Quick Navigation

Report Overview

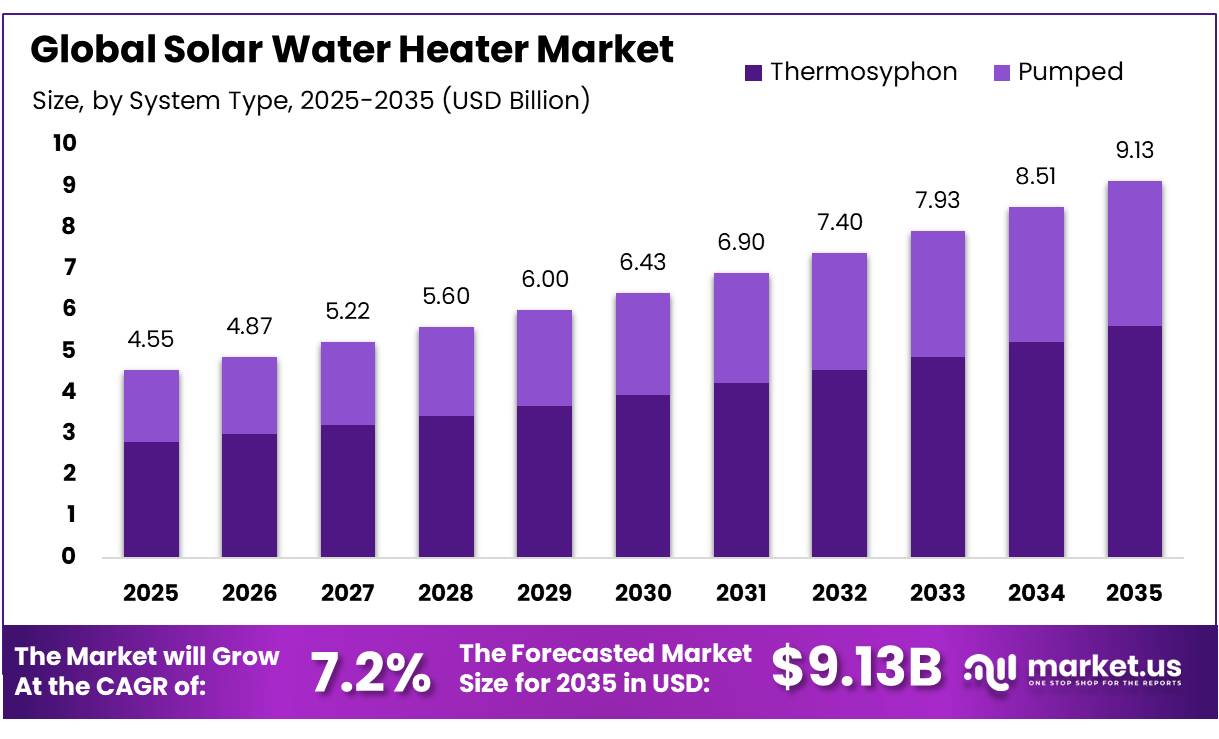

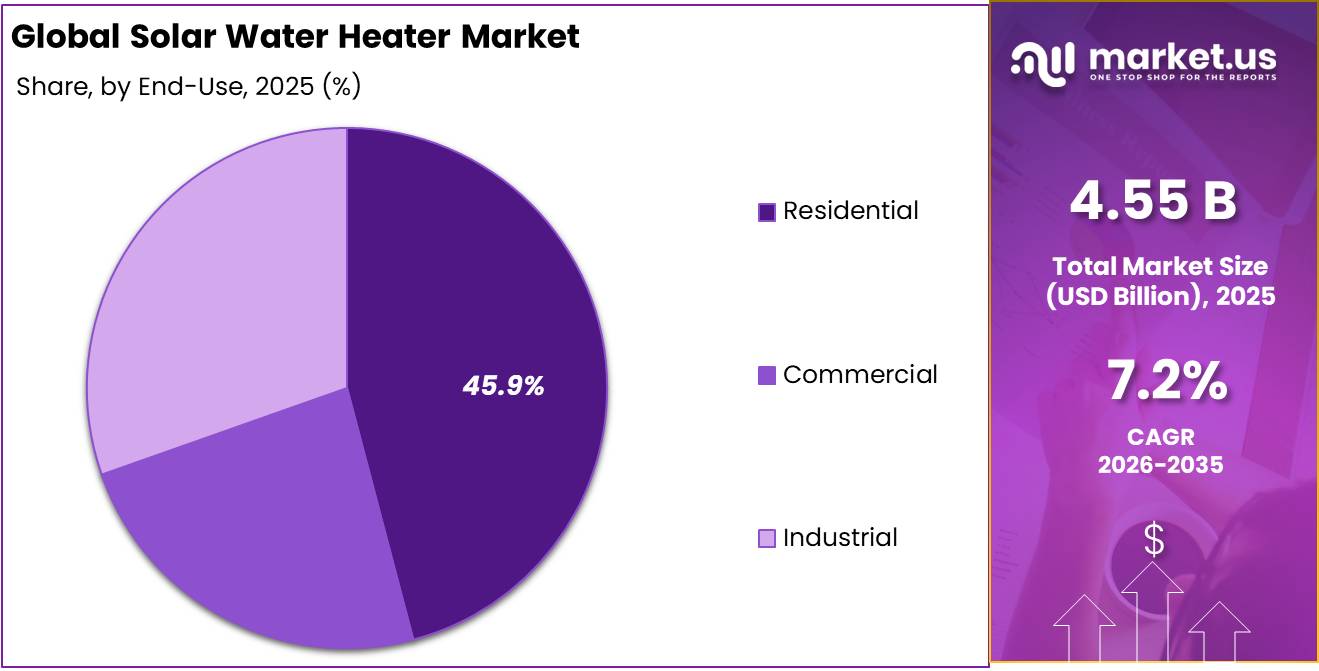

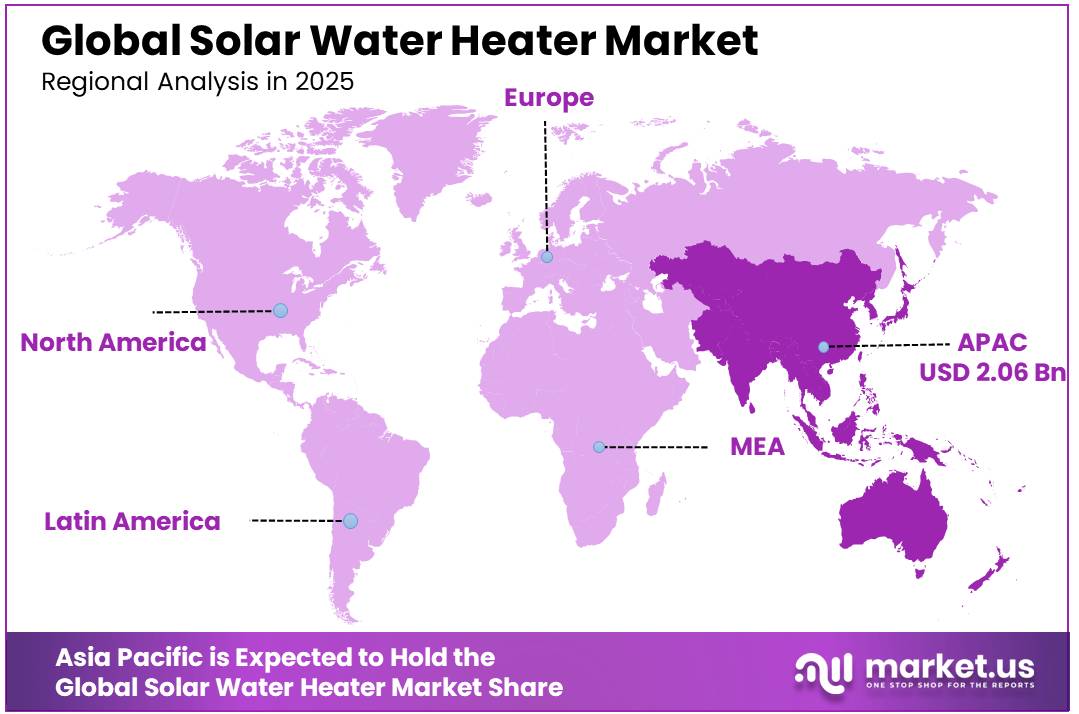

The Global Solar Water Heater Market size is expected to be worth around USD 9.13 Billion by 2035, from USD 4.5 Billion in 2025, growing at a CAGR of 7.2% during the forecast period from 2026 to 2035. In 2025, the Asia Pacific held a dominant market position, capturing more than a 34.4% share, holding USD 0.9 billion in revenue.

A solar water heater is a renewable energy system that captures thermal energy from sunlight to heat water for domestic, commercial, or industrial use. Unlike standard photovoltaic panels that generate electricity, solar water heaters use collectors to absorb heat directly and transfer it to a water supply or a heat-transfer fluid. The market is shaped by a combination of policy support, technological innovation, and user demand patterns.

Government initiatives such as capital subsidies, low-interest loans, and building bye-law mandates have lowered adoption barriers, while energy savings of 70-80% relative to electric heaters provide a strong economic incentive. The Asia Pacific region, led by China and India, dominates global deployment due to favorable solar insolation, large residential populations, and targeted renewable energy programs.

Technologically, evacuated tube collectors are preferred over flat plate or unglazed collectors for their higher efficiency, reduced heat loss, and adaptability to low ambient temperatures, while thermosyphon systems are favored over pumped systems for their simplicity, reliability, and lower maintenance requirements. Residential users dominate the market, with 300-600 liter systems most common, balancing hot water demand, rooftop space, and cost.

The International Energy Agency (IEA) projects that solar thermal technologies must be deployed in approximately 400 million dwellings by 2030 to align with the Net Zero Scenario. Emerging trends include smart, IoT-enabled SWHs, which enhance operational monitoring, efficiency, and predictive maintenance. However, challenges remain in high upfront costs, maintenance needs, and supply-chain sensitivities due to geopolitical factors, influencing material access and system deployment.

Key Takeaways

- The global solar water heater market was valued at USD 4.5 billion in 2025.

- The global solar water heater market is projected to grow at a CAGR of 7.2% and is estimated to reach USD 9.13 billion by 2035.

- On the basis of technology, the evacuated tube collector dominated the market, constituting 52.3% of the total market share.

- Based on the system type, the thermosyphon solar water heater dominated the market, with a substantial market share of around 61.5%.

- Based on the capacity, the solar water heaters with a capacity of 300-600 liters led the market, comprising 28.9% of the total market.

- Among the end-uses of solar water heaters, residential uses are the most considerable within the market, accounting for around 45.9% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the solar water heater market, accounting for 45.3% of the total global consumption.

Technology Analysis

Evacuated Tube Collector is a Prominent Segment in the Market

The market is segmented based on technologies into evacuated tube collectors, flat plate collectors, and unglazed water collectors. The evacuated tube collector led the market, comprising 52.3% of the market share, primarily due to higher thermal efficiency and lower heat losses, especially under variable climatic conditions.

Compared with unglazed collectors, typically suited for low-temperature applications such as swimming pools, ETCs can achieve higher water temperatures, often 60-80°C or more, required for domestic and institutional hot water use. Additionally, modular tube replacement reduces maintenance complexity, contributing to lifecycle practicality and wider adoption.

System Type Analysis

Thermosyphon Solar Water Heaters Dominated the Market

The market is segmented into thermosyphon and pumped. The thermosyphon solar water heaters dominated the market, comprising 61.5% of the market share, primarily due to their structural simplicity, lower installation cost, and operational reliability. These systems operate on natural convection.

As water in the collector heats, it becomes less dense and rises into the storage tank positioned above the collector, while cooler water flows downward. This passive circulation eliminates the need for pumps, controllers, sensors, or external power.

Pumped (forced-circulation) systems require electric pumps, control units, wiring, and differential temperature sensors, increasing capital cost and technical complexity. Although pumped systems offer design flexibility for large or multi-story buildings, thermosyphon systems remain dominant in small- to medium-scale applications due to their energy independence, ease of maintenance, and lower lifecycle risk.

Capacity Analysis

Solar Water Heaters with a Capacity of 300-600 Liters held a Major Share of the Market

Based on capacity, the solar water heater market is segmented into up to 300 liters, 300-600 liters, 600-900 liters, and above 900 liters. 36.2% of the solar water heaters consumed globally are of capacity 300-600 liters, as they align closely with the hot water requirements of medium-sized households, small apartment clusters, guest houses, and small commercial establishments.

Systems below 300 liters are generally suited to smaller households and may become insufficient where occupancy fluctuates or multiple bathrooms operate simultaneously. Conversely, 600-900 liter and above 900 liter systems are typically designed for institutional applications, such as hostels, hospitals, or hotels, where space availability, structural load-bearing capacity, and plumbing integration become more complex.

End-Use Analysis

Solar Water Heater Are Mostly Utilized by Residential Users

Among the end-users, 45.9% of the total global consumption of solar water heaters is by residential users, as their design and capacity closely match household hot water needs. Residential systems, often ranging from 100 to 600 liters, provide sufficient daily hot water for bathing, cooking, and cleaning without requiring complex infrastructure or high capital investment.

In contrast, commercial and industrial applications often demand very large volumes of hot water at higher temperatures, sometimes continuously, which requires either multiple high-capacity units, pumped circulation systems, or integration with backup heating sources.

Similarly, residential users benefit from simpler installation on rooftops, eligibility for government subsidies, and lower operational and maintenance requirements due to passive thermosyphon designs. Consequently, solar water heaters remain most accessible and widely adopted in the residential sector.

Key Market Segments

By Technology

- Evacuated Tube Collector

- Flat Plate Collector

- Unglazed Water Collector

By System Type

- Thermosyphon

- Pumped

By Capacity

- Up to 300 Liters

- 300-600 Liters

- 600-900 Liters

- Above 900 Liters

By End-Users

- Residential

- Commercial

- Industrial

Challenges

The solar thermal industry supported an estimated 318,000 jobs globally in 2023 across manufacturing, installation, and maintenance, but this workforce remains limited relative to an installed base of about 126 million solar thermal systems. The constraint is becoming more severe as the market shifts from simple residential thermosiphon units toward more complex systems such as pumped configurations, hybrid solar-plus-storage setups, district heating integration, and industrial heat applications, all of which require higher-level skills in hydraulics, controls, commissioning, and operations and maintenance.

Even a 3%–5% commissioning error rate can reduce annual yield by 8%–15% and increase service callbacks above 120 per 1,000 installations. This skill gap is estimated to create a -0.9 percentage point drag on market CAGR, driven by 2–6 week longer installation lead times, constrained expansion into tier-2 and tier-3 cities, and weaker referral-driven demand.

Addressing it requires standardized installer certification, modular pre-plumbed systems, remote diagnostics, higher per-partner training investment, and region-specific technical design libraries to scale capability over a 2–4 year horizon.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| China-Centric ETC Dependence | -1.2% | APAC core, MENA importers, LATAM volume markets | Medium term (2-4 years) |

| Installer Skill Bottleneck | -0.9% | India, Africa growth markets, EU retrofit zones, LATAM secondary cities | Medium term (2-4 years) |

| Policy-to-Project Lag Mismatch | -0.8% | EU regulatory hubs, district heat corridors, industrial heat clusters | Long term (≥ 4 years) |

| Heat Pump Substitution Pressure | -1.1% | Europe core, China urban markets, Australia, North America | Medium term (2-4 years) |

| Large-System Execution Complexity | -0.7% | EU district heating, China public infrastructure, industrial process heat markets | Long term (≥ 4 years) |

| Last-Mile Cost Volatility | -0.6% | Sub-Saharan Africa, island markets, remote LATAM, dispersed rural demand zones | Short term (≤ 2 years) |

Opportunity

Hotels, resorts, serviced apartments, and religious lodging facilities represent an underdeveloped retrofit opportunity because they combine high daily hot-water demand, large contiguous roof space, and rising sustainability disclosure pressure. However, solar water heating is still largely deployed on a project-by-project basis rather than through structured, networked retrofit programs.

A cluster-based approach, such as franchise-level procurement, city-wide retrofit bundles, and performance-guarantee contracts, creates a distinct scaling lever beyond general energy-price inflation. In India, tourism-heavy Southern Europe, and MENA, this model can reduce customer acquisition costs by 25%–40%, cut design and procurement overhead by 15%–20%, and compress payback periods to 3–5 years for high-occupancy properties.

When deployed through hotel chains or pilgrimage corridors, it can increase average deal sizes by 4x–10x, achieve service attach rates above 50%, and generate an estimated +1.4 percentage point uplift to CAGR through 2030.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| ESCO heat-as-a-service | +1.8% | EU, India, MENA, LatAm | Short term |

| Hospitality retrofit clusters | +1.4% | South Europe, India, SEA, MENA | Short term |

| Industrial low-temp hot water | +2.2% | China, India, the EU, and Mexico | Medium term |

| Smart hybrid SWH + HP systems | +1.6% | EU, Japan, South Korea, urban China | Medium term |

| Multifamily and district hot-water loops | +2.0% | EU, China, Gulf, dense Asian cities | Medium term |

| Roll-up of fragmented installers | +1.3% | India, Africa, LatAm, South Europe | Long term |

Drivers

Lower-cost thermosyphon and evacuated tube collector (ETC) supply chains are a key driver of solar water heating adoption because residential systems are relatively standardized and highly price sensitive. According to IEA SHC 2026 market analysis, a typical 150 litre, 2 m² thermosyphon system costs about USD 250–500 in India, around USD 250–1,000 in China, and generally USD 1,000–1,500 in Europe, with even higher prices in Australia and parts of Africa.

China remains the dominant global production and export hub for ETC-based systems, while India has a strong domestic manufacturing base, with solar water heaters accounting for 97% of India’s installed solar thermal capacity and cumulative solar thermal deployment exceeding 20 million m² as of December 2023. This cost differential is important because regions such as Latin America, Africa, and MENA combine strong solar irradiation with limited consumer financing depth, meaning lower-cost thermosyphon kits can unlock first-time ownership, especially where direct systems are sufficient, and freeze protection is not required.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Building decarbonization mandates lifting solar heat compliance demand | +1.4% | China core, EU/Mediterranean, India urban states, MENA spill-over | Medium term (2-4 years) |

| High retail power tariffs are improving household payback economics | +1.2% | India urban clusters, South Africa, Latin America, islands/MENA, Southern Europe | Short term (≤ 2 years) |

| Rooftop hot-water substitution where DHW is 25%+ of home energy load | +1.0% | APAC corridors, Sub-Saharan Africa, Latin America, Mediterranean Europe | Medium term (2-4 years) |

| Public housing, hospitality, and institutional procurement scaling volumes | +0.9% | India, Brazil, Mexico, Sub-Saharan Africa, MENA, and island markets | Medium term (2-4 years) |

| Lower-cost thermosyphon, ETC supply chains are widening affordability | +0.8% | China export corridors, India, Latin America, Africa, MENA | Short term (≤ 2 years) |

| Smart controls, PV-hot-water hybridization, and product reliability upgrades are expanding use cases | +0.7% | China, Australia, South Africa, Europe, and India are premium urban markets | Long term (≥ 4 years) |

Restraints

Lower-cost thermosyphon and evacuated tube collector (ETC) supply chains are a key driver of solar water heating adoption because residential systems are relatively standardized and highly price sensitive. According to IEA SHC 2026 market analysis, a typical 150 litre, 2 m² thermosyphon system costs about USD 250–500 in India, around USD 250–1,000 in China, and generally USD 1,000–1,500 in Europe, with even higher prices in Australia and parts of Africa.

China remains the dominant global production and export hub for ETC-based systems, while India has a strong domestic manufacturing base, with solar water heaters accounting for 97% of India’s installed solar thermal capacity and cumulative solar thermal deployment exceeding 20 million m² as of December 2023.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heat pump & PV substitution | -2.4% | EU core, North America, urban China, ANZ | Medium term (2-4 years) |

| China real-estate slowdown | -1.9% | China’s core, East Asia supply chain | Short term (≤ 2 years) |

| High upfront cost & rates | -1.7% | EU, North America, India metros, LATAM cities | Short term (≤ 2 years) |

| Metal cost & tariff pressure | -1.3% | North America, EU import markets, APAC export corridors | Short term (≤ 2 years) |

| Subsidy/policy discontinuity | -1.2% | EU, India states, MENA tenders, Africa programs | Medium term (2-4 years) |

| Installer quality & project complexity | -0.9% | Emerging APAC, Africa, LATAM, mixed EU retrofit markets | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Tensions Have Led to Increased Prices of Solar Water Heaters

The geopolitical tensions are affecting renewable energy supply chains in ways that extend to the broader solar ecosystem, including solar thermal technologies such as solar water heaters, by exposing material and trade dependencies and prompting policy responses.

A study by the International Renewable Energy Agency (IRENA) highlights that the global renewable energy transition is increasingly resource-intensive, with concentrated production and processing of critical materials creating geopolitical vulnerabilities that could disrupt supply chains for renewable technologies. These dependencies differ from traditional fossil fuel risks but carry analogous disruption potential when concentrated geographically or politically.

The major trade measures, such as the United States imposing preliminary countervailing duties of around 126% on certain Indian solar imports, reflect that international trade tensions can reshape access to clean energy technologies and inputs. Such tariffs are instituted on grounds of subsidy concerns, potentially affecting cross-border flows of essential solar components that share supply linkages with broader solar value chains.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Solar Water Heater Market

In 2025, the Asia Pacific dominated the global solar water heater market, holding about 45.3% of the total global consumption. According to the Solar Heat Worldwide dataset coordinated under the International Energy Agency Solar Heating & Cooling Programme, China alone accounted for about 73% of cumulative worldwide solar thermal installed capacity by the end of 2023, with significant annual additions. This dominance places the Asia Pacific at the forefront of global solar thermal utilization.

National policy support in the region, such as China’s longstanding solar thermal deployment programs and India’s renewable energy initiatives, reinforces this concentration of installed systems. The ample solar insolation and large residential and commercial hot-water demand across the Asia Pacific enhance the suitability for solar water heating technologies relative to other regions. The primary technology and deployments underscore Asia Pacific’s leadership in solar water heater adoption worldwide.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of solar water heaters focus on technology differentiation, quality compliance, cost optimization, and channel expansion to strengthen competitiveness. The focus is on product innovation, including higher-efficiency collectors, improved insulation to reduce thermal losses, and corrosion-resistant storage tanks for hard-water conditions.

Several firms invest in R&D and testing certifications, such as compliance with national standards and quality control orders, to enhance reliability and eligibility for government-linked procurement or subsidy programs. Moreover, manufacturers emphasize localized sourcing and backward integration to reduce input cost volatility and improve supply stability.

Strategic partnerships with housing developers, institutional buyers, and public agencies support volume deployment. Additionally, companies increasingly integrate digital monitoring features and smart controllers to differentiate offerings and improve lifecycle performance transparency, strengthening brand positioning in institutional and urban residential segments.

The Major Players in The Industry

- O. Smith Corporation

- Bradford White Corporation

- Eurostar Solar

- Himin Solar Energy Group

- Rheem Manufacturing Company

- Ariston Holding N.V.

- V-Guard Industries Ltd.

- SunEarth Inc.

- Solahart Industries

- Orb Energy

- SUNPAD, GREENoneTEC Solarindustrie GmbH

- Alternate Energy Technologies LLC

- Rinnai Corporation

- Jiangsu Sunpower Solar Technology Co., Ltd.

- Jiangsu Sunrain Solar Energy Co., Ltd.

- Apparent

- Other Key Players

Key Development

- In November 2025, Apparent, a recognized leader in innovative energy solutions, announced the launch of its DC-powered solar water heater. The company stated that the system redefines a conventional household appliance as a private, value-generating energy asset, designed to deliver measurable financial returns daily.

- In May 2025, Lennox, a prominent innovator in climate solutions within the HVACR industry, and Ariston Group, a global leader in sustainable climate and water comfort, formed a joint venture. The collaboration aims to introduce a competitive range of residential water heaters to homeowners in the United States and Canada.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.55 Bn |

| Forecast Revenue (2035) | USD 9.13 Bn |

| CAGR (2026-2035) | 7.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology Type (Evacuated Tube Collector, Flat Plate Collector, Unglazed Water Collector), By System Type (Thermosyphon, Pumped), By Capacity (Up to 300 Liters, 300–600 Liters, 600–900 Liters, Above 900 Liters), By End-use (Residential, Commercial, Industrial) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | O. Smith Corporation, Bradford White Corporation, Eurostar Solar, Himin Solar Energy Group, Rheem Manufacturing Company, Ariston Holding N.V., V-Guard Industries LTD, SunEarth Inc., Solahart Industries, Orb Energy, SUNPAD, GREENoneTEC Solar, Alternate Energy Technologies, Rinnai Corporation, Jiangsu Sunpower Solar Tech, Jiangsu Sunrain Solar Energy, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |