Quick Navigation

Report Overview

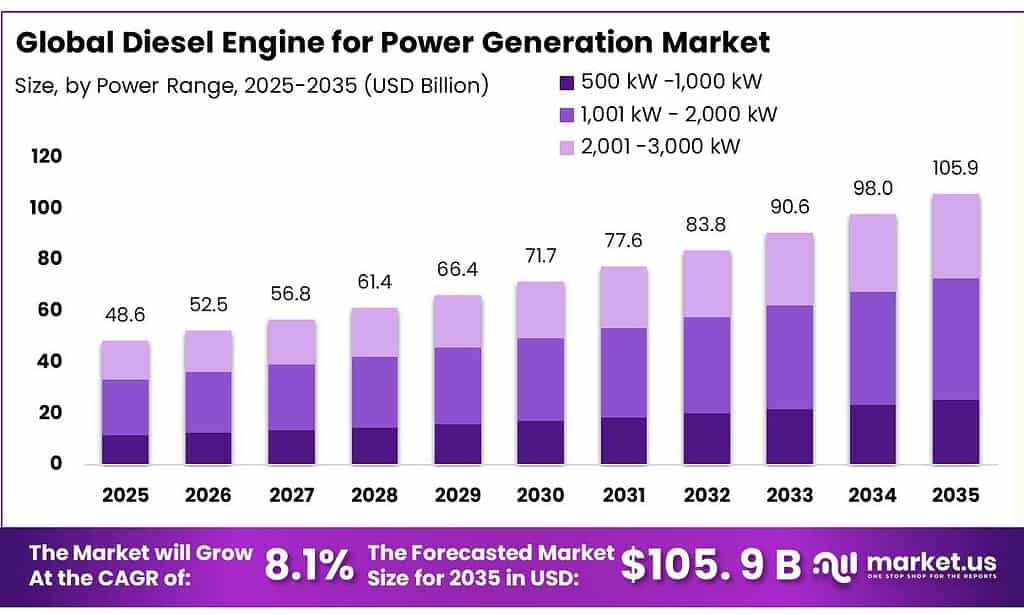

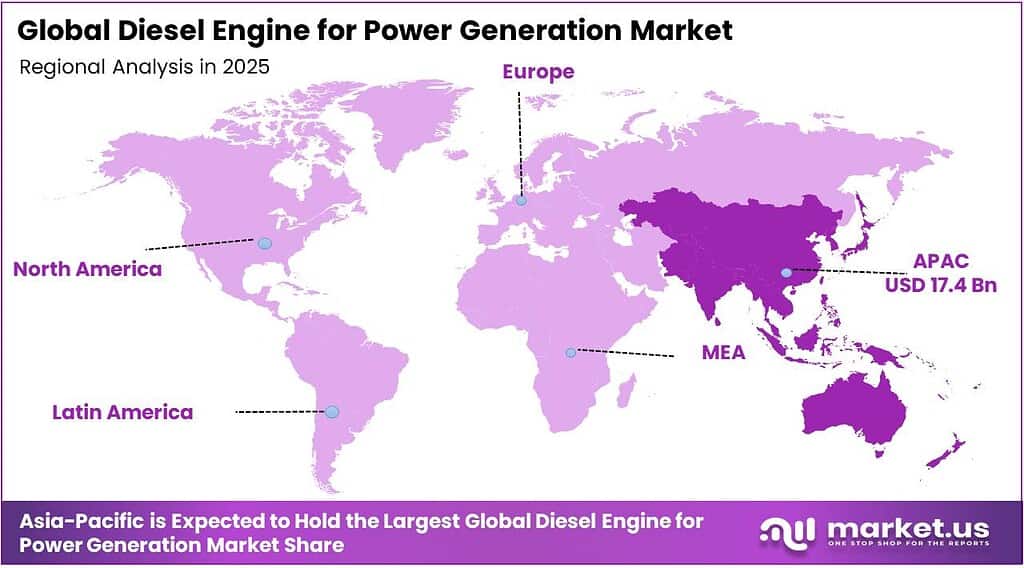

The Global Diesel Engine for Power Generation Market size is expected to be worth around USD 105.9 Billion by 2035, from USD 48.6 Billion in 2025, growing at a CAGR of 8.1% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 35.8% share, holding USD 17.4 Billion revenue.

A diesel engine for power generation, often called a diesel generator or genset, is a machine that combines a diesel internal combustion engine with an electrical alternator to produce electricity. The market is characterized by robust adoption in industrial and off-grid applications, with the Asia Pacific serving as the largest regional base due to extensive installation and production volumes.

- In Southeast Asia, electricity demand is projected by the International Energy Agency (IEA) to grow at 4% annually through 2035, significantly outpacing other regions. In countries such as Indonesia and Vietnam, major investments in oil and gas infrastructure and remote manufacturing clusters continue to necessitate high-capacity diesel prime movers.

Diesel engines are predominantly deployed for standby power, leveraging rapid start-up and high reliability to protect industrial facilities, data centers, and critical infrastructure from grid outages. Mid-capacity units are favored for their balance of output, fuel efficiency, and operational flexibility, meeting the needs of medium-to-large industrial plants without the complexity of larger engines.

Strategic deployment is concentrated in sectors with high operational continuity requirements, including manufacturing, mining, and telecom, where intermittent or weak grid connectivity necessitates reliable onsite generation.

Manufacturers emphasize low-emission technology, regulatory compliance, customized solutions, after-sales support, and localized production to enhance competitiveness. While prime or continuous power applications are limited due to higher operational costs, diesel engines remain integral for standby, off-grid, and remote operations, where reliability and rapid response are critical.

Key Takeaways

- The global diesel engine for power generation market was valued at USD 48.6 billion in 2025.

- The global diesel engine for power generation market is projected to grow at a CAGR of 8.1% and is estimated to reach USD 105.9 billion by 2035.

- On the basis of power range, 1,001kW-2,000kW diesel engines dominated the market, constituting 45.7% of the total market share.

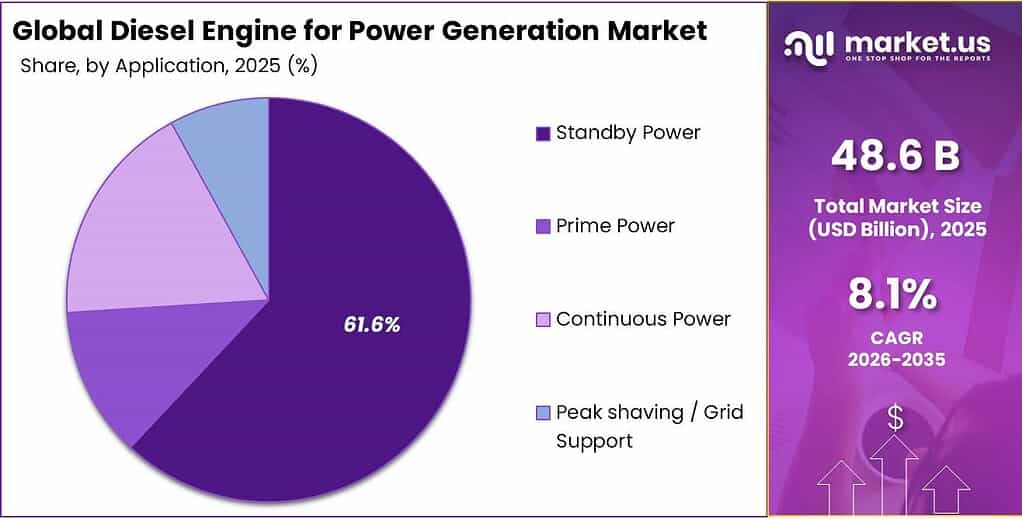

- Based on the applications, standby power led the market, comprising 61.6% of the total market.

- Among the end-uses, the industrial sector held a major share of the market, accounting for around 30.2% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the diesel engine for power generation market, accounting for 35.8% of the total global consumption.

Power Range Analysis

1,001 kW-2,000 kW Diesel Engines are a Prominent Segment in the Market.

The market is segmented based on the power range into 500 kW-1,000 kW, 1,001 kW-2,000 kW, and 2,001-3,000 kW. The 1,001 kW-2,000 kW diesel engine led the market, comprising 45.7% of the market share, as they offer an optimal balance between capacity, operational flexibility, and infrastructure compatibility. These engines provide sufficient output for medium-to-large industrial plants, commercial complexes, data centers, and telecom hubs, where continuous or backup power needs exceed the capabilities of 500 kW–1,000 kW units but do not justify the higher complexity and capital footprint of 2,001 kW–3,000 kW engines.

Operational efficiency is higher in this mid-capacity range due to favorable fuel consumption per kWh, simplified maintenance relative to larger units, and compatibility with standard switchgear and cooling systems. Additionally, deployment logistics, transportation, installation space, and grid interconnection are easier to manage than with the largest units, making 1,001 kW-2,000 kW engines the preferred choice for most off-grid, industrial, and critical infrastructure applications.

Application Analysis

Standby Power Dominated the Diesel Engine for Power Generation Market.

On the basis of application, the diesel engine for power generation market is segmented into standby power, prime power, continuous power, and peak shaving/grid support. The standby power dominated the diesel engine for power generation market, comprising 61.6% of the market share, due to their reliability, fast start-up, and ability to operate intermittently without efficiency losses. Standby applications, such as hospitals, data centers, telecom towers, and industrial facilities, require immediate backup during grid outages, which diesel engines can provide within seconds.

In contrast, prime or continuous power operation demands sustained fuel consumption and higher maintenance frequency, which increases operational costs and engine wear. Similarly, peak shaving or grid support requires frequent load cycling and long-duration operation, which can reduce engine life and efficiency. Diesel engines’ design and operational economics favor short-duration, high-reliability deployment, making them the most practical solution for emergency and standby scenarios, where uptime and rapid responsiveness are prioritized over continuous energy generation or cost optimization.

End-Use Analysis

Diesel Engines for Power Generation Are Mostly Used in Industrial Sectors.

Among the end-uses, 30.2% of the total global consumption of diesel engines for power generation is in industrial sectors, outperforming commercial, utilities, and captive power plants, telecom infrastructure, construction and infrastructure projects, and residential sectors, as industrial facilities demand reliable, high-capacity, and continuous backup power to prevent costly production downtime. Manufacturing plants, processing units, and refineries often operate in locations with intermittent grid reliability or high energy intensity, making diesel gensets essential for safeguarding operations.

In contrast, utilities and captive plants typically rely on larger centralized generation or grid supply, reducing the need for multiple diesel units. Telecom infrastructure and construction sites use smaller or temporary engines, while residential sectors rarely require high-capacity standby systems. The industrial sector benefits from engines that can handle heavy loads, maintain long operational hours, and integrate with existing infrastructure, making diesel engines the preferred solution for robust, site-specific, and high-demand applications where power continuity directly impacts operational performance.

Key Market Segments

By Power Range

- 500 kW-1,000 kW

- 1,001 kW-2,000 kW

- 2,001-3,000 kW

By Application

- Standby Power

- Prime Power

- Continuous Power

- Peak Shaving / Grid Support

By End-Use

- Industrial

- Manufacturing

- Mining

- Oil & gas

- Cement

- Metals

- Commercial

- Data Centers

- Healthcare Facilities

- Commercial Buildings

- Utilities and captive power plants

- Telecom infrastructure

- Construction and infrastructure projects

- Residential

Drivers

Infrastructure Development and Industrialization Drive the Diesel Engine for Power Generation Market.

Infrastructure expansion and industrialization exert measurable pressure on diesel engine demand for power generation, primarily through reliability gaps and off-grid requirements, particularly in manufacturing and data centers, which are driving high-capacity diesel generator demand for reliable, uninterrupted power. According to a report by the IEA, increased industrial electricity consumption, expected to grow 2-3% by 2026, alongside data center power demand projected to reach up to 12% by 2028, necessitates standby and prime power solutions.

The diesel-based captive generation in India reached 17,700 MW in March 2022, accounting for 21% of total captive capacity. This reflects sustained industrial reliance on self-generation, especially where grid quality is inconsistent. The Central Electricity Authority further records 250 million hours of annual outages, reinforcing the structural need for backup systems across infrastructure assets.

Moreover, construction sites and transport projects frequently lack grid connectivity. The diesel gensets provide prime and continuous power in remote or early-stage project phases. Similarly, medium-high capacity gensets are routinely deployed in data centers, healthcare, manufacturing, and commercial complexes, sectors expanding alongside urban infrastructure. These factors establish diesel engines as a functional complement to infrastructure growth rather than a substitute for grid expansion.

Restraints

Stringent Emission Regulations and Decarbonization Trends Might Hamper the Demand for the Diesel Engine for Power Generation.

Stringent emission regulations and global decarbonization initiatives represent significant structural challenges to the diesel engine market for power generation, forcing a transition toward advanced after-treatment and alternative fuel compatibility. Mandatory emission standards have progressively lowered the allowable limits for criteria pollutants, increasing the technical complexity and capital cost of diesel systems.

For instance, the EPA Tier 4 Final implemented by the U.S. Environmental Protection Agency requires a 90% reduction in Nitrogen Oxides (NOx) and a 95% reduction in Particulate Matter (PM) compared to Tier 3 levels. Similarly, the European Commission introduced Stage V regulations (2019/2021), which include a Particle Number (PN) count limit for engines between 19 kW and 560 kW, effectively mandating the use of Diesel Particulate Filters (DPFs) in addition to Selective Catalytic Reduction (SCR).

Furthermore, the Central Pollution Control Board mandates limits for gensets (75-800 kW) at less than 4.0g/kWh (NOx+HC) and less than 0.2g/kWh (PM), with uniform applicability across domestically manufactured and imported units. Subsequent CPCB IV+ standards, effective July 2023, require about 90% reductions in particulate matter and NOx relative to earlier norms, necessitating advanced after-treatment systems and redesign of engines. These regulatory thresholds and enforced emission reductions structurally challenge diesel-based power solutions by increasing technological complexity and limiting legacy fleet viability.

Opportunity

Off-Grid and Remote Operations Create Opportunities in the Diesel Engine for Power Generation Market.

Off-grid and remote operations represent a critical opportunity for the diesel engine market, particularly where grid extension is cost-prohibitive or technically unfeasible. These engines serve as the primary power source for decentralized industrial and community infrastructure. Energy access deficits remain quantitatively significant. The International Energy Agency reports 675 million people globally lack electricity access, concentrated in Asia and Africa, necessitating decentralized solutions. Diesel gensets are widely deployed as primary power sources in such off-grid settings, supporting residential loads, clinics, and small industries.

Remote mining and oil and gas operations are primary consumers of high-capacity diesel engines due to their energy density and load-following capabilities. Diesel units can accept full load in as little as 10 seconds and ramp from 25% to 100% load in 5 seconds, making them ideal for heavy industrial cycles. For instance, the Agnew Gold Mine in Australia utilizes a hybrid microgrid where diesel generators provide essential firming to maintain 100% uptime alongside renewable sources.

In the U.S., Caterpillar’s Tucson Proving Ground, located 8 miles from the nearest utility, requires approximately 11,000 hours of generator operation annually, consuming 250,000 gallons of diesel to support a peak load of 500 kW. The diesel engines provide rapid deployment, high load-following capability, and continuous operation in isolated microgrids, where grid extension is cost-prohibitive. These conditions establish off-grid environments as a durable application domain for diesel-based power generation.

Trends

Expansion in Telecom Infrastructure.

The expansion of telecommunications infrastructure, particularly in regions with unreliable grid connectivity, remains a primary driver for diesel engine adoption in power generation. Telecom tower operations exhibit consistent dependence on diesel-based generation. The deployment of Base Transceiver Stations (BTS) in remote areas necessitates autonomous power solutions. According to International Telecommunication Union (ITU) data, while mobile cellular coverage reaches 95% of the global population, a significant coverage gap persists in least developed countries, where rural connectivity requires off-grid power.

In these environments, diesel generators typically operate as the primary power source or in a hybrid configuration with renewable energy and battery storage to ensure 99.9% uptime. According to the Telecom Regulatory Authority of India, 400,000 towers, each consuming 3-4 kW, with diesel generators operating 8 hours daily, resulting in 8,760 liters of diesel per tower annually. This translates into sector-wide emissions of 10 million tons of CO₂, underscoring the scale of diesel utilization.

Expansion into rural and off-grid regions, supported by universal service obligations, requires decentralized, always-available power systems, where diesel gensets provide continuous and backup supply. These quantified deployment patterns establish telecom infrastructure as a persistent application segment for diesel-based power generation.

Geopolitical Impact Analysis

Geopolitical Tensions Have Led to Severe Disruptions in the Supply Chains of Diesel.

Geopolitical friction in the Middle East, especially the ongoing Israel-US-Iran conflict, has disrupted crude and refined product flows through the Strait of Hormuz, historically a conduit for 10-20% of global seaborne diesel supplies. Disruptions here have been linked to losses of 3-4 million barrels per day (bpd) of diesel supply and a further 500,000 bpd loss due to blocked refined fuel exports. This constitutes a measurable pressure on global distillate availability. Strategic export shifts and trade realignments have occurred due to Europe’s embargo on Russian diesel imports. The imports from Russia fell from 30 million tons to 2.9 million by 2024, shrinking a major regional supply route.

Amid these tensions, diesel futures in the U.S. rose by US$28 per barrel in Feb-Mar 2026, a faster increase than crude oil futures, which rose by US$16 per barrel. Sustained conflict could double retail diesel prices if chokepoints remain compromised.

In response to supply volatility, some countries pursue infrastructure adjustments. For instance, Hungary and Slovakia agreed to build a 127‑km fuel pipeline with capacity for 1.5 million tons of gasoline and diesel annually to reduce reliance on traditional routes affected by geopolitical friction.

Higher and volatile fuel prices, rooted in geopolitical conflict and supply chain realignments, directly affect operational expenditure for diesel generator users in industry, telecom, mining, and remote infrastructure, where grid access is limited. Shifts in diesel supply logistics force operators to adjust fuel procurement strategies, storage, and backup planning, with quantifiable impacts on inventories and procurement cycles. The geopolitical tensions have caused observable diesel supply disruptions, regional trade realignments, and measurable price volatility, which in turn affect fuel availability and cost structures critical to diesel engine‑based power generation.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Diesel Engine for Power Generation Market.

In 2025, the Asia Pacific dominated the global diesel engine for power generation market, holding about 35.8% of the total global consumption, underpinned by measurable installation and production. The region functions as the primary global hub for diesel engine power generation, driven by rapid industrialization, large-scale infrastructure expansion, and persistent grid reliability challenges in emerging economies.

For instance, the Ministry of Power in India reported a peak electricity demand of 250.1 GW in FY 2024-25, a 4.2% increase over the previous year. While the grid gap is narrowing, the demand for diesel gensets remains critical for industrial and commercial backup. Similarly, in China, total power consumption surpassed 10 trillion kWh for the first time in 2025, growing 5% year-over-year. Despite a massive shift toward renewables, which added 421 GW of capacity in 2024, the National Energy Administration (NEA) maintains fossil fuels as a top priority for system stabilization.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of diesel engines for power generation focus on operational and technological strategies to strengthen their market position. A primary activity is product innovation, including the development of low-emission and fuel-efficient engines to meet evolving regulatory standards and decarbonization mandates. They further emphasize customization for end-use sectors, such as telecom, industrial, and remote infrastructure, ensuring engines meet site-specific load requirements. After-sales service networks, including predictive maintenance, spare parts logistics, and warranty support, are expanded to reduce downtime and operational risk. Additionally, manufacturers invest in strategic partnerships and localized production, optimizing supply chains and securing fuel or component availability in high-demand regions.

The Major Players in The Industry

- AKSA Power Generation Company

- Atlas Copco AB

- Caterpillar Inc.

- Cummins Inc.

- Generac Power Systems, Inc.

- Kohler Co.

- Mitsubishi Heavy Industries, Ltd.

- Rolls-Royce plc (MTU Onsite Energy)

- Weichai Power Co., Ltd.

- Yanmar Holdings Co., Ltd.

- Other Key Players

Key Developments

- In November 2025, AKSA Power Generation Company acquired DeltaGen, a specialist provider of custom prime and standby diesel generators, to strengthen its engineering capabilities.

- In March 2026, Atlas Copco introduced the QHS Integrated Hybrid Generator range, combining diesel engines with battery technology to significantly reduce fuel consumption, emissions, and operating costs. Designed for rental applications, the system enables simplified operation, reduced maintenance, autonomous performance, and remote monitoring capabilities.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 48.6 Bn |

| Forecast Revenue (2035) | US$ 105.9 Bn |

| CAGR (2026-2035) | 8.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Power Range (500 kW-1,000 kW, 1,001 kW-2,000 kW, and 2,001-3,000 kW), By Application (Standby Power, Prime Power, Continuous Power, and Peak Shaving/Grid Support), By End-Use (Industrial, Commercial, Utilities and Captive Power Plants, Telecom Infrastructure, Construction and Infrastructure Projects, and Residential) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | AKSA Power Generation Company, Atlas Copco AB, Caterpillar Inc., Cummins Inc., Generac Power Systems, Inc., Kohler Co., Mitsubishi Heavy Industries, Ltd., Rolls-Royce plc (MTU Onsite Energy), Weichai Power Co., Ltd., Yanmar Holdings Co., Ltd., and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |