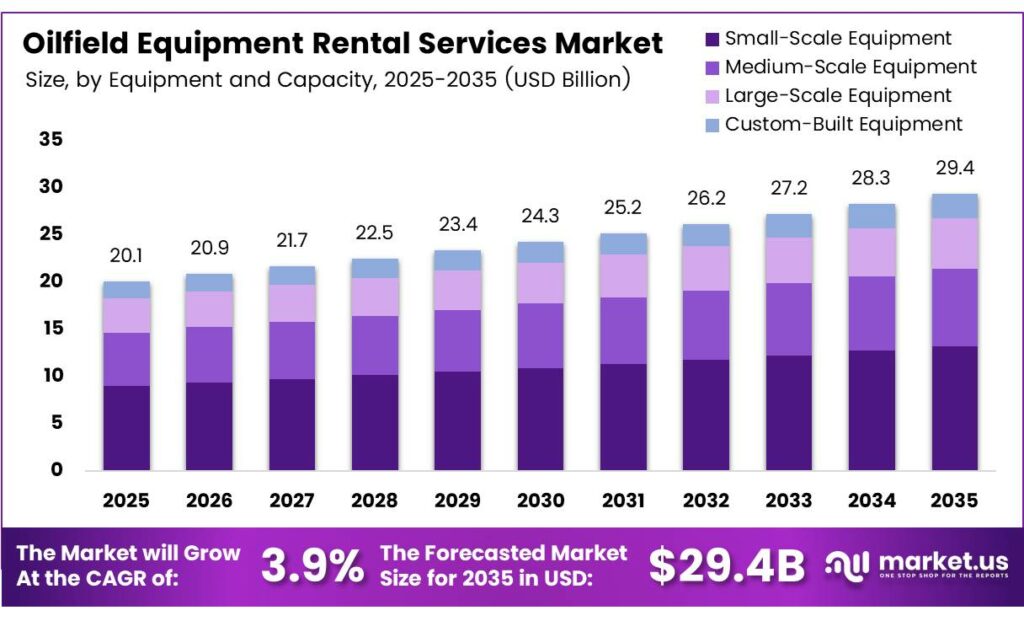

The Global Oilfield Equipment Rental Services Market size is expected to be worth around USD 29.4 billion by 2035 from USD 20.1 billion in 2025, growing at a CAGR of 3.9% during the forecast period 2026 to 2035.

The oilfield equipment rental services market provides exploration and production companies with access to critical drilling, completion, and production equipment without large capital commitments. Companies rent assets such as drilling rigs, wellheads, and pumping systems on flexible terms. This model reduces financial risk and supports faster project deployment across upstream oil and gas operations.

Global offshore marketed rig committed utilization for the full-year 2025 reached 89%, with jackup utilization at 90.9% and drillships at 87.8%. These indicate robust equipment demand and confirm that rental fleets are operating near peak capacity, which supports sustained revenue growth for service providers through 2035.

The market benefits from a clear structural shift in how operators manage capital. Exploration and production companies increasingly prefer operating expenditure models over heavy capital outlays. Active Mobile Offshore Drilling Units reached 502, with utilization at 80% — the second highest since 2014 — confirming strong demand for rental assets in offshore drilling activities.

Key Takeaways

- The Global Oilfield Equipment Rental Services Market is valued at USD 20.1 billion in 2025 and is projected to reach USD 29.4 billion by 2035, growing at a CAGR of 3.9%.

- Drilling Equipment leads with a 31.8% market share.

- Long-Term Rentals dominate with a 42.6% share.

- Medium-Scale Equipment holds a 36.3% share.

- Direct Rental Agreements hold the largest share at 44.9%.

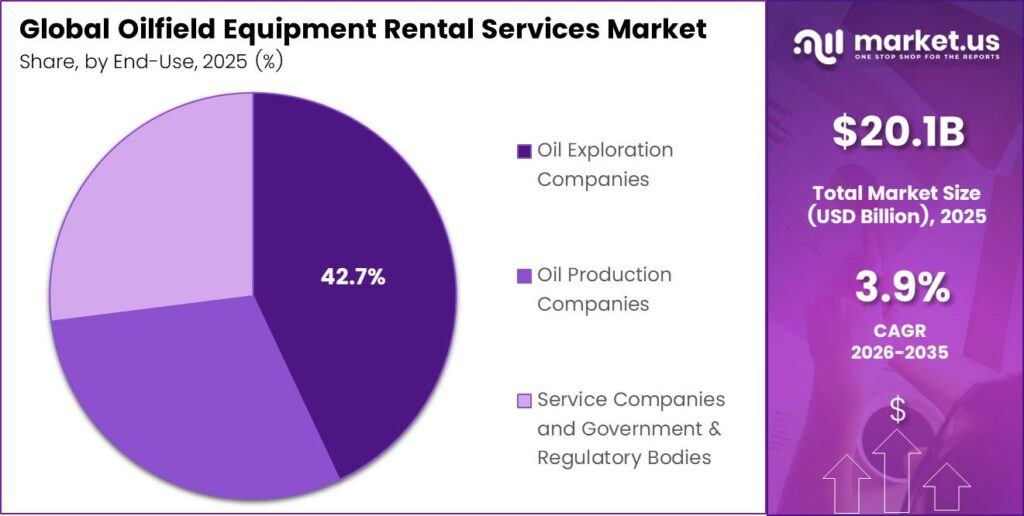

- Oil Exploration Companies account for 42.7% of the total market demand.

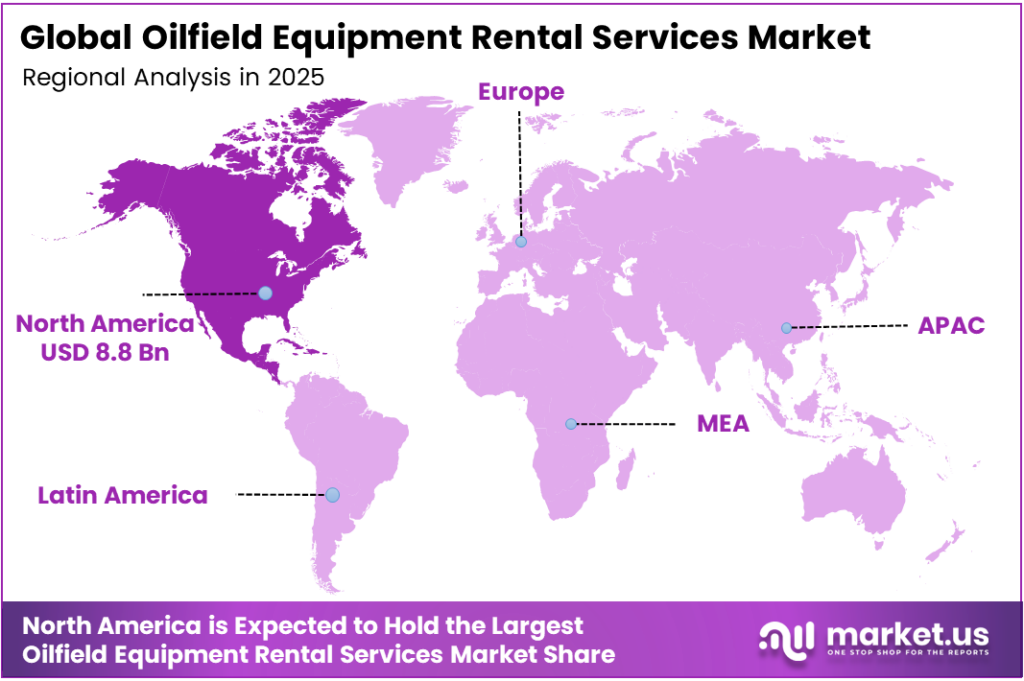

- North America is the dominant region with a 42.4% share, valued at USD 8.8 billion.

Equipment Type Analysis

Drilling Equipment dominates with 31.8% due to its critical role in upstream oil and gas exploration activities.

In 2025, Drilling Equipment held a dominant market position in the By Equipment Type segment of the Oilfield Equipment Rental Services Market, with a 31.8% share. Drilling rigs, rotary systems, and downhole tools represent the highest-demand rental assets. Operators prefer renting over owning as drilling programs vary in duration and location, making flexible access to high-spec drilling systems commercially essential.

Completion Equipment supports the final stage of well preparation, including perforating guns, packers, and wellhead systems. Consequently, rental demand for completion assets grows alongside drilling activity levels. Operators renting completion tools benefit from access to the latest technology without capital investment, improving well productivity and reducing time-to-production across both onshore and offshore projects.

Service Type Analysis

Long-Term Rentals dominate with 42.6% due to operator preference for cost predictability and supply continuity.

In 2025, Long-Term Rentals held a dominant market position in the By Service Type segment of the Oilfield Equipment Rental Services Market, with a 42.6% share. Operators engaged in multi-year drilling programs and sustained production campaigns favor long-term agreements to secure equipment availability and lock in favorable pricing. This model also reduces procurement complexity across extended project timelines.

Short-Term Rentals serve operators managing seasonal drilling campaigns, well testing, or emergency equipment requirements. Consequently, this segment attracts smaller operators and independent producers who require flexibility without long-term commitments. Rent-to-Own Options appeal to companies transitioning from rental to ownership, allowing gradual capital deployment while maintaining immediate equipment access throughout the contract duration.

Maintenance and Repair Services represent a high-value add-on that rental providers increasingly bundle with equipment agreements. Operators benefit from guaranteed uptime and reduced internal workforce requirements. Moreover, comprehensive maintenance contracts reduce the total cost of ownership for lessees and create recurring revenue streams for rental companies, strengthening long-term client relationships across the upstream oil and gas sector.

Equipment Size and Capacity Analysis

Medium-Scale Equipment dominates with 36.3% due to its versatile application across onshore and shallow offshore operations.

In 2025, Medium-Scale Equipment held a dominant market position in the By Equipment Size and Capacity segment of the Oilfield Equipment Rental Services Market, with a 36.3% share. This category includes mid-range drilling rigs, pumping systems, and handling equipment suitable for conventional onshore wells and shallow water platforms. Operators prefer medium-scale units for their balance of performance, mobility, and rental cost efficiency.

Small-Scale Equipment serves independent producers, workover operations, and early-stage exploration projects with limited infrastructure. Consequently, this category supports a large base of small and mid-size operators across emerging production regions. Large-Scale Equipment covers deepwater rigs, high-pressure drilling systems, and heavy lifting assets used in complex offshore and unconventional resource programs, where specialized capability justifies higher rental rates.

Rental Engagement Model Analysis

Direct Rental Agreements dominate with 44.9% due to their simplicity and direct cost transparency for operators.

In 2025, Direct Rental Agreements held a dominant market position in the By Rental Engagement Model segment of the Oilfield Equipment Rental Services Market, with a 44.9% share. This model allows operators to negotiate terms directly with equipment providers, enabling flexibility in contract duration, asset selection, and pricing. Consequently, direct agreements remain the preferred choice across independent and large-scale exploration programs globally.

Consortium and Government Contracts support large national oil company programs and multi-operator field developments where shared rental arrangements reduce individual capital exposure. Fleet Management Services allow operators to outsource complete equipment lifecycle management, from procurement to maintenance and retirement. Therefore, this model appeals to operators seeking to streamline vendor relationships and reduce operational complexity across multi-asset projects.

End-User Analysis

Oil Exploration Companies dominate with 42.7% due to their consistent demand for high-spec drilling and completion equipment.

In 2025, Oil Exploration Companies held a dominant market position in the By End-User segment of the Oilfield Equipment Rental Services Market, with a 42.7% share. Exploration firms drive the highest rental volumes as they require diverse equipment across varying project stages and geographies. Moreover, renting equipment allows exploration companies to match asset deployment precisely with project timelines without permanent capital commitments.

Oil Production Companies represent a stable and growing end-user segment that requires long-duration rentals for production and workover equipment. These firms prioritize equipment reliability and integrated maintenance services to sustain consistent output levels. Consequently, rental providers that offer bundled production support solutions capture significant long-term revenue from producing field operators seeking to minimize downtime.

Service Companies, Government, and Regulatory Bodies collectively form the third major end-user category. Oilfield service firms rent specialized equipment to fulfill contracts across multiple client sites, while government bodies and national oil companies use rental agreements for state-managed exploration programs. Therefore, this end-user segment supports diversified demand streams that help rental providers sustain consistent fleet utilization across regional market cycles.

Key Market Segments

By Equipment Type

- Drilling Equipment

- Completion Equipment

- Production Equipment

- Workover Equipment

- Auxiliary Equipment

By Service Type

- Long-Term Rentals

- Short-Term Rentals

- Rent-to-Own Options

- Maintenance and Repair Services

By Equipment Size and Capacity

- Small-Scale Equipment

- Medium-Scale Equipment

- Large-Scale Equipment

- Custom-Built Equipment

By Rental Engagement Model

- Direct Rental Agreements

- Consortium and Government Contracts

- Fleet Management Services

- Service Level Agreements (SLAs)

By End-User

- Oil Exploration Companies

- Oil Production Companies

- Service Companies, Government, and Regulatory Bodies

Emerging Trends

IoT and AI Drive Real-Time Equipment Monitoring Across Rental Fleets

Rental service providers increasingly integrate IoT sensors and AI-driven analytics into their equipment fleets. These technologies enable real-time remote monitoring, automated performance alerts, and predictive diagnostics. Approximately 48% of oilfield rental service providers have already integrated digital monitoring systems, delivering measurable improvements in efficiency and asset management. Additionally, electric fracturing systems now reduce CO2 emissions by up to 74% compared to diesel fleets, signaling a clear shift toward cleaner rental solutions.

Asset-Light Models and Customized Equipment Shape the Future Rental Landscape

Operators across the energy sector increasingly adopt asset-light strategies, preferring flexible rental models over direct equipment ownership. This shift accelerates demand for customized, high-specification rental assets designed for complex well interventions and deepwater environments. Moreover, the ongoing energy transition encourages providers to offer modular, adaptable equipment configurations. Consequently, rental companies that combine technical customization with flexible engagement models gain a measurable competitive advantage in high-growth upstream markets.

Drivers

Strategic CAPEX-to-OPEX Shift Accelerates Oilfield Equipment Rental Adoption

Exploration and production companies increasingly prefer renting over owning oilfield equipment to reduce capital exposure and maintain financial flexibility. This structural shift from capital expenditure to operating expenditure models directly drives rental service demand. Moreover, industry data confirms that average jackup contract lengths rose to 829 days in the first half of 2025 — 34% higher than in 2024 — reflecting stronger operator commitment to securing long-term rental capacity across offshore drilling programs.

Deepwater Exploration and Rising Global E&P Investments Fuel Equipment Demand

Rising global investments in oil and gas exploration and production activities expand the addressable market for rental service providers. Deepwater and ultra-deepwater programs require highly specialized equipment that most operators cannot justify purchasing outright. Additionally, industry analysis shows that in-house maintenance of sophisticated offshore handling systems costs 40% more than comprehensive rental agreements that include maintenance. Therefore, rental arrangements deliver clear financial advantages that drive continued market adoption across complex drilling environments.

Restraints

Crude Oil Price Volatility Creates Unpredictable Demand Cycles for Rental Providers

Global crude oil price fluctuations directly impact exploration and production budgets, causing operators to adjust or defer equipment rental plans rapidly. Rental service providers face revenue uncertainty during price downturns as operators reduce drilling activity and return leased assets early. Oil and gas operators using hybrid rental strategies have reported cost reductions of up to 25%, yet price volatility remains a persistent structural risk that limits long-term contract commitments from budget-sensitive operators.

Environmental Regulations Increase Compliance Costs for Rental Equipment Operations

Stringent environmental regulations across key markets require rental equipment to meet increasingly demanding emissions, waste handling, and operational safety standards. Providers must invest in equipment upgrades, certification programs, and compliance monitoring to meet evolving regulatory requirements. Moreover, these compliance costs reduce profit margins and raise barriers to entry for smaller rental providers.

Growth Factors

Shale Development and Offshore Expansion Create New Rental Market Opportunities

Shale gas and tight oil programs require specialized, rapidly deployable equipment that rental models deliver efficiently. Operators developing new offshore frontiers in West Africa, Southeast Asia, and Latin America similarly rely on rental solutions to access high-spec assets without permanent capital commitment. Implementing predictive maintenance in oil and gas operations results in a 30% reduction in maintenance costs and a 70% elimination of equipment breakdowns, making tech-enabled rental fleets an increasingly attractive value proposition for operators worldwide.

Digital Technologies and Emerging Market Penetration Accelerate Fleet Revenue Growth

Growing adoption of digital and IoT-enabled equipment within rental fleets enhances operational value and supports premium pricing strategies. AI adoption supports a 20% increase in operational efficiency for oil and gas companies integrating digital technologies into oilfield operations. Additionally, well-managed rental equipment fleets typically achieve 75%–90% utilization rates, with a 5% increase in utilization generating approximately 20% revenue uplift.

Regional Analysis

North America Dominates the Oilfield Equipment Rental Services Market with a Market Share of 42.4%, Valued at USD 8.8 Billion

North America leads the global oilfield equipment rental services market, holding a 42.4% share valued at approximately USD 8.8 billion in 2025. The United States drives this dominance through active shale oil and gas programs in the Permian Basin, Eagle Ford, and Bakken formations. Moreover, deepwater Gulf of Mexico projects sustain a strong demand for high-specification drilling and completion rental equipment across the region.

Europe maintains a steady market presence driven by North Sea exploration and production activity in the UK, Norway, and the Netherlands. Operators in this region favor rental solutions to manage aging asset replacement costs and meet strict offshore safety regulations. Additionally, the energy transition push in Europe encourages investment in cleaner, technologically advanced rental equipment for ongoing extraction operations.

Asia Pacific represents one of the fastest-growing regions for oilfield equipment rental services, supported by expanding upstream activity in China, India, Australia, and Southeast Asia. National oil companies across the region are increasing exploration budgets, creating fresh rental demand for both onshore and offshore assets. Consequently, foreign rental service providers are actively expanding operations and forming local partnerships to capture this high-growth opportunity.

Latin America offers significant growth potential driven by offshore pre-salt exploration in Brazil and upstream investment expansion across Mexico, Argentina, and Colombia. Operators in the region increasingly adopt rental models to accelerate project execution while managing capital constraints. Therefore, rental service providers targeting Latin America can leverage growing E&P activity and improving regulatory environments to establish long-term market positions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Schlumberger (now rebranded as SLB) operates as one of the largest oilfield technology and services companies globally, offering an extensive rental equipment portfolio spanning drilling, completion, and production systems. The company integrates digital solutions across its rental operations, enabling clients to access real-time performance data. Consequently, SLB’s technology-first approach differentiates its rental offering from conventional asset-only providers in both onshore and offshore markets.

Baker Hughes delivers integrated oilfield equipment rental services across drilling, evaluation, and completion segments, supported by strong manufacturing and digital capabilities. The company’s Oilfield Services and Equipment division consistently improves operational efficiency through technology-enabled asset management. Reflecting sustained performance strength across its equipment services business.

Halliburton is a leading provider of oilfield services and rental equipment, serving exploration and production companies across more than 70 countries. The company offers a comprehensive range of rental solutions, including pressure control, wellbore intervention, and production equipment. Moreover, Halliburton’s global logistics infrastructure supports rapid equipment mobilization in remote and offshore environments, making it a preferred partner for large-scale, time-sensitive drilling programs worldwide.

Weatherford International provides specialized oilfield equipment rental services with a focus on well construction, completion, and production solutions. The company has restructured its operations to concentrate on high-margin rental and service segments. Additionally, Weatherford invests in digital monitoring and automation technologies to enhance fleet performance and reduce client downtime. Therefore, its technologically upgraded rental portfolio positions the company competitively in premium deepwater and unconventional resource markets globally.

Top Key Players in the Market

- Schlumberger

- Baker Hughes

- Halliburton

- Weatherford International

- Transocean

- Seadrill

- Superior Energy Services

- Oil States International

- Noble Corporation

- Valaris

Recent Developments

- In 2025, SLB OneSubsea signed a collaboration agreement with Subsea7 and PETRONAS Suriname for asset development; SLB also completed the dissolution of the Sensia joint venture with Rockwell Automation (digital/automation solutions for oilfield operations). SLB OneSubsea entered an agreement to acquire the subsea business of Envirex Group AS (Norway), strengthening its subsea equipment and services portfolio.

- In 2025, Baker Hughes secured a strategic gas technology order supporting Argentina’s gas expansion (equipment and technology for gas operations). Announced strategic collaboration with XGS Energy to advance geothermal energy (transferable technologies for well equipment and services).

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 20.1 Billion |

| Forecast Revenue (2035) | USD 29.4 Billion |

| CAGR (2026-2035) | 3.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Equipment Type (Drilling Equipment, Completion Equipment, Production Equipment, Workover Equipment, Auxiliary Equipment), By Service Type (Long-Term Rentals, Short-Term Rentals, Rent-to-Own Options, Maintenance and Repair Services), By Equipment Size and Capacity (Small-Scale Equipment, Medium-Scale Equipment, Large-Scale Equipment, Custom-Built Equipment), By Rental Engagement Model (Direct Rental Agreements, Consortium and Government Contracts, Fleet Management Services, Service Level Agreements (SLAs)), By End-User (Oil Exploration Companies, Oil Production Companies, Service Companies and Government and Regulatory Bodies) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Schlumberger, Baker Hughes, Halliburton, Weatherford International, Transocean, Seadrill, Superior Energy Services, Oil States International, Noble Corporation, Valaris |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |