Quick Navigation

Report Overview

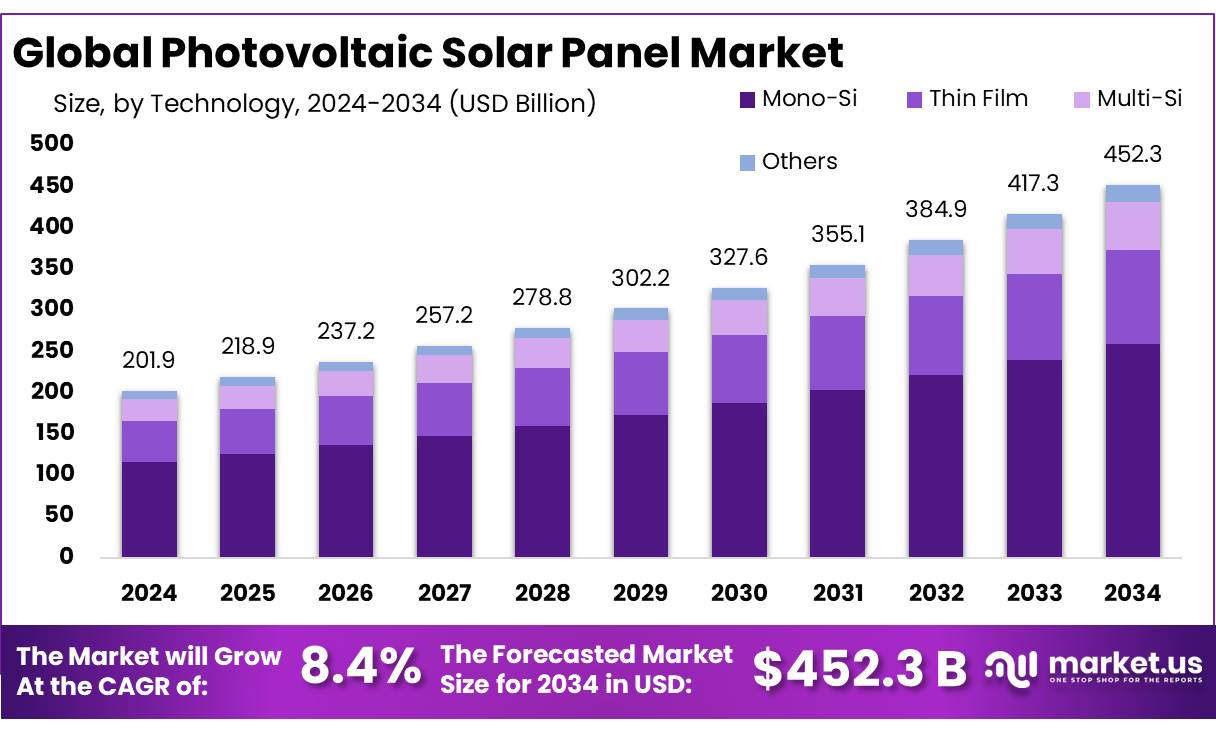

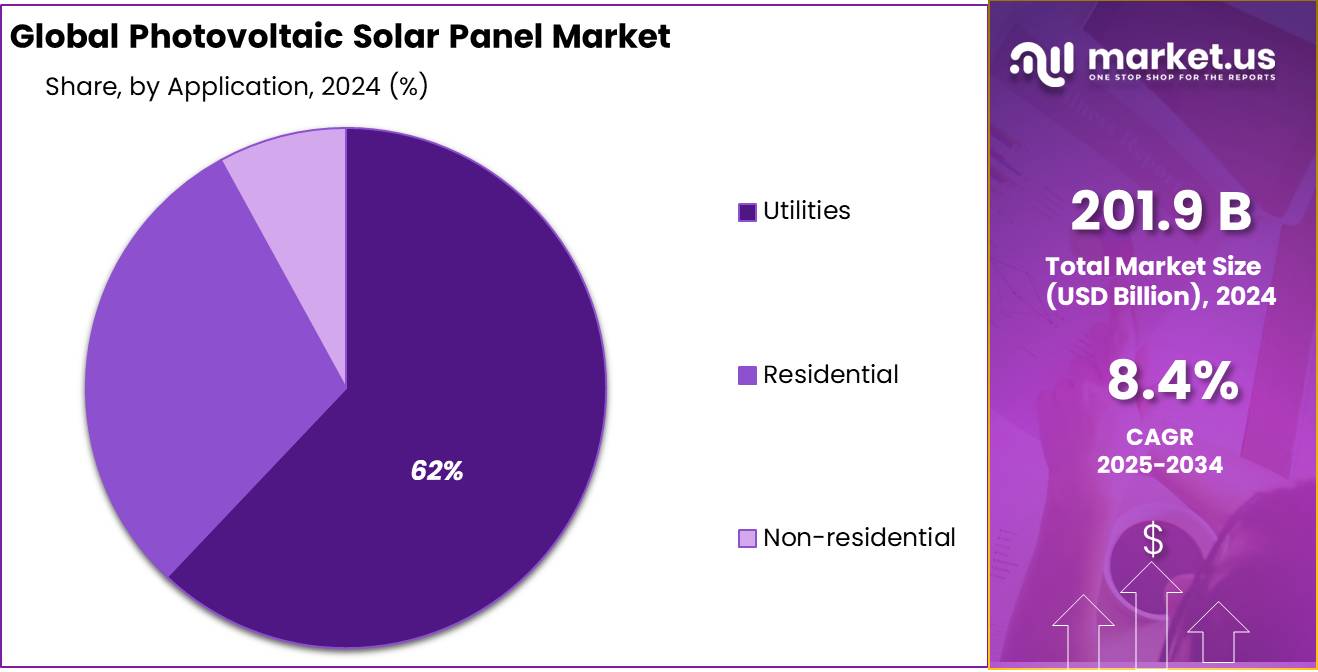

The Global Photovoltaic Solar Panel Market size is expected to be worth around USD 452.3 Billion by 2034, from USD 201.9 Billion in 2024, growing at a CAGR of 8.4% during the forecast period from 2025 to 2034.

The photovoltaic (PV) solar panel industry in India has experienced significant growth, driven by supportive government policies, technological advancements, and increasing demand for clean energy. As of April 2025, India’s total installed solar power capacity reached approximately 107.94 GW, comprising 82.39 GW from ground-mounted plants and 17.69 GW from grid-connected rooftop systems.

Reliance Industries plans to commence operations at its solar PV module factory in 2025, aiming to scale up production to 20 GW per year, which would position it as a major global player outside China. Similarly, Insolation Energy Ltd (INA Solar) reported a consolidated revenue of ₹1,333.76 crore for the fiscal year 2024-25, marking an 81% increase from the previous year, and plans to expand its module capacity to 8 GW by FY 2025-27.

Government initiatives have been pivotal in driving this expansion. The Pradhan Mantri Surya Ghar Muft Bijli Yojana, launched in February 2024, aims to provide rooftop solar installations to 1 crore households, offering 300 units of free electricity monthly and subsidies up to ₹78,000 for systems up to 3 kW. Additionally, the PM-KUSUM scheme supports farmers by subsidizing solar-powered irrigation pumps, with the government covering up to 60% of the installation cost.

To support these targets, several schemes have been implemented. The Pradhan Mantri Surya Ghar Muft Bijli Yojana, launched in February 2024, aims to provide rooftop solar systems to 10 million households, offering up to 300 units of free electricity per month and subsidies up to ₹78,000 for systems up to 3 kW. Additionally, the PM-KUSUM scheme focuses on solarizing agricultural pumps, providing a 60% subsidy to farmers for installing solar irrigation pumps, thereby reducing reliance on diesel and enhancing farmers’ income.

Key Takeaways

- Photovoltaic Solar Panel Market size is expected to be worth around USD 452.3 Billion by 2034, from USD 201.9 Billion in 2024, growing at a CAGR of 8.4%.

- Mono-Si (Monocrystalline Silicon) held a dominant market position, capturing more than a 57.4% share.

- Ground Mounted installations held a dominant market position, capturing more than a 67.1% share.

- On-grid systems held a dominant market position, capturing more than an 84.6% share of the global photovoltaic solar panel market.

- Utilities held a dominant market position, capturing more than a 62.2% share of the global photovoltaic solar panel market.

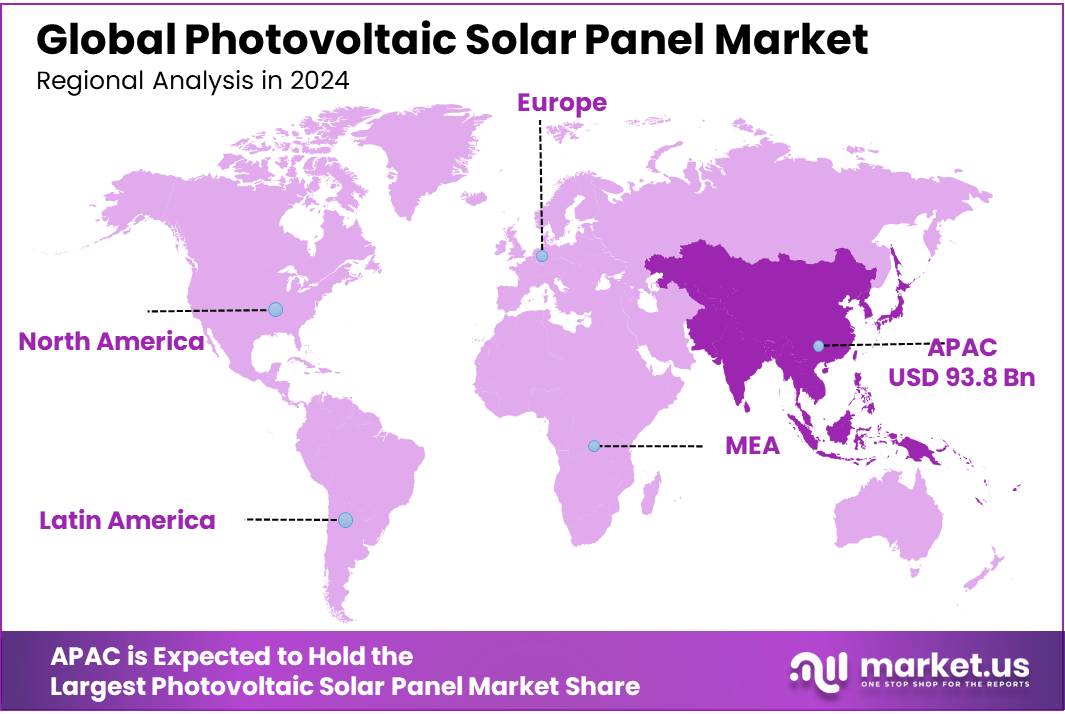

- Asia-Pacific (APAC) region held a commanding position in the global photovoltaic (PV) solar panel market, capturing approximately 46.5% of the market share, equating to a valuation of around USD 93.8 billion.

By Technology

Mono-Si commands 57.4% share in 2024, driven by high efficiency and growing rooftop adoption

In 2024, Mono-Si (Monocrystalline Silicon) held a dominant market position, capturing more than a 57.4% share of the global photovoltaic solar panel market. This strong lead was mainly supported by the superior energy conversion efficiency of Mono-Si panels, which typically range between 18% and 22%, making them a preferred choice for residential rooftop and commercial installations where space is limited. The sleek black appearance and compact footprint of Mono-Si modules have also enhanced their appeal among homeowners and businesses seeking both performance and aesthetics.

By Installation

Ground Mounted systems lead with 67.1% share in 2024, backed by utility-scale solar project expansion

In 2024, Ground Mounted installations held a dominant market position, capturing more than a 67.1% share of the global photovoltaic solar panel market. This segment continued to grow steadily due to the large-scale adoption of utility-grade solar farms, particularly in regions with vast open land and high solar irradiance. These systems are often favored for their scalability, ease of maintenance, and cost-efficiency in high-capacity installations, which are critical for national renewable energy goals.

By Grid Type

On-grid solar leads with 84.6% share in 2024, fueled by rising grid connectivity and government-backed incentives

In 2024, On-grid systems held a dominant market position, capturing more than an 84.6% share of the global photovoltaic solar panel market. This overwhelming preference for grid-tied installations was largely driven by their seamless integration with national power supply systems, allowing excess electricity to be fed back into the grid and monetized through net metering policies. Utility-scale solar farms, commercial rooftops, and urban residential installations have increasingly shifted toward on-grid models due to better financial returns and policy support.

By Application

Utilities dominate with 62.2% share in 2024, supported by large-scale solar power generation and national energy targets

In 2024, Utilities held a dominant market position, capturing more than a 62.2% share of the global photovoltaic solar panel market by application. This strong position was driven by the rapid expansion of utility-scale solar power plants that are designed to feed electricity directly into the national grid. These large installations typically span hundreds of acres and are backed by long-term power purchase agreements (PPAs) with government or private utilities, ensuring stable demand and steady returns.

Key Market Segments

By Technology

- Mono-Si

- Thin Film

- Multi-Si

- Others

By Installation

- Ground Mounted

- Roof Mounted

- Others

By Grid Type

- On-grid

- Off-grid

By Application

- Utilities

- Residential

- Non-residential

Drivers

Government Initiatives Fueling Solar Panel Market Growth

One of the primary drivers behind the rapid expansion of the photovoltaic (PV) solar panel market is the proactive role of government initiatives aimed at promoting renewable energy adoption. These policies not only provide financial incentives but also create an enabling environment for both consumers and investors to embrace solar energy solutions.

In India, the government’s commitment to renewable energy is evident through various schemes and programs. As of April 2025, the country achieved a cumulative solar power installed capacity of approximately 107.95 GW, with ground-mounted solar plants contributing 82.39 GW and grid-connected rooftop systems accounting for 17.69 GW. This significant growth reflects the impact of supportive policies and initiatives.

The Pradhan Mantri Surya Ghar Muft Bijli Yojana, launched in 2024, exemplifies the government’s efforts to encourage rooftop solar adoption. With a budget allocation of ₹75,021 crore, the scheme aims to provide free electricity up to 300 units per month to one crore households through rooftop solar installations. Such initiatives not only reduce the financial burden on consumers but also contribute to the overall increase in solar capacity.

Additionally, the PM-KUSUM scheme focuses on promoting solar energy in the agricultural sector. By offering subsidies up to 60% for farmers to install solar-powered irrigation pumps, the program aims to reduce reliance on diesel and enhance agricultural productivity. This initiative not only supports the farming community but also contributes to the broader goal of expanding solar energy usage across various sectors.

Restraints

Land Acquisition Challenges Impeding Solar Panel Market Growth

One of the significant challenges facing the photovoltaic (PV) solar panel market is the difficulty in acquiring suitable land for large-scale solar projects. In densely populated countries like India, land is a scarce and valuable resource, leading to conflicts between the need for renewable energy infrastructure and existing land uses.

For instance, in Nandgaon, western India, Tata Power’s 100-megawatt solar project encountered substantial opposition from local farmers. These farmers, who have cultivated the state-owned land for generations, perceived the solar plant as a corporate encroachment on their livelihoods. Protests and hunger strikes ensued, prompting the Maharashtra forest department to temporarily halt the project. This situation underscores the complexities of balancing green energy development with local community interests.

Moreover, the sheer scale of land required for utility-scale solar power plants presents a logistical hurdle. It is estimated that approximately 1 square kilometer of land is needed for every 40–60 megawatts of solar power generated. This demand for land often competes with agricultural, residential, and ecological needs, leading to further complications in project implementation.

To address these challenges, innovative solutions like agrivoltaics—where solar panels are installed above agricultural fields—are being explored. This approach allows for simultaneous land use for energy generation and agriculture, potentially mitigating land use conflicts. However, the widespread adoption of such solutions requires supportive policies, financial incentives, and community engagement to ensure successful implementation.

Opportunity

A Sustainable Growth Opportunity for India’s Solar Market

One of the most promising growth avenues for India’s photovoltaic (PV) solar panel market lies in agrivoltaics—the dual use of land for both solar energy generation and agriculture. This innovative approach addresses the critical challenge of land scarcity by allowing solar panels to be installed above crops, enabling simultaneous farming and energy production.

A recent study highlights the immense potential of agrivoltaics in India, estimating a capacity of up to 3,200 gigawatts (GWp). States like Punjab, Haryana, and Rajasthan alone account for significant portions of this potential, with 871 GWp, 700 GWp, and 592 GWp respectively . This dual-use model not only optimizes land utilization but also offers farmers an additional revenue stream, enhancing rural livelihoods.

Agrivoltaic systems provide several benefits: they shield crops from excessive sunlight and heat, reduce water evaporation, and can improve crop yields in certain conditions. Moreover, by integrating solar panels into agricultural settings, the need for large-scale land acquisition for standalone solar farms is mitigated, reducing potential conflicts with local communities.

The Indian government recognizes the potential of agrivoltaics and is supporting its adoption through various initiatives. For instance, the Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan (PM-KUSUM) scheme encourages farmers to install solar pumps and panels on their lands, promoting decentralized solar energy generation. Such programs not only contribute to the nation’s renewable energy targets but also empower farmers by reducing their dependence on grid electricity and diesel generators.

Trends

Artificial Intelligence Enhances Solar Panel Efficiency and Grid Integration

A notable trend in the photovoltaic (PV) solar panel market is the integration of Artificial Intelligence (AI) to optimize energy generation and grid management. AI algorithms analyze vast datasets, including weather patterns, sunlight intensity, and panel performance, to accurately forecast energy output. This predictive capability allows for real-time adjustments, reducing downtime and enhancing overall system efficiency.

In 2024, the U.S. solar industry installed nearly 50 gigawatts (GW) of direct current (DC) capacity, marking a 21% increase from the previous year. This growth underscores the importance of advanced technologies like AI in managing the complexities of large-scale solar deployments.

Government initiatives further support this trend. The Inflation Reduction Act (IRA) in the United States provides incentives for adopting clean energy technologies, including AI-driven solutions. These policies aim to accelerate the transition to renewable energy sources and enhance grid resilience.

Globally, the International Energy Agency (IEA) projects that solar PV will become the largest renewable energy source by 2029, accounting for 80% of the growth in global renewable capacity between 2024 and 2030. The adoption of AI technologies is expected to play a crucial role in achieving this milestone by improving the efficiency and reliability of solar energy systems.

Regional Analysis

In 2024, the Asia-Pacific (APAC) region held a commanding position in the global photovoltaic (PV) solar panel market, capturing approximately 46.5% of the market share, equating to a valuation of around USD 93.8 billion. This dominance is primarily driven by substantial investments in solar infrastructure, supportive government policies, and the region’s commitment to renewable energy adoption.

Technological advancements and declining costs of solar components have further accelerated the adoption of PV systems across the region. Countries like Japan, South Korea, and Australia have also made significant strides, integrating solar energy into their national grids and promoting residential and commercial installations. For instance, Australia’s solar PV installations surpassed 37.8 GW by September 2024, highlighting the country’s rapid uptake of solar technology.

Government initiatives have played a pivotal role in this growth trajectory. Policies offering subsidies, tax incentives, and favorable regulatory frameworks have created an enabling environment for both domestic and foreign investments in the solar sector. Moreover, the region’s focus on reducing carbon emissions and enhancing energy security aligns with global sustainability goals, further propelling the PV market’s expansion.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Abengoa, a Spanish multinational, has been a pioneer in solar energy, particularly in Concentrated Solar Power (CSP). The company has developed several CSP plants globally, including the Solana Generating Station in the U.S. and the Atacama 1 project in Chile. Despite facing financial restructuring, Abengoa’s technological advancements in thermal energy storage and solar field design have contributed significantly to the solar industry’s growth.

Acciona Energía, based in Spain, is a leading renewable energy company with a strong presence in solar PV. As of June 2024, the company reported a total installed capacity of 13,944 MW across various renewable technologies, including solar PV. Acciona continues to expand its solar portfolio, with recent projects like the 412 MWp solar plant in India, demonstrating its commitment to global renewable energy development.

Canadian Solar, a global solar energy company, reported $1.5 billion in revenue for Q4 2024, with a gross margin of 14.3%. The company has a diversified portfolio, including solar module manufacturing and project development. Canadian Solar’s total global solar development pipeline reached 25 GWp by the end of 2024, reflecting its significant role in the solar PV market.

Top Key Players in the Market

- Abengoa

- AccionaEnergia S.A

- BrightSource Energy, Inc.

- Canadian Solar Inc.

- eSolar Inc.

- First Solar

- GCL-SI

- Hanwha Q-CELLS

- JA Solar

- JinkoSolar

- LONGi Solar

- Nextera Energy Sources LLC

- Risen Energy

- SunPower Corporation

- Tata PowerSolar Systems Ltd.

- Trina Solar

- Vivaan Solar

- Waaree Group

- Wuxi Suntech Power Co. Ltd

- Yingli Solar

Recent Developments

In 2024, Acciona Energía solidified its position in the photovoltaic solar panel market by expanding its global footprint and enhancing its renewable energy portfolio. The company achieved a record revenue of €19.19 billion, marking a 12.7% increase from the previous year, with a net profit of €422 million .

In 2024, Abengoa continued to play a significant role in the photovoltaic solar panel market through its engineering, procurement, and construction (EPC) services. Notably, the company developed the Atacama 1 Solar PV Park in Chile, a 100 MW project comprising 392,000 modules over 300 hectares, supplying clean energy to approximately 110,000 households and offsetting 400,000 tons of CO2 annually.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 201.9 Bn |

| Forecast Revenue (2034) | USD 452.3 Bn |

| CAGR (2025-2034) | 8.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Mono-Si, Thin Film, Multi-Si, Others), By Installation (Ground Mounted, Roof Mounted, Others), By Grid Type (On-grid, Off-grid), By Application (Utilities, Residential, Non-residential) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Abengoa, AccionaEnergia S.A, BrightSource Energy, Inc., Canadian Solar Inc., eSolar Inc., First Solar, GCL-SI, Hanwha Q-CELLS, JA Solar, JinkoSolar, LONGi Solar, Nextera Energy Sources LLC, Risen Energy, SunPower Corporation, Tata PowerSolar Systems Ltd., Trina Solar, Vivaan Solar, Waaree Group, Wuxi Suntech Power Co. Ltd, Yingli Solar |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |