Quick Navigation

Report Overview

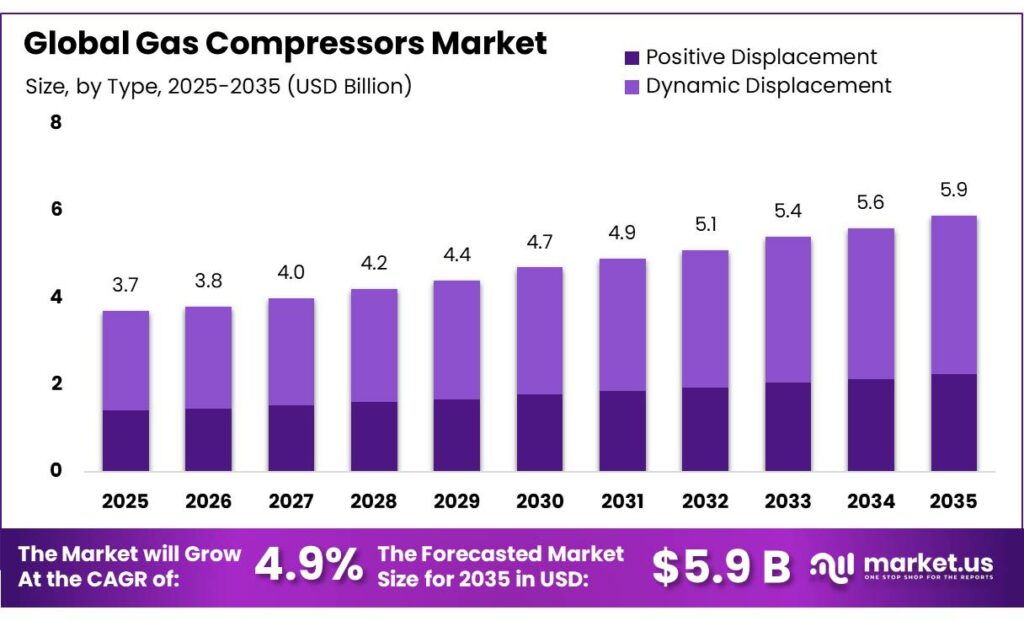

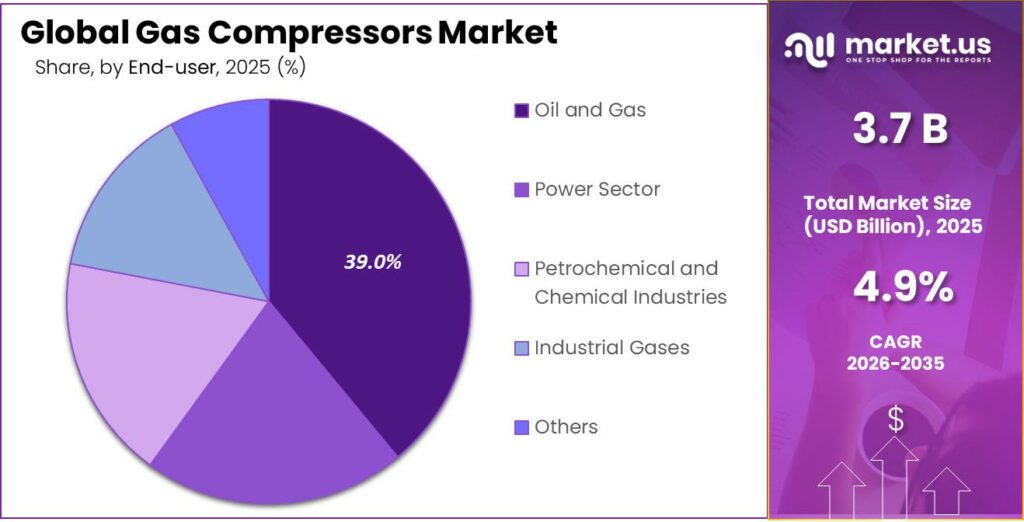

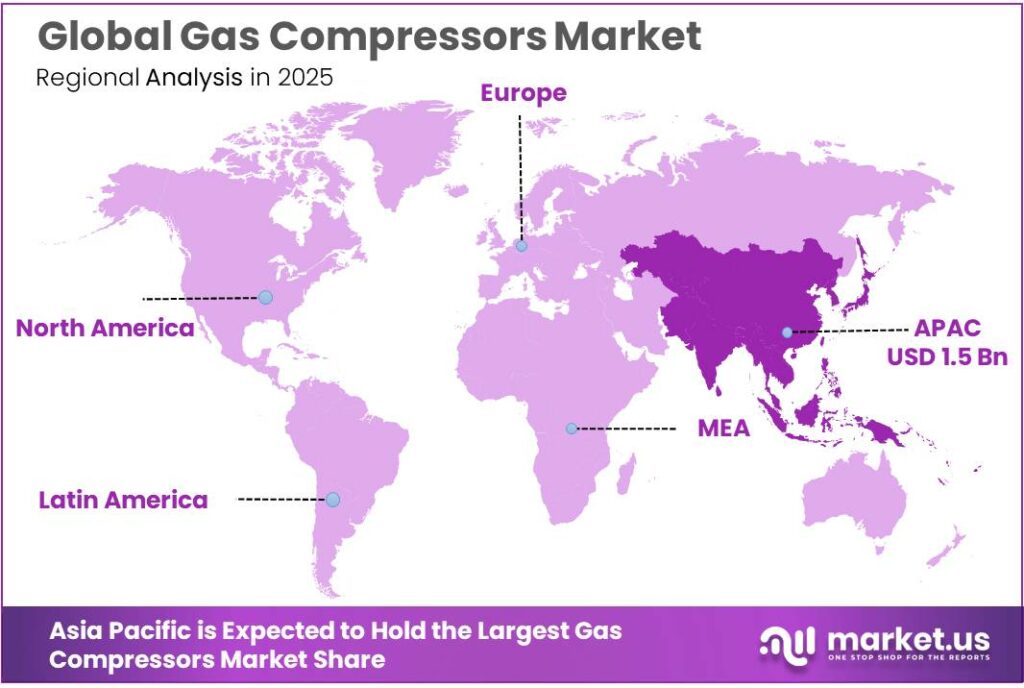

The Global Gas Compressors Market size is expected to be worth around USD 5.9 Billion by 2035, from USD 3.7 Billion in 2025, growing at a CAGR of 4.9% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 42.6% share, holding USD 1.5 Billion revenue.

Gas compressors form a critical utility layer across food and beverage manufacturing because they support refrigeration loops, controlled-atmosphere handling, pneumatic conveying, bottling, packaging, inert-gas blanketing, and plant air systems that must run continuously with high cleanliness and uptime. Their industrial relevance is reinforced by the scale of food processing itself.

- In the United States, food and beverage processing employed 1.7 million workers in 2021, equal to 15.4% of all U.S. manufacturing employment, according to USDA ERS. In Europe, the food and drink industry employs about 4.7 million people, generates roughly €1.2 trillion in turnover, and creates about €249 billion in value added, making it the EU’s largest manufacturing sector by turnover and employment. That operating scale directly underpins recurring demand for oil-free air compression, gas recovery, refrigeration compression, and associated condensate-treatment systems.

The industrial scenario remains favorable because food processors are balancing throughput expansion with stricter hygiene, energy, and emissions expectations. Eurostat reported that the EU produced 258 million tonnes of cereals, 162 million tonnes of raw milk, and 21 million tonnes of pigmeat in 2024; such volumes require reliable compression across storage, chilling, gas handling, and packaging infrastructure.

The main demand drivers are cost control, food safety, and environmental compliance. The U.S. Department of Energy states that compressed air systems consume around 90 billion kWh of electricity annually in the United States, which explains why food plants are prioritizing leak reduction, variable-speed systems, heat recovery, and cleaner compression architectures.

USDA’s Rural Energy for America Program also continues to support energy-efficiency upgrades for agricultural producers and rural small businesses, including processing-related equipment, strengthening the business case for modern compressor packages. On the refrigerant side, the EPA’s AIM Act framework is driving a long-term HFC phasedown of 85% by 2036, which is encouraging investment in new refrigeration and gas-management configurations across cold-chain and food processing assets.

- Government support remains material: the European Commission’s IF25 Hydrogen Auction carries a budget of €1.3 billion, and a third European Hydrogen Bank auction was planned for end-2025 with up to €1 billion, both of which improve visibility for future hydrogen compression, storage, and handling equipment demand.

Key Takeaways

- Gas Compressors Market size is expected to be worth around USD 5.9 Billion by 2035, from USD 3.7 Billion in 2025, growing at a CAGR of 4.9%.

- Dynamic Displacement held a dominant market position, capturing more than a 62.5% share.

- Oil and Gas held a dominant market position, capturing more than a 39.9% share.

- Asia Pacific held the dominant position in the Gas Compressors market, accounting for 42.6% of the global market and reaching nearly USD 1.5 Bn.

By Type Analysis

Dynamic Displacement dominates with 62.5% share, supported by its strong fit for continuous high-volume gas handling across industrial operations.

In 2025, Dynamic Displacement held a dominant market position, capturing more than a 62.5% share. This leadership was mainly supported by its wide use in large-scale industrial processes where steady gas flow, high operating efficiency, and reliable pressure control are critical. These compressors are commonly preferred in sectors such as oil and gas, chemicals, power generation, and manufacturing because they can handle continuous operations with lower vibration and smoother performance.

By End-user Analysis

Oil and Gas leads with 39.9% share, driven by continuous demand for gas compression in upstream, midstream, and downstream operations.

In 2025, Oil and Gas held a dominant market position, capturing more than a 39.9% share. This strong position was mainly supported by the sector’s constant need for gas compression across exploration, production, processing, and transportation activities. Gas compressors play a vital role in pressure boosting, gas gathering, pipeline transmission, gas lift operations, and refinery processes, making them essential equipment throughout the oil and gas value chain. The segment continued to see stable demand due to ongoing investments in natural gas infrastructure, LNG facilities, and cross-country pipeline networks.

Key Market Segments

By Type

- Positive Displacement

- Dynamic Displacement

By End-user

- Oil and Gas

- Power Sector

- Petrochemical and Chemical Industries

- Industrial Gases

- Others

Emerging Trends

Smart monitoring and predictive maintenance are becoming the biggest trend in gas compressors

One of the most important latest trends in the gas compressors market is the fast shift toward smart monitoring, IoT sensors, and predictive maintenance systems. Industries are no longer relying only on scheduled servicing. Instead, operators now use real-time vibration, temperature, pressure, and motor health data to predict failures before shutdowns happen.

This trend is becoming stronger because compressors are critical assets in pipelines, LNG terminals, refineries, and manufacturing plants where downtime directly impacts production. The International Energy Agency noted that industry represents nearly 40% of total global final energy consumption, which is pushing plants to use digital tools that reduce waste and improve equipment efficiency.

Government-backed efficiency policies are also supporting this trend. The IEA reported that over 250 new or updated energy-efficiency policies were introduced in 2025 across economies covering 85% of global energy demand. This is encouraging compressor users to adopt AI-enabled controls, remote diagnostics, and digital twins to improve lifecycle performance.

Energy-optimized compressor systems are trending with stricter industrial efficiency goals

Another clear latest trend is the growing demand for energy-optimized compressor packages with advanced motor controls and automation. As electricity costs rise and industries focus on emission reduction, buyers increasingly prefer systems with variable speed drives, automated load balancing, and digital efficiency dashboards. This is especially visible in gas transmission, LNG, and process industries where compressors operate continuously. According to the IEA, global energy efficiency progress improved to 1.8% in 2025 from 1% in 2024, showing stronger adoption of optimization technologies across industrial assets.

Drivers

Rising global natural gas consumption is creating strong compressor demand

One of the biggest driving factors for the gas compressors market is the steady rise in global natural gas consumption, especially from power generation and industrial use. As more countries shift from coal and oil toward cleaner-burning fuels, the need for compression systems in pipelines, storage terminals, LNG plants, and processing stations continues to increase. According to the International Energy Agency (IEA), global natural gas demand grew by 2.7% in 2024, adding nearly 115 billion cubic metres (bcm), while industry and power generation together contributed about 75% of this incremental demand.

Government-backed gas grid expansion programs in Asia and Europe, along with LNG import terminal additions, are further strengthening equipment demand. Countries such as India and China are investing heavily in city gas distribution and cross-country pipelines, making compression infrastructure a basic requirement. As gas becomes more important for energy security and lower-emission power generation, compressor demand is naturally rising alongside network expansion.

LNG infrastructure expansion and energy security projects are accelerating installations

Another major growth driver is the rapid expansion of LNG and gas transmission infrastructure under government energy security initiatives. New LNG export terminals, regasification units, and strategic pipeline corridors all require heavy-duty gas compressors for liquefaction, boil-off gas recovery, and transmission boosting. The IEA’s latest medium-term outlook highlights that the coming LNG supply wave is expected to reshape global gas trade through 2030, with multiple new projects being commissioned to improve affordability and supply resilience.

This is especially important because compressors are core equipment in LNG trains and large transmission stations. Public infrastructure spending, cross-border pipeline agreements, and national gasification missions are turning into direct equipment demand. For example, the IEA notes that India’s gas consumption growth is forecast to reach 7% in 2026, supported by city gas distribution expansion, rising industrial gas use, and increasing electricity needs.

Restraints

High energy consumption and operating cost remain a major restraint for gas compressors

One of the biggest restraining factors for the gas compressors market is the high electricity consumption involved in continuous industrial use. Gas compressors, especially in oil & gas pipelines, LNG terminals, petrochemical plants, and large manufacturing facilities, often run for long hours without interruption. This makes power cost a major burden for end users. According to the International Energy Agency (IEA), industry accounts for nearly 40% of total global final energy demand, making energy-intensive equipment one of the biggest cost centers in industrial operations.

This becomes a strong market restraint because many small and mid-sized industrial operators delay compressor upgrades or capacity expansion due to rising power tariffs and uncertain returns on investment. In energy-sensitive regions, users often continue operating older systems instead of replacing them with advanced compressor units, simply to avoid upfront and running expenses. Government energy-efficiency regulations are also becoming stricter, pushing industries to invest in monitoring, variable speed drives, and optimized motor systems, which raises the total ownership cost.

Efficiency compliance pressure is slowing replacement cycles in cost-sensitive industries

Another important restraint is the growing pressure to meet industrial efficiency standards and emission targets. Governments and trusted energy agencies are promoting better motor and equipment performance to cut wasteful electricity use. The IEA reported that more than 250 new or updated energy-efficiency policies were introduced in 2025 across countries representing 85% of global energy demand.

While these initiatives are positive in the long run, they can slow short-term market growth because buyers become more selective and project approvals take longer. Many industries now spend more time evaluating lifecycle energy savings before purchasing new compressors. In sectors such as chemicals, refining, and heavy manufacturing, management teams often postpone large capital spending until they can justify lower energy intensity and faster payback.

Opportunity

Hydrogen infrastructure expansion is opening a strong long-term growth path for gas compressors

One of the biggest growth opportunities for the gas compressors market is the fast expansion of hydrogen infrastructure. As countries invest in cleaner energy systems, hydrogen production plants, storage terminals, refueling stations, and pipeline injection networks all require advanced gas compression systems. Compressors are critical here because hydrogen must be handled at very high pressures for transport and storage.

According to the International Energy Agency, global hydrogen demand reached almost 100 million tonnes in 2024, showing a 2% annual increase, while more than 1,000 hydrogen policy measures have been introduced worldwide since 2020 to support infrastructure rollout.

This creates a direct equipment opportunity for compressor manufacturers, especially in high-pressure reciprocating and centrifugal systems. Government-backed hydrogen corridor projects in Europe and Asia are accelerating this trend. A strong example is Spain’s Enagás plan to invest EUR 3.13 billion in hydrogen infrastructure between 2025 and 2030, with hydrogen becoming the center of its future network strategy.

Cross-border hydrogen trade corridors and export hubs are creating new installation demand

Another major opportunity lies in the development of international hydrogen trade routes and export terminals. Long-distance hydrogen movement needs multi-stage compression at production hubs, storage nodes, and pipeline booster stations. The IEA notes that nearly 45% of low-emissions hydrogen from announced projects is intended for export, exceeding 16 Mtpa hydrogen equivalent by 2030 if projects move ahead.

Governments are supporting these projects through auctions, subsidies, and long-term clean fuel contracts, making the opportunity highly policy driven and more dependable. Europe’s H2Med corridor, Middle East export hubs, and Asia’s industrial hydrogen import plans are all creating demand for compressor packages designed for continuous high-pressure duty.

Regional Insights

Asia Pacific dominated the Gas Compressors market with a 42.6% share, valued at USD 1.5 Bn, supported by strong gas infrastructure growth and rising LNG demand across China, India, and Southeast Asia.

Asia Pacific held the dominant position in the Gas Compressors market, accounting for 42.6% of the global market and reaching nearly USD 1.5 Bn. The region’s leadership is strongly linked to rapid industrialization, large-scale natural gas infrastructure investments, and the continuous expansion of LNG import and regasification capacity.

The International Energy Agency noted that Asia Pacific gas demand is expected to increase by nearly 5% in 2026, accounting for around half of global gas demand growth, highlighting the region’s critical role in future gas movement infrastructure. Supportive regional momentum is also coming from LNG trade. Industry data indicates that Asia accounts for about 60% of global LNG imports, making the region the largest gas-consuming and gas-importing hub worldwide.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Acme Engineering & Manufacturing Corp. remains a notable player in industrial air movement and gas handling equipment, supported by its 80+ years of operating history and nearly 500,000 sq. ft. of manufacturing space. The company’s strength lies in engineered blowers, ventilation systems, and customized compressor-support airflow solutions used across industrial and commercial applications.

DongKun Industrial Co. Ltd. continues to strengthen its role in the Asian industrial equipment market through a growing portfolio of blowers and gas movement systems. The company is estimated to offer 20+ industrial blower and compressor-support models, targeting sectors such as chemicals, electronics, wastewater, and manufacturing. Its market competitiveness is supported by cost-effective engineering, export-oriented supply, and increasing adoption in Asia-Pacific industrial installations.

Continental Blower LLC has built a specialized position through its focus on centrifugal blowers and engineered air systems. The company has strong visibility across 3 major end-use sectors—wastewater, petrochemical, and manufacturing—where continuous gas flow and pressure stability are critical. Its specialization in custom blower engineering, retrofit upgrades, and performance optimization gives it a strong niche advantage.

Top Key Players Outlook

- Acme Engineering & Manufacturing Corp.

- Airmaster Fan Company Inc.

- Continental Blower LLC

- CG Power and Industrial Solutions Limited

- DongKun Industrial Co. Ltd.

- Flakt Woods Group SA

- Gardner Denver Inc.

- Greenheck Fan Corp.

- Howden Group Ltd

- Loren Cook Company

- Pollrich GmbH

Recent Industry Developments

DongKun’s export strength is another key numerical indicator, with 20+ years of exports to Japan and cumulative exports to the Middle East reported at over USD 300 million, showing strong acceptance in demanding industrial markets.

Acme Engineering & Manufacturing Corp. founded in 1938, brings nearly 88 years of engineering presence, which supports its credibility in oil & gas, process industries, petrochemical ventilation, and industrial gas handling applications. Its manufacturing strength remains notable with an estimated 500 employees and annual revenue ranging around USD 149.1 million, reflecting stable industrial demand across North America and export markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.7 Bn |

| Forecast Revenue (2035) | USD 5.9 Bn |

| CAGR (2026-2035) | 4.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Positive Displacement, Dynamic Displacement), By End-user (Oil and Gas, Power Sector, Petrochemical and Chemical Industries, Industrial Gases, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Acme Engineering & Manufacturing Corp., Airmaster Fan Company Inc., Continental Blower LLC, CG Power and Industrial Solutions Limited, DongKun Industrial Co. Ltd., Flakt Woods Group SA, Gardner Denver Inc., Greenheck Fan Corp., Howden Group Ltd, Loren Cook Company, Pollrich GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |