Quick Navigation

Report Overview

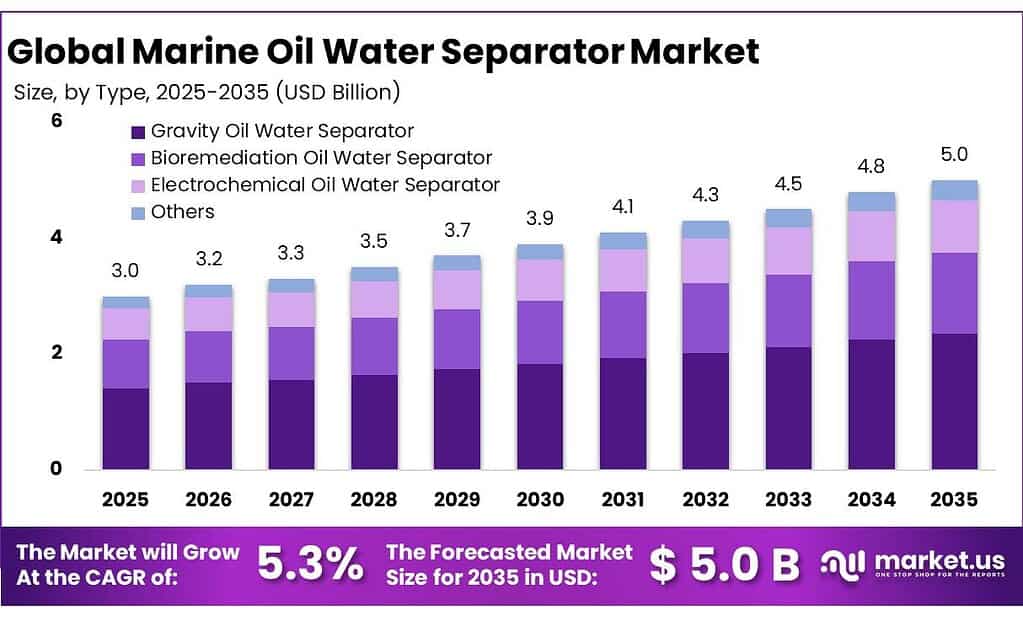

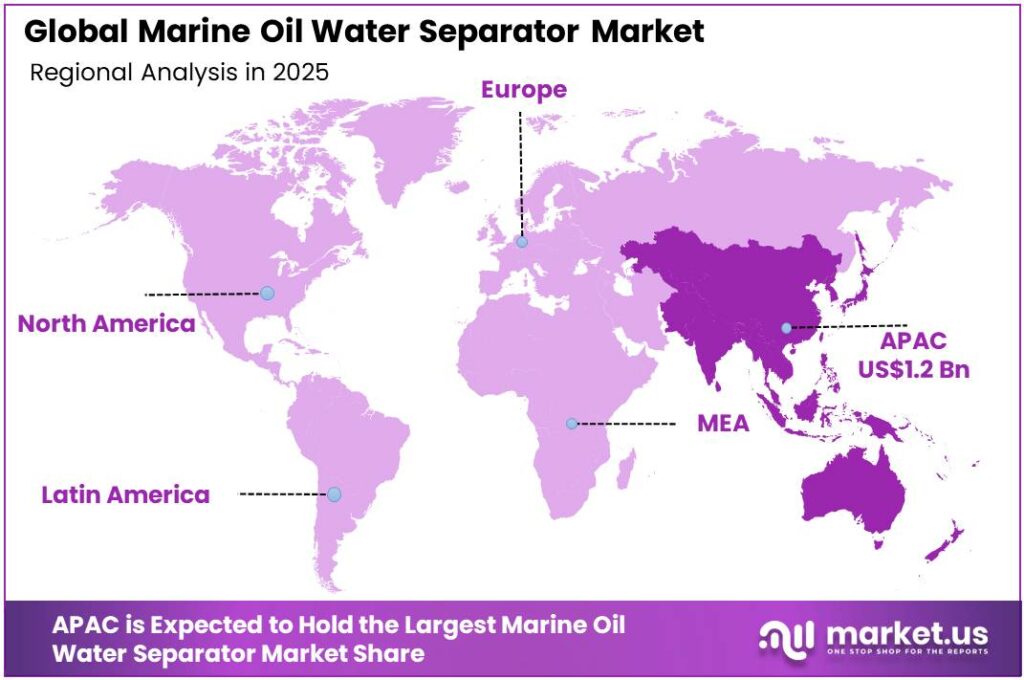

The Global Marine Oil Water Separator Market size is expected to be worth around USD 5.0 Billion by 2035, from USD 3.0 Billion in 2025, growing at a CAGR of 5.3% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 42.5% share, holding USD 1.2 Billion revenue.

The marine oil water separator industry forms a mission-critical part of shipboard environmental compliance, because these systems treat oily bilge water before discharge and help vessels remain within international pollution limits. Under MARPOL Annex I, discharged effluent processed through approved oil filtering equipment must not exceed 15 parts per million (ppm) of oil, which keeps separator performance directly tied to regulatory enforcement and vessel operability.

The industrial scenario remains favorable because the addressable fleet is large and still expanding. UNCTAD reported that the global fleet stood at around 109,000 vessels of at least 100 gross tons at the start of 2024, while global maritime trade reached 12.3 billion tons in 2023, up 2.4% year on year. UNCTAD also projected maritime trade growth of 2% in 2024 and an average annual increase of 2.4% during 2025–2029. In practical terms, more vessel movements, longer voyages, and larger installed fleets support steady demand for compliant bilge-water treatment, replacement units, controls, filters, and retrofit services.

The main driving factors are regulatory tightening, harmonized enforcement, and operating-risk reduction. In U.S. waters, the EPA’s vessel discharge framework continues to govern oily bilgewater controls for commercial vessels, while Federal standards published in 2024 reaffirm that U.S. Coast Guard regulations enforce the 15 ppm discharge standard and require most seagoing ships to have an oily water separator. In another major compliance step, from 1 January 2025, new MARPOL special-area restrictions applied in the Red Sea and Gulf of Aden, raising the operational importance of separator performance and recordkeeping for ships of 400 gross tonnage and above.

Technology differentiation is increasingly centered on discharge assurance below the regulatory minimum. Compass Water Solutions states that its marine portfolio delivers continuous discharge of less than 5 ppm, below the conventional 15 ppm compliance ceiling, and notes more than 50 years of experience in water treatment. Its product pages also show compact marine units with 5 ppm monitoring capability and automatic membrane cleaning cycles that can restart within 30 minutes, signaling a market shift toward higher-performance, lower-operator-intervention systems for offshore and space-constrained vessels.

Key Takeaways

- Marine Oil Water Separator Market size is expected to be worth around USD 5.0 Billion by 2035, from USD 3.0 Billion in 2025, growing at a CAGR of 5.3%.

- Gravity Oil Water Separator held a dominant market position, capturing more than a 47.8% share.

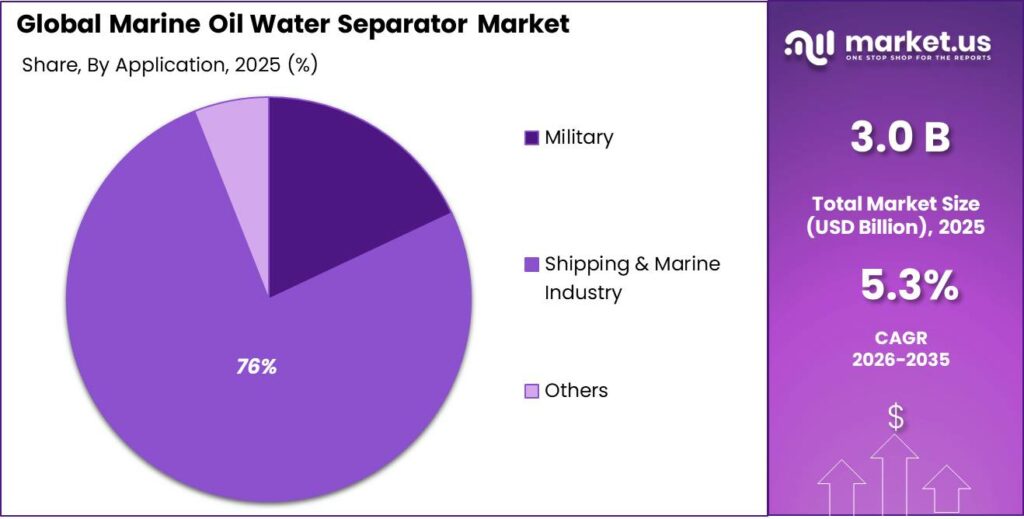

- Shipping & Marine Industry held a dominant market position, capturing more than a 76.4% share.

- Asia Pacific emerged as the leading regional market in the Marine Oil Water Separator industry, accounting for 42.5% of the global market, equivalent to nearly USD 1.2 Bn.

By Type Analysis

Gravity Oil Water Separator dominates with 47.8% thanks to its reliable performance and simple operating design.

In 2025, Gravity Oil Water Separator held a dominant market position, capturing more than a 47.8% share. This strong position was mainly supported by its wide use across marine vessels where dependable oil-water separation is essential for smooth engine room operations and regulatory compliance. Ship operators continued to prefer gravity-based systems because they offer a straightforward working mechanism, low maintenance needs, and consistent separation efficiency in routine marine applications.

By Application Analysis

Shipping & Marine Industry leads with 76.4% driven by rising vessel operations and strict marine discharge needs.

In 2025, Shipping & Marine Industry held a dominant market position, capturing more than a 76.4% share. This leading share was largely supported by the continuous demand for effective bilge water treatment systems across cargo ships, tankers, passenger vessels, offshore support ships, and naval fleets. The segment remained the largest consumer of marine oil water separators because these systems are a standard requirement for onboard wastewater management and environmental compliance. Growing global seaborne trade and steady fleet movement across international routes further strengthened product demand from the shipping sector during the year.

Key Market Segments

By Type

- Gravity Oil Water Separator

- Bioremediation Oil Water Separator

- Electrochemical Oil Water Separator

- Others

By Application

- Military

- Shipping & Marine Industry

- Others

Emerging Trends

Smart 15 ppm monitoring and digital compliance logging is the latest market trend

One of the most visible latest trends in the Marine Oil Water Separator market is the shift toward smart 15 ppm monitoring systems with digital data logging. Shipowners are no longer satisfied with only separating oil from bilge water; they now want systems that continuously record proof of compliance. The IMO continues to enforce the globally accepted 15 ppm discharge benchmark, and this requirement is pushing demand for separators integrated with oil content monitors, alarm history, automatic shutdown, and tamper-proof records.

A major reason behind this trend is the rise in port-state inspections and environmental audits, where digital records make it easier to demonstrate compliant discharge practices. Newer systems are also coming with 5-year certified monitoring cells, reducing calibration downtime and improving vessel uptime.

Hybrid separator designs with membrane and coalescer stages are gaining fast adoption

Another major trend is the growing preference for hybrid multi-stage oil water separators, especially systems that combine gravity plates, coalescers, fiber filtration, and membrane polishing. Traditional gravity-only units still remain common, but modern bilge mixtures now contain detergents, emulsified oils, and chemical residues that are harder to separate. Because of this, vessel operators are increasingly choosing advanced units designed to consistently discharge at 15 ppm or lower under varying load conditions.

This trend is especially strong in new shipbuilding and high-spec retrofit programs, where operators want future-ready systems that can pass stricter inspection checks without repeated manual intervention. Government-backed maritime compliance frameworks under MARPOL Annex I continue to support this shift, as ships must maintain reliable oily water discharge performance across global trade routes.

Drivers

Strict IMO discharge rules are pushing shipowners to install better oil water separators

One of the biggest drivers for the Marine Oil Water Separator market is the continued tightening of marine pollution rules under IMO’s MARPOL Annex I. The regulation makes oily water separators mandatory on ships above 400 gross tons, which directly supports steady equipment demand across commercial fleets. A major compliance benchmark remains the 15 ppm oil discharge limit, meaning ships can release bilge water only when oil concentration stays below this level.

This limit is closely monitored during port inspections, shipowners are investing in more reliable and easy-to-maintain separator systems. The International Maritime Organization also notes that oil tankers move around 2,900 million tonnes of crude oil and oil products every year by sea, which naturally increases the volume of bilge water and oily residues generated onboard.

Rising global seaborne oil movement is increasing bilge water treatment demand

Another strong growth driver comes from the sheer scale of oil transportation and engine-room wastewater generated by global shipping activity. With around 2,900 million tonnes of oil and petroleum products transported annually by sea, even a small rise in voyages creates a significant increase in oily bilge water volumes that must be treated before discharge.

Every vessel operating long-haul routes continuously produces machinery space bilge mixtures from fuel leaks, lubricants, wash water, and engine residue. Since MARPOL requires this water to remain below 15 ppm before discharge, ship operators are prioritizing advanced separation systems that reduce manual intervention and improve compliance accuracy.

Restraints

High retrofit and maintenance costs are slowing faster adoption across aging vessel fleets

One major restraining factor for the Marine Oil Water Separator market is the high cost of retrofitting and maintaining compliant systems on older ships. While MARPOL Annex I makes oily water separators mandatory for ships above 400 gross tons, many aging vessels still operate with outdated systems that struggle to consistently meet the 15 ppm discharge limit.

For shipowners, upgrading these systems is not only about buying the separator unit itself, but also involves pipeline changes, sensor upgrades, 15 ppm alarms, calibration modules, sludge handling modifications, and crew retraining. These added technical adjustments increase dry-docking time and raise total ownership cost. Annual verification requirements and 5-yearly cell renewal and calibration of 15 ppm monitoring equipment add another recurring expense layer for operators.

Older ships face performance issues with complex bilge mixtures, increasing operating burden

A second challenge comes from the poor performance of legacy separators when dealing with modern emulsified bilge water mixtures. Today’s ships use advanced lubricants, detergents, and fuel blends that create stable emulsions, making separation more difficult than traditional gravity systems were originally designed for. Although regulations still require discharge below 15 ppm, many older units need repeated filtration cycles, manual sludge removal, and frequent spare part replacement to stay compliant.

Opportunity

New shipbuilding and fleet modernization are creating strong replacement demand

One major growth opportunity for the Marine Oil Water Separator market is the steady expansion of the global commercial fleet and new shipbuilding activity. As more vessels enter service, every ship requires certified oily bilge water treatment systems that comply with the 15 ppm discharge standard under MARPOL Annex I. The International Maritime Organization notes that around 2,900 million tonnes of crude oil and oil products are transported by sea every year, showing the massive scale of marine operations that continuously generate oily wastewater onboard.

This directly opens long-term demand for new separator installations across cargo vessels, tankers, offshore support ships, and passenger fleets. A strong opportunity is also coming from fleet renewal, where older ships are being replaced by fuel-efficient and digitally monitored vessels. New-generation ships are increasingly integrating compact, automated separator systems with real-time discharge alarms, making advanced units more attractive than legacy equipment.

Digital compliance systems and smart monitoring upgrades open a premium opportunity

A second major opportunity is the shift toward smart marine monitoring and automated compliance technology. In 2025, the IMO highlighted a roadmap for digital transformation in shipping to improve efficiency, safety, and sustainability across global fleets. This trend is creating room for marine oil water separator suppliers to move beyond basic gravity separation and offer integrated solutions with sensors, data logging, remote diagnostics, and predictive maintenance support.

Regional Insights

Asia Pacific dominated the Marine Oil Water Separator market with a 42.5% share, valued at USD 1.2 Bn, supported by its massive shipbuilding base and high maritime traffic.

Asia Pacific emerged as the leading regional market in the Marine Oil Water Separator industry, accounting for 42.5% of the global market, equivalent to nearly USD 1.2 Bn. The region’s dominance is strongly linked to the concentration of global shipbuilding and vessel operations across China, South Korea, Japan, Singapore, and India. A major supporting factor is Asia’s leadership in global maritime trade, with UNCTAD highlighting that Asia handles 63% of global container trade, making it the busiest region for commercial vessel movement and bilge water generation.

Another major regional strength comes from ship construction and fleet expansion. Recent maritime trade data shows that China, the Republic of Korea, and Japan together delivered 93% of all new global ship tonnage, reinforcing Asia Pacific’s unmatched position in vessel manufacturing and retrofit demand. Since every newly built commercial vessel requires certified oily water separation systems under MARPOL discharge rules, shipyard-led installations continue to provide strong recurring demand.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Promac B.V. has built a solid reputation in marine and industrial separation technologies, particularly in oil-water treatment, centrifugal separation, and vessel fluid management systems. The company benefits from its European engineering base and project-driven delivery model, which supports demand from shipyards, tankers, and offshore service fleets. In competitive terms, Promac’s strength lies in 2-stage and 3-stage separator configurations, helping improve bilge treatment consistency under changing operating loads. Its market relevance is supported by increasing retrofit demand in Europe and Asia, where 15 ppm regulatory compliance and lower service intervals remain major buying priorities.

Sulzer Ltd stands out as a major global engineering company with strong capabilities in fluid separation, wastewater treatment, pumps, and marine process solutions. In 2023, the company reported CHF 3.3 billion in revenue and employed 13,130 people, reflecting its strong industrial scale and technical depth. For the marine oil water separator market, Sulzer benefits from its advanced Chemtech and flow equipment divisions, which support high-efficiency separation, static mixing, and filtration technologies. Its numerical strength in 180+ manufacturing and service locations worldwide further strengthens aftermarket and vessel retrofit opportunities.

Top Key Players Outlook

- Compass Water Solutions, Inc.

- Freytech Inc.

- Promac B.V.

- Sulzer Ltd

- Wartsila Oyj Abp

- Kanagawa Kiki Kogyo Co.,Ltd.

- Victor Marine Ltd

- SkimOIL Inc.

- Recovered Energy Inc

- HSN-KIKAI KOGYO CO., LTD.

- PS International, LLC

- GEA Group AG

Recent Industry Developments

Wärtsilä reported EUR 6,914 million in net sales in 2025, while total order intake reached EUR 8,102 million, showing strong marine systems demand across its wider portfolio.

Freytech’s strength lies in its ability to deliver up to 5 ppm separation for non-emulsified oils and as low as 0.1 ppm for emulsified oils, which is well aligned with modern marine discharge compliance requirements and premium vessel retrofit demand.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.0 Bn |

| Forecast Revenue (2035) | USD 5.0 Bn |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Gravity Oil Water Separator, Bioremediation Oil Water Separator, Electrochemical Oil Water Separator, Others), By Application ( Military, Shipping And Marine Industry, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Compass Water Solutions, Inc., Freytech Inc., Promac B.V., Sulzer Ltd, Wartsila Oyj Abp, Kanagawa Kiki Kogyo Co.,Ltd., Victor Marine Ltd, SkimOIL Inc., Recovered Energy Inc, HSN-KIKAI KOGYO CO., LTD., PS International, LLC, GEA Group AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |