Quick Navigation

Report Overview

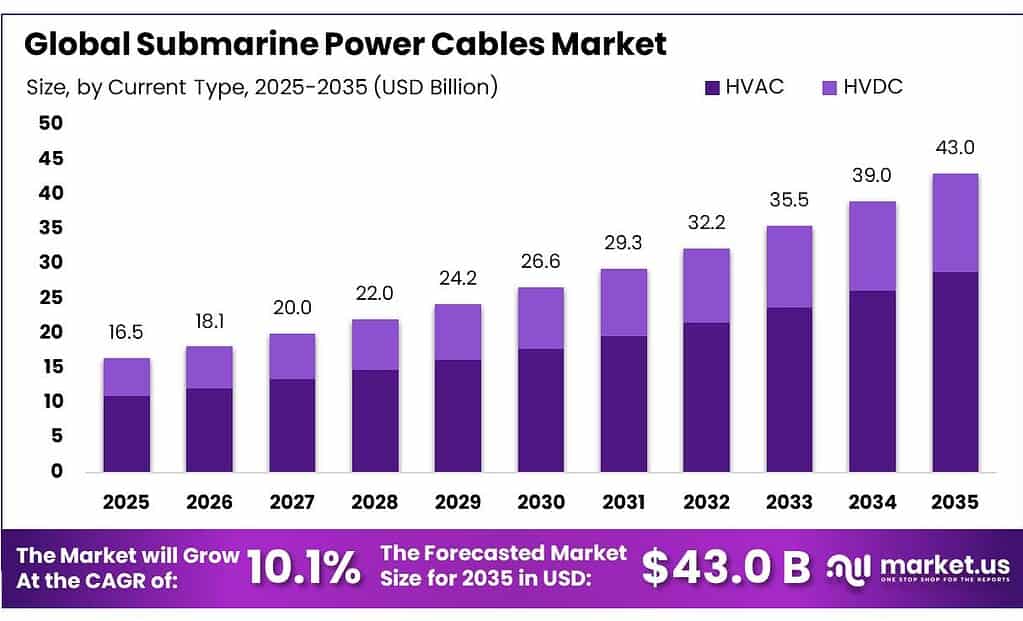

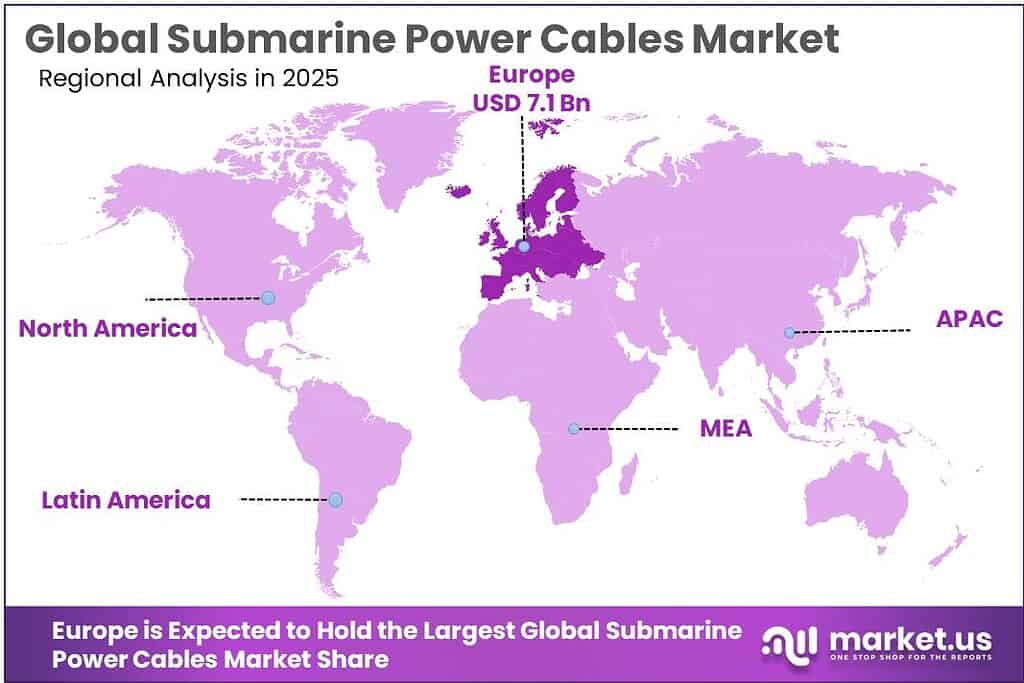

The Global Submarine Power Cables Market size is expected to be worth around USD 43.0 Billion by 2035, from USD 16.5 Billion in 2025, growing at a CAGR of 10.1% during the forecast period from 2026 to 2035. In 2025, Europe held a dominant market position, capturing more than a 43.4% share, holding USD 7.1 Billion revenue.

Submarine power cables are a strategic transmission asset for modern power systems because they connect offshore wind farms, islands, and cross-border grids where overhead lines are impractical or politically difficult. The industrial profile is moving from niche interconnection infrastructure toward a core enabler of energy transition investment.

This shift is visible in offshore wind alone: global offshore wind capacity reached 79.4 GW in 2024, while total wind capacity reached 1,131 GW, confirming that offshore generation is becoming large enough to require sustained submarine export-cable and interconnector build-out. Offshore wind costs also remain structurally more competitive than a decade ago, with the global weighted-average offshore wind LCOE falling to USD 0.079/kWh in 2024 from USD 0.208/kWh in 2010.

The current industrial scenario is defined by three demand clusters. First, offshore wind grid connection is scaling quickly. The European Commission’s offshore renewables strategy targets an increase in Europe’s offshore wind capacity from 12 GW to at least 60 GW by 2030 and 300 GW by 2050, while the North Seas Energy Cooperation countries agreed on 120 GW by 2030 and at least 300 GW by 2050 for the North Sea basin alone.

Second, grid-security policy is supporting more subsea interconnection: the EU interconnection target is at least 15% by 2030. Third, national reform programs are raising project visibility; for example, the UK stated in February 2025 that it already had 30.7 GW of offshore wind installed or committed, plus 7.2 GW consented, against a 43 GW to 50 GW clean-power requirement for 2030.

The main driving factors are therefore clear: renewable integration, energy security, and long-distance efficiency. HVDC submarine systems are particularly favored for long routes because transmission losses are materially lower than AC on long-distance, high-capacity links. That policy pull is increasingly supported by public funding.

Under the EU’s Connecting Europe Facility, the energy program for 2021-2027 allocates €5.8 billion to the sector, and the 2025 call alone made €600 million available for eligible cross-border infrastructure projects.

The expansion outlook remains strong even with recent auction and cost pressure: the IEA expects offshore wind capacity expansion to reach 140 GW over the forecast period, with the annual offshore wind market rising from 9.2 GW in 2024 to more than 37 GW by 2030; Europe’s annual market is expected to approach 14.6 GW by 2030.

Key Takeaways

- Submarine Power Cables Market size is expected to be worth around USD 43.0 Billion by 2035, from USD 16.5 Billion in 2025, growing at a CAGR of 10.1%,

- HVAC held a dominant market position, capturing more than a 67.2% share.

- Medium Voltage (≤ 66 kV) held a dominant market position, capturing more than a 45.8% share.

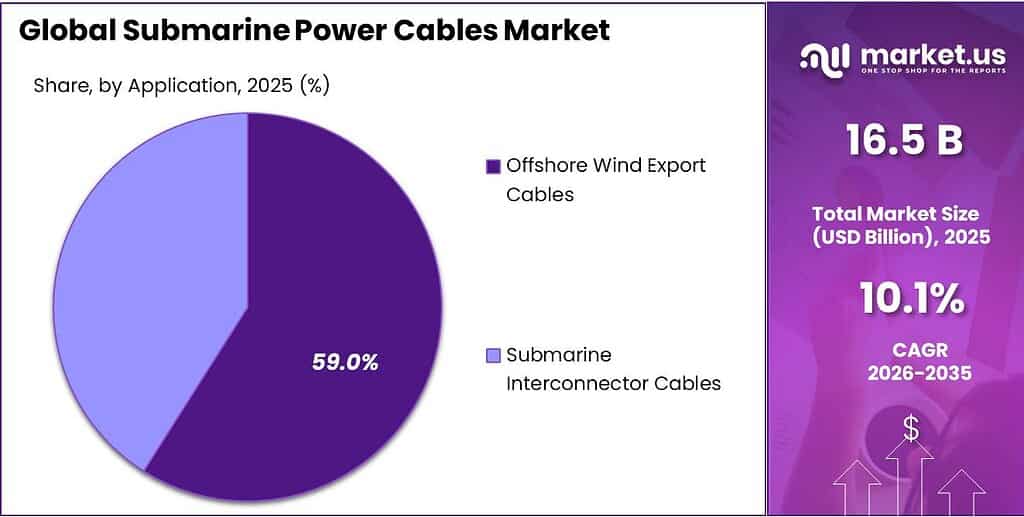

- Offshore Wind Export Cables held a dominant market position, capturing more than a 59.6% share.

- Europe held the dominant position in the submarine power cables market, accounting for 43.4% of the global share and valued at USD 7.1 billion.

By Current Type Analysis

HVAC leads the submarine power cables market with a strong 67.2% share in 2025, supported by its wide use in long-distance offshore transmission.

In 2025, HVAC held a dominant market position, capturing more than a 67.2% share. This strong position was mainly supported by its continued use in submarine power cable projects that require reliable transmission across offshore wind farms, island connections, and cross-border electricity links. HVAC systems remain a preferred choice in many large-scale installations because they are well understood, widely deployed, and easier to integrate with existing grid infrastructure.

By Voltage Analysis

Medium Voltage (≤ 66 kV) dominates with a 45.8% share in 2025, driven by its strong fit for offshore wind array links and short-distance marine connections.

In 2025, Medium Voltage (≤ 66 kV) held a dominant market position, capturing more than a 45.8% share. This segment maintained its leadership due to its extensive use in offshore wind farm inter-array cable systems, nearshore renewable projects, and short-distance submarine connections where efficient and stable power transfer is essential. Medium voltage cables are widely preferred for linking turbines within offshore wind installations and for connecting smaller islands, coastal facilities, and marine infrastructure to nearby grids.

By Application Analysis

Offshore Wind Export Cables dominate with a 59.6% share in 2025, supported by rising offshore wind grid connection projects worldwide.

In 2025, Offshore Wind Export Cables held a dominant market position, capturing more than a 59.6% share. This leading share was largely driven by the rapid expansion of offshore wind farms and the growing need to transmit generated electricity from offshore sites to onshore substations efficiently. These cables play a critical role in connecting large-scale offshore renewable projects to mainland grids, making them a key part of energy transition investments across coastal regions.

Key Market Segments

By Current Type

- HVAC

- HVDC

By Voltage

- Medium Voltage (≤ 66 kV)

- High Voltage (66-220 kV)

- Extra High Voltage (> 220 kV)

By Application

- Offshore Wind Export Cables

- Submarine Interconnector Cables

Emerging Trends

Shift toward 525 kV HVDC and long-distance offshore links is the latest trend shaping submarine power cables

One of the most important latest trends in the submarine power cables market is the fast shift toward 525 kV HVDC XLPE cable systems for large offshore wind and cross-border transmission projects. A strong example is the Netherlands offshore wind expansion, where around 1,700 km of 525 kV HVDC submarine cable is being deployed for a 6 GW offshore wind connection program, making it one of the largest projects of its kind.

This clearly shows how utilities are now prioritizing fewer but higher-capacity cable corridors to improve project efficiency. The same trend is also visible in Europe’s long-term energy roadmap, where studies estimate 140,000 km of additional HVDC cables may be required by 2050 to support renewable integration and interconnector growth.

Offshore wind mega-hubs and multi-terminal grids are becoming the new cable design trend

Another clear latest trend is the rise of multi-terminal offshore grids and mega-hub wind zones, where one submarine cable network serves multiple wind farms and national grids at the same time. This is changing the way submarine power cables are designed, with greater focus on converter compatibility, multi-point routing, and advanced protection systems.

Governments and transmission operators are supporting this trend because shared offshore hubs reduce seabed congestion and improve regional power balancing. In the UK, the first 2 GW 525 kV XLPE HVDC submarine interconnection route under Eastern Green Link reflects how this design trend is already moving into large-scale deployment.

Drivers

Rising offshore wind installations are creating strong demand for submarine power cables

One of the biggest driving factors for the submarine power cables market is the fast expansion of offshore wind energy projects across major coastal economies. Every new offshore wind farm needs a strong network of inter-array and export cables to move electricity from turbines at sea to onshore substations, making submarine power cables a direct infrastructure requirement rather than an optional component.

In 2025, this demand became even stronger as global wind installations reached 117 GW in a record year, according to the Global Wind Energy Council. At the same time, the International Energy Agency noted that global renewable power capacity is expected to rise by 4,600 GW between 2025 and 2030, creating large-scale transmission needs for offshore and cross-border marine projects.

Government-backed interconnector projects are accelerating long-distance cable deployment

Another major growth driver is the sharp rise in government-supported cross-border power interconnectors and national grid modernization plans. These projects rely heavily on submarine power cables to improve energy security, connect renewable-rich coastal regions, and reduce dependence on fossil-fuel imports.

A strong example is Great Britain, where operating and under-construction interconnector capacity already stands at 11.7 GW, with approved projects expected to increase this to 18 GW by 2032. In Europe, the North Sea energy partnership has gone even further, with 10 countries planning a shared offshore grid system targeting 100 GW of offshore wind-linked capacity by 2040.

Restraints

Complex permitting and seabed compliance delays are a major restraint for submarine power cable projects

One of the biggest restraining factors for the submarine power cables market is the long and highly complex permitting process linked to seabed use, environmental clearances, and marine route approvals. Before a cable can be laid, developers often need consent from multiple agencies covering fisheries, shipping lanes, coastal authorities, and environmental regulators.

This creates long approval cycles that can slow project execution and increase financing pressure. A clear example comes from the offshore wind industry, where the Global Wind Energy Council reported that 410 GW of offshore wind capacity is currently in different stages of development globally, and a significant share of these projects faces timeline pressure from permitting and grid connection bottlenecks.

Rising route complexity and protection requirements are pushing project costs higher

Another major restraint is the growing technical difficulty of cable routing across busy and environmentally sensitive seabeds. Modern submarine power cables must avoid shipping anchors, fishing zones, rocky seabeds, protected ecosystems, and even historical wreck sites, which makes route engineering more time-consuming and expensive.

If the route passes through hard rock or unstable seabeds, developers may need additional trenching, armoring, or rerouting work, sharply increasing total installation costs. Trusted industry body ICPC also highlighted that its membership grew from 218 members in 2024 to 245 members in 2025, reflecting the rising global focus on cable protection and seabed coexistence standards.

Opportunity

Cross-border offshore interconnectors are opening the biggest growth opportunity for submarine power cables

One of the strongest growth opportunities for the submarine power cables market is the rapid development of cross-border offshore grids and interconnector networks. Countries are no longer building offshore renewable projects only for domestic use; they are increasingly planning shared marine transmission systems that connect multiple nations.

This creates long-distance demand for high-capacity submarine power cables, especially for offshore wind evacuation and cross-border electricity trade. A major example is Europe’s offshore grid roadmap, where the European Union is targeting up to 365 GW of offshore renewable capacity by 2050, creating a huge long-term need for submarine export and interconnector cables.

Government-backed energy corridor projects are creating long-term project pipelines

Another major opportunity is the rise of government-supported energy corridor programs connecting islands, coastal regions, and neighboring countries. These initiatives are backed by energy security goals, renewable integration plans, and international financing support, which reduces project risk and speeds up deployment.

In parallel, trusted global energy agencies highlight that transmission expansion is becoming one of the most critical investment themes of the clean energy transition. The International Energy Agency notes that global grid modernization and expansion needs are accelerating, especially for lines above 66 kV, directly supporting demand for submarine high-voltage systems used in marine corridors and offshore renewable links.

Regional Insights

Europe dominates the submarine power cables market with 43.4% share, reaching USD 7.1 Bn, driven by offshore wind and cross-border grid expansion.

Europe held the dominant position in the submarine power cables market, accounting for 43.4% of the global share and valued at USD 7.1 billion. The region’s leadership is strongly supported by its mature offshore wind ecosystem, extensive subsea interconnector network, and aggressive clean energy transition goals.

Europe remains the global center for offshore renewable transmission, with the region continuing to lead in cross-border electricity trading infrastructure and marine grid resilience programs. Recent industry estimates also show Europe remains the largest regional contributor in 2025, supported by the strongest concentration of offshore wind export cable deployments worldwide.

A major support factor behind this regional dominance is the rapid scale-up of North Sea offshore grid plans. In 2026, ten European countries signed an agreement to jointly develop 100 GW of offshore wind capacity in shared waters, creating substantial future demand for submarine export and bidirectional interconnector cables. In addition, long-term technical studies indicate that Europe may require around 140,000 km of additional HVDC cable installations by 2050, reflecting the scale of future subsea transmission needs across offshore wind hubs and international power corridors.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ABB remains a strong technology-led player in submarine power cables, especially in HVDC converter systems and offshore grid integration, where numerical performance matters most. The company’s strength is visible in projects supporting 320 kV to 525 kV HVDC links, which are widely used for long-distance subsea transmission. Its role in offshore wind grid connections and interconnector substations supports high-capacity transmission projects often exceeding 1 GW to 2 GW per link.

Furukawa Electric holds a notable position in the submarine power cables market through its strong manufacturing base and high-voltage cable engineering expertise. The company is widely recognized for supplying 66 kV, 132 kV, and above 220 kV class submarine cable systems for island grids and offshore renewable connections. Numerical strength in its business comes from long route execution capability, where projects often extend beyond 50 km to 100 km depending on marine terrain.

Hengtong Group is one of the fastest-scaling Asian players in submarine power cable manufacturing, supported by large production volumes and offshore project execution capabilities. The company is increasingly active in 220 kV and 500 kV submarine cable projects, especially for offshore wind and inter-country energy transmission. Its numerical edge comes from expanding annual high-voltage cable output capacity measured in thousands of kilometers, allowing it to support large utility tenders and marine renewable corridors.

Top Key Players Outlook

- ABB

- Furukawa Electric

- Hengtong Group

- LS Cable & System

- Nexans

- NKT

- Prysmian Group

- Sumitomo Electric Industries

- TFKable

- ZTT Group

Recent Industry Developments

In 2025, Furukawa Electric strengthened its position in the submarine power cables sector by moving more clearly into the high-voltage offshore transmission space. In October 2025, the company approved about JPY 100.0 billion in capital spending to build out 500 kV-class HVDC cable production, which is the highest voltage class mentioned in its plan, with a targeted production capacity of 200 km per year.

In August 2025, Hengtong Group highlighted delivery and installation for the Bohai Bay project, which included 37 km of 220 kV offshore export cable and 80 km of inter-array cable, showing its strength in complete marine cable execution.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 16.5 Bn |

| Forecast Revenue (2035) | USD 43.0 Bn |

| CAGR (2026-2035) | 10.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Current Type (HVAC, HVDC), By Voltage (Medium Voltage (≤ 66 kV), High Voltage (66-220 kV), Extra High Voltage (> 220 kV)), By Application (Offshore Wind Export Cables, Submarine Interconnector Cables) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ABB, Furukawa Electric, Hengtong Group, LS Cable & System, Nexans, NKT, Prysmian Group, Sumitomo Electric Industries, TFKable, ZTT Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |